Specialty Polymers Market Size by Type, End Use, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

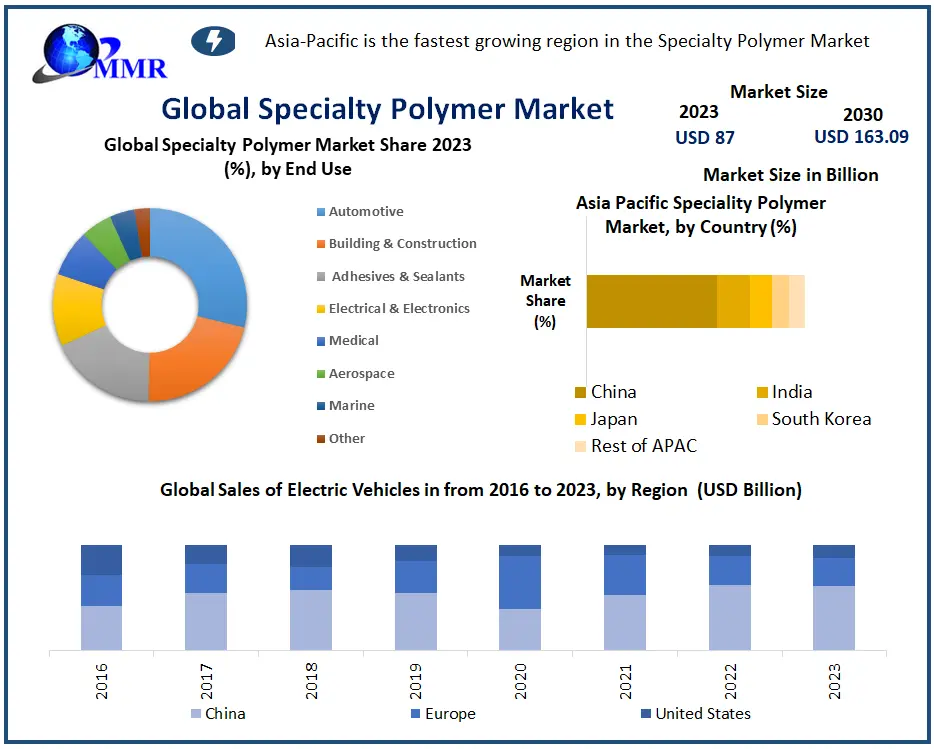

The Specialty Polymers Market size was valued at USD 87 Billion in 2023 and the total Specialty Polymers revenue is expected to grow at a CAGR of 6.6% from 2024 to 2030, reaching nearly USD 163.09 Billion by 2030.

Specialty Polymers Market Overview

Specialty polymers refer to a class of synthetic materials that have been designed and engineered to possess specific properties and functions for a wide range of industrial and commercial applications. These polymers are typically produced by modifying the chemical structure of the base polymer or by blending two or more different polymers to achieve the desired properties.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The demand for specialty polymers has surged as a result of their use in various applications where traditional polymers are not suitable owing to performance or processing limitations. The need for lightweight and fuel-efficient vehicles has led to an increased utilization of polymers in automobile parts, replacing heavy metals and reducing weight. This transition not only enhances automotive efficiency but also indirectly stimulates the economy through specialty polymer market growth. Additionally, as infrastructure and construction projects expand, requiring high-quality and durable structures, the demand for specialty polymers is expected to further increase. These polymers offer exceptional performance in challenging conditions without compromising specific operations, making them essential in various end-user applications such as biomedical devices, aerospace components, and consumer goods.

The key market players such as Eastman Chemical Company (United States), PolyOne Corporation (United States), Mitsui Chemicals, Inc. (Japan), DIC Corporation (Japan), RTP Company (United States), Clariant AG (Switzerland), LANXESS AG (Germany), Covestro AG (Germany), Saudi Basic Industries Corporation (SABIC) (Saudi Arabia), and Sumitomo Chemical Co., Ltd. (Japan), etc. invest in research and development to innovate new products and enhance existing ones, aiming to meet specific performance requirements and expand their market presence. However, the market remains positive, fueled by the increasing demand for lightweight vehicles and untapped opportunities in developing countries, promising ongoing growth and advancement in the specialty polymers industry.

