Automotive Split-View Camera Module Market Size by Lens Type, Resolution, Camera View, Sensor Type, Vehicle Type, Technology, Sales Channel

Overview

Global Automotive Split-View Camera Module Market Introduction

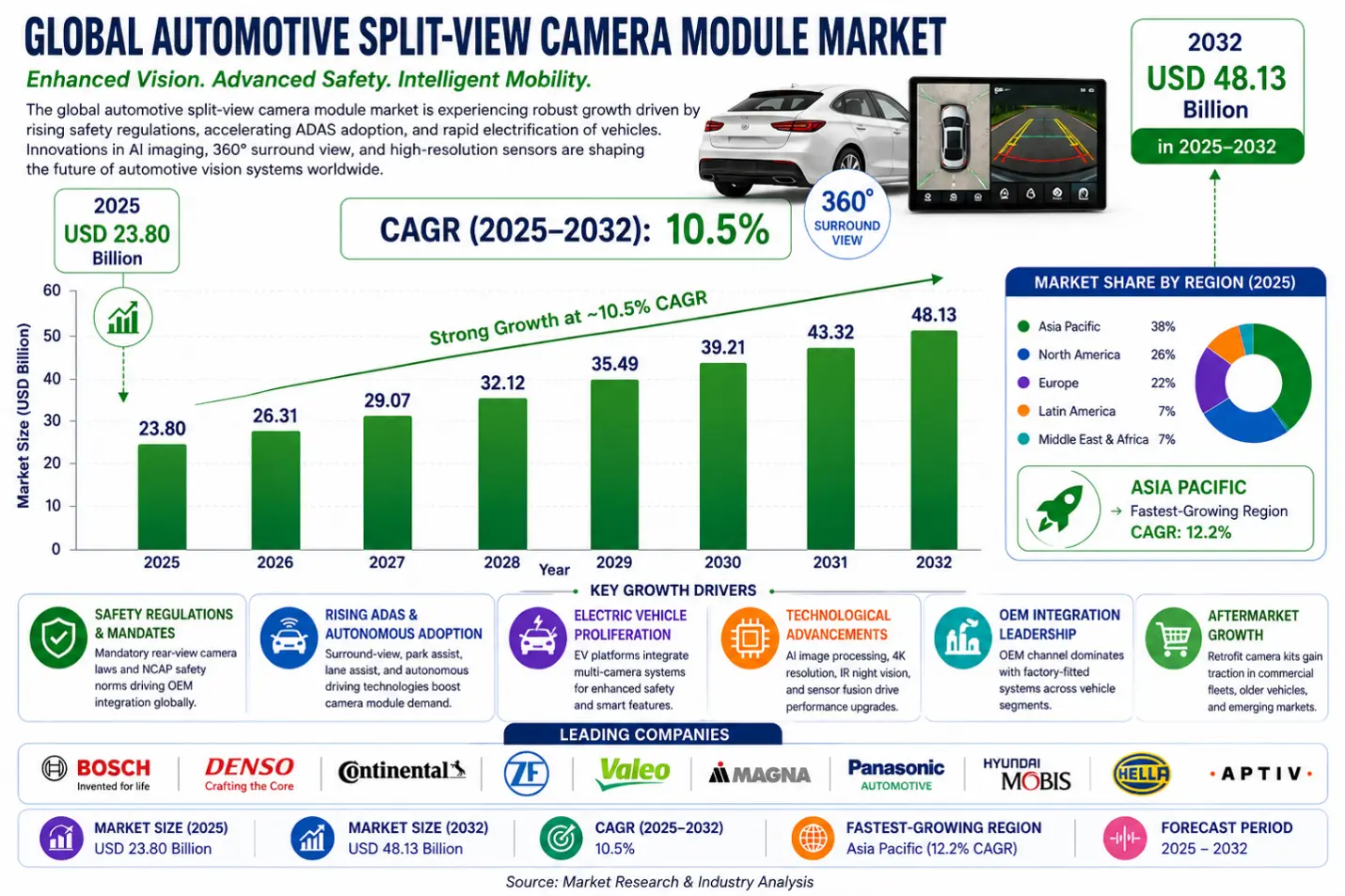

The Global Automotive Split-View Camera Module Market is undergoing one of the most transformative shifts seen in the automotive safety and intelligent mobility ecosystem in the last decade. What initially emerged as a regulatory-driven rear-view camera solution has evolved into a sophisticated multi-camera imaging architecture supporting ADAS, autonomous driving, and next-generation driver monitoring systems. In 2025, the market was valued at USD 23.80 billion, and by 2032 it is forecast to reach USD 48.13 billion, expanding at a CAGR of approximately 10.5%. This upward trajectory reflects the accelerating integration of artificial intelligence, high-resolution imaging, and real-time environmental sensing into modern vehicle platforms, fundamentally redefining automotive safety, navigation precision, and driver assistance capabilities worldwide.

Automotive Split-View Camera Module Market Key Highlights

The Automotive Split-View Camera Module Market is projected to grow from USD 23.80 Bn (2025) to USD 48.13 Bn by 2032, at a ~10.5% CAGR, driven by mandatory vehicle safety regulations, accelerating ADAS penetration, and rapid electrification of global automotive platforms.

Asia Pacific leads as the fastest-growing region, with China, Japan, South Korea, and India emerging as high-volume manufacturing and adoption hubs, while North America and Europe dominate premium ADAS-integrated camera system deployment.

Multi-camera surround-view systems and dual-lens configurations are rapidly replacing traditional single-camera solutions, supported by rising consumer demand for 360-degree situational awareness and semi-autonomous driving functionality.

OEM integration remains the dominant sales channel, while aftermarket retrofit demand is accelerating across commercial fleets, passenger vehicles, and emerging economies due to increasing affordability of advanced driver visibility solutions.

Innovation and AI convergence trends are reshaping the market, with growing adoption of 4K ultra-HD imaging, infrared night vision, AI-powered object detection, sensor fusion with radar and LiDAR, and autonomous parking assistance technologies.

