Vanadium Pentoxide Market by Type, Application, End-Use Industry, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

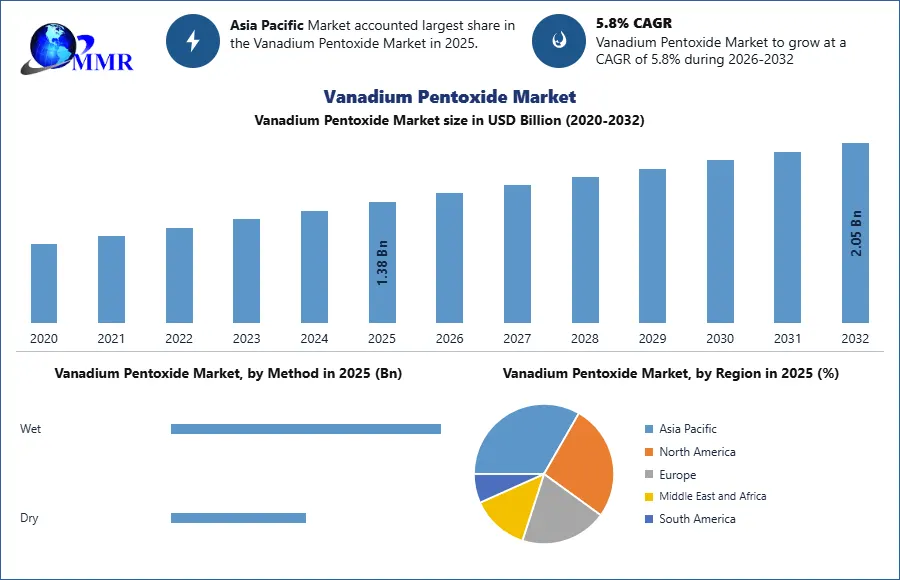

The Vanadium Pentoxide Market was valued at USD 1.38 Billion in 2025 and is estimated to grow at a CAGR of 5.8% over the forecast period, reaching USD 2.05 Billion by 2032.

Global Vanadium Pentoxide Market Overview

The Vanadium Pentoxide Market represents the global value chain for vanadium pentoxide (V2O5), a critical vanadium oxide used as an intermediate and finished commercial material in ferrovanadium production, sulfuric acid catalysts, titanium alloys, specialty chemicals, ceramics, pigments, and energy-storage electrolytes. Vanadium pentoxide sits at the center of the broader vanadium economy because it is both a tradable product and a feedstock for higher-value downstream materials. In industrial practice, it is produced from primary vanadium-bearing ores, steel slag, and secondary sources such as spent catalysts, petroleum residues, fly ash, and other vanadium-containing waste streams. USGS notes that U.S. secondary production already includes processing waste materials into ferrovanadium, vanadium-bearing chemicals, and vanadium pentoxide, showing that recycling is becoming structurally important to supply resilience.

Growth in the Vanadium Pentoxide Market has been anchored by steel microalloying demand. More than 90% of reported vanadium consumption remained tied to metallurgical uses, primarily as an alloying agent in iron and steel, because vanadium improves strength, wear resistance, toughness, and fatigue performance in high-strength low-alloy steels used in construction, transport, pipelines, and industrial machinery. This base-load steel demand has kept vanadium pentoxide commercially relevant even during periods of battery-market volatility. At the same time, demand diversification has strengthened. Nonmetallurgical uses in catalysts remain essential, especially for sulfuric acid and maleic anhydride production, while aerospace and defense applications continue to require high-purity vanadium inputs for titanium alloys.

Technological development is increasingly shifting the market toward higher-purity and battery-oriented products. Largo states that its VPURE+ vanadium pentoxide powder exceeds typical industry purity and is suitable for catalyst applications and vanadium electrolyte for flow batteries. Parallel to this, DOE and PNNL have highlighted vanadium redox flow batteries as a promising long-duration storage platform, while public projects in the U.S. and Australia are moving toward domestic electrolyte production and 24-hour grid-storage demonstrations. The demand outlook is therefore no longer defined only by steel; it is now supported by grid resilience, critical minerals policy, clean-energy storage, aerospace localization, and recycling-based processing routes. That combination positions the Vanadium Pentoxide Market as a strategic specialty materials market with industrial and energy-transition relevance.

