Metal Powder Market by Material, Technology, End-use Industry and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

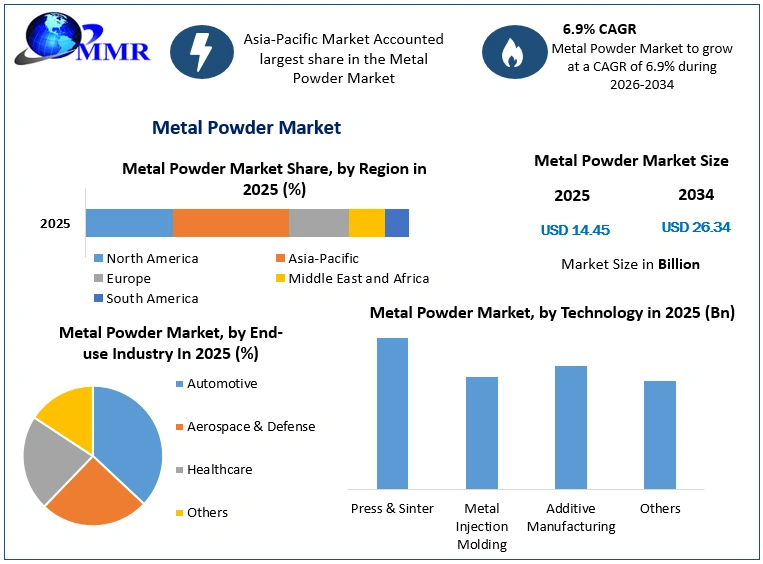

The Metal Powder Market is set to grow at a CAGR of 6.9%, reaching USD 14.45 Bn. by 2034, from USD 26.34 Bn., fueled by demand for 3D printing and lightweight components.

Metal Powder Market Overview

Metal powder refers to finely divided solid particles of metals or alloys, typically ranging in size from a few micrometers to a few millimeters. It is produced through various methods like atomization, reduction, or electrolysis and is used in applications such as additive manufacturing, powder metallurgy, and coatings.

The metal powder market is experiencing strong growth, driven primarily by the rising demand from the additive manufacturing (3D printing) and automotive industries, where lightweight and high-performance materials are essential. Asia-Pacific dominates the market, led by China and India, due to rapid industrialization, government initiatives like "Make in India," and expanding automotive production. Key growth drivers include the shift toward eco-friendly manufacturing and the rising use of metal injection moulding (MIM). An emerging trend is the development of nanostructured metal powders for enhanced mechanical properties, alongside increasing investments in recyclable and sustainable metal powders to meet environmental regulations. The U.S. Department of Energy highlights the role of metal powders in reducing energy consumption in manufacturing, further boosting market prospects.

The reports also help in understanding the Global Metal Powder Market dynamics and structure by analysing the market segments and projecting the Global Metal Powder Market size. Clear representation of competitive analysis of key players by Distribution Channel, price, financial position, product portfolio, growth strategies, and regional presence in the Metal Powder Market makes the report an investor’s guide.

Metal Powder Market Size, Growth & Share Analysis

To know about the Research Methodology:-Request Free Sample Report

Global Metal Powder Market Dynamics

Sustainability Trend Supporting Additive Manufacturing

Market participants are embracing green manufacturing to lower overall operating costs by utilizing energy-efficient processes that can significantly lower energy and electricity bills. Aerospace, automotive, viscosifiers, medical, building & construction, etc., are just a few industries that share a concern for green manufacturing. Additionally, regional governments have implemented limitations on carbon dioxide emissions, which ultimately improves the overall efficiency of a facility that uses metal powder to create customized items in response to particular demand. Therefore, owners of medium- to large-scale industries are concentrating on employing green energy in their metal powder operations.

Demand in the Metal Fabrication Industry is Growing Rapidly

Metal fabrication industries are being forced to increase their production capacities in order to take advantage of the enormous opportunity that has been created in the market by the growing demand for various metal-fabricated components across a wide range of end-use industries such as automotive, aerospace, construction, and various others.

