Organic Wine Market Size by Type, Packaging, Distribution Channel, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

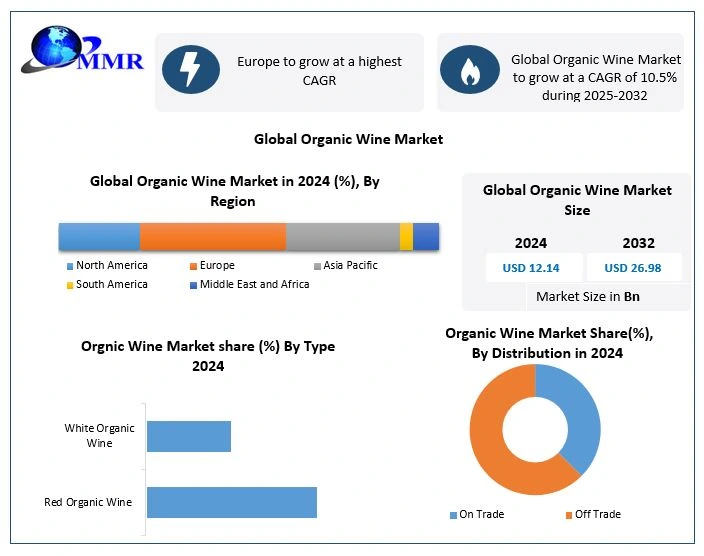

Organic Wine Market size was valued at USD 12.14 Bn in 2024, and the Global Organic Wine Market revenue is expected to grow at 10.5% from 2025 to 2032, reaching nearly USD 26.98 Bn.

Organic Wine Market Overview:

Organic wine is made with vine-grown grapes without synthetic pesticides and fertilizers. It meets strict certification standards, e.g., USDA Organic or EU Organic, to ensure environmentally sustainable growing and winemaking. The organic wine market has been driven by the shift towards organic winemaking practices, such as natural yeasts, no added synthetic materials, and sustainable vineyard management. The trend is also influenced by certifications and innovation in production and appeals to health and environment-conscious consumers and the use of sustainable winemaking practices, such as organic and biodynamic practices, is capitalizing on growing consumer confidence in health- and environmentally sustainable products, driving market growth and premium price opportunity. Segmentation of packaging bottles, cans and others, supports convenience and sustainability trends appealing to various buying groups such as environmentally aware millennials or convenience-oriented consumers. The company Banfi and Boisset are at the forefront of developing the organic wine segment by embracing sustainable practices, such as Banfi's partnership with 1% for the Planet to promote regenerative farming and Boisset's organic and biodynamic certifications of its vineyards, targeting environmentally conscious consumers. Europe is the leading market 35% share due to strong organic vineyard development in France, Italy, and Spain, and strong demand for health-oriented and sustainable wines from consumers. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Organic Wine Market Dynamics

Winemaking Methods Modifications to Drive the Organic Wine Market

Winemaking Methods Modifications to Drive the market for the organic wine market. Within the food and beverage industry, there are changing consumer trends and growing awareness of specialised product categories like organic and natural. Natural and organic food items have seen significant growth in popularity over the past ten years, especially among millennials. The push for natural food and drink is primarily fueled by consumers' declining interest in agricultural practices dependent on chemicals. Currently, organic wine is becoming more and more popular in the beverage sector, especially in wine-consuming nations like Australia, New Zealand, France, Italy, Argentina, etc. In addition to being fueled by sustainable vineyard practices, the market for organic wine is also expected to increase favourably as a result of minimalist and manipulative winemaking methods.

High cost and lack of regulatory authority restrain the Organic Wine Market

The high cost and lack of regulatory authority for the production of organic wine are expected to restrain market growth. The expense of organic viticulture is frequently higher than the majority of vineyards managed conventionally, and as a result, the wines are typically more expensive. Extremely bad weather, unexpected fungal diseases, or pests severely harm a crop for the year in the absence of preventative sprays. This explains why organic viticulture is more common in warm, dry regions and less common in cooler, wetter ones. Since getting certified is expensive, many smaller producers choose to maintain their vines organically.

Adoption of sustainable winemaking methods creates Market Opportunities

The adoption of sustainable winemaking methods has had a significant impact on the shift to organic wines, and the trend is expected to continue over the course of the forecast period. Another element that is likely to be important in driving up the sales of organic wine in the coming decade is a large increase in the number of wine exhibits and expos. The rise in the world organic wine market is expected to benefit from the increased attention on biodynamic farming techniques, as academics, retailers, government organisations, wineries, and farmers place more emphasis on improving soil health and reducing total carbon footprint.

