Semiconductor Fabrication Material Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

The Semiconductor Market size was valued at USD 627.86 Billion in 2025 and the total Semiconductor Market revenue is expected to grow at a CAGR of 6.21 % from 2026 to 2032, reaching nearly USD 957.25 Billion by 2032.

Semiconductor Market Overview

Semiconductors are an essential component of electronic devices, enabling advances in communications, computing, healthcare, military systems, transportation, clean energy, and countless other applications. Semiconductors also known as integrated circuits (ICs) or microchips, are made from pure elements, typically silicon or germanium, or compounds such as gallium arsenide. In a process called doping, small amounts of impurities are added to these pure elements, causing large changes in the conductivity of the material. The semiconductor market supply chain is intricate and globally dispersed, involving multiple stages from raw material sourcing to final product assembly.

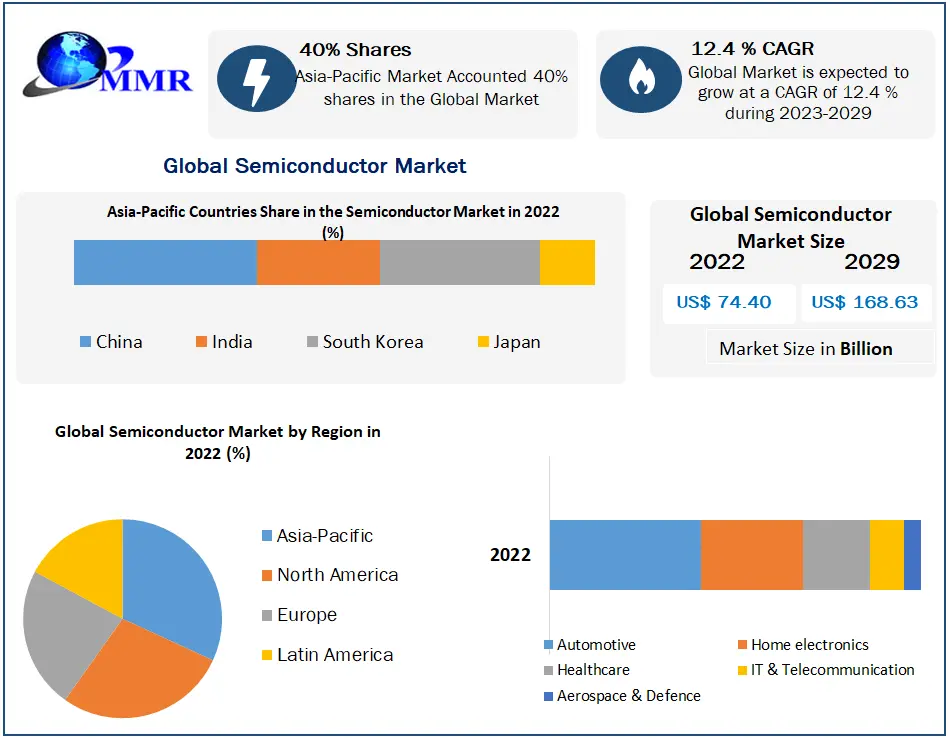

China, the world’s leading manufacturing nation by output, was the largest downstream user of semiconductors in 2022, accounting for 32% of global semiconductor sales. Chinese manufacturers integrate these semiconductors into a wide array of electronic products, which are either used domestically or exported worldwide. The United States and China were the top consumers of semiconductors embedded in electronic goods, with shares of 25% and 24%, respectively, followed by the European Union (EU) at 20%.

According to MMR, global semiconductor sales reached $46.4 billion in April 2024, marking a 15.8% increase from $40.1 billion in April 2023 and a 1.1% rise from $45.9 billion in March 2024. These monthly sales figures, compiled are based on a three-month moving average. Furthermore, the latest forecast predicts annual global sales growth of 16.0% in 2024 and 12.5% in 2025. The SIA represents 99% of the U.S. semiconductor industry by revenue and almost two-thirds of non-U.S. chip companies.

Strengthening the US Semiconductor supply chain

1. U.S. fab capacity is projected to increase by 203% by 2032, a tripling of U.S. capacity.

2. The U.S. is expected to increase its share of global fab capacity for the first time in decades, growing from 10% today to 14% by 2032.

3. The U.S. will secure more than one-quarter (28%) of global capital expenditures between 2025-2032 – an estimated $646 billion – an amount second only to Taiwan.

