Hotels Market by Hotel Type ( Business/ Commercial Hotels, Boutique Hotels, Resort Hotels ) Price Level ( Luxury, Upscale, Midscale ) Room Capacity ( Small, Medium, Large Business Model ) Individual, Chain, Others) Global Forecast to 2030

Overview

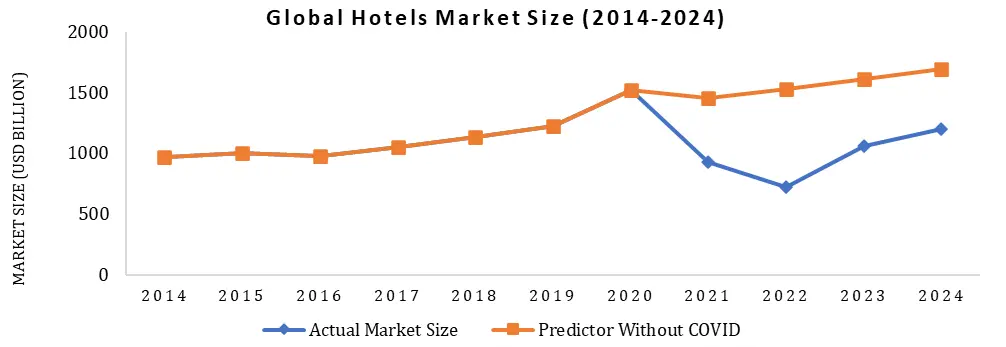

The Hotels Market size was valued at USD 1071.49 Billion in 2024 and the total Hotels revenue is expected to grow at a CAGR of 9.2% from 2025 to 2032, reaching nearly USD 2166.55 Billion.

Hotels Market Executive Summary

The hotel business is entering its most consequential cycle in decades. Between 2025 and 2032, the industry’s value will be defined less by inventory and more by understanding—how precisely a brand can recognize a guest, anticipate needs, and price experiences in real time. Occupancy and ADR still matter—but loyalty economics, distribution control, and experience design now decide margin. India, Southeast Asia, and the Gulf are scaling demand engines; the U.S. and Europe are pivoting to conversion-led growth and asset-light expansion. Meanwhile, wellness and spiritual travel are becoming structural demand pillars rather than fads. Winners will look like tech companies with beds: cloud-native ops, AI-driven revenue labs, and zero-leakage distribution. Losers will overpay for keys and underinvest in guest data.

Why this RD matters: it gives you a complete playbook—from RevPAR drivers and cost structure to licensing, pipeline strategy, risk, and financial modeling—so your brand can grow faster with tighter control of unit economics and a clear route to premium multiples.

Hotels Market Objective & Scope

This RD arms developers, operators, investors, and policy makers with decision-ready insight for 2025–2032. It covers global and India with attention to metro vs Tier-2, chain vs independent, business vs leisure, OTA vs direct vs B2B, and ownership formats (managed, franchised, leased, owner-operator). You get historical context (2021–2024), modeled forecasts, CapEx/Opex benchmarks per key, pricing and booking-mix intelligence, regulatory pathways, technology roadmaps, competitive positioning, SWOT + risk mitigation, methodology, and assumptions—all written as flowing analysis with bolded takeaways (no sterile boilerplate).

Hotels Market Definition & Segment Analysis

Hotels are no longer just shelters with rate fences; they’re multi-format experience platforms. The market spans budget and midscale (efficiency, location, reliability), upper-mid and upscale (service depth, F&B, meetings), and luxury (identity, design, discretion). Chain affiliation brings rate integrity, loyalty, and financing benefits; independents trade on neighborhood authenticity and owner agility. Demand splits across business, “bleisure”, leisure/resort, MICE, wellness, spiritual/heritage, and extended stay. Distribution is the battlefield: OTAs for reach, direct for lifetime value, B2B/TMCs for a predictable base.

Global Hotel Market Size

To know about the Research Methodology :- Request Free Sample Report

Market Dynamics & Growth Drivers

The next leg of growth is powered by five structural forces. First, bleisure: corporate trips stretch into weekends, so weekend ADR strength and length-of-stay (LOS) rise. Second, personalization becomes table stakes—brands that stitch loyalty, CRM/CDP, and pricing win both rate and retention; anonymous guests equal margin leakage. Third, wellness and spiritual tourism harden into year-round demand, lifting shoulder months and stabilizing cash flows. Fourth, asset-light expansion scales faster at lower capital intensity; conversion and soft-brand plays monetize existing buildings with brand and system strength. Fifth, ESG discipline is now revenue-positive: certified green hotels win RFPs, command rate premiums, and cheapen energy cost via smart systems.