To know about the Research Methodology :- Request Free Sample Report

Automotive Split-View Camera Module Market Key Drivers

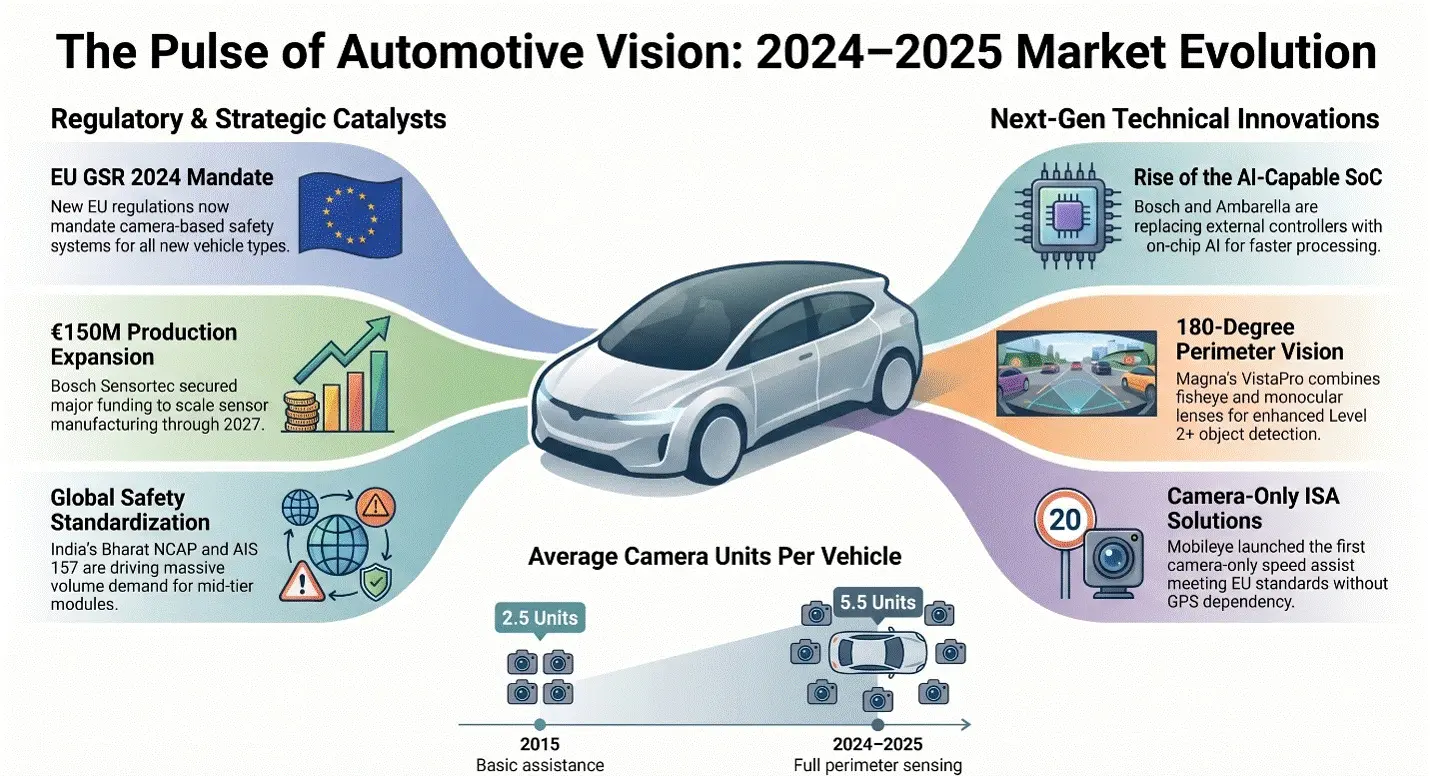

The Automotive Split-View Camera Module Market Growth is primarily fuelled by the global expansion of mandatory rear-view camera regulations — most notably the U.S. NHTSA rear-view camera rule (fully effective since 2018), Euro NCAP safety protocol updates, and similar mandates across Japan, South Korea, and Australia — which have structurally embedded camera modules into new vehicle production baselines. The accelerating deployment of Advanced Driver Assistance Systems (ADAS) across passenger and commercial vehicle platforms is generating sustained multi-camera demand, as split-view, surround-view, and blind-spot monitoring systems increasingly operate as integrated optical networks rather than standalone peripherals. Close to 60% of new vehicle models launched globally now incorporate split-view camera systems as standard or optional equipment, confirming the pivotal role of these modules in modern automotive safety architectures.

Beyond regulatory compliance, consumer demand for parking assistance, lane-change support, trailer-hitch alignment, and 360-degree surround visibility is driving premium camera module integration across SUVs, crossovers, and pickup trucks — the fastest-growing vehicle segments globally. The rapid growth of the electric vehicle (EV) segment further amplifies demand, as EVs require a greater density of cameras and sensors relative to conventional internal combustion engine vehicles, given their autonomous-readiness architecture and the absence of traditional powertrain noise for spatial orientation. The Automotive Split-View Camera Module Industry is also benefiting from significant cost reductions in CMOS image sensor manufacturing, advanced ISP (image signal processing) chip miniaturization, and the declining per-unit price of wide-angle optical lens assemblies — collectively lowering the bill-of-materials cost and enabling mid-segment vehicle integration at scale.

