Virtual Client Computing Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

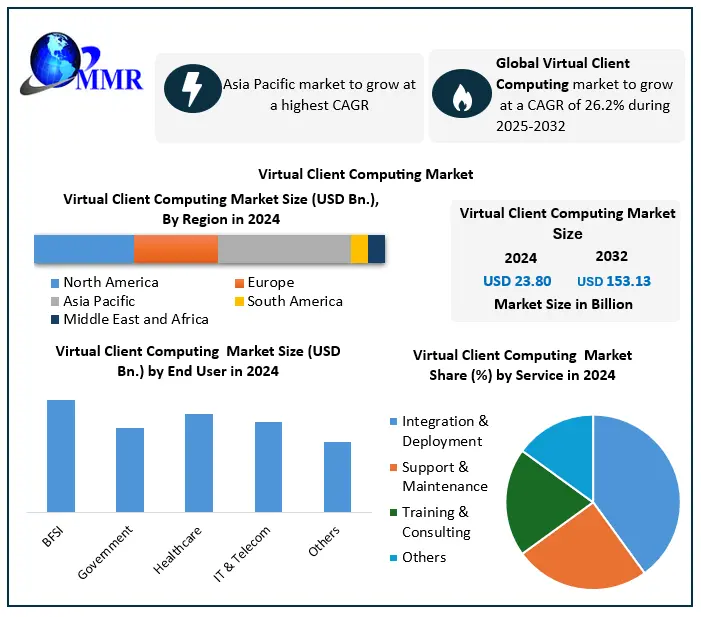

Global Virtual Client Computing Market size was valued at USD 23.80 Bn. in 2024, and the total Virtual Client Computing Market revenue is expected to grow by 26.2% from 2025 to 2032, reaching nearly USD 153.13 Bn.

Virtual Client Computing Market

Virtual computing is the use of a remote computer from a local computer where it is located. For instance, a home computer user logs in to a remote office computer, using the internet or any network to perform various jobs. Therefore, computing refers to a model that provides a virtualized desktop solution to overcome the limitations associated with the traditional environment of distributed desktop systems. The technology makes use of 4 major software technologies, which are desktop virtualization, application virtualization, user state virtualization, and virtual user session. The global Virtual Client Computing Market for computing is perceiving a huge development, thanks to the rising agile labor, improved user productivity, lowered costs, information security, and simplified IT management helps to boost the Virtual Client Computing Market. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Virtual Client Computing Market Dynamics:

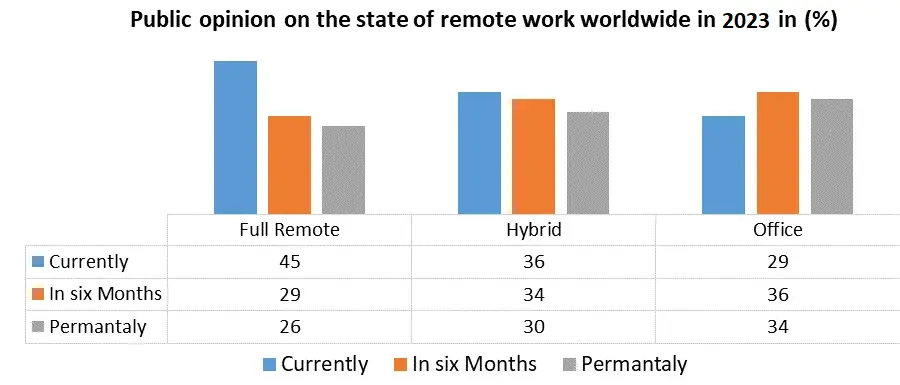

Rising Remote Work Trends boost the Market Growth

The virtual client computing market is experiencing a substantial surge in growth, largely attributed to the growing trends in remote work. The global shift towards remote work, catalyzed by events such as the COVID-19 pandemic, has propelled the adoption of virtual client computing solutions to the forefront. Organizations worldwide are grappling with the challenge of enabling remote employees to seamlessly access applications and data securely. Virtual client computing offers a compelling solution and provides remote workers with the ability to connect to their work environments from virtually anywhere with an internet connection. This newfound accessibility boosts productivity and promotes workplace flexibility, making it an increasingly attractive option for both employers and employees.

The heightened focus on security and data protection in remote work scenarios has amplified the importance of virtual client computing. These solutions centralize control and implement strong security measures, mitigating the risks associated with data breaches and unauthorized access. The cost-efficiency, scalability, improved IT management, and compatibility with collaboration tools further strengthen the adoption of virtual client computing. As remote work continues to be a fundamental aspect of the modern workforce, the virtual client computing market is poised for sustained growth, serving as a vital enabler for organizations navigating the evolving landscape of remote work arrangements.

Digital transformation drives the Market

Digital transformation refers to the strategic process in which organizations harness the power of digital technologies to revolutionize their business operations, strategies, and the way they engage with customers. This entails incorporating digital tools, leveraging data, and implementing technology-driven procedures to effectively navigate the ever-changing digital environment and secure a competitive edge. Digital transformation involves using the cloud, analyzing lots of data, connecting devices to the internet, using smart machines, making things automatic, and making things work better. Leveraging these technological advancements, businesses augment their efficiency, flexibility, and customer-centric approach.