Organic Wine Market Segment Analysis

Based on Type, The Organic Wine Market is segmented into Red Organic Wine and White Organic Wine In this segments, red organic wine dominates the market in 2024 and is expected to dominate the market in the forecast period. Red organic wines are produced by fermenting red or black grapes with yeast. In vineyards with organic certification, the grapes are grown organically. The European region is where the majority of the vineyards are found. Most of the world's organic vineyards are located in nations like Italy, France, and Germany. Red wine consumption is believed to decrease cholesterol and prevent human cancer. When compared to organic red wines, white wines are consumed less frequently. One of the most widely consumed white wines in the world is Chardonnay Champagne. The world's biggest market for white organic wine is Germany. Compared to red organic wines, white organic wines are less expensive, but they are less healthful.

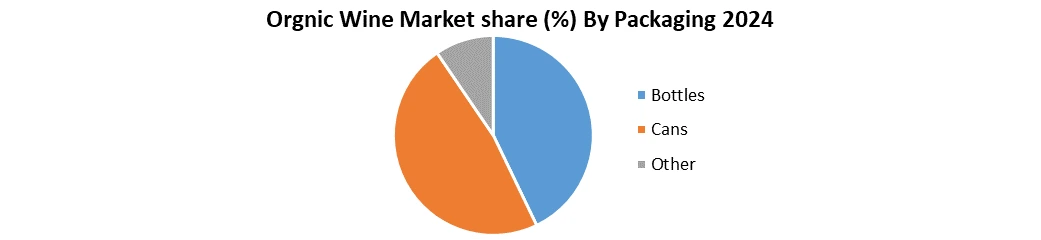

Based on packaging, the Organic Wine Market is segmented into Bottles, Cans and Others. In these segments, bottles dominated the market in 2024 and is expected to dominate the market in the forecast period. For organic wines, glass bottles are the preferred packaging type. Additionally, they are often utilised in beverage packaging. The third most popular packing material is glass. Since glass is recyclable, reusable, and inert, it is frequently used for wine packaging. Unlike plastic bottles and cans, they keep wines for a long period due to its inert nature. In the beverage business, cans are being used more and more. Cans made of metal, such as steel and aluminium, are frequently used in the packaging of carbonated beverages. Because cans are more portable and practical than bottles, canned wines are becoming increasingly popular. Aluminium cans are lighter than glass bottles, which reduces the amount of carbon dioxide released during transportation from the vineyard to the distributors. In response, this has increased demand for organic wine packaging that is environmentally friendly.

Based on distribution channel, the Organic Wine Market is segmented into On-trade and Off-trade. In this segment, Off-trade dominates the market in 2024 and is expected to dominate the market in the forecast period. Wine merchants, supermarkets, hypermarkets, retail establishments, caterers, organic stores, and e-commerce platforms are some examples of off-trade distribution channels for organic wine. The segment is expected to develop as a result of consumer preference for e-commerce. The nationwide lockdown increased the market for off-trade sales of organic wines.

Organic Wine Market Regional Insights

Europe Region Dominated the Organic Wine Market due to the High Demand for Wine in Europe

The majority of organic wine is consumed in European nations. The European continent, which has long been a popular destination for wine lovers due to the strong wine cultures found in Spain, Italy, and even the Nordic nations, is expected to offer a wealth of prospects for producers competing in the present organic wine market. Ecological wine, commonly referred to as organic wine, is free of artificial pesticides, weed killers, and fertilisers. As customers continue to demand transparency from food & beverage manufacturers regarding ingredients, production or manufacturing procedures, nutritional content, etc., the "free-from" trend has accelerated significantly throughout the European region.

The objective of the report is to present a comprehensive analysis of the Organic Wine Market to the stakeholders in the industry. The past and current status of the industry, with the forecasted market size and trends, are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analysed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Organic Wine Market dynamics, structure by analysing the market segments and projecting the Organic Wine Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Organic Wine Market makes the report an investor’s guide.

Organic Wine Market Competitive Landscape:

Banfi and Boisset, are the two topmost companies in the Organic Wine Market. Banfi Vintners, a premier Italian winery, has a focus on sustainable viticulture and makes organic wines under its Natura label, including varietals such as Sauvignon Blanc, Rosé, Pinot Noir, and Cabernet Sauvignon, at an affordable price of $14.99 a bottle. Its offerings run the gamut from Tuscan classics such as Brunello di Montalcino and Chianti to terroir-based production. Boisset Family Estates, a Franco-American clan, owns Burgundy (e.g., Jean-Claude Boisset) and California (e.g., Raymond Vineyards, DeLoach) biodynamic and organic vineyards. Its wines, including Burgundy's Clos de la Roche Grand Cru and Napa biodynamic wines, boast state-of-the-art techniques such as lunar-cycle farming and solar-power facilities. Both are eco-friendly winemakers but differ in regional focus. Banfi is well-positioned in Italian organic wines, and Boisset blends Old-World tradition and New-World green approaches.

