India Fertilizer Market by Type (Organic Fertilizer, Chemical Fertilizer, Mixed Fertilizers), Distribution Channel (Direct Sales, Retailers, Government Agencies and Cooperatives) - Forecast to 2030

Overview

The India Fertilizer Market size was valued at at INR 1046.85 Bn. in 2023 and the total India Fertilizer revenue is expected to grow at a CAGR of 5.7% from 2024 to 2030, reaching nearly INR 1543.15 Bn. by 2030.

The Indian fertilizer sector is vital for agricultural output and food security, offering nitrogenous, phosphatic, potassium, and organic fertilizers tailored to diverse soil and crop needs.

India's fertilizer is the production, distribution, and utilization of substances or formulations applied to soil or crops to promote plant growth and enhance agricultural productivity. The Indian fertilizer sector is crucial for sustaining agricultural output and food security in the country. The market includes various types of fertilizers, including nitrogenous, phosphatic, potassium, and organic fertilizers, catering to different soil and crop requirements.

India has one of the world's largest fertilizer industries, driven by substantial agricultural demand. The market has seen consistent growth, propelled by increased agricultural activity, government support, and technological advancements in the sector. The industry comprises both domestic production and significant imports to meet fertilizer demands. Supportive government policies, subsidies, and schemes like the Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) drive fertilizer usage and agricultural productivity. Integration of innovative technologies like precision farming, smart fertilization methods, and bio-fertilizers enhances efficiency and boosts market growth. Growing environmental awareness fosters the demand for organic and eco-friendly fertilizers, driving market growth. International collaborations and agreements between companies contribute to market growth, expanding the availability of specialized fertilizers.

Increasing awareness of sustainable farming practices and environmental concerns drives the demand for organic and specialty fertilizers. The adoption of digital platforms, precision farming techniques, and R&D in high-efficiency fertilizers signifies evolving trends in the market. Partnerships between fertilizer companies and agri-input platforms aim to provide convenient access to farmers, indicating emerging opportunities. Market key players like ICL, Coromandel International, IFFCO, and others have undertaken various initiatives including product launches, agreements, and technological innovations to cater to evolving agricultural needs, increase product accessibility, and reduce environmental impact.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Market Dynamics:

Catalytic Policies and Diverse Infrastructures Fueling India's Fertilizer Growth:

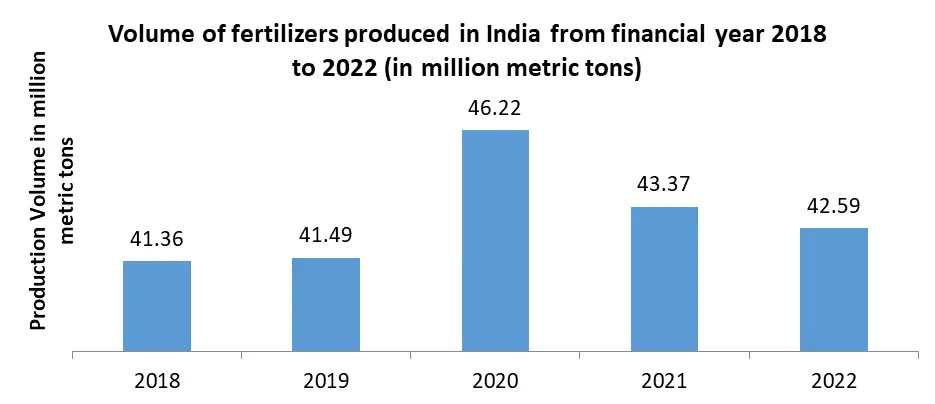

The India Fertilizer Market has experienced substantial growth owing to multiple factors that have contributed to its expansion and evolution. The conducive policy environment has catalyzed investments across the public, cooperative, and private sectors, fostering a surge in fertilizer production. This encouragement led to a remarkable increase in total fertilizer output, reaching 462.15 LMT in 2021-22, representing an impressive 11.40% year-on-year growth. India boasts a robust infrastructure with 32 large-scale urea plants, 19 units dedicated to producing DAP and complex fertilizers, and 2 units generating Ammonium Sulphate as a by-product. Such a diverse and extensive network of production facilities has substantially contributed to meeting the country's fertilizer demands.