Market Challenges

Headwinds are real—and predictable. Fixed-cost weight is unforgiving: manpower, utilities, and maintenance compress EBITDA when occupancy dips. OTA commission “tax” of 12–20% erodes contribution when direct engines are weak. Talent churn—especially in housekeeping and F&B—forces wage inflation and service inconsistency. Licensing drag slows new supply (fire NOCs, FSSAI, local clearances, CRZ in coastal zones), pushing pre-opening costs higher. Rate parity battles and excessive discounting train guests away from direct. Climate volatility and macro shocks whiplash demand unless portfolios are geographically and segment-diversified.

Hotels Market Scope: Inquire before buying

| Hotels Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 1071.49 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 9.2% | Market Size in 2032: | USD 2166.55 Bn. |

| Segments Covered: | by Hotel Type | Business/ Commercial Hotels Boutique Hotels Resort Hotels Casino Hotels Transit Hotels Bed & Breakfast Hotels Others |

|

| by Price Level | Luxury Upscale Midscale Economy |

||

| by Room Capacity | Small Medium Large Mega |

||

| by Business Model | Individual Chain |

||

Regional & Segment Intelligence (Global + India)

India is the most exciting multi-segment canvas: metros drive ADR and corporate base, while Tier-2/Tier-3 cities and spiritual corridors (Ayodhya, Varanasi, Haridwar, Rishikesh) inject secular growth through events, pilgrimage, education, and medical travel. Leisure hills and coastal belts remain supply-constrained due to land and environmental approvals—a pricing opportunity for branded, compliant assets. Globally, APAC continues to outgrow other regions on volume and new wealth, GCC invests in giga-destinations (improving year-round seasonality), and the U.S. and Europe are in a conversion cycle—flag swaps and soft brands unlocking rate via loyalty platforms, without new ground-up CapEx. Extended stay and select-service out-earn full-service peers on flow-through and stability.

Globally, APAC continues to outgrow other regions on volume and new wealth, GCC invests in giga-destinations (improving year-round seasonality), and the U.S. and Europe are in a conversion cycle—flag swaps and soft brands unlocking rate via loyalty platforms, without new ground-up CapEx. Extended stay and select-service out-earn full-service peers on flow-through and stability.

RevPAR, ADR, Occupancy: What Really Moves the P&L

The story executives need is simple: ADR is the lever; occupancy is the cushion; mix is the multiplier. Post-pandemic, global occupancy re-normalized in the low-60s with ADR stepping higher due to mix upgrades (more leisure, more suites, more experiential pricing). As corporate and MICE fill back in, expect weekday rates to firm, with weekend premiums held by leisure. India’s spiritual/leisure nodes smooth seasonality and extend LOS, while metro weekday strength protects base. Where revenue labs run real-time price fences (length-of-stay, mobile-only, loyalty-tiered), we see superior RevPAR uplift without self-cannibalization.

Cost Structure (CapEx/Opex per Key)

Build and run for unit economics—not vanity. Indicative CapEx per key trends around USD xx–xxk (budget), USD xx–xxk (midscale), and USD xx–xxk+ (luxury) depending on land, brand standards, and fit-out. Opex stacks with manpower XX%, utilities/maintenance xx–xx%, OTA commission xx%, and F&B xx% (with banquet-led hotels achieving outsize GOP during event cycles). Smart energy systems (heat pumps, BMS, sensors) pay back sub-36 months in high-tariff cities. Renovation cadence (soft goods 5–7 years, case goods 10–12) must be funded through FF&E reserves—under-fund and you will lose ADR power.