The semiconductor market report by MMR includes a detailed analysis of investments in the sector, segmented by country, type, and private entities over the past five years. It identifies key trends and investment patterns within this period, providing a comprehensive overview of the financial landscape. The report highlights recent product launches from leading companies in the semiconductor industry, such as Intel, NVIDIA, and AMD, showcasing the latest technological advancements and innovations. The report forecasts future investments over the next 7 years, offering valuable insights into expected market growth and development. This predictive analysis aims to help stakeholders make informed decisions by understanding where and how investments are likely to occur, thereby driving strategic planning and resource allocation. The inclusion of recent launches and future investment estimates makes this report an essential resource for comprehending both current market dynamics and future potential in the semiconductor industry.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Semiconductor Market Dynamics

China's Semiconductor Surge: Building a Robust Local Ecosystem

In the dynamic realm of semiconductors, China is making significant strides toward developing a robust local ecosystem. According to the SEMI World Fab Forecast report, China is set to construct an impressive 18 new fabs in 2024. This ambitious expansion reflects the Chinese government’s steadfast commitment to fostering domestic chip development in response to ongoing U.S. sanctions, which is expected to boost the Semiconductor Market growth.

This surge in fab construction will undoubtedly enhance China’s production capacity, particularly in mature node technologies. The increased supply of chips will not only meet the growing demand from domestic industries but also intensify competition for analog and discrete chips, which are critical components in automotive, industrial, and other markets.

A remarkable display of technological prowess is evident in Huawei’s Mate 60 smartphone, developed with SMIC’s 7-nm technology, showcasing China’s relentless pursuit of advanced chip manufacturing. The successful production of this high-end device demonstrates China’s ability to compete in the global semiconductor arena despite geopolitical challenges. Additionally, Chinese automaker Nio has recently unveiled its first in-house developed autonomous-driving chip, the NX9031. Built on a 5-nm process with over 50 billion transistors, this chip underscores China's growing capabilities in cutting-edge semiconductor technology.

For some semiconductor companies, expansion efforts involve building fabs in regions or countries where they have not previously operated. Traditionally, companies sought locations with established semiconductor ecosystems meeting basic requirements: stable energy and water supplies, a pool of technically skilled potential employees, the right infrastructure, and a solid transportation network. Notable ecosystems that fit this profile include Taiwan’s Hsinchu Science Park and Germany’s Silicon Saxony. While these basic requirements remain crucial, they are no longer sufficient to guarantee investment. Semiconductor companies now prioritize the three S’s—sustainability, supply chain security, and subsidies—when selecting new sites. This shift reflects broader global changes, including growing concerns about climate change, geopolitical issues disrupting shipments, and economic uncertainty.

The semiconductor industry value and its benefits to local economies, much is at stake as companies expand. Both businesses and the regions or countries where they establish new sites stand to gain significantly. Here's a look at the industry's growth potential and the factors that may determine where new fabs are built over the next decade. If semiconductor companies in the United States or other high-production-cost countries rely entirely on renewable energy sources, their energy costs could be two to four times lower than in many Asian countries. This reduction might help offset other expenses. Eventually, fabs in regions with limited renewable energy might import it from other countries, potentially raising overall energy costs above current rates. For instance, Singapore aims to import 4 gigawatts of low-carbon electricity—about 30 percent of its supply—from neighboring countries by 2035.

Effective Automation in Semiconductor Manufacturing and are the Biggest Challenges in Semiconductors Market

In the realm of semiconductor manufacturing, automation systems play a crucial role in overseeing and controlling the complex and dynamic wafer fabrication process in the semiconductors market. This process must adapt to evolving demands placed on semiconductors, necessitating continuous adjustments, and fine-tuning. To ensure seamless operation and optimization of wafer fabrication and related processes, semiconductor manufacturers must prioritize investments in both human expertise and artificial intelligence (AI) oversight. This strategic combination allows for efficient monitoring and control of the automation frameworks, ensuring they remain responsive to the evolving demands of the fabrication process. While automation is indispensable in this semiconductors industry, it is important to acknowledge the substantial cost involved. Semiconductor manufacturers face not only the initial investment of retrofitting facilities for automated processes but also ongoing expenses associated with maintaining and sustaining the functionality of these automated systems.