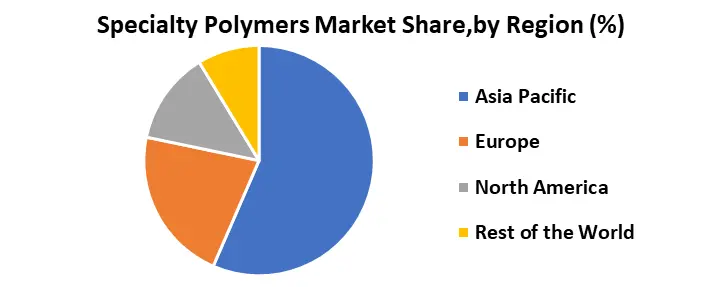

North America plays a significant role in the specialty polymer market, accounting for a substantial share. The growth of the region is attributed to the demand for specialty polymers in specialized applications like electrical insulation, corrosion resistance, wear resistance, and thermal stability. North America is expected to continue playing a pivotal role in driving innovation and demand for the specialty polymers market.

Specialty Polymers Market Dynamics

Innovative Trends Driving Sustainability

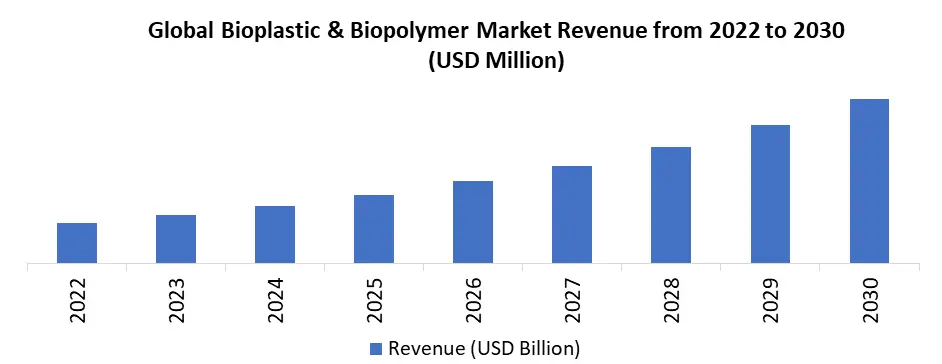

Bio-based and biodegradable polymers, functionalization, nano-composites, and 3D printing present significant opportunities in the specialty polymer market, driving innovation and sustainability. The utilization of bio-based polymers offers a renewable alternative to traditional petro-based polymers, addressing environmental concerns and reducing reliance on non-renewable resources. These biodegradable polymers are gaining traction for their eco-friendly nature and diverse applications in various industries. In addition, functionalization techniques enhance the properties of polymers, making them more versatile and tailored to specific needs, thereby expanding their market potential. Nano-composites, particularly sustainable polymer nanocomposites, are at the forefront of material innovation, offering improved performance characteristics and environmental benefits. Also, the integration of biobased polymers in 3D printing processes is revolutionizing manufacturing by enabling the production of complex structures with reduced environmental impact.

The combination of these advancements not only opens new avenues for specialty polymer applications but also aligns with the growing demand for sustainable solutions in the polymer industry, positioning bio-based materials, functionalized polymers, nano-composites, and 3D printing as key drivers of future growth and development in the specialty polymer market.

Transformative Impact of Recycling Technologies

Advancements in recycling technologies are significantly impacting the specialty polymer market by revolutionizing the way plastics are recycled and reused. The adoption of depolymerization technologies, which break down plastic waste into monomers that have been used to manufacture high-quality recycled plastics. These technologies offer a solution to the limitations of conventional mechanical recycling methods, ensuring consistent quality in recycled plastics suitable for various applications. Chemical recycling is considered a game-changer as it enables the production of natural and pure forms of resins from hard-to-recycle plastic waste streams, driving substantial investment in recycling infrastructure. The integration of artificial intelligence (AI) and machine learning is optimizing waste plastic identification, sorting, and processing, enhancing efficiency and quality in recycling processes. These advancements are reshaping the plastics market towards a circular economy model by promoting the reuse of resources, reducing plastic pollution, and decreasing reliance on virgin plastic production.

The global recycled plastics market is projected to grow significantly, reaching $50 billion by 2030, driven by factors such as technological innovations in recycling and a shift towards circular economy principles. Hence, advancements in recycling technologies are poised to transform the specialty polymer market by increasing recycling capacity, improving quality, and driving sustainability across the industry.