Urea production during 2021-2022 increased to 249.3 LMT, while the estimated production of DAP and complex fertilizers rose to 137.36 LMT, reflecting a growth rate of approximately 6.51% over the previous year. India's reliance on imports, especially for Urea (25%), Phosphates (90%), and Potash (100%) has driven the government's push for joint ventures abroad. These collaborations, with buy-back arrangements, foster long-term agreements for the supply of vital fertilizer inputs, securing the nation's fertilizer demands. The convergence of these factors favorable policies, robust production facilities, specific fertilizer type growth, and strategic international collaborations stands as the primary driver propelling the India Fertilizer Market towards sustainable growth and self-sufficiency in meeting its agricultural requirements.

Government Subsidies and Initiatives Driving Fertilizer Demand:

Government subsidies and initiatives to support the agricultural sector, like the Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM) scheme promoting solar-powered irrigation, boost fertilizer demand and production. Advancements in farming techniques and the adoption of modern agricultural practices necessitate increased fertilizer use for better crop yields and soil health, propelling India Fertilizer Market growth. Integration of technology like precision farming, smart fertilization methods, and bio-fertilizers enhances efficiency, driving India Fertilizer Market growth. With a rising population, the demand for food products increases, subsequently augmenting the need for fertilizers to improve agricultural output. Growing environmental concerns lead to an increasing preference for organic and bio-fertilizers, creating new India Fertilizer Market avenues.

Collaboration with other countries for raw material procurement and joint ventures abroad ensure a steady supply chain, aiding India Fertilizer Market growth. Investments in R&D for innovative and efficient fertilizer formulations cater to specific crop needs, fostering market growth. Efforts to adapt to climate change effects on agriculture drive the demand for specialized fertilizers, such as those resistant to drought or floods, bolstering market growth. Increasing farmer education and awareness programs regarding the judicious use of fertilizers for sustainable agriculture stimulate India Fertilizer Market demand. Infrastructure enhancement, like the expansion of storage and distribution networks, aids in efficiently meeting fertilizer demand, and fostering India Fertilizer Market growth.

Regulatory and Chemical Law Challenges in Indian Fertilizer Manufacturing:

Regulatory constraints and chemical laws significantly impact India's fertilizer manufacturing landscape, presenting multifaceted challenges including both business operations and production processes. In the fertilizer industry, adherence to stringent chemical laws is paramount for ensuring product safety, environmental sustainability, and regulatory compliance. Challenges arise due to diverse chemical regulations across regions, posing hurdles to production standardization and distribution. India's fertilizer manufacturing faces intricate business challenges, including the increasing cost of raw materials and energy, amplified by fluctuating global prices of essential components like phosphates, potash, and natural gas, vital inputs in fertilizer production.

The dependency on imports for raw materials adds complexity due to geopolitical factors, trade restrictions, and currency fluctuations. This reliance raises vulnerability to supply chain disruptions, impacting production schedules and pricing strategies. Environmental concerns and evolving regulatory frameworks necessitate continuous innovation and adaptation of manufacturing processes to meet stringent emission norms and reduce carbon footprints. For instance, the restriction on the use of hazardous substances like heavy metals in fertilizers, as stipulated by chemical laws, demands extensive research and investment in alternative eco-friendly formulations, impacting manufacturing costs and product efficacy. The industry also grapples with challenges related to outdated manufacturing infrastructure and technological obsolescence, requiring substantial capital investments for modernization and upgradation. Variability in subsidy disbursement and policy inconsistencies create uncertainties, affecting the financial viability of fertilizer manufacturers and impeding long-term strategic planning.

The application of different chemical laws across Indian states further complicates the business landscape, causing disparities in compliance requirements and operational standards. For instance, varying regulations on nutrient-based subsidies and state-specific policies for fertilizer pricing influence the business environment, leading to regional disparities and market fragmentation. This dynamic regulatory landscape demands extensive legal expertise, robust compliance frameworks, and continuous monitoring to ensure conformity with evolving chemical laws while maintaining operational efficiency and business sustainability across diverse regions in India. These multifaceted challenges underscore the need for a cohesive approach by industry stakeholders, government bodies, and regulatory agencies to address compliance intricacies, promote sustainable practices, and foster a conducive environment for the growth of the Indian fertilizer manufacturing sector.

