Robot Drilling Market Size by Installation Type, Component, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

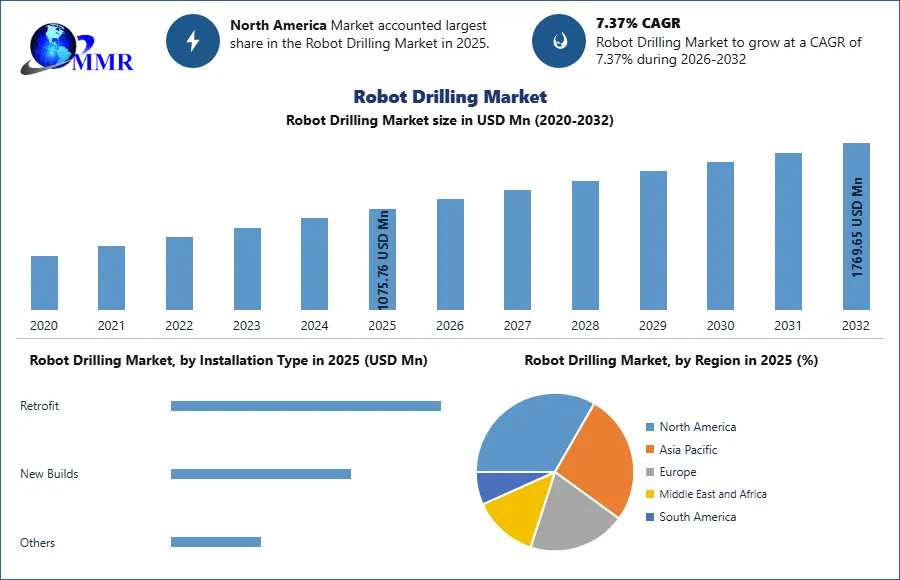

The Robot Drilling Market size was valued at USD 1075.76 Million in 2025 and the total Robot Drilling revenue is expected to grow at a CAGR of 7.37% from 2025 to 2032, reaching nearly USD 1769.65 Million.

Robot Drilling Market Overview

To know about the Research Methodology :- Request Free Sample Report

Robot Drilling Market Dynamics

Trend: Integration of AI and Autonomous Drilling Systems

One of the major trends shaping the Robot Drilling Market is the growing integration of artificial intelligence (AI), machine learning, and autonomous drilling technologies into modern drilling rigs. Oilfield operators are increasingly adopting automated drilling systems capable of performing real-time data analysis, predictive maintenance, autonomous decision-making, and remote-controlled drilling operations. These technologies significantly improve drilling accuracy, optimize well placement, and reduce non-productive time (NPT). Companies are deploying robotic pipe handling systems, automated drill floor equipment, and digital twin technologies to enhance operational efficiency and minimize human exposure to hazardous environments. Offshore drilling contractors are particularly investing in fully automated rigs to reduce labor costs and improve safety standards.

Driver: Increasing Demand for Operational Efficiency and Worker Safety

The increasing need for operational efficiency, cost optimization, and worker safety is a major driver fueling the growth of the Robot Drilling Market. Traditional drilling operations involve hazardous manual tasks such as pipe handling, drill floor management, and equipment maintenance, which expose workers to high-risk environments. Robotic drilling systems help reduce human intervention by automating repetitive and dangerous drilling activities, thereby minimizing workplace accidents and improving safety compliance. Furthermore, oil & gas companies are under pressure to reduce drilling downtime, lower operational expenditures, and maximize production efficiency. Automated drilling technologies improve drilling precision, reduce equipment failure, and enhance well productivity through real-time monitoring and predictive analytics.

High Initial Investment and Integration Complexity to Hamper Robotic Drilling Market

The high capital investment required for robotic drilling infrastructure and the complexity associated with system integration are major restraints limiting market growth. Advanced robotic drilling systems involve expensive hardware components, AI-enabled software platforms, automated pipe handling systems, sensors, and real-time monitoring technologies, resulting in significant upfront costs for oilfield operators. Small and medium-sized drilling contractors often face financial limitations in adopting fully automated rigs due to budget constraints. Additionally, integrating robotic systems with existing conventional drilling infrastructure can be technically challenging and time-consuming. Many aging drilling rigs require major modifications and software upgrades before automation technologies can be implemented effectively. The need for skilled personnel to manage, monitor, and maintain robotic systems further increases operational costs. Cybersecurity risks associated with cloud-connected and remotely operated drilling systems also create concerns among operators. Moreover, fluctuations in crude oil prices can negatively impact capital expenditure decisions, delaying investments in advanced robotic drilling technologies across several regions.