But the lengthy lead times of conventional production methods have long been a hindrance to the growth of the metal fabrication sector. The metal fabrication sector is dependent on cutting-edge production techniques, including powder metallurgy, additive manufacturing, and a few others, to seize the market opportunity. The Metal Powder market is expected to grow significantly during the forecast period due to such production methods and the raw materials used in these production processes, including metal powder.

Metal powder sales are benefited by the need for lightweight components

Manufacturers must make a large investment in R&D to create their products and thrive in a competitive world, where the competitive environment is constantly getting more intense. Previously unnoticed small details are now being paid attention to by manufacturers. Growth in the market now heavily depends on innovation and development.

The need for lightweight components with excellent accuracy is therefore constantly growing in all end-use sectors. To give their customers fuel-efficient options, the automotive and aerospace industries are leading the way in increasing demand for lightweight components. The great accuracy demanded by end-use industries, however, is not achievable with standard production techniques for such lightweight components.

Modern manufacturing techniques, such as 3D printing, additive manufacturing, and laser cladding, have been developed to produce these components efficiently and at relatively low production costs.

Asia Pacific has Access to Low-Cost, Subpar Metal Powder Manufacturing.

The Asian market is distinguished by the existence of a sizable number of competitors who offer items that are adapted to suit customer demand and have highly established sales and distribution networks throughout MEA, APEJ, and Latin America.

The SME sector, which typically looks for low-investment solutions, is the main driver in these regions. Chinese competitors frequently succeed in providing items at relatively low prices because of intense competition, the affordability of resources, and advantageous trade policies.

As a result, it is challenging for numerous American and European businesses to retain their respective profit margins in these markets while producing high-quality metallic powder with strict safety and operational requirements.

China produces metal powder at a lower cost than nations like the United States, Germany, and Japan. As a result, the majority of clients opt to import parts from China. The dominance of Chinese producers forces international players to operate on thin profit margins, which hinders their overall performance. As a result, metal powder sales are expected to decline globally during the forecast period.

Metal Powder Market Segment Analysis

The Metal Powder Market is segmented by Material, Technology, and End-use Industry.

Based on the Material, the market is segmented into ferrous and Non-ferrous. The ferrous material segment is expected to hold the largest market share of xx% by 2034. The ferrous segment consists of metal powders made of iron, all forms of steel, and their alloys, as well as nickel, molybdenum, and chromium, which are used as alloying agents. When using additive manufacturing, steel is one of the least expensive metal types. It may also be combined with other metals, such as bronze, for special purposes.

The non-ferrous material segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. Metal powders composed of aluminium, copper, zinc, titanium, tungsten, magnesium, and other materials are included in the non-ferrous segment. The need for aluminium is expected to rise due to its qualities, including strength and lightweight. Manufacturing machinery, including functional parts and cycles, uses aluminium. Direct metal laser sintering is used in 3D printing to produce equipment made of aluminium. It is expected that the growing interest in titanium implants in the healthcare sector would help the segment flourish. To correct deformations in the human skull, bones, and vertebrae, organizations like Novax DMA and CEIT Biomedical Engineering have entered the production of titanium-based medical implants.

Based on the Technology, the market is segmented into Press & Sinter, Metal Injection Molding, Additive Manufacturing, and Others. Press & Sinter Technology segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. The traditional powder metallurgy procedure is press and sinter. It creates components that are nearly net-shape and are economical. To create a green compact, thermal treatment or compaction at a temperature below the melting point of metal is required.

This aids in strengthening components by metallurgical glueing the particles together. Additionally, green compact undergoes controlled-environment sintering, where metallurgical bonding creates the finished components. To achieve tight tolerances and a superior surface quality, secondary procedures including plating, repressing, and grinding are carried out.

The Metal Injection Molding Technology segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. Over the past 20 years, metal injection moulding (MIM) has been increasingly significant in the components manufacturing sector. This procedure utilises the shaping and sintering of metal particles, much as pressing and sintering. With this technique, a large number of intricately shaped pieces can be produced with excellent manufacturing accuracy. Injection moulding, binder removal, sintering, and mixing or preparation of feedstock Are some of the phases in the MIM process.

