Industrial Gas Turbine Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

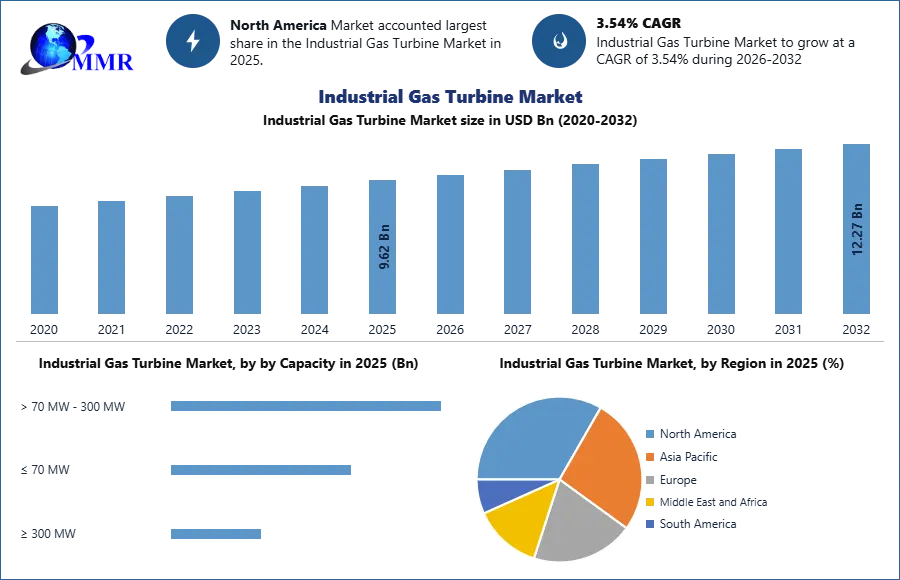

Industrial Gas Turbine Market was valued at USD 9.62 Bn in 2025 and is expected to reach USD 12.27 Bn by 2032, growing at a CAGR of 3.54% during the forecast period.

Industrial Gas Turbine Market Overview

An industrial gas turbine is a combustion engine that converts natural gas or other fuels into mechanical energy, which is then used to generate electricity or power industrial processes. These turbines are known for their high efficiency, low emissions, and flexibility in combined heat and power (CHP) systems.

The industrial gas turbine market is experiencing significant growth, driven by the rising demand for efficient and cleaner power generation solutions. Increasing industrialisation, coupled with stringent government regulations on emissions, is pushing industries to adopt gas turbines over coal-based plants. For instance, the U.S. Energy Information Administration (EIA) projects a 3.5% annual growth in gas turbine capacity additions by 2030, supported by policies like the Inflation Reduction Act (IRA).

North America and Asia-Pacific dominate the market, with North America leading due to shale gas abundance and government incentives for combined-cycle power plants. Meanwhile, Asia-Pacific is expanding rapidly, fueled by rising energy demands in China and India, where governments are investing heavily in gas infrastructure to reduce coal dependency.

An emerging trend is the use of AI and IoT for predictive maintenance, enhancing turbine efficiency and lifespan. Governments worldwide are also funding carbon capture (CCUS) projects, further boosting market prospects. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Global Industrial Gas Turbine Market Dynamics

Industrial Gas Turbine Market Driver

Gas Turbine Technology Reduces Greenhouse Emissions to Drive Industrial Gas Turbine Market Growth

Traditional coal-fired power plants are known to emit large amounts of toxic gases and contribute significantly to global warming. Coal-fired power plants are one of the major contributors to emissions. Rising greenhouse gas emissions create an urgency to develop cleaner methods of generating electricity, which is expected to increase demand for industrial gas turbines over the next decade. Natural gas, a primary fuel for gas turbines, contains very little sulfur, resulting in almost no sulfur dioxide emissions. The CO2 emissions from natural gas-fired gas turbines are also very low—0,37 kilograms of CO2 per kWh of electricity generated. This compares to 1.01 kg/kWh for lignite and 0.8 kg/kWh for anthracite. As a result, the factors listed above drive the growth of the industrial gas turbine market during the forecast period.

Growing Electricity Demand Accelerates Global Market Growth

The global increase, thriving industrial sector, and growth in infrastructure development activities have resulted in an enormous increase in demand for electricity. As the electricity demand grows, several countries around the world are increasing their capacity to generate electricity by building new plants or growing the capacity of existing ones! Companies are more inclined to adopt industrial gas turbine systems due to stringent government norms regarding greenhouse gas emissions. These factors augment the industrial gas turbine market growth during the forecast period.

Growing environmental concerns and stringent regulatory commitments to reduce GHG emissions have focused on energy conservation, which benefits the industrial gas turbine market. Gas turbines have emerged as a critical factor for power and heat delivery systems as environmental concerns have grown. In line with rapid technological developments in combustion, aerodynamics, matter, and cooling, ongoing changes in critical power markets have been critical to this development. Increasing cash flow to replace conventional energy systems with improved units would accelerate market demand even further. The power-to-weight ratio, modularity, and high power rating all play important roles in driving dynamics in the market. The recent shale trend has resulted in increased investment in research and drilling in inland and onshore remote basins, which complements business growth.