Automotive Split-View Camera Module Market Restraints

Despite strong structural growth, the Automotive Split-View Camera Module Market faces challenges related to the complexity and cost of multi-camera sensor fusion integration, particularly as OEMs demand seamless interoperability between split-view camera feeds, radar sensors, ultrasonic arrays, and LiDAR inputs within unified ADAS domain controllers. High-resolution camera modules — especially Full HD (1080p) and Ultra HD (4K) systems with night-vision and thermal imaging capabilities — carry significant per-unit hardware costs that can limit adoption in entry-level vehicle segments and price-sensitive emerging markets. Supply chain vulnerabilities in semiconductor components, particularly image sensor chips (primarily manufactured in Taiwan and South Korea), have exposed automotive OEMs to significant production disruption risks, as demonstrated during the 2021–2023 global chip shortage period that constrained vehicle output and delayed ADAS feature rollout programs.

Automotive Split-View Camera Module Market Growth is also constrained by the technical challenges of maintaining consistent optical performance across extreme operating temperatures, weather conditions (fog, heavy rain, direct solar glare), and high-vibration environments, requiring extensive validation and qualification cycles that extend product development timelines and increase engineering cost. Data privacy concerns surrounding always-on camera systems in vehicles — particularly related to the inadvertent capture of pedestrian and third-party imagery — are beginning to attract regulatory attention in the European Union and several U.S. states, creating potential compliance uncertainty for OEMs and Tier 1 suppliers developing next-generation connected camera platforms.

Automotive Split-View Camera Module Market Opportunities

The Automotive Split-View Camera Module Market Opportunities are expanding significantly with the emergence of AI-embedded camera systems capable of real-time object classification, pedestrian detection, lane-marking recognition, and predictive hazard alerting — transforming split-view modules from passive imaging peripherals into active safety intelligence nodes within vehicle ADAS architectures. The rapid global rollout of SAE Level 2 and Level 2+ autonomous driving systems by leading OEMs (Tesla, General Motors Super Cruise, Mercedes-Benz Drive Pilot, Stellantis, BMW) is generating sustained premium camera module demand across multiple vehicle lines simultaneously.

Furthermore, the commercial vehicle segment — encompassing long-haul trucks, delivery vans, buses, and construction equipment — represents a structurally underserved opportunity, as regulatory mandates for side-object detection, trailer coupling assistance, and blind-spot elimination in heavy transport are beginning to accelerate fleet-wide camera integration programs across North America, the EU, and increasingly across Southeast Asian logistics markets.

Emerging opportunities include the integration of camera-based electronic mirror replacement systems (CMS — Camera Monitor Systems) enabled by EU Regulation No. 46 (effective 2016) and gradually adopted across premium commercial and passenger vehicles, offering superior aerodynamic efficiency and wider field-of-view performance versus conventional glass mirrors. The integration of QR-enabled vehicle health monitoring, OTA (over-the-air) firmware updates for camera ISPs, and cloud-connected fleet telematics platforms powered by split-view camera data streams is creating new recurring revenue and data monetization opportunities for Tier 1 camera system suppliers — driving the Automotive Split-View Camera Module Market Forecast toward sustained premium margin expansion.

Emerging Trends Shaping the Automotive Split-View Camera Module Industry

The Automotive Split-View Camera Module Market Trends indicate a powerful shift toward AI-native camera architectures where embedded neural processing units (NPUs) within image signal processors enable real-time semantic segmentation, object tracking, and depth estimation — all previously requiring dedicated compute hardware external to the camera module itself. The adoption of high dynamic range (HDR) CMOS sensors capable of simultaneously resolving deep shadow and bright highlight detail in a single frame is becoming standard across premium ADAS camera modules, addressing one of the most critical real-world failure modes of early-generation systems: overexposed image washout in direct sunlight or underexposed failure in nighttime urban environments.