Organic Wine Market Key Trends

| Trends | Details |

| Health‑and‑wellness-driven innovations | • Demand is rising for low alcohol and no alcohol organic wines, catering to health-conscious and moderation-focused consumers • Organic red wines hold the dominant market share (60%), with white wines growing faster (CAGR 9–10%) as lighter vintages gain interest. |

| Sustainable, eco-friendly packaging & convenience formats | • Growth in organic sparkling and canned wines appeals to younger generations seeking portability and sustainability • Innovations include lightweight glass, biodegradable corks, recycled labels, and non glass options like cans and boxes |

| Climate & cost pressures | • Climate change, unpredictable weather, pests, and higher costs pose significant challenges for organic producers • Still, seasoned organic viticulturists report yields comparable to conventional farms, and some even see stronger profitability thanks to premium positioning |

Organic Wine Market Key Developments

| Year | Company Name | Recent Development |

| February 3,2024 | Banfi Vintners (USA) | Joined 1% for the Planet, pledging 1% of Natura (organic wine) sales in the U.S. to support Rodale Institute’s regenerative organic agriculture research and education. |

| March 21, 2023 | Boisset Family Estates (France) | Extended use of eco-packaging formats like Tetra Pak, PET bottles, and reusable bag-in-barrel packaging for lower carbon emissions and consumer awareness in Europe and the U.S |

| November 22, 2023 | Casella Wines Pty. Ltd.(Australia) | Through its subsidiary Australian Beer Co., acquired the Ampersand brand, expanding into ready-to-drink and spirits segments — enabling future diversification of organic or sustainable lines. |

| September 15, 2024 | Avondale (South Africa) | Became a founding member of Organic Wines South Africa, uniting certified-organic estates to promote and educate on organic wine standards in the country. |

| August 5, 2024 | Viña Concha y Toro SA (Chile) | Successfully recertified as a B-Corp, achieving a score of 93.9, reflecting environmental, social, and ethical wine practices including organic farming, low water use, and eco-packaging. |

Organic Wine Market Scope: Inquire before buying

| Organic Wine Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 12.14 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 10.5% | Market Size in 2032: | USD 26.98 Bn. |

| Segments Covered: | by Type | Red Organic Wine White Organic Wine |

|

| by Packaging | Bottles Cans Others |

||

| by Distribution Channel | On-trade Off-trade |

||

Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Taiwan, Indonesia, Philippines, Malaysia, Vietnam, Thailand, Rest of Asia Pacific region)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Organic Wine Market Key Players

North America

1. Banfi Vintners (Old Brookville, New York, USA)

2. Bronco Wine Co. (Ceres, California, USA)

3. Charlie and Echo (San Diego, California, USA)

4. Frey Vineyards (Redwood Valley, California, USA)

5. Grgich Hills Estate (Rutherford, California, USA)

6. Jackson Family Wines Inc. (Santa Rosa, California, USA)

7. King Estate Winery (Eugene, Oregon, USA)

8. The Organic Wine Co. (San Rafael, California, USA)

9. Wine Cellar Group (Elmsford, New York, USA)

10. Dry Farm Wines (Napa, California, USA)

11. Winc Inc. (Los Angeles, California, USA)

Europe

1. Boisset Family Estates (Nuits-Saint-Georges, France)

2. Boutinot Ltd. (Stockport, England, UK)

3. Grands Vignobles En Mediterranee SARL (Languedoc-Roussillon, France)

4. Vintage Roots Ltd. (Hampshire, England, UK)

5. Elgin Ridge Wines (Originally South Africa)

Asia Pacific

1. Casella Wines Pty. Ltd. (Yenda, New South Wales, Australia)

2. Harris Organic Wines (Swan Valley, Western Australia, Australia)

3. Organic Wine Pty Ltd (Australia)

4. Radford Dale Pty Ltd (Stellenbosch, South Africa)

5. Mount Avoca (Avoca, Victoria, Australia)

6. Tamburlaine Organic Wines (New South Wales, Australia)

Middle East & Africa

1. Avondale (Paarl, Western Cape, South Africa)

2. Radford Dale Pty Ltd (Stellenbosch, Western Cape, South Africa)

South America

1. Vina Concha y Toro SA (Santiago, Chile)

2. Emiliana Organic Vineyards (Casablanca Valley, Chile)

FAQs:

1. Which is the potential market for the Organic Wine Market in terms of the region?

Ans. In the Europe region, the growing business and educational sectors are expected to help drive the use of collaborative screens.

2. What are the opportunities for new market entrants?

Ans. The key opportunity in the market is new initiatives from governments that provide funding for Organic Wine Markets in educational institutes

3. What is expected to drive the growth of the Organic Wine Market in the forecast period?

Ans. A major driver in the Organic Wine Market is the prevalence of work from home and remote collaboration created by the COVID-19 pandemic

4. What is the projected market size & growth rate of the Organic Wine Market?

Ans. The Organic Wine Market size was valued at USD 12.14 Bn in 2024, and the total Organic Wine Market revenue is expected to grow at 10.5% from 2025 to 2032, reaching nearly USD 26.98 Bn.

5. What segments are covered in the Organic Wine Market report?

Ans. The segments covered are Type, Packaging, Distribution Channel and Region.