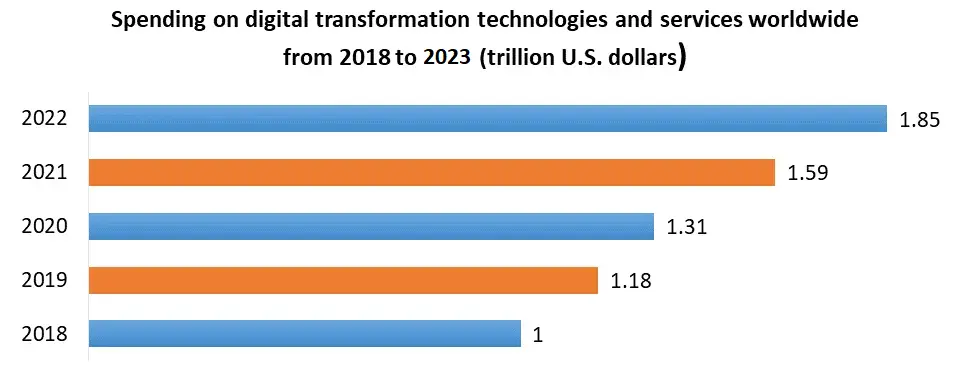

Digital transformation results in enhanced decision-making through the utilization of data insights, the automation of repetitive tasks for streamlined operations, improved customer engagement, and the delivery of personalized experiences. Digital transformation growth is due to several contributing factors. Among these is the recent COVID-19 pandemic, which has increased the digital transformation tempo in organizations around the globe in 2023 considerably. Other contributing causes include customer demand and the need to be on par with competitors. Overall, utilizing technologies for digital transformation renders organizations more agile in responding to changing markets and enhancing innovation, thereby making them more resilient. For Example, in 2018, spending on digital transformation (DX) reached 1 trillion U.S. dollars. By 2023, global digital transformation spending is forecast to reach 1.85 trillion U.S. dollars. High-Security Concerns Limit the Market Growth

High-Security Concerns Limit the Market Growth

Security concerns in Virtual Client Computing (VCC) are dominant due to the centralized nature of data and applications. This consolidation makes VCC environments potentially vulnerable to security breaches, unauthorized access, and various cyber threats. A primary issue is data privacy, as centralized data storage and transmission expose sensitive information to breaches if not properly safeguarded through encryption, access controls, and data segregation. Cyber-attacks, including malware, phishing, and DDoS attacks, are also significant threats to Virtual Client Computing environments, with potential consequences for data integrity and availability. Also, following the rules about handling data, like GDPR or HIPAA, is hard because the data is kept in different places. The involvement of third-party service providers introduces additional security risks, necessitating careful assessment and monitoring. Overall, addressing these security concerns requires organizations to invest in comprehensive cyber security measures, regular updates to security protocols, user education, and frequent security audits to ensure the safe operation of Virtual Client Computing systems.

Integration with Emerging Technologies creates lucrative growth opportunities for the Market.

Integration with emerging technologies presents a significant opportunity for the Virtual Client Computing (VCC) market, promising to elevate its capabilities and user experience. Incorporating cutting-edge technologies such as Artificial Intelligence (AI) and Machine Learning, VCC optimizes resource allocation, offers predictive analytics, and personalizes virtual desktops based on user behavior. The integration of Virtual Reality (VR) and Augmented Reality (AR) allows for immersive virtual workspaces, enhancing collaboration and training experiences. Edge computing enables VCC to reduce latency and provide real-time applications, while blockchain integration ensures heightened security and transparency. IoT integration enables control over smart devices within the virtual workspace, and voice and natural language processing simplify user interactions. These innovations, coupled with 5G connectivity, advanced cybersecurity measures, and data analytics, position VCC solutions to deliver more efficient, secure, and personalized experiences for users, opening up new avenues for growth and adoption in an increasingly digitized world.

Virtual Client Computing Market Segment Analysis

Based on Type, Virtual User Session (VUS) Segment dominated the Virtual Client Computing Market in the year 2024. VUS offers users individualized applications, profile settings, and data storage within their own dedicated accounts. This approach was widely adopted by organizations, particularly on older versions of Windows Server, to facilitate remote access to applications and data within a controlled and centralized environment. VUS solutions are cost-effective, efficiently serving a large user base through a terminal-based experience, and minimizing expenses. VUS solutions have limitations as they lack customization options, offering users a standardized set of products. With the introduction of newer operating system versions, VUS is experiencing a decline in popularity. On the other hand, the Virtual Desktop Infrastructure (VDI) is poised to become the fastest-growing segment due to increasing demand for workplace flexibility and productivity benefits. VDI addresses security concerns and enhances network protection against cyber threats. Moreover, its deployment in data centres improves safety, increases IT control, and reduces annual desktop hardware upgrade expenses. Advances in graphics and storage capabilities further position VDI as a compelling choice for emerging data centre applications, creating significant market opportunities.

