Plastic Films and Sheets Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

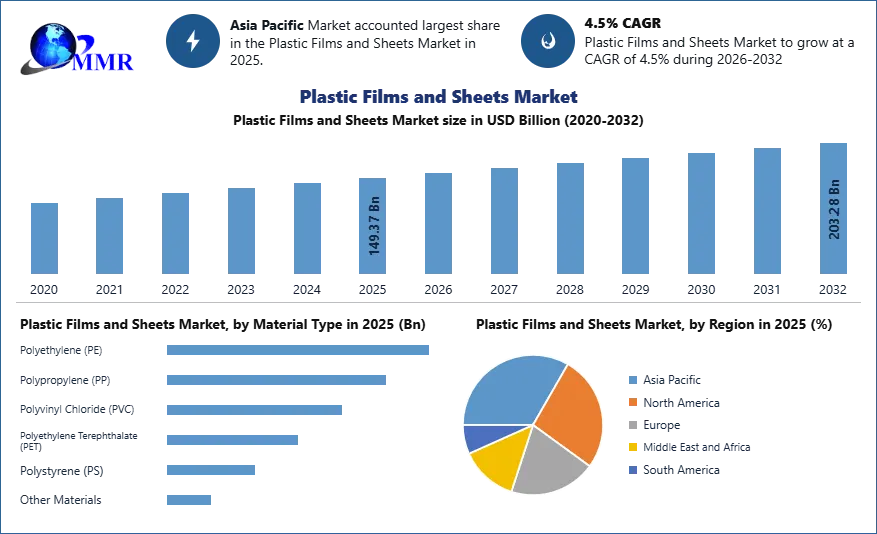

Plastic Films and Sheets Market size was valued at USD 149.37 Bn. in 2025 and the total Plastic Films & Sheets revenue is expected to grow at 4.5% from 2026 to 2032, reaching nearly USD 203.28Bn.

The Plastic film is a continuous, thin polymeric material. A "sheet" of thicker plastic material is a common term. These thin plastic membranes are used to divide regions or volumes, to contain goods, function as barriers, or provide printing surfaces. Plastic sheets are generally used in agriculture to build greenhouses, low tunnel coverings, mulching, and walk-in tunnels. HDPE sheets have a variety of applications in agriculture. These films are provided with many rows of perforations, which aid in the growth and development of plants. They are lightweight, exceedingly resilient, resistant to weather, corrosion, binding, and waterproof.

The growing demand for processed foods is driving up the need for plastic films and sheets in packaging applications. The global plastic films and sheets market is being driven by an increase in demand for plastic films and sheets in rising economies such as APAC and South America. Various plastic pollution rules are pushing the emergence of sustainable plastic films. The increasing agricultural sector is a chance for the plastic films and sheets business to grow. Rising demand for specialized films is also expected to support the plastic film market growth. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Plastic Films and Sheets Market Dynamics:

Growing demand for bi-axially oriented films across the world

Biaxially oriented films are distinguished by their ability to stretch in two separate directions. Orientation causes changes in the properties of the film, such as increased stiffness, decreased elongation, and increased lustrousness. BOPP films are utilized in a variety of applications including electrical and electronics, packaging, imaging, graphics, and industrial specialties. Because of the increasing demand for bi-axially oriented films, several plastic film producers have diverted their manufacturing efforts and invested in bi-axially oriented films. Food packaging is the most common application for these films.

As the food packaging business in developing markets has grown, so has the demand for bi-axially oriented films. It is the most popular material for food packaging since it is non-toxic and functions as an odor barrier. Bi-axial films are stretched in both the machine and transverse directions to improve mechanical, optical, and barrier characteristics.

Financial turmoil in European Countries restraining the market growth

In European countries, the market for plastic films and sheets has grown slowly over the recent five years. This was mostly due to mature markets in major economies including Germany, France, Italy, and the United Kingdom. During the recent decade, both the PE and PP film sectors in Western Europe witnessed moderate development. Additionally, Italy's financial crisis reduced demand for packaged food, which affected the growth of the country's plastic films and sheets sector. Similarly, France and the United Kingdom had a moderate increase in film demand.

Specialty films offer lucrative Opportunities

Specialized films are manufactured of specialty polymers and have distinct properties from standard films. Polyolefin, polyester, nylon, and polyvinyl butyl films are the most common. Specialty films cost more than commodity films and are utilized in a variety of packaging and non-packaging applications. The demand for specialty plastic films is growing faster than for conventional commercial films.