Another significant trend is the development of multi-spectral camera modules integrating standard visible-light imaging with near-infrared (NIR) and thermal sensing capabilities in a single compact form factor — enabling consistent object detection performance across all-weather and all-lighting conditions without requiring redundant sensor hardware. The increasing adoption of MIPI CSI-2 and GMSL2 (Gigabit Multimedia Serial Link 2) high-bandwidth camera interfaces is enabling automotive-grade streaming of 4K split-view feeds from multiple simultaneous camera channels into centralized ADAS domain controllers without signal latency or compression artifacts — a critical requirement for Level 2+ and Level 3 autonomous driving validation. The Automotive Split-View Camera Module Industry Outlook is further shaped by the rapid adoption of fisheye ultra-wide-angle optics (180–220-degree field of view) and the integration of electronic image stabilization (EIS) for camera systems mounted in high-vibration commercial vehicle and off-road applications.

Automotive Split-View Camera Module Market — Manufacturing Cost & Pricing Analysis

Optical & Hardware Component Cost Analysis

The optical and hardware component segment represents the largest share of manufacturing cost in the Automotive Split-View Camera Module Market, primarily driven by sourcing of automotive-grade CMOS image sensors, precision-ground aspheric glass lens elements, IR-cut filter assemblies, and weatherproof camera housing modules that meet AEC-Q100 Grade 1 or Grade 2 automotive reliability qualification standards.

• Premium wide-angle lens assemblies for surround-view and split-view applications (typically 180–220-degree fisheye configurations) incorporate multi-element aspherical glass optics, requiring specialized grinding, polishing, and coating processes that increase per-unit optical costs by 40–60% versus standard automotive rear-view lens configurations.

• CMOS image sensor cost structures are heavily influenced by wafer fabrication node (28nm–45nm BSI CMOS processes), pixel pitch dimensions (sub-3-micron for HD/FHD sensors), and automotive-grade qualification requirements (AEC-Q100, ISO 26262 ASIL-B/C functional safety certification), all of which add significant engineering and testing overhead versus consumer-grade equivalents.

• Pricing for complete camera module assemblies typically ranges from USD 18–35 per unit for standard HD single-lens rear-view modules, USD 45–90 for Full HD wide-angle front/side split-view modules, and USD 120–250 for AI-integrated 4K surround-view multi-camera system nodes — reflecting significant performance and integration complexity premiums across tiers.

• OEMs with vertically integrated optical and sensor supply chains (e.g., Sony, Samsung Electro-Mechanics, LG Innotek) or those with preferred-supplier agreements with Aptina/ON Semiconductor achieve superior camera module BOM cost management relative to competitors relying on spot-market sensor procurement.

ISP & Embedded Processing Cost Analysis

The image signal processor (ISP) and embedded compute component represents the second-largest cost driver in the Automotive Split-View Camera Module Industry, characterized by the integration of automotive-grade ISP SoCs (Renesas R-Car, NXP i.MX, Texas Instruments TDA series, Ambarella CV series), hardware security modules (HSMs), and LPDDR4X/5 memory subsystems within compact module footprints that must meet ASIL-B or ASIL-C functional safety integrity levels.

• AI-embedded ISPs capable of on-module neural inference (pedestrian classification, lane detection, object tracking) command a 2.5–4x cost premium over standard ISP solutions, but eliminate the need for a separate external ADAS compute board — net system-level cost savings of 15–25% at the platform level are achievable through module-level AI integration.

• Thermal management engineering for high-performance ISP modules operating in enclosed vehicle environments (dashboard, door mirror, A-pillar) represents a significant NRE cost and ongoing per-unit cost element, particularly in markets with extreme ambient temperature requirements (Middle East, South Asian summer, Scandinavian winter).

• GMSL2 and FPD-Link III automotive serializer/deserializer ICs add USD 4–12 per camera channel to BOM costs but enable 15-meter+ coaxial cable runs with sufficient bandwidth for 4K/60fps streaming and bidirectional control data — making them essential for cameras integrated into exterior mirror housings, tailgates, and front grille positions.

