Secure Access Service Edge Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

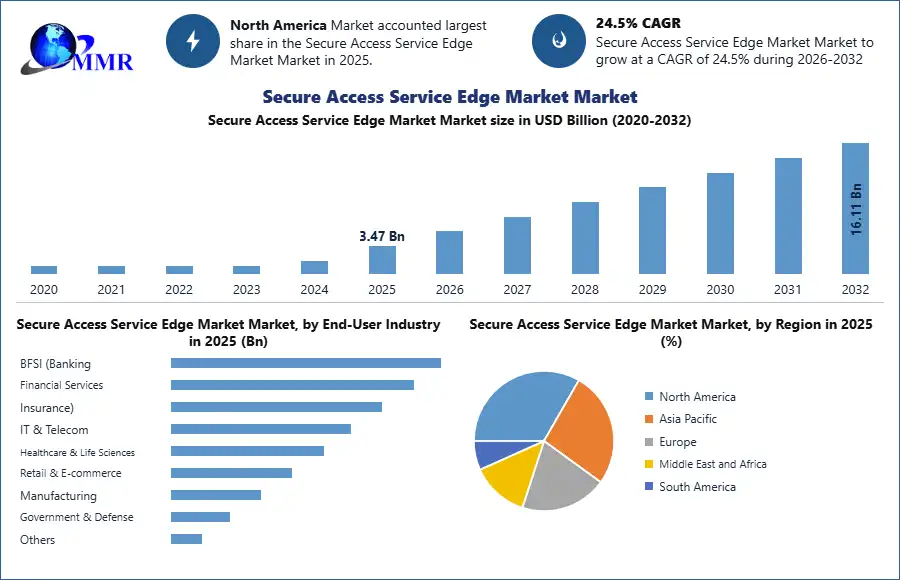

Secure Access Service Edge Market size was valued at USD 3.47 Bn. in 2025 and the total Global Secure Access Service Edge revenue is expected to grow by 24.5 % from 2026 to 2032, reaching nearly USD 16.11 Bn.

Secure Access Service Edge Market Overview:

The Secure Access Service Edge(SASE) is a cloud-based enterprise security framework and a network architecture that combines VPN and SD-WAN challenges caused by digital business transformation. The SASE model responds to reversal delivering network and controlling the network security for the users. Using secure access service edge distributed enterprises access network resources rapidly and safely. The SASE products combine software-defined wide-area networking (SD-WAN) with network security technologies to offer protection end-to-end, including Secure Web Gateways (SWG), Zero-Trust Network Access (ZTNA), and Cloud Access Security Brokers (CASB). Major key players are spending a lot to increase their product lines, which helps to grow SASE. Hence, the demand for the Secure Access Service Edge Market is growing rapidly.

To know about the Research Methodology :- Request Free Sample Report

Drivers

Usage of SASE is increased as cyberattacks and data breaches have increased

The usage of cloud-based has grown in recent years as more organizations and industry verticals transfer the data of an organization to the cloud to boost productivity, cut costs, and scalability. With the increasing usage of cloud-based applications, cyber security also increases because cyber attacks and data breaches have increased. Secure Access Service Edge Market reduces the cost, reduces complexity, helps to secure access for users continuously, and enables more secure remote and mobile access. The growth in mobile devices and the IoT is raising the demand for effective and rapid access to network resources from remote places and devices (IoT). SASE provides solutions that are scalable and adaptive network security solutions that can change to meet the requirements of businesses. As a result, the

Secure Access Service Edge Market growing its demand.

Restraints

Migration of IT infrastructure to public clouds compromising security architecture

As migration of many applications and workloads are on the public cloud, organizations need to check that the data is protected which can hamper the market. For understanding the security capabilities it’s important to work closely with cloud service providers. It is important for organizations to clearly understand these responsibilities to ensure the proper security measures are implemented. Cloud security controls, configurations, and the integration of security services are difficult to handle within the SASE framework which can create challenges if organizations lack the necessary knowledge and resources. Cloud environments are striking targets for cyber threats or cyber attackers and organizations must keep an eye on evolving security challenges.