Based on the End-use Industry, the market is segmented into Automotive, Aerospace & Defence, Healthcare, and Others. The Automotive End-use Industry segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. One of the largest users of metal powder is the automobile industry, which produces a variety of parts through the use of procedures like hot isostatic pressing (HIP), additive manufacturing (AM), press and sinter, and metal injection moulding (MIM). When it comes to the production of auto parts, the press and sinter method is dominant in the automotive application segment. In contrast to the press and sinter, other processes, including AM, HIP, and MIM, are witnessing faster penetration.

The Healthcare End-use Industry segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. The healthcare end-use industry segment is expected to be driven by growing consumer health awareness and increased customer willingness to pay more for finished products. Additionally, the healthcare end-use industry segment is driven by powder metal technologies, which are utilised to make connecting plates, foot adaptor plates, blacking plates, operation blades, forceps, graspers, and blacking hooks.

Metal Powder Market Regional Insights

The Asia Pacific region is expected to dominate the Metal Powder Market during the forecast period 2026-2034. The Asia Pacific region is expected to hold the largest market share of xx% by 2034. China has the second-largest economy in the world. The country is also expected to use metal powder at a second-place global level. The unusual density of end-use industries in the country significantly contributes to the increase in metal powder sales.

China is considered a global manufacturing powerhouse and is among the top producers of a few key end-use markets for powdered metal, including electronics, automotive, infrastructure, and manufacturing.

The North American region segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. The need for various sintered parts in transmissions and engines in the region has mostly dropped as electric and hybrid vehicles have become more and more common. However, it is expected that market sellers would have attractive chances during the forecast period due to powder forging technology. According to the Metal Powder Industries Federation, the powder forging method is used to create roughly 30% of the connecting rods used in vehicle production globally.

Metal Powder Market Competitive Landscape

The global metal powder market is highly competitive and moderately fragmented, with key players focusing on innovation, strategic partnerships, and capacity expansion to strengthen their market presence. Leading companies such as Höganäs AB, Carpenter Technology Corporation, Sandvik AB, and GKN Hoeganaes Corporation dominate due to their wide product range and strong global distribution networks. In 2025, Höganäs held an estimated 12–14% market share globally, followed by Carpenter Technology with 8–9%. Rising demand from additive manufacturing, particularly in aerospace and medical industries, has driven companies like ATI and Elementum 3D to invest in high-performance alloy powders and advanced production technologies.

Asian players such as CNPC Powder Group and Daido Steel Co., Ltd. are expanding aggressively, especially in 3D printing and automotive sectors, benefiting from growing domestic manufacturing. Meanwhile, collaborations like the Sandvik-Renishaw alliance on titanium powder for medical implants are shaping a more innovation-driven landscape.

Metal Powder Market Key Trends

• Rise of Additive Manufacturing

The 3D printing sector is a major driver for metal powders, particularly in aerospace and medical implants. The U.S. Air Force has invested $100 million in metal AM for lightweight aircraft components, while GE Additive reports a 30% annual growth in metal powder usage for jet engine parts. Government initiatives like America Makes further accelerate adoption.

• Sustainable & Recycled Metal Powders

Environmental regulations are pushing manufacturers toward green production methods. The EU’s Horizon Europe program has allocated €2 billion for sustainable material innovation, including metal powder recycling.

• AI and Automation in Powder Production

Smart manufacturing is optimising metal powder quality and reducing waste. Germany’s Fraunhofer Institute has developed AI-based particle size analysers, cutting inspection time by 70%. Sandvik’s fully automated powder plants use machine learning to ensure consistency, boosting output by 25%.