Specialty Polymers Market Segment Analysis

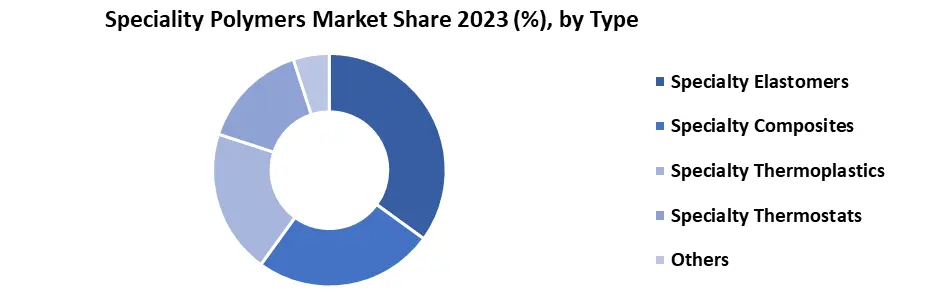

Based on Type, the specialty elastomers segment held the largest market share in the Global Specialty Polymers Market in 2023. According to MMR analysis, the segment is further expected to grow at a CAGR of 6.6% during the forecast period. It stands out as the dominant segment within the Specialty Polymers Market. Specialty elastomers are distinguished from other specialty polymers by their remarkable ability to return to their original shape even after undergoing significant deformation making the segment dominant in the specialty polymer market. They are extensively used in various sectors, ranging from automotive engineering to the manufacturing of medical implants and sports equipment. The versatility of specialty elastomers is evident in the wide range of formulations available, each specifically tailored to meet particular performance requirements, which increases their demand in the specialty polymer market. Additionally, specialty elastomers have been effectively blended with other materials to form composites with improved properties. By incorporating fibers into elastomers, manufacturers enhance their tensile strength and tear resistance, making them suitable for even the most challenging applications in the specialty polymer market. The specialty elastomer segment stands out thanks to its unmatched elasticity, versatility across different applications, advantages in processing, compatibility with other materials, and a strong emphasis on continuous innovation. These factors collectively position specialty elastomers as essential materials that drive growth and establish dominance in the specialty polymer market.

Specialty Polymers Market Regional Analysis

Asia Pacific dominated the Global Specialty Polymers Market with the highest share of over 65% in 2023. The region is expected to grow at a CAGR of 6.6% during the forecast period and maintain its dominance by 2030. The demand for specialty polymers in the Asia-Pacific region is being driven by the growing automotive and electrical industries in countries such as China and India. These countries are experiencing significant infrastructural and industrial development, which further contributes to the demand for specialty polymer market. China and India, with their large automotive markets and steady growth in vehicle production and sales, present profitable opportunities for the specialty polymer market. The growth is fueled by urbanization, rising disposable incomes, and technological advancements. Additionally, the increasing adoption of electric and hybrid vehicles in these countries adds to the demand for specialty polymers, which are essential in key components like battery systems, wiring, connectors, and thermal management solutions. China being the world's largest consumer and producer of specialty polymers and the government's support for electric and hybrid vehicles as part of its broader environmental program opens new growth opportunities for specialty polymers, especially in battery technologies and electrical systems. Additionally, government policies like the "Aatma Nirbhar Bharat" (Self-Reliant India) and "Make in India" programs in India strengthen domestic manufacturing, improve the competitiveness of the automotive industry, and attract foreign investments, ultimately fostering innovation and technological advancements making the region dominant in the Speciality Polymer Market. The expected rise in government assistance aimed at enhancing the automotive sector is likely to create opportunities for the specialty polymer market.

1. According to MMR analysis, in 2023, the total production of automotive production in India was 2,59,31,867 units, while in 2022 it was 2,30,40,066 units- an increase of 11.15%.

Additionally, Europe is a mature market with a significant market share and is growing with a CAGR of 6.6% during the forecast period. Europe is home to some of the world's leading automotive, aerospace, and medical device manufacturers which heavily rely on high-performance specialty polymers. The region's strict regulations on safety, sustainability, and recyclability have compelled manufacturers to adopt advanced specialty polymers, leading to consistent growth in the specialty polymer market. The increasing aging population and the emphasis on advanced medical treatments in Europe have also contributed to the rising demand for specialty polymers in the medical device market. Additionally, a significant need for lightweight materials to enhance fuel efficiency and bio-based polymers to minimize environmental impact influences the specialty polymer market. As a result, Europe's specialty polymer market shows great growth potential, driven by technological advancements, environmental concerns, and a robust manufacturing sector.