Presently, the semiconductor manufacturing industry has achieved production of 7 nanometers (nm) chips, with an ongoing exploration into the possibilities of developing even smaller-scale components, such as 5 nm and potentially 3 nm chips in the semiconductors market. However, manufacturing at such minuscule scales introduces challenges related to electrostatic and quantum effects, which can significantly impact chip performance and yield. Moreover, imperfections in the silicon substrate, which were once negligible, now possess the potential to render entire batches of wafers unusable. In addressing these challenges, the integration of artificial intelligence (AI) offers unique advantages that surpass the capabilities of manual production processes in the semiconductors market.

AI technologies effectively identify anomalies in production test results or sensor data, enabling the assessment of potential causes such as material impurities or damage caused by electrostatic discharge (ESD). With this valuable information, control engineers can make informed decisions and implement adjustments to fabrication processes, effectively mitigating the negative impact of substrate imperfections on production yields. By leveraging AI, semiconductor manufacturers enhance quality control measures and optimize production processes to ensure consistent and reliable chip manufacturing in the semiconductors market.

Semiconductor Market Segment Analysis

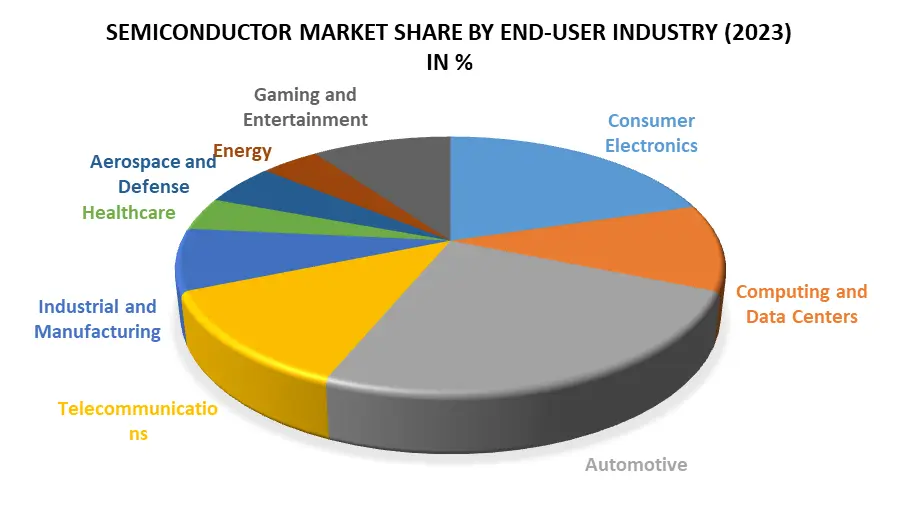

Based on End-User Industry, the market is segmented into Consumer Electronics, Computing and Data Centers, Automotive, Telecommunications, Industrial and Manufacturing, Healthcare, Aerospace and Defense, Energy, and Gaming and Entertainment. Automotive segment dominated the market in 2023 and is expected to hold the largest Semiconductor Market share over the forecast period. Automotive segment consist of Infotainment Systems, Advanced Driver Assistance Systems (ADAS), Electric Vehicles (EVs), and Autonomous Vehicles. The automotive segment is a significant and rapidly growing part of the semiconductor market. Semiconductors are essential for a wide range of applications in vehicles, from basic functions to advanced driver-assistance systems (ADAS) and electric vehicles (EVs).

The increasing adoption of EVs is a major driver of demand for automotive semiconductors. In 2023, global EV sales surpassed 10 million units, a significant increase from previous years. Each EV typically requires about twice as many semiconductors as a traditional internal combustion engine (ICE) vehicle. The largest market for automotive semiconductors, driven by high vehicle production in countries like China, Japan, and South Korea.

Semiconductor Market Regional Insight

Asia Pacific dominated the market in 2025 and is expected to hold the largest Semiconductor Market share over the forecast period (2026-2032). South Korea, Japan, Mainland China, and Taiwan have each played a pivotal role in the semiconductor industry's development, encompassing both upstream and downstream activities. Recent black swan events have underscored the strategic importance of the Asia Pacific semiconductor market. It is expected that by 2032, the Asia Pacific region will account for 62% of the global semiconductor market.

The semiconductor manufacturing hub of the world, China plays a pivotal role in global supply chains, particularly in electronics, textiles, automotive, and consumer goods. Known for its advanced technology and automotive industries, Japan is a major player in the high-tech and precision manufacturing sectors. Major ports such as Shanghai, Singapore, and Hong Kong serve as crucial nodes in global shipping routes. The region has some of the busiest ports in the world, facilitating enormous volumes of trade.