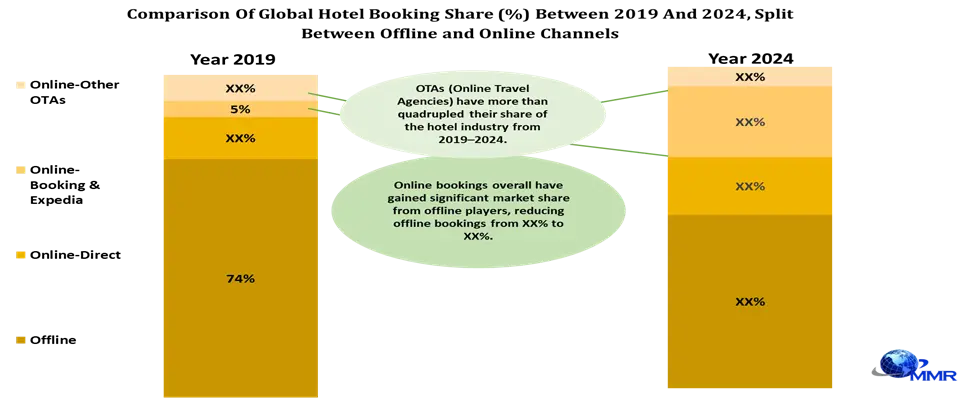

Pricing & Booking-Channel Mix

Distribution is strategy, not a toggle. OTAs deliver reach, but direct delivers lifetime value. Loyalty-driven direct share rises when brands bundle rate + early check-in + F&B credit and reward app-only behavior. Corporate/B2B returns as procurement seeks duty-of-care + ESG. Metasearch is the new battleground—own your brand bid or pay the leakage tax. Invest in rate-integrity tools; deploy mobile-only fences, geo-targeting, and length-of-stay ladders to lift ADR without billboard effect. The % shown in the image represents the year-on-year brand value growth rate of each hotel brand in 2023

The % shown in the image represents the year-on-year brand value growth rate of each hotel brand in 2023

Entry Barriers & Regulatory Landscape (India focus, globally relevant)

Expect 8–12 approvals for a compliant opening in India: fire, police, trade license, FSSAI, pollution control/environment, sometimes heritage/coastal clearances. Liquor licensing and signage guidelines vary by state and municipality. Building codes and life-safety require early alignment to avoid rework. Globally, accessibility, ESG reporting, and labor laws shape timelines and opex; GCC provides incentives but needs local-partner fluency. Regulatory mastery is a moat—build it once, monetize for years.

Business Strategy & Expansion Roadmap

Phase 1: Speed to market with asset-light conversions and select-service builds in Tier-2 growth corridors (corporate satellites, medical/education hubs, pilgrimage belts). Phase 2: Cluster strategy—one hub full-service + three to five spokes (select-service/extended stay) sharing sales, procurement, and HR; funnel everything into a central revenue lab. Phase 3: Experience moat—codify a loyalty-first, mobile-native journey (pre-stay offers, in-stay personalization, post-stay reactivation), then scale via franchising with non-negotiable brand standards and owner education on revenue and capex discipline.

Pipeline Analysis (What to Build, What to Convert)

The cheapest key is the one you convert. Globally and in India, conversion/soft-brand pipelines are swelling: owners want system revenue and ADR lift without the time and risk of ground-up. Pilgrimage and wellness clusters are under-branded; select-service with strong housekeeping and breakfast CX outperforms on flow-through. Mixed-use (co-working + retail + F&B streets) around hotels thickens demand and diversifies NOI.

Financial Modeling & Sensitivity (What your CFO really needs)

Underwrite on stabilized RevPAR and flow-through, not just pro-forma occupancy. Break-even occupancy for midscale typically sits in the mid-50s, but pricing power and distribution mandcontrol decide how fast you get there. +10% ADR often yields +XX% RevPAR when fences hold, while –XX% occupancy can compress margins XX% if fixed cost is undisciplined. Interest-rate and currency sensitivity matter for cross-border debt and FF&E imports; hedge where exposure is real. Pre-opening costs and ramp curves (12–24 months) must be in the model—rosy curves kill equity.

Technology & Innovation (From PMS to Profit OS)

Tomorrow’s leaders run cloud PMS + RMS + channel manager + CDP/CRM as a single nervous system. AI concierges lift satisfaction and upsell; digital keys reduce friction; smart housekeeping cuts idle time and energy. First-party data powers next-stay offers and ancillary attach (spa, dining, transport). In luxury, biometric access, digital-twin guest profiles, and in-room sustainability dashboards drive both rate and reputation. Tech without adoption is capex waste—tie every feature to RevPAR, GOPPAR, or NPS.