Specialty Polymers Market Competitive Landscapes

The Global Specialty Polymers Market industry is competitive among companies owing to the presence of numerous players across the industry. The major players in the market include BASF SE (Germany), DowDuPont Inc. (United States), Solvay S.A. (Belgium), Evonik Industries AG (Germany), Arkema SA (France), Celanese Corporation (United States), Kuraray Co., Ltd. (Japan), SABIC (Saudi Arabia), Eastman Chemical Company (United States), PolyOne Corporation (United States), etc. These companies are pushing boundaries, investing in research and development to expand their product lines, and undertaking strategic activities including new product launches, contractual agreements, mergers and acquisitions, and collaborations with other organizations. The future of the Specialty Polymers Market promises to be vibrant and dynamic, driven by technological innovation and appealing consumer experiences.

1. In 2023, Total Polymer Solutions (TPS) was acquired by Formerra, a leading distributor of highly engineered thermoplastic resins and specialty polymers in North America. This acquisition aimed to enhance Formerra's presence in the healthcare market and expand into Europe, leveraging TPS's market presence in Ireland and the United Kingdom, known for their leadership in medical device production.

2. In 2023, LyondellBasell Industries acquired a controlling stake in A. Schulman Inc., a leading global provider of high-performance specialty plastics.

3. In 2023, BAS introduced a novel flame-retardant engineering plastic specifically designed for demanding applications in electrical and electronics.

Specialty Polymers Market Scope: Inquire before buying

| Specialty Polymers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | USD 87 Billion |

| Forecast Period 2024 to 2030 CAGR: | 6.6 % | Market Size in 2030: | USD 163.09 Billion |

| Segments Covered: | by Type | Specialty Elastomers Specialty Composites Specialty Thermoplastics Specialty Thermosets Others |

|

| by End Use | Automotive Building and Construction Adhesives and Sealants Electrical and Electronics Medical Aerospace Marine Other |

||

Specialty Polymers Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Specialty Polymers Market Key Players

1. North America

1. DowDuPont Inc. (United States)

2. Celanese Corporation (United States)

3. Eastman Chemical Company (United States)

4. PolyOne Corporation (United States)

5. RTP Company (United States)

6. Celanese International Corporation (United States)

7. 3M (United States)

8. LyondellBasell Industries (United States)

9. Ashland Inc. (United States)

2. Europe

1. BASF SE (Germany)

2. Solvay S.A. (Belgium)

3. Evonik Industries AG (Germany)

4. Arkema SA (France)

5. Clariant AG (Switzerland)

6. LANXESS AG (Germany)

7. Covestro AG (Germany)

8. Wacker Chemie AG (Germany)

9. Trelleborg AB (Sweden)

10. Victrex PLC (United Kingdom)

11. Arkema Group (France)

12. Lanxess Corporation (Germany)

3. Asia Pacific

1. Kuraray Co., Ltd. (Japan)

2. Mitsui Chemicals, Inc. (Japan)

3. DIC Corporation (Japan)

4. Sumitomo Chemical Co., Ltd. (Japan)

5. Kaneka Corporation (Japan)

6. LG Chem Ltd. (South Korea)

7. Polyplastics Co., Ltd. (Japan)

8. Asahi Kasei Corporation (Japan)

9. Teijin Limited (Japan)

4. Middle East & Africa

1. SABIC (Saudi Arabia)

FAQs:

1. What are the growth drivers for the Specialty Polymers market?

Ans. Increasing demand for high-performance materials and technological advancements are the drivers of the Global Specialty Polymers Market.

2. What are the opportunities for the Specialty Polymers market growth?

Ans. Advancements in recycling technologies and a rising focus on light-weighting are the opportunities for the Specialty Polymers Market.

3. Which region is the fastest-growing region in the Global Specialty Polymers market during the forecast period?

Ans. Asia Pacific is the fastest-growing region in the global Specialty Polymers market during the forecast period.

4. What is the projected market size & and growth rate of the Specialty Polymers Market?

Ans. The Specialty Polymers Market size was valued at USD 87 Billion in 2023 and the total Specialty Polymers revenue is expected to grow at a CAGR of 6.6% from 2024 to 2030, reaching nearly USD 163.09 Billion by 2030.

5. What segments are covered in the Specialty Polymers Market report?

Ans. The segments covered in the Specialty Polymers market report are type, end-use, and region.