Based on Service, the integration and deployment segment dominated the Virtual Client Computing Market in the year 2024. These services play an essential role in facilitating the deployment of solutions within organizations. They ensure that solutions are smoothly integrated with both internal and external systems, thereby maximizing the value of the client's investments in their IT infrastructure. Integration services are instrumental in helping organizations understand the operational functionalities of their systems and establish reliable connectivity among various solutions. The growth of this segment is primarily propelled by the escalating organizational demand for advanced services, the increasing adoption of automation, and the widespread embrace of cloud computing. As organizations seek to enhance their operational capabilities, integration, and deployment services become increasingly important. The constant evolution of operating systems necessitates frequent system upgrades. Virtual client computing solutions must keep pace with these updates, along with other technical advancements. Support and maintenance services are essential to ensure that virtual solutions remain up-to-date, continually facilitate data import and export operations, and promptly adapt to evolving technological requirements. The growing trend of organizations shifting to cloud-based operations has led to more frequent updates, further boosting the growth of this segment.

Virtual Client Computing Market Regional Analysis:

The Asia-Pacific region is expected to dominate the Virtual Client Computing Market in the year 2023. For several key reasons. The region encompasses a diverse range of countries with changing levels of technological maturity, making it a rich ground for both established and emerging players in the virtual client computing space. The region's rapid economic growth has led to increased enterprise adoption of virtual client computing solutions to enhance productivity and cost efficiency. This growth fuels demand for virtual client computing technologies. Asia-Pacific hosts a substantial number of global technology giants and a burgeoning start-up ecosystem, fostering innovation and competition in the market. The region's large and increasingly mobile workforce necessitates flexible and scalable computing solutions, making virtual client computing a highly sought-after technology. Governments in the Asia-Pacific region have been actively promoting digitalization and IT infrastructure development, further boosting the adoption of virtual client computing. These factors combined position Asia-Pacific as a dominant force in the Virtual Client Computing Market.

Competitive Landscape:

The Virtual Client Computing Market is dynamic and includes a mix of established players and innovative start-ups. The key players in the market majorly focus on ongoing innovation, consolidation, and partnerships as companies strive to address evolving customer needs, such as remote work enablement, security enhancements, and improved user experiences. Customer choice often depends on factors such as scalability, integration capabilities, cost-effectiveness, and vendor reputation, making the market highly competitive and diverse. The virtual client computing market is highly competitive, with major players dominating the market. The market is expected to continue growing rapidly, which is further expected to intensify the competition among the key players.

Virtual Client Computing Market Scope: Inquiry Before Buying

| Virtual Client Computing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 23.80 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 26.2% | Market Size in 2032: | USD 153.13 Bn. |

| Segments Covered: | by Type | Virtual User Sessions (VUS) Terminal Sessions Virtual Desktop Infrastructure Others |

|

| by Services | Integration & Deployment Support & Maintenance Training & Consulting Others |

||

| by Deployment Mode | Hosted / Cloud-based On Premise |

||

| by Enterprise Size | Large Enterprises SMEs (Small & Medium Enterprises) |

||

| by End Use | BFSI Government Healthcare IT & Telecom Others |

||

Virtual Client Computing Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Virtual Client Computing Market, Major Players:

1. VMware, Inc. (United States)

2. Citrix Systems, Inc.(United States)

3. Microsoft Corporation (United States)

4. Dell Technologies, Inc.(United States)

5. HP Inc.(United States)

6. Nutanix, Inc.(United States)

7. Cisco Systems, Inc.(United States)

8. IBM Corporation (United States)

9. IGEL Technology (Germany)

10. Parallels International GmbH (United States)

11. Ericom Software (United States)

12. Sangfor Technologies (China)

13. Huawei Technologies Co., Ltd.(China)

14. Oracle Corporation (United States)

15. NComputing Co., Ltd. (South Korea)

16. Lenovo Group Limited (China)

17. Teradici Corporation

18. Unidesk Corporation

FAQ

1] What segments are covered in the Global Virtual Client Computing Market report?

Ans. The segments covered in the Virtual Client Computing Market report are based on Type, Services, End User, Deployment Mode, Enterprise Size and Regions.

2] Which region is expected to hold the highest share in the Global Virtual Client Computing Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Virtual Client Computing Market.

3] What is the market size of the Global Virtual Client Computing Market by 2032?

Ans. The market size of the Virtual Client Computing Market by 2032 is expected to reach US$ 153.13 Bn.

4] What was the market size of the Global Virtual Client Computing Market in 2024?

Ans. The market size of the Virtual Client Computing Market in 2024 was valued at US$ 23.80 Bn.

5] Key players in the Global Virtual Client Computing Market.

Ans. VMware, Inc. (United States), Citrix Systems, Inc. (United States), Microsoft Corporation (United States), Dell Technologies, Inc. (United States), HP Inc. (United States), Nutanix, Inc.(United States), Cisco Systems, Inc.(United States), IBM Corporation (United States), IGEL Technology (Germany), and Parallels International GmbH (United States)