Secure Access Service Edge Market Opportunity

Rise in cloud adoption helps the Secure Access Service Edge Market

The Secure Access Service Edge Market is poised for substantial growth due to several factors such as increasing adoption cloud services. Migration of Applications and workloads to the cloud for its scalability, agility, and cost-efficiency is done by organizations. As more businesses hold cloud computing, there is a rising need for a complete and secure approach to connect users and applications across dispersed environments.

Secure Access Service Edge provides a unified solution that combines network and security services in the cloud, making it an ideal choice for cloud-centric organizations. The ability to provide secure access from remote places, on any device, guarantees that remote employees can work efficiently while maintaining a high level of security. SASE's integrated many security services, including advanced threat detection which can prevent cyber threats, secure web gateways, and prevention of data loss, offer a more widespread and proactive approach to security, helping enterprises defend against emerging threats.

Secure Access Service Edge Market Segment Analysis:

Based on the Offerings,

The security as a service(SaaS) segment has witnessed market growth in the year 2025 and is expected to dominate during the forecast period. It is cloud-based that provides security solutions that are found in Business Intelligence and Data centers. SaaS offers harmless access to apps and services as it is a very important component of the market across the world. Network as a Service is expected to gain popularity in the coming years. Network as a Service is another essential component of the market. NaaS in SASE influences virtualization technologies that do not rely on physical network appliances, The network services are provided through software-defined networking (SDN) and network function virtualization (NFV).

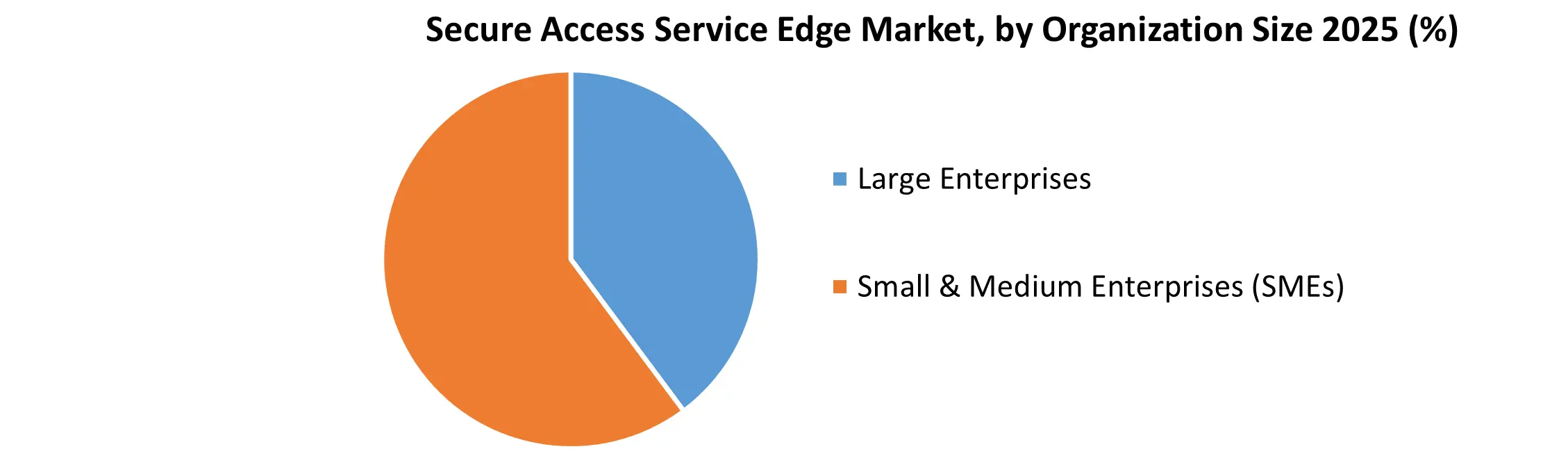

Based on Organization Size,

The large Enterprises segment has dominated the Secure Access Service Edge Market revenue in the year 2025 and is projected to grow during the forecast period. The SASE market segmentation is based on organization size, divided into Small & Medium Enterprises and Large Enterprises. Big organizations use SASE to prevent cyberattacks and for the safety of crucial information hence, large businesses are redesigning security architecture and policies. As large companies have a cost advantage for the use of SASE. However, Small and Medium enterprises use cloud-based solutions in the secure access service edge business. As a result, Large enterprises have dominated the SASE market.