Natural gas price volatility to Create Restraint for the Industrial Gas Turbine Market

Natural gas prices are affected by actions that can disrupt natural gas research. Geopolitical tensions are a disruptive factor that creates uncertainty about gas availability and demand. This may result in increased volatility in gas prices. Gas prices in the United States have dropped dramatically as a result of shale gas extraction, but prices elsewhere in the world remain relatively high. The majority of the countries in the Middle East region have significant natural gas reserves. Because of political and cultural issues, it is a highly volatile region. Additionally, due to the COVID-19 pandemic, demand has increased in recent months. Natural gas prices have dropped significantly. Gas prices have fallen, which hurts the industrial gas turbine market.

Broader Scope in Emerging Economies to Create Industrial Gas Turbine Market Opportunity

The rise of industrial hubs and rising FDI in all major manufacturing sectors across emerging economies such as China, India, Brazil, and Southeast Asian countries is expected to create lucrative growth opportunities for this market during the forecast period. Various foreign developers interested in establishing businesses through FDI incentive schemes are focusing on emerging economies. This will indirectly boost the country's economy and accelerate industrialisation. To attract investments and enable growth, countries such as the United States and many Asian countries have evolved and restructured their manufacturing policies and procedures. Industrialisation will accelerate the automation process, increasing overall production efficiency and streamlining operations. As a result, it is possible to conclude that the expansion of the industrial sector, particularly in emerging economies, will provide an opportunity for the industrial gas turbine market.

The new contracts are occupying the attention of key participants

The industrial gas turbine market is highly fragmented, with several large-scale key players operating globally. This includes a group of four to five key companies with a broader geographic presence. Several companies are increasingly investing in organic and inorganic developments in order to strengthen their global market position. The firms are looking for new contracts in order to increase their market share. For example, in February 2022, GE began construction on six 34 MWLM250EXPRESS aero-derivative gas turbines that will replace a coal plant in Colorado.

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 03 February 2026 | Siemens Energy AG | Siemens Energy finalized a $1 billion investment plan to expand U.S. manufacturing for large gas turbines and grid solutions, including resuming turbine production in Charlotte, North Carolina. | This expansion addresses the surging power demand from data centers and AI infrastructure, strengthening the domestic supply chain for high-capacity power generation. |

| 28 January 2026 | GE Vernova | GE Vernova announced a $600 million investment to boost its heavy-duty gas turbine production to 80 units per year by 2026. | The strategic capital injection scales manufacturing capacity to fulfill an 80-GW backlog, ensuring reliable delivery of HA-class turbines for global utility projects. |

| 14 January 2026 | Mitsubishi Power | Mitsubishi Power secured a major contract to supply hydrogen-ready M701JAC gas turbines for Qatar’s 2.4 GW Facility E IWPP project. | The deployment marks the first use of JAC technology in Qatar, providing 20% of the national grid capacity with a pathway to low-carbon hydrogen co-firing. |

| 24 December 2025 | Mitsubishi Power / Mitsubishi Electric | The partners completed functional testing for a next-generation gas turbine control system capable of handling rapid load adjustments for renewable energy integration. | The system’s planned 2026 market launch will enable thermal plants to operate with higher flexibility, supporting the stability of grids with high intermittent renewable penetration. |

| 18 December 2025 | Ansaldo Energia | Ansaldo Energia was selected to supply its GT26 gas turbine for the Matra Power Plant in Hungary to support national energy security. | This project facilitates Hungary's decarbonization goals by replacing older assets with high-efficiency, flexible gas technology suitable for grid stabilization. |

| 03 March 2025 | GE Vernova | GE Vernova completed the acquisition of the gas turbine combustion parts business from Woodward, Inc. to secure its internal supply chain. | Vertical integration of critical combustion components allows the company to maintain production schedules amidst unprecedented growth in the heavy-duty turbine market. |

Industrial Gas Turbine Market Segment Analysis

In 2024, the > 70 MW – 300 MW segment holds the highest demand in the industrial gas turbine market. These turbines offer an optimal balance between power output, efficiency, and operational flexibility, making them widely suitable for power generation, oil & gas operations, and industrial manufacturing facilities. They are commonly deployed in combined cycle power plants and mid-scale industrial power stations where reliable and efficient energy supply is required. The ≤ 70 MW segment is also widely used, particularly in decentralized power generation and mechanical drive applications in the oil and gas sector. Meanwhile, the ≥ 300 MW segment is primarily utilized in large-scale utility power plants, where high-capacity electricity generation is required, though its deployment is more limited compared to mid-capacity turbines.

Based on technology, Heavy Duty gas turbines represent the most demanded segment in 2024 due to their high durability, long operational life, and suitability for continuous power generation in large industrial facilities and utility-scale power plants. These turbines are extensively used in base-load power generation and combined cycle systems because of their high efficiency and reliability. Aeroderivative turbines are witnessing growing demand due to their lightweight design, fast start-up capability, and higher operational flexibility, making them suitable for oil & gas operations and peak load power generation. Meanwhile, Light Industrial turbines are primarily used for smaller-scale power generation and mechanical drive applications in industrial plants.