Finished Product Manufacturers (Total System Cost)

The total cost structure in the Automotive Split-View Camera Module Market includes optical assembly, CMOS sensor integration, ISP/SoC processing, housing and weatherproofing (IP69K rating for exterior-mounted units), harness/connector integration, EOL testing (optical alignment, image quality, thermal cycling, vibration), and OEM program qualification costs across IATF 16949-compliant manufacturing processes.

• The final OEM supply price is typically 35–55% above total manufacturing cost, reflecting Tier 1 supplier R&D amortization, program management overhead, warranty reserve provisions, and the logistics cost of automotive-grade just-in-time delivery to vehicle assembly lines across global OEM platforms.

• Lifecycle product costs — including module design iterations for platform carryover, OTA firmware validation, field recall management, and end-of-life recycling compliance (EU ELV Directive, China GB/T standards) — represent 8–15% of gross revenue for leading Tier 1 automotive camera module suppliers.

• Leading manufacturers differentiate through ASIL-certified functional safety architectures, multi-OEM platform compatibility (enabling shared development cost amortization across customer programs), advanced production automation (automated optical alignment, AI-powered AOI inspection), and proprietary ISP tuning capabilities that deliver superior image quality across their target OEM vehicle segments.

Strategic Cost & ROI Analysis in the Automotive Split-View Camera Module Market

From a strategic perspective, the Automotive Split-View Camera Module Market offers strong program revenue and margin profile advantages for Tier 1 suppliers able to secure multi-platform OEM sourcing awards. Premium ADAS camera system suppliers are increasingly adopting integrated module-to-software business models to optimize:

• Gross margin improvement through AI software licensing and OTA update revenue streams (15–30% margin premium vs hardware-only supply models)

• Platform lifetime value through multi-generation architecture contracts (5–8 year OEM program cycles with carry-forward sourcing commitments)

• Brand premium through ASIL-D system-level safety certification and automotive cyber-security (ISO 21434) compliance credentials

• Scale efficiency through shared optical and ISP platform architecture across passenger car, commercial vehicle, and EV programs within a single manufacturing footprint

Automotive Split-View Camera Module Market Competitive Landscape

The Global Automotive Split-View Camera Module Market Competitive Landscape is moderately consolidated, characterized by a combination of established Tier 1 automotive systems integrators, specialized automotive imaging technology companies, and vertically integrated CMOS sensor and optics manufacturers investing in ADAS camera R&D, automotive-grade manufacturing capability, and OEM platform program management. Leading companies such as Robert Bosch GmbH have established strong market leadership in integrated ADAS camera and processing system supply to European and global OEM platforms. Continental AG continues to advance across 360-degree surround-view, split-view, and camera-based mirror replacement systems for passenger and commercial vehicles.

Valeo SA leads in parking assistance and front-camera ADAS integration. Magna International commands significant share in mirror-integrated and A-pillar camera system supply. Denso Corporation leads in Japanese OEM camera module supply for Toyota, Honda, and Mazda platforms. Mobileye (Intel) increasingly anchors the AI-powered camera perception software stack integrated above Tier 1 hardware supply. Collectively, these companies are significantly influencing Automotive Split-View Camera Module Market Share by investing in ASIL-certified hardware, AI-powered perception software, and vertically integrated optical sensor production — thereby shaping the long-term competitive dynamics of the Automotive Split-View Camera Module Industry.

Automotive Split-View Camera Module Market Scope: Inquire before buying

| Automotive Split-View Camera Module Market — Report Coverage | |

| Base Year: 2025 | Forecast Period: 2025–2032 |

| Historical Data: 2020 to 2024 | Market Size in 2025: USD 23.80 Bn |

| Forecast Period CAGR: ~10.5% | Market Size in 2032: USD 48.13 Bn |

| Segments Covered | By Lens Type: Single Lens | Dual Lens |

| By Resolution: HD (720p) | Full HD (1080p) | Ultra HD (4K) | |

| By Camera View: Front View | Rear View | Side View | 360° Surround View | |

| By Sensor Type: CCD | CMOS | |

| By Vehicle Type: Passenger Vehicles | Commercial Vehicles | Electric Vehicles | |