Metal Powder Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 27 February 2025 | Metal Powder Works | Metal Powder Works merged with K-Tig Advanced Welding Systems in an A$10 million deal to scale its proprietary DirectPowder™ production process. | The merger accelerates commercial supply of high-yield, cost-effective aluminum and copper powders for defense and advanced manufacturing applications. |

| 24 June 2025 | Sandvik AB | Sandvik formed a powder supply partnership with Additive Industries for direct filling via the Powder Load Tool (PLT). | The collaboration improves operator safety, material traceability, and bulk handling efficiency for users of Osprey® metal powders on MetalFab 3D printers. |

| 15 July 2025 | Continuum Powders | Continuum Powders entered into a long-term supply agreement with Revolutionary Technologies (Rev-Tec) for sustainable defense additive manufacturing. | The agreement provides over 20 tons of recycled-content metal powder produced via Melt-to-Powder (M2P) atomization technology. |

| 13 August 2025 | Sandvik AB | Sandvik launched Osprey® MAR 55, a new tool steel metal powder designed for additive manufacturing. | The alloy bridges the performance gap between maraging and carbon-bearing steels, offering ultra-high strength and high weldability in the as-built state. |

| 27 March 2026 | 6K Additive | 6K Additive secured a $1.1 million purchase order from a major OEM for its sustainably produced Nickel 718 superalloy powder. | The order validates commercial demand for high-purity, lower-carbon plasma-upcycled superalloy powders used in critical aerospace and energy components. |

| 03 June 2026 | Sandvik AB | Sandvik introduced Osprey® GRCop-42, a high-conductivity copper alloy powder featuring full cradle-to-gate material traceability. | The specialized powder reduces qualification risk and enables additive production of high-heat components for demanding space and aerospace applications. |

Metal Powder Market Scope: Inquire before buying

| Metal Powder Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 14.45 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 6.9% | Market Size in 2034: | USD 26.34 Bn. |

| Segments Covered: | by Material | Ferrous Non-ferrous |

|

| by Technology | Press & Sinter Metal Injection Molding Additive Manufacturing Others |

||

| by End-use Industry | Automotive Aerospace & Defense Healthcare Others |

||

Metal Powder Market, by region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Russia, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Philippines, Malaysia, Vietnam, Thailand, Rest of Asia Pacific)

Middle East and Africa (South Africa, Saudi Arabia, UAE, Rest of the Middle East &Africa)

South America (Brazil, Argentina, Rest of South America)

Metal Powder Market Key Players

North America

1. Carpenter Technology Corporation (United States)

2. GKN Hoeganaes Corporation (United States)

3. Praxair Surface Technologies (United States)

4. ATI – Allegheny Technologies Inc. (United States)

5. 6K Inc. (United States)

Europe

6. Höganäs AB (Sweden)

7. BASF SE (Germany)

8. Heraeus Holding GmbH (Germany)

9. Renishaw plc (United Kingdom)

10. Aubert & Duval (France)

11. Deutsche Edelstahlwerke (Germany)

12. Ecka Granules GmbH (Germany)

Asia Pacific

13. JFE Steel Corporation (Japan)

14. Mitsubishi Chemical Group (Japan)

15. Daido Steel Co., Ltd. (Japan)

16. Sumitomo Electric Industries, Ltd. (Japan)

17. CNPC Powder Group Co., Ltd. (China)

18. Changsha Hualiu Metal Powders Ltd. (China)

19. MMP Industries Ltd. (India)

Middle East and Africa

20. Powders for Africa (South Africa)

21. Emirates Steel Arkan (United Arab Emirates)

22. Kimetsan Group (Turkey)

South America

23. CBMM (Brazil)

24. Gerdau Graphene (Brazil)

25. CIA. General de Carbureto (Argentina)

Frequently Asked Questions:

1] Which region is expected to hold the highest share in the Metal Powder Market?

Ans. The Asia Pacific region is expected to hold the highest share in the Metal Powder Market.

2] Who are the top key players in the Metal Powder Market?

Ans. The leading players in the global metal powder market in 2026 include Höganäs AB, Carpenter Technology Corporation, GKN Hoeganaes Corporation, Sandvik AB, ATI – Allegheny Technologies Inc., and CNPC Powder Group Co., Ltd.

3] Which segment is expected to hold the largest market share in the Metal Powder Market by 2034?

Ans. The ferrous material segment is expected to hold the largest market share in the Metal Powder Market by 2034.

4] What is the market size of the Metal Powder Market by 2034?

Ans. The market size of the Metal Powder Market is expected to reach USD 26.34 Bn. by 2034.

5] What was the market size of the Metal Powder Market in 2025?

Ans. The market size of the Metal Powder Market was worth USD 14.45 Bn. in 2025.