Technology-driven initiatives, Precision Farming and Smart Nutrient Delivery Systems:

Rising awareness about sustainable agriculture and environmental concerns creates a lucrative market for organic fertilizers. Companies like Coromandel International in India are expanding their organic product lines to meet this growing demand. Increased focus on eco-friendly farming practices presents an opportunity for bio-fertilizers. Various Indian agricultural companies, such as Tata Chemicals and National Fertilizers Limited, are investing in the research and production of bio-fertilizers to cater to this emerging market. Embracing innovation in fertilizer production methods like precision farming, smart nutrient delivery systems, and AI-driven solutions can enhance productivity. Companies like IFFCO and Indian Potash Limited (IPL) are investing in technology-driven initiatives to improve efficiency. Continued government support through subsidies, policies promoting balanced fertilization, and financial aid for farmers can significantly boost the fertilizer market. Schemes like Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) in India aid in increasing fertilizer usage and agricultural productivity.

Expanding fertilizer exports to neighboring countries due to increasing demand and strengthening trade relations can open new market avenues. India's fertilizer exports to countries like Nepal, Bangladesh, and Sri Lanka are growing, showcasing export potential. Tailoring fertilizer blends to specific soil types and crop requirements can be a lucrative opportunity. Companies offering customized nutrient solutions, like Zuari Agro Chemicals, are gaining traction by addressing diverse agricultural needs. Investing in farmer education and awareness programs regarding optimized fertilizer usage can drive market growth. Collaborative efforts by industry players and NGOs in educating farmers about the right fertilization practices can lead to increased consumption.

Research and development to create high-efficiency fertilizers while minimizing nutrient losses and environmental impact can shape future market growth. Companies engaging in R&D initiatives, such as Nagarjuna Fertilizers and Chemicals Limited (NFCL), are pioneering in this space. Integrating digital platforms for fertilizer distribution, farm management, and advisory services can streamline the supply chain and enhance market penetration. Initiatives like 'IFFCO iMandi' by IFFCO leverage digital technology to connect farmers and offer agri-inputs. Utilizing waste materials or by-products to create fertilizers can reduce costs and environmental impact. Initiatives by companies like Gujarat State Fertilizers & Chemicals Ltd (GSFC) in recycling waste for fertilizer production signify a sustainable growth opportunity.

India Fertilizer Market Segment Analysis:

Based on Type, Chemical fertilizers play a pivotal role in the India Fertilizer Market, commanding approximately 60% of the market share. These fertilizers are essential for addressing specific nutrient deficiencies in soils and optimizing crop yields across a wide range of agricultural practices. The dominance of chemical fertilizers in the market is driven by their effectiveness in providing essential nutrients like nitrogen, phosphorus, and potassium, which are crucial for plant growth and development. They are extensively used in large-scale farming operations to boost productivity and meet the growing demand for food grains and cash crops in India. Additionally, ongoing advancements in fertilizer technology and formulations continue to enhance their efficiency and application precision, further solidifying their role in supporting agricultural sustainability and food security in the country.