| By Sales Channel: OEM | Aftermarket | |

| By Technology: Digital | Infrared | Thermal | AI-Enhanced | |

| Regions Covered | North America (United States, Canada, Mexico) |

| Europe (Germany, France, UK, Italy, Spain, Sweden, Netherlands, Rest of Europe) | |

| Asia Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of APAC) | |

| Middle East & Africa (UAE, Saudi Arabia, South Africa, Rest of ME&A) | |

| South America (Brazil, Argentina, Chile, Rest of Latin America) | |

Automotive Split-View Camera Module Market Key Players

The Global Automotive Split-View Camera Module Market comprises camera-based vision systems that provide multiple viewing angles around a vehicle by splitting and processing images from different cameras. These modules enhance driver visibility, reduce blind spots, and support ADAS functions such as parking assistance and surround-view monitoring. Market growth is driven by increasing vehicle safety regulations, rising ADAS adoption, and growing demand for advanced automotive imaging technologies.

| Company | Type | Description |

| Robert Bosch GmbH | Market Leader | Global leader in automotive electronics and ADAS solutions, offering advanced multi-camera and surround-view systems for passenger and commercial vehicles. |

| Continental AG | Market Leader | Provides integrated camera modules, vision sensors, and driver assistance technologies supporting split-view and 360-degree vehicle visibility. |

| Valeo SA | Market Leader | Specializes in automotive vision systems, parking assistance technologies, and high-performance camera solutions for enhanced vehicle safety. |

| Magna International Inc. | Tier-1 Automotive Supplier | Develops advanced camera modules and digital vision systems integrated into ADAS and autonomous driving platforms. |

| Denso Corporation | Tier-1 Automotive Supplier | Manufactures automotive camera modules and imaging technologies for safety, parking, and driver monitoring applications. |

| Aptiv PLC | ADAS Technology Provider | Focuses on intelligent vehicle architecture, vision systems, and camera-based safety solutions for connected and autonomous vehicles. |

| ZF Friedrichshafen AG | Vehicle Safety Technology Provider | Offers camera-based sensing solutions integrated with ADAS and active safety systems for global automakers. |

| Autoliv Inc. | Automotive Safety Specialist | Develops camera-assisted safety systems that complement passive and active vehicle safety technologies. |

| Panasonic Corporation | Automotive Electronics Provider | Supplies automotive imaging modules and electronic vision systems for next-generation vehicle platforms. |

| LG Innotek | Camera Module Manufacturer | Produces high-resolution automotive camera modules used in surround-view and split-view applications. |

| Sony Corporation | Image Sensor Provider | Leading supplier of CMOS image sensors that power advanced automotive camera modules and vision systems. |

| OmniVision Technologies | Imaging Technology Provider | Develops automotive-grade image sensors optimized for low-light performance and ADAS applications. |

| Samsung Electro-Mechanics | Camera Module Manufacturer | Provides compact and high-performance camera modules for vehicle vision and safety applications. |

| Mobileye | Vision-Based ADAS Leader | Offers AI-driven vision technologies and camera-based perception systems supporting advanced driver assistance functions. |

| Harman International | Automotive Electronics Company | Develops connected vehicle technologies and camera-integrated safety systems for OEM customers. |

| Gentex Corporation | Digital Vision Systems Provider | Known for digital rear-vision and camera-monitoring systems that enhance vehicle visibility and safety. |

| Ambarella Inc. | Automotive Vision Semiconductor Provider | Supplies AI vision processors and image processing solutions for automotive camera systems and ADAS platforms. |

| Stoneridge Inc. | Commercial Vehicle Vision Specialist | Focuses on camera-monitoring systems and visibility solutions for commercial and heavy-duty vehicles. |