The market for specialized films is driven by the need for multi-layer barrier films. Such films are ideal for the meat packing business due to their non-porous and light-barrier qualities. The use of such films in pharmaceutical and cosmetic packaging is also expected to increase demand for them. The largest rise is being seen in the market for specialized films consisting of biodegradable and compostable materials.

Recyclability of flexible plastic

The recyclability of flexible plastic is an environmental and social problem, as well as a significant challenge for the packaging and non-packaging industries. Multiple-layer flexible plastic recycling is more complicated than mono-layer flexible plastic recycling since it includes additional stages. Multi-layer flexible plastic sheets or packages contain a variety of polymer kinds and inks, making them difficult to separate from bulk garbage. Each layer must be studied, recognized, and recycled separately. Polypropylene (PE) sheets and other polymers used for flexible plastic packaging become trapped in the recycling machine, creating interruption and increasing manufacturing costs and time.

Plastic Films and Sheets Market Segment Analysis (2026–2032)

By Material Type

The Polyethylene (PE) segment dominated the Plastic Films and Sheets Market in 2025 and is expected to maintain its dominance during the 2026–2032 forecast period. Polyethylene is widely used in film and sheet production due to its excellent flexibility, durability, moisture resistance, and cost-effectiveness. Within polyethylene, LLDPE (Linear Low-Density Polyethylene) is extensively utilized because of its high tensile strength, superior puncture resistance, and enhanced impact resistance compared with conventional LDPE materials. These properties make LLDPE highly suitable for packaging films, agricultural films, and stretch films.

LLDPE films can be produced through both blown and cast extrusion processes, providing strong mechanical performance while maintaining flexibility. Due to its lower manufacturing cost and improved performance characteristics, LLDPE is increasingly replacing traditional LDPE in various applications such as food packaging, retail bags, textile packaging, and agricultural films.

The HDPE (High-Density Polyethylene) segment is also expected to experience steady growth during the forecast period. HDPE sheets offer several advantages including high chemical resistance, corrosion resistance, excellent electrical insulation, moisture resistance, and high impact strength. These characteristics make HDPE suitable for industrial and packaging applications. Additionally, HDPE is approved for food-contact applications, supporting its extensive use in food packaging and processing industries. The increasing use of polyethylene-based materials in packaging and agricultural applications is expected to drive segment growth throughout the forecast period.

By Product Type

The Plastic Films segment held the largest share of the Plastic Films and Sheets Market in 2025 and is projected to maintain its dominance during the 2026–2032 forecast period. Plastic films are widely used due to their lightweight nature, flexibility, and excellent barrier properties. These films are commonly used in applications such as stretch films, shrink films, barrier films, and agricultural films, particularly in packaging and agricultural sectors.

Plastic films are widely utilized as protective barriers that prevent contamination from moisture, gases, dust, and microorganisms, thereby extending product shelf life. Their ability to provide high clarity, durability, and cost-efficient packaging solutions has increased their adoption across food packaging, consumer goods packaging, and industrial packaging.

The Plastic Sheets segment is also expected to witness steady growth during the forecast period. Plastic sheets are commonly used in industrial and construction applications due to their strength, durability, and resistance to chemicals and corrosion. These sheets are widely used in applications such as thermoformed products, protective panels, and industrial components. Increasing demand from construction, automotive, and electronics industries is expected to support the growth of plastic sheets during the forecast period.

Plastic Films and Sheets Market Regional Insights:

Asia Pacific dominated the global Plastic Films and Sheets Market in 2025, accounting for 36–38% of the total market revenue and is expected to maintain its leadership while registering the highest CAGR during the 2026–2032 forecast period. The region remains the largest and fastest-growing market due to rapid industrialization, expanding manufacturing activities, and rising demand from key end-use industries such as packaging, construction, agriculture, electronics, and healthcare.

Growth is primarily driven by developing economies including China, India, Indonesia, Vietnam, Malaysia, and Thailand, where increasing urbanization and rising disposable income are boosting demand for packaged food and consumer goods. Changing consumer lifestyles and the expansion of organized retail and e-commerce are further accelerating the adoption of flexible packaging solutions. The growing food and beverage sector, along with rapidly expanding pharmaceutical and healthcare industries in China and India, is significantly contributing to demand for plastic films used in packaging and medical applications.

Additionally, strong manufacturing bases in China, South Korea, Taiwan, and Japan in electronics and electrical equipment, along with India’s expanding chemical and petrochemical sector and government initiatives promoting manufacturing investments, are supporting regional market growth. Rapid urbanization, infrastructure development, and agricultural modernization across countries such as India, Vietnam, Indonesia, and the Philippines are expected to further strengthen market demand during the forecast period.