Based on cycle type, the Combined Cycle segment dominates the industrial gas turbine market in 2024 due to its superior efficiency and ability to generate additional power by utilizing waste heat from gas turbines to produce steam. Combined cycle plants are widely used in large-scale electricity generation and utility power projects as they significantly reduce fuel consumption and emissions. In contrast, the Simple Cycle segment continues to play a vital role in peak load power plants, emergency power generation, and remote industrial facilities where quick start-up and operational simplicity are essential.

| Industrial Gas Turbine Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 9.62 USD Bn |

| Forecast Period 2026-2032 CAGR: | 3.54% | Market Size in 2032: | 12.27 USD Bn |

| Segments Covered: | by Capacity | > 70 MW - 300 MW ≤ 70 MW ≥ 300 MW |

|

| by Technology | Heavy Duty Light Industrial Aeroderivative |

||

| by Cycle | Simple Cycle Combined Cycle |

||

| by Sector | Electric Power Utility Oil & Gas Manufacturing |

||

Industrial Gas Turbine Market Regional Insights

Based on region, North America dominates the industrial gas turbine market in 2024 due to strong investments in natural gas–based power generation, advanced energy infrastructure, and the presence of leading turbine manufacturers. The region’s focus on replacing aging coal power plants with cleaner natural gas facilities further supports market demand. Asia Pacific is expected to experience significant growth driven by rapid industrialization, rising electricity demand, and expanding power infrastructure in countries such as China, India, and Southeast Asia. Europe maintains steady demand due to energy transition policies and modernization of power plants. Meanwhile, Middle East & Africa and South America show moderate growth supported by increasing energy projects, oil and gas infrastructure expansion, and rising electricity consumption.

Industrial Gas Turbine Market Competitive Landscape

The industrial gas turbine market in 2025 remains highly competitive, led by major players such as General Electric (GE), Siemens Energy, Mitsubishi Power, Rolls-Royce, and Ansaldo Energia. Together, these companies control more than 70% of the global market, leveraging their advanced turbine technologies, extensive global service networks, and established customer bases. GE has strengthened its position with a 29 GW order backlog and a $600 million investment in U.S. manufacturing to support AI-driven and hydrogen-capable turbines. Siemens Energy is increasing its local manufacturing footprint, notably in the Middle East, where it delivered Saudi Arabia’s first domestically assembled heavy-duty turbine. Mitsubishi Power is focusing on hydrogen-ready turbines, with new units supporting up to 50% blending, aiming for 100% capability by 2030.

Rolls-Royce and Ansaldo Energia are maintaining their competitiveness through innovations in efficiency and flexible operation. The market also sees growing competition from regional firms like Doosan Enerbility in South Korea and Harbin Electric in China. Competitive strategies include digital turbine optimisation, long-term service agreements, and carbon-reduction technologies. As demand grows for cleaner and more efficient energy solutions, innovation and localisation remain key factors shaping the evolving market landscape.

Industrial Gas Turbine Market Key Trends

• Shift to Hydrogen-Blended & Zero-Carbon Fuels

Governments and energy firms are investing heavily in hydrogen-compatible gas turbines to meet decarbonization goals. The European Commission’s Hydrogen Strategy targets 40GW of hydrogen-ready turbines by 2030.

• Digital Transformation and Advanced Analytics

Operators are implementing AI-driven monitoring systems to optimise performance and predict maintenance needs. These digital solutions are becoming standard for maximising turbine efficiency and lifespan.

• Growing LNG Infrastructure in Asia

Asia’s LNG expansion is a major turbine market driver. China aims to derive 15% of its energy from gas by 2030, requiring 200+ new gas-fired plants (NDRC). India’s LNG imports rose 25% in 2023, with plans to build 50GW of gas power capacity by 2032.

Industrial Gas Turbine Market Recent Development

Industrial Gas Turbine Market Scope: Inquire before buying

Industrial Gas Turbine Market, by region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Russia, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Philippines, Malaysia, Vietnam, Thailand, Rest of Asia Pacific)

Middle East and Africa (South Africa, Saudi Arabia, UAE, Rest of the Middle East &Africa)

South America (Brazil, Argentina, Rest of South America)

Key Players /Competitor Profiles Covered in the Industrial Gas Turbine Market Report from a Strategic Perspective.

- General Electric

- Solar Turbines – Caterpillar

- Siemens Energy Inc.

- PW Power Systems – Mitsubishi Heavy Industries

- Rolls-Royce North America

- Vericor Power Systems

- Siemens Energy AG

- Rolls-Royce plc

- Ansaldo Energia France

- Ansaldo Energia

- MAN Energy Solutions

- UEC-Aviadvigatel – United Engine Corporation

- Alstom SA

- Mitsubishi Power

- Kawasaki Heavy Industries

- Harbin Electric Corporation

- Dongfang Electric Corporation

- Shanghai Electric Group

- Doosan Enerbility

- Bharat Heavy Electricals Limited – BHEL

- Mubadala Energy

- Saudi Aramco

- Sasol

- Siemens Energy Brazil

- Industrias Juan F. Secco

- WEG S.A.

- Colbún S.A.