Hotels Market Competitive Intelligence (How the brands actually win)

IHCL (Taj) is leaning into India’s spiritual and heritage circuits while sharpening luxury wellness; Marriott compounds with Bonvoy flywheel and conversion-friendly playbooks; Hilton and Hyatt double down on select-service and extended-stay for predictable flow-through; Accor scales lifestyle/experiential with strong ESG narrative; ITC weaponizes responsible luxury with LEED leadership; Radisson/IHG dominate owner-friendly mid-upscale; Lemon Tree and Sarovar own value-centric urban. OYO/Fab keep the budget/long-tail aggregated and price-transparent. Translation: brand systems that protect ADR and fill base demand will keep taking share; badge-only plays will be squeezed.

SWOT & Risk Mitigation (Truth on one page)

Strengths: hospitality demand is multipolar and multi-seasonal; loyalty ecosystems and ESG credentials command corporate preference.

Weaknesses: fixed-cost drag, OTA leakage, and talent churn.

Opportunities: Tier-2 growth corridors, spiritual/wellness permanence, conversion-led pipelines, ancillary monetization.

Threats: macro shocks, extreme weather, rate wars, regulatory stalls.

Mitigate with intent: balanced portfolios, owner CAPEX education, direct-first marketing, energy savings that drop to EBITDA, multi-source staffing, scenario-tested revenue plans. If it’s not measured, it won’t move—tie every mitigation to KPIs and incentives.

Strategic Recommendations (Do this next)

Own Tier-2 and spiritual nodes now while land is still rational. Go asset-light where speed and scale beat control; own flagship assets where brand theater drives pricing power. Build a central revenue lab and treat distribution as a P&L. Design for loyalty, not just for OTA conversion: mobile-only rates, instant benefits, and human service recovery. Make ESG a revenue center, not a report—audit utilities, monetize green in RFPs, tell the story. Codify brand standards and train owners to protect ADR. Finally, fund the renovation cycle—because shiny rooms sell, tired rooms discount.

Methodology & Frameworks (Why you can trust the view)

This RD blends primary conversations with owners, operators, and distribution partners; secondary sources (industry databases/brand filings); and bottom-up market builds for key nodes. We apply PESTEL for macro, Porter’s for structure, and SVOR to prioritize Supply-Demand-Value-Opportunity-Risk. Forecasts are scenario-tested (demand and price bands) and cross-checked to unit economics (CapEx/Opex, flow-through, renovation).

Glossary & Assumptions (So teams speak one language)

ADR (Average Daily Rate), RevPAR (Revenue per Available Room), GOPPAR (Gross Operating Profit per Available Room), LOS (Length of Stay), PMS (Property Management System), RMS (Revenue Management System), CDP/CRM (Customer Data Platform/Relationship Management), OTA (Online Travel Agency), TMC (Travel Management Company), MICE (Meetings, Incentives, Conferences, Exhibitions), FF&E (Furniture, Fixtures & Equipment). Assumptions: base year 2024, USD currency, inflation-adjusted modeling, and scenario bands for demand/pricing; where explicit datasets are absent, figures are indicative ranges judged against market norms.

Why Buy This Report (The executive promise)

Because it speaks the language of owners and operators, not just analysts. You get clear levers to grow RevPAR, discipline to protect EBITDA, a route to lower CAC via direct, and a credible plan to finance, staff, and scale.

Hotels Market Regional Scope

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Hotels Market, Key Players are:

1. Accor SA / Accor

2. Marriott International

3. Hyatt Hotels Corporation

4. Hilton Worldwide Holdings Inc.

5. InterContinental Hotels Group PLC (IHG)

6. Best Western International, Inc.

7. Choice Hotels International, Inc.

8. Wyndham Destinations, Inc.

9. Radisson Hospitality A.B. / Radisson Hotel Group

10. Indian Hotels Company Limited / Taj Hotels

11. Oravel Stays Private Limited

12. TC Limited

13. EIH Limited / Oberoi Hotels & Resorts

14. Bharat Hotels Limited / ITC Hotels

15. Lemon Tree Hotels

16. The Leela Palaces

17. Four Seasons Hotels and Resorts

18. Huazhu Hotels Group

19. Ryman Hotel Properties

20. GF Hotels & Resorts

21. HOTEL THE MITSUI KYOTO

22. The Hoxton

23. The Muraka at Conrad Maldives Rangali Island

24. Motel One

25. Eccleston Square

26. W Singapore Sentosa Cove

27. YOTEL Singapore Orchard Road Hotel

28. Hotel Clark Budapest

29. Hotel Chinzanso Tokyo