Robot Drilling Market Segment Analysis

By Component

The Hardware segment dominated the Robot Drilling Market in 2025 due to the extensive deployment of robotic arms, automated pipe handling equipment, drill floor robots, sensors, control systems, and robotic actuators across drilling operations. Hardware components form the backbone of automated drilling systems and account for a significant share of total project investments. Oil & gas operators are increasingly investing in advanced robotic equipment to improve drilling precision, reduce manual intervention, and enhance worker safety in hazardous environments. Automated drilling rigs require sophisticated hardware integration for real-time monitoring, remote operations, and predictive maintenance capabilities. The rising adoption of autonomous drilling technologies in offshore and shale drilling activities is further driving demand for robotic hardware systems. In addition, continuous advancements in sensor technologies, robotic mobility, machine vision systems, and AI-integrated control units are strengthening segment growth. High replacement demand for aging drilling infrastructure and modernization of conventional rigs are also contributing to the dominance of the hardware segment globally.

By Installation Type

The New Builds segment dominates the Robot Drilling Market as oilfield operators increasingly prefer newly designed automated drilling rigs equipped with advanced robotic systems, AI-driven software, and digital monitoring technologies. New build rigs offer better compatibility with autonomous drilling solutions compared to retrofitting older conventional rigs, which often require extensive structural modifications and higher integration costs. Offshore exploration companies and major drilling contractors are heavily investing in technologically advanced rigs capable of supporting remote operations, predictive maintenance, and fully automated drill floor management. These new-generation rigs improve drilling efficiency, reduce non-productive time, and enhance operational safety. Growing investments in deepwater and ultra-deepwater exploration projects are further accelerating demand for smart drilling rigs with integrated robotics capabilities. Additionally, energy companies are focusing on long-term operational cost reduction and sustainability goals, encouraging the adoption of advanced automated rigs from the design stage itself. Rising digital transformation initiatives across the upstream oil & gas sector continue to support the dominance of the new builds segment.

Robot Drilling Market Regional Analysis

North America dominates the Robot Drilling Market due to the strong presence of shale exploration activities, advanced oilfield infrastructure, and early adoption of drilling automation technologies across the United States and Canada. The region has witnessed significant investments in autonomous drilling rigs, AI-driven drilling optimization platforms, and robotic pipe handling systems, particularly in major shale basins such as the Permian Basin, Eagle Ford, and Bakken formations. Leading oilfield service providers including SLB, Halliburton, Nabors Industries, and NOV are actively deploying advanced robotic drilling technologies to improve drilling efficiency and reduce operational costs.

The stringent worker safety regulations imposed by regulatory authorities are encouraging operators to automate hazardous drilling activities. Offshore drilling projects in the Gulf of Mexico are further supporting demand for remote-operated and autonomous drilling systems. The increasing focus on digital oilfields, real-time drilling analytics, and predictive maintenance technologies is strengthening regional market growth. High R&D spending and strong technological capabilities continue to position North America as the dominant market for robotic drilling solutions globally.

Recent Developments

March 2025: SLB expanded its autonomous drilling portfolio through the enhancement of its DrillOps and Neuro autonomous directional drilling solutions for offshore and shale operations in North America and the Middle East. The company integrated AI-driven real-time drilling analytics and automated wellbore steering technologies to reduce drilling cycle time and improve well placement accuracy. SLB also collaborated with several national oil companies to deploy cloud-connected robotic drilling platforms that optimize rig performance and minimize non-productive time (NPT). These developments strengthened SLB’s position in smart drilling automation and supported the industry’s transition toward fully autonomous drilling operations focused on efficiency, safety, and reduced operational expenditure.

January 2025: Baker Hughes strengthened its robotic drilling capabilities by expanding its automated drilling services and digital well solutions portfolio. The company launched new AI-enabled drilling optimization technologies that improve drilling speed, reservoir targeting accuracy, and real-time operational monitoring. Baker Hughes also partnered with offshore operators to deploy remote drilling automation systems designed for harsh deepwater environments. The development included advanced sensors, cloud-based analytics, and autonomous control technologies that reduce manual intervention and enhance safety performance.

Robot Drilling Market Scope: Inquire before Buying

| Robot Drilling Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 1075.76 USD Mn |

| Forecast Period 2026-2032 CAGR: | 7.37% | Market Size in 2032: | 1769.65 USD Mn |

| Segments Covered: | by Component | Hardware Software |

|

| by Installation Type | Retrofit New Builds Others |

||

| by Application | Onshore Offshore |

||

Robot Drilling Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/Competitors profiles covered in the Robot Drilling Market report in strategic perspective

- Schlumberger (SLB)

- Halliburton

- Baker Hughes

- Nabors Industries

- NOV Inc. (National Oilwell Varco)

- Huisman Equipment

- Drillmec S.p.A.

- Automated Rig Technologies Ltd. (ART)

- Helmerich & Payne (H&P)

- Precision Drilling Corporation

- KCA Deutag

- Weatherford International

- Transocean Ltd.

- Saipem S.p.A.

- Seadrill Limited

- Shelf Drilling

- ADNOC Drilling

- Parker Drilling Company

- Ensign Energy Services

- China Oilfield Services Limited (COSL)

- Honghua Group Limited

- Bentec GmbH Drilling & Oilfield Systems

- Aker Solutions

- Siemens Energy

- ABB Ltd.

- National Drilling Company (NDC)

- HitecVision / Hitec Products

- Cyberhawk Innovations

- RigArm Inc.

- Robotic Drilling Systems AS (RDS)