North America held the second-largest share of the global Plastic Films and Sheets Market in 2025 and is expected to grow steadily during the 2026–2032 forecast period. Market growth in the region is primarily supported by strong demand from packaging, pharmaceutical, personal care, and consumer goods industries. Packaging remains the largest application segment, driven by the increasing demand for lightweight and high-performance flexible packaging solutions, particularly in the food and beverage industry.

The growing demand for personal care and cosmetic products in these countries is also expected to positively influence the market. In addition, rising investments in pharmaceutical research and development and the increasing demand for medical packaging solutions are expected to support product demand across the region. Furthermore, regulatory emphasis on recyclable and sustainable packaging materials is encouraging innovation and the development of advanced polymer films, which is expected to contribute to the continued growth of the Plastic Films and Sheets Market in Europe throughout the forecast period.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 14 May 2025 | Jindal Poly Films Ltd. | Announced a ₹700 crore investment to expand its Nashik facility with new BOPP, PET, and CPP film production lines. | Strengthens flexible packaging film production capacity and supports rising demand from food, personal care, and pharmaceutical packaging industries. |

| 01 July 2025 | Dow Inc. | Launched INNATE™ TF 220 Precision Packaging Resin to enable production of recyclable BOPE plastic films for flexible packaging. | Supports the industry’s transition toward a circular economy and recyclable plastic film packaging solutions. |

| 02 September 2025 | Xampla | Raised $14 million in funding to scale production of plant-protein-based biodegradable packaging films as alternatives to conventional plastics. | Accelerates development of sustainable and biodegradable film materials for food and consumer goods packaging. |

| 12 October 2025 | Intertape Polymer Group (IPG) | Introduced a new automotive-grade plastic sheeting product line designed for vehicle protection and industrial transport. | Expands the use of protective plastic films and sheets in automotive manufacturing and logistics. |

| 22 January 2025 | Polyplex Corporation | Announced a ₹558 crore investment to build a new BOPET film manufacturing plant to expand global production capacity. | Enhances supply of high-performance polyester films widely used in packaging, electrical insulation, and industrial applications. |

Plastic Films and Sheets Industry Ecosystem

Plastic Films and Sheets Market Scope: Inquire before buying

| Plastic Films and Sheets Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 149.37 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.5% | Market Size in 2032: | 203.28 USD Billion |

| Segments Covered: | by Material Type | Polyethylene (PE) Low-Density Polyethylene (LDPE) Linear Low-Density Polyethylene (LLDPE) High-Density Polyethylene (HDPE) Polypropylene (PP) Polyvinyl Chloride (PVC) Polyethylene Terephthalate (PET) Polystyrene (PS) Other Materials |

|

| by Product Type | Plastic Films Stretch Films Shrink Films Barrier Films Agricultural Films Plastic Sheets Rigid Plastic Sheets Flexible Plastic Sheets Thermoformable Sheets |

||

| by Technology | Extrusion Technologies Blown Film Extrusion Cast Film Extrusion Thermoforming Calendaring Co-extrusion |

||

| by End User | Food and Beverage Industry Pharmaceutical and Healthcare Industry Agriculture Industry Construction Industry Automotive Industry Consumer Goods Industry Electronics Industry Others |

||

Plastic Films and Sheets Market By Region:

Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Malaysia, Vietnam, Thailand, Taiwan, Bangladesh, Pakistan and Rest of Asia Pacific)

North America (United States, Canada and Mexico)

Europe (Germany, UK, France, Italy, Spain, Sweden, Netherlands, Switzerland and Rest of Europe)

Middle East and Africa (South Africa, Saudi Arabia, UAE, Qatar, Egypt, Nigeria and Rest of Middle East and Africa)

South America (Brazil, Argentina and Rest of South America)

Plastic Films and Sheets Market Key Players

1. Amcor PLC.

2. Berry Global Group, Inc.

3. SABIC

4. Toray Industries, Inc.

5. Sealed Air Corporation

6. Uflex Limited

7. Toyobo Co., Ltd.

8. Jindal Poly Films Limited

9. DuPont Teijin Films

10.Oben Holding Group

11.British Polythene Ltd.

12.SABIC

13.Plastic Film Corporation of America

14.Sealed Air

15.Dow

16.Novolex

17.Griffon Corporation Inc.

18.Mitsuibishi Chemical Holdings Corporation

19.Evonik Industries AG

20.Honeywell International Inc.