Regional Insights:

North America region acquired the largest revenue in the year 2025 and is expected to grow during the forecast period. SASE is growing substantially as it has advanced technology, and the adoption of cloud services is increasing in the US and Canada. The regional market in the US is increasing rapidly and SASE is used across the region widely due to the rising number of cyberattacks against large enterprises or organizations which affects the overall business. Whereas Asia-Pacific is anticipated to witness considerable market growth in the upcoming years. The rising demand for security and cloud networks increases the progress of the market. Software and support services adoption strongly drives revenue growth in the market during the assessment period.

Secure Access Service Edge Market Scope: Inquire before buying

| Secure Access Service Edge Market Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 3.47 USD Billion |

| Forecast Period 2026-2032 CAGR: | 24.5% | Market Size in 2032: | 16.11 USD Billion |

| Segments Covered: | by Offering | SD-WAN (Network Layer) Software-defined SD-WAN Appliance-based SD-WAN Security Service Edge (SSE) Zero Trust Network Access (ZTNA) Cloud Access Security Broker (CASB) Secure Web Gateway (SWG) Firewall-as-a-Service (FWaaS) Others |

|

| by Component | Solutions Integrated SASE platforms Standalone modules Services Managed Services Professional Services (consulting, integration, support) |

||

| by Deployment Mode | Cloud-native SASE Hybrid SASE On-premise |

||

| by Organization Size | Large Enterprises Small & Medium Enterprises (SMEs) |

||

| by Access Type / User Environment | Remote / Mobile Users Branch Offices Headquarters / Data Centers IoT & Edge Devices |

||

| by End-User Industry | BFSI (Banking, Financial Services, Insurance) IT & Telecom Healthcare & Life Sciences Retail & E-commerce Manufacturing Government & Defense Others |

||

Secure Access Service Edge Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players

1. Cisco

2. HPE

3. Broadcom

0. Fortinet

5. Akamai

6. Oracle

7. Extreme Networks

8. Palo Alto Networks

9. Barracuda Networks

10.Riverbed Technology

11.Forcepoint

12.Zscaler

13.Cloudflare

14.Netskope

15.McAfee

16.Proofpoint

17.SonicWall

18.Open Systems

19.Exium

20.Twingate

21.Aryaka

22.FlexiWAN

23.Cato Networks

24.Peplink

25.Check Point Software Technologies

26.Versa Networks

27.FatPipe Networks

28.Lavelle Networks

29.NordLayer

30.Verizon

31.AT&T

32.Lumen Technologies

33.Comcast Corporation

34.GTT Communications

35.BT Group

36.Vodafone

37.Orange Business

38.Deutsche Telekom

39.Colt Technology Services

40.Zain Group

41.Tata Communications

42.NTT Communications

43.Saudi Telecom Company

44.Singtel

45.Telefónica

46.Telstra International

47.Claro Enterprise Solutions

48.MCM Telecom

49.Kyndryl Solutions

50.HCLTech

51.Microland

52.Wipro

53.TIBCO Software

64.Nour Global

65.Others

Frequently Asked Questions:

1] What segments are covered in the Global Secure Access Service Edge Market report?

Ans. The segments covered in the market report are based on Offerings, Organization Size, Industry Vertical, Component, and Region.

2] Which region is expected to hold the highest share of the Global Secure Access Service Edge Market?

Ans. The North American region is expected to hold the highest share of the Secure Access Service Edge Market.

3] What is the market size of the Global Secure Access Service Edge Market by 2032?

Ans. The market size of the market by 2032 is expected to reach US$ 16.11 Bn.

4] What is the forecast period for the Global Secure Access Service Edge Market?

Ans. The forecast period for the Secure Access Service Edge Market is 2026-2032.

5] What was the market size of the Global NLP in the Education Market in 2025?

Ans. The market size of the NLP in the Education Market in 2025 was valued at US$ 3.47 Bn.