China is expected to accelerate efforts to substitute semiconductor imports with domestically produced alternatives, driving an increase in demand for non-imported semiconductors and stimulating domestic investment. China has established the "Big Fund," a substantial investment fund worth USD 50 billion dedicated to the development of its domestic semiconductor industry. This fund will be utilized in two phases to support industry growth. However, this amount may not be sufficient to meet long-term capital requirements. To support its semiconductor ambitions, China need to nurture a skilled talent pool by strengthening education and encouraging more students to major in electronics and related fields. Chinese semiconductor companies generally lag behind global leaders in terms of technology. China remains a relatively small player in the global semiconductor market, particularly in mid-to-high-end segments such as semiconductor equipment and EDA & IP. Despite this, Chinese companies are significantly increasing their investments to close the gap in all aspects of the industry.

Semiconductor Market Competitive Landscape

Intel unveiled its "IDM 2.0" strategy, which centers on becoming a significant provider of semiconductor manufacturing services for both Intel's own products and external companies. Intel introduced its latest CPU architecture, code-named "Alder Lake," featuring a hybrid design that combines high-performance cores and high-efficiency cores to enhance power efficiency. Intel made its entry into the discrete graphics market by launching the Intel Arc brand, which encompasses a range of gaming GPUs. Intel completed the acquisition of Habana Labs, an Israeli AI chip company, to reinforce its portfolio of artificial intelligence accelerators. Intel acquired Barefoot Networks, a networking chip company, to augment its capabilities in data center networking. The most notable PC product milestones for Intel in 2023 include, the Intel Core processor's new asymmetric architecture with P-cores and E-cores, Intel's End-to-End Foundry and IDM 2.0, and Intel's jump back into discrete GPUs with Intel Arc. Intel announced its 13th Gen Core processors, codenamed Intel Raptop Lake, at its annual IntelON event in 2022, specifically its higher-end desktop K-series. It is building on the momentum of its K-series with a 40% increase in Gen-over-Gen performance.

Samsung Electronics unveiled the Galaxy Note20 series, showcasing advanced mobile technologies and enhanced S Pen functionality. Samsung introduced its flagship smartphone lineup, the Galaxy S21 series, which demonstrated innovative features such as improved camera capabilities and powerful processing performance. Samsung announced the launch of "Neo QLED," its next-generation display technology that combines Quantum Mini LED technology with advanced image processing, delivering superior picture quality. Samsung completed the acquisition of Zhilabs, a Spanish network analytics company, to enhance its expertise in network monitoring and optimization. Samsung Electronics showcased its unparalleled technical expertise and innovation at InfoComm 2023, North America’s largest audiovisual trade show. Samsung Electronics today announced a partnership with the United Nations Development Programme (UNDP) to support young change-makers working to achieve the 17 Global Goals in the semiconductors market.

Semiconductors Market Scope Table : Inquire Before Buying

| Semiconductor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 627.86 USD Bn |

| Forecast Period 2026-2032 CAGR: | 6.21% | Market Size in 2032: | 957.25 USD Bn |

| Segments Covered: | by Component | Microprocessors Memory Chips Sensors Analog (ICs) Discrete Semiconductors Power Management (ICs) Optoelectronics Others |

|

| by Material Type | Silicon Gallium Arsenide (GaAs) Silicon Carbide (SiC) Gallium Nitride (GaN) Germanium Others |

||

| by Manufacturing Process | Front-End Manufacturing Back-End Manufacturing Testing & Assembly |

||

| by End-Use Industry | Consumer Electronics Automotive Industrial Telecommunications Healthcare Aerospace & Defense Data Centers Others |

||

| by Sales Channel | Direct Sales Distributors Online/E-commerce |

||

Semiconductors Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Leading Semiconductor Key Players Include:

1. Intel Corporation

2. Samsung Electronics Co., Ltd.

3. Taiwan Semiconductor Manufacturing Company Limited (TSMC)

4. SK Hynix Inc.

5. Qualcomm Incorporated

6. Broadcom Inc.

7. NVIDIA Corporation

8. Texas Instruments Incorporated

9. Advanced Micro Devices, Inc. (AMD)

10. Micron Technology, Inc.

11. Infineon Technologies AG

12. NXP Semiconductors N.V.

13. Sony Corporation

14. STMicroelectronics N.V.

15. Renesas Electronics Corporation

16. MediaTek Inc.

17. Xilinx, Inc.

18. Analog Devices, Inc.

19. ON Semiconductor Corporation

20. Marvell Technology Group Ltd.