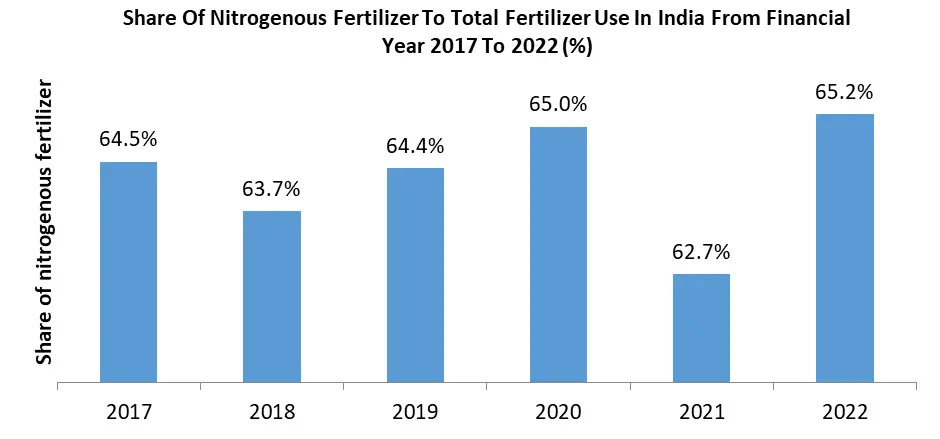

Based on Product, The India fertilizer market exhibits a diversified landscape segmented into Nitrogenous, Phosphatic, Potassic, and other categories. The nitrogenous segment has traditionally held dominance, constituting a major share. Among its subtypes, Urea stands as a key player, extensively utilized owing to its cost-effectiveness and versatile application across various crops, holding a substantial market share. The phosphatic sector, while significant, generally holds a smaller share in comparison to nitrogenous fertilizers. Within this category, Di-Ammonium Phosphate (DAP) and Mono-Ammonium Phosphate (MAP) are prominent, and widely used due to their high phosphorus content, essential for root development and crop yield enhancement. Potassic fertilizers, focusing on potassium content, occupy a lesser share of the Indian market. Their utilization is vital for improving stress resistance and overall plant health, but their dominance remains comparatively low in overall market share.

The dominance of these segments reflects their diverse applications. Nitrogenous fertilizers find extensive use in promoting vegetative growth, ensuring better yield and quality of crops. Phosphatic fertilizers are pivotal for root establishment, blooming, and fruiting stages, while potassium fertilizers enhance disease resistance and improve the overall quality of produce. Considering evolving agricultural practices and technological advancements, the dominance in the fertilizer market is expected to persist for Nitrogenous fertilizers, followed by Phosphatic fertilizers, while the Potassic segments are anticipated to maintain their relatively small shares. This trajectory is contingent upon the continued emphasis on crop productivity, sustainability, and balanced fertilization practices aimed at addressing specific soil deficiencies and crop needs.

India Fertilizer Market Regional Insights:

The Indian fertilizer market exhibits regional variations in dominance and growth, with certain regions playing pivotal roles in shaping the market landscape. Northern India emerged as a dominant region in the fertilizer market, primarily attributed to its agrarian economy and substantial agricultural activities. States like Uttar Pradesh, Punjab, and Haryana have a historical stronghold in agricultural practices, driving considerable fertilizer demand and consumption. These regions benefit from fertile plains and a strong focus on cereal cultivation, necessitating consistent fertilizer utilization. The eastern and southern regions of India are poised for significant growth. Eastern states like West Bengal, Odisha, and Bihar, with their increasing emphasis on diversification of crops and adoption of modern agricultural practices, are anticipated to witness notable market growth. For example, Odisha has been focusing on enhancing soil health and nutrient management, thereby driving fertilizer demand.

The Southern region, particularly states like Andhra Pradesh, Telangana, and Karnataka, is experiencing agricultural transformations through technological advancements and horticultural developments. The adoption of precision farming and increased cultivation of cash crops like fruits and vegetables augur well for heightened fertilizer utilization in these states. Initiatives promoting organic farming in Southern states are likely to bolster the demand for organic fertilizers. The Western region, encompassing states such as Maharashtra and Gujarat, presents a mixed scenario, witnessing moderate growth due to a blend of traditional and progressive farming practices. Gujarat, known for its diverse crop cultivation, stands as a notable contributor to fertilizer demand. Additionally, the Indian government's initiatives like 'Paramparagat Krishi Vikas Yojana' (PKVY) and 'National Mission on Oilseeds and Oil Palm' (NMOOP) are driving fertilizer consumption across regions by promoting balanced fertilization and sustainable agricultural practices. The collective efforts to address regional agronomic needs and optimize fertilizer utilization signify a comprehensive approach toward ensuring balanced growth and sustainability across India's diverse agricultural landscape.

Competitive Landscape

Recent developments in the Indian fertilizer market signify a shift towards innovative products and strategic collaborations, contributing significantly to market growth. Agreements like ICL's long-term commitment to supply Polysulphate to India Potash Limited (IPL) expand the availability of specialized fertilizers, aligning with the Government of India's organic agriculture agenda. The agreements signed by ICL in May 2022 to supply potash to customers in India and China demonstrate growing international trade and demand for essential nutrients in agriculture, positively impacting the fertilizer market. Introducing advanced fertilizers by companies like ICL, Coromandel International, and Smartchem Technologies, featuring technologies such as EnPhos, nano-formulations, and robotic lawnmower-compatible options, cater to evolving agricultural needs, enhancing productivity while ensuring environmental sustainability. The initiatives like IFFCO's Nano Technology-based products showcase a commitment to reducing chemical fertilizer usage, aligning with sustainable farming practices. Collaborations between Smartchem Technologies and AgroStar also indicate a transition towards direct-to-farmer delivery models, enhancing accessibility and convenience. These collective advancements reflect an industry-wide shift towards technology-driven, eco-friendly, and customized fertilizer solutions, fostering market growth while addressing varied agricultural challenges in India.

In June 2022, ICL inked a long-term deal with India Potash Limited (IPL) to supply 1 million metric tons of polysulphate until 2026, aimed at supporting the Government of India's organic agriculture program.

In May 2022, ICL finalized framework agreements with Indian and Chinese customers to provide 600,000 and 700,000 metric tons of potash, respectively, at 590 USD per ton for 2022.

In February 2022, ICL introduced innovative lawn care fertilizers featuring urea coated with sulfur and a biodegradable polymer membrane (Poly-S) or resin-coated nitrogen blended with phosphorus and potash (PACE), reducing uncontrolled growth and mowing effort, ideal for robotic lawnmowers.

In September 2021, Coromandel International launched GroShakti Fertilizer, a high-nutrient complex fertilizer with EnPhos Technology and Zincated 14-35-14, designed to preserve soil health by minimizing filler content.

In January 2021, Smartchem Technologies Limited partnered with AgroStar, facilitating direct delivery of specialized fertilizers to farmers in Maharashtra & Madhya Pradesh.

In November 2019, IFFCO initiated field trials for nano nitrogen, nano zinc, and nano copper-based products to reduce chemical fertilizer usage and elevate farmers' income.

India Fertilizer Market Scope: Inquire before buying

| India Fertilizer Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 1046.85 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 5.7% | Market Size in 2030: | US $ 1543.15 Bn. |

| Segments Covered: | by Type | Organic Fertilizer Chemical Fertilizer Mixed Fertilizers |

|

| by Distribution Channel | Direct Sales Retailers Government Agencies and Cooperatives Others |

||

India Fertilizer Market Key Players:

1. Ajay Farm-Chem Private Limited

2. Balaji Fertilizers Private Limited

3. Bharat Fertilizer Industries Limited

4. Chambal Fertilizers & Chemicals Limited

5. Coromandal Fertilizers Limited

6. Deepak Fertilizer and Petrochemicals Corporation Limited

7. Duncans Industries Limited

8. Fertilizers And Chemicals Travancore Limited (FACT)

9. Godavari Fertilizers & Chemical Limited

10. Gujarat Narmada Valley Fertilizers & Chemicals Limited (GNFC)

11. Gujarat State Fertilizers & Chemicals Limited (GSFC)

12. Hindustan Fertilizer Corporation Limited (HFCL)

13. Indian Farmers Fertilizer Cooperative Limited (IFFCO)

14. Karnataka Agro Chemicals

15. Krishak Bharati Cooperative Limited (KRIBHCO)

16. Madras Fertilizers Limited

17. Meerut Agro Chemicals Private Limited

18. National Fertilizers Limited

19. Neyveli Lignite Corporation Limited

20. Paradeep Phosphates Limited

21. Pyrites, Phosphates & Chemicals Limited

22. Rashtriya Chemicals & Fertilizers Limited

FAQs:

1. What are the growth drivers for the India Fertilizer Market?

Ans. Government Subsidies and Initiatives Driving Fertilizer Demand and is expected to be the major driver for the India Fertilizer Market.

2. What is the major opportunity for the India Fertilizer Market growth?

Ans. Technology-driven initiatives, Precision Farming and Smart Nutrient Delivery Systems.

3. Which country is expected to lead the India Fertilizer Market during the forecast period?

Ans. The North India is expected to lead the India Fertilizer Market during the forecast period.

4. What is the projected market size and growth rate of the India Fertilizer Market?

Ans. India Fertilizer Market size was valued at USD 1046.85 billion in 2023 and the total India Fertilizer Market revenue is expected to grow at a CAGR of 5.7 % from 2024 to 2030, reaching nearly USD 1543.15 billion.

5. What segments are covered in the India Fertilizer Market report?

Ans. The segments covered in the India Fertilizer Market report are by Type, Application, and Distribution Channel.