Report covers Global vanadium pentoxide market dynamics, structure by analyzing market segments and projecting Global vanadium pentoxide market size. Clear representation of competitive analysis of key players By Application, price, financial position, product portfolio, growth strategies and regional presence in Global vanadium pentoxide market.

The Global Vanadium Pentoxide Market is currently undergoing a structural transformation as the 2026 Middle East crisis paralyzes traditional trade routes. With crude oil stabilized at $120/bbl and 400% maritime freight surcharges hindering supply from secondary producers, the cost of energy-intensive thermal reduction has spiked by 30%. Market leaders are responding by deploying AI-driven refining models and circular vanadium recovery from industrial waste to bypass the Hormuz blockade and ensure battery-grade supply.

To know about the Research Methodology :- Request Free Sample Report

Vanadium Pentoxide Market Dynamics:

Vanadium Pentoxide Market Advancement Through Energy Storage and Battery-Grade Material Development

A second major growth force came from long-duration energy storage, where vanadium pentoxide is upgraded into electrolyte materials for vanadium redox flow batteries. DOE, PNNL, and other public technical programs have repeatedly positioned flow batteries as promising for grid-scale and long-duration applications because their architecture decouples power and energy, supports large-scale stationary deployment, and fits resilience-oriented grid use cases. That has practical implications for vanadium pentoxide demand because battery-grade V2O5 and electrolyte supply require tighter purity control, more sophisticated refining, and longer-term contractual structures than conventional bulk metallurgical trade.

The commercial importance of this trend increased as governments and utilities prioritized renewable integration, microgrid resilience, and multi-hour storage rather than only short-duration lithium-ion balancing. Public and private projects in North America and Australia showed that vanadium flow battery supply chains were shifting from concept to industrial execution. The Queensland Government’s 2025 investment in a commercial-scale vanadium electrolyte facility and PNNL’s 24-hour flow battery project both signaled that vanadium pentoxide was gaining relevance not just as a mineral commodity, but as a strategic precursor for stationary energy-storage infrastructure. This broadened the market narrative beyond steel and catalysts and supported premium positioning for battery-grade material.

Technology leadership also mattered. Producers capable of manufacturing high-purity vanadium pentoxide were better positioned to supply both catalyst and electrolyte customers, creating margin expansion opportunities. Largo explicitly markets high-purity vanadium pentoxide for both catalyst and vanadium electrolyte uses, showing how product refinement is becoming a competitive differentiator. Over time, this shifts the Vanadium Pentoxide Market toward a more specialized structure in which battery applications may still be smaller than steel in tonnage but disproportionately important in pricing, purity, offtake strategy, and investor attention.

Vanadium Pentoxide Market Support From Critical Minerals Policy and Supply Security Strategies

Critical minerals policy became another structural driver for the Vanadium Pentoxide Market. The European Union classifies vanadium among its critical and strategic raw materials, explicitly linking it to the green transition, digital industries, defense, and aerospace resilience. In March 2025, the European Commission approved 47 Strategic Projects under the Critical Raw Materials Act to strengthen extraction, processing, recycling, and supply diversification. Even when those projects span multiple materials, the policy signal is highly favorable for vanadium pentoxide because it raises the commercial attractiveness of local refining, recycling, and downstream battery or specialty-alloy integration.

This policy environment helped elevate vanadium pentoxide from a cyclical industrial chemical into a strategic processed material. Governments increasingly viewed concentrated vanadium supply chains as a risk, especially because production and refining remain concentrated in a limited set of geographies. That translated into stronger support for domestic refining, recycling from spent catalysts and residues, and localized battery-electrolyte production. Public funding, accelerated permitting, and industrial policy all improved the outlook for suppliers able to offer traceable, non-Chinese, or regionally integrated V2O5 supply.

The result was a more supportive investment case across the value chain. Producers, recyclers, and project developers gained a stronger rationale to commercialize high-purity vanadium pentoxide projects because end users in defense, aerospace, chemicals, and energy storage increasingly valued secure supply as much as spot pricing. That changed procurement behavior. Instead of buying only on price, more customers began to factor in geopolitical diversification, domestic content, and long-term availability. For the Vanadium Pentoxide Market, this policy-backed shift supported project development, encouraged investment in refining capacity, and reduced the historical dependence on purely commodity-cycle economics.

Vanadium Pentoxide Market Pressure From Price Volatility and High Production Costs

The Vanadium Pentoxide Market faced a persistent restraint in the form of price volatility and uneven cost competitiveness. USGS reported that the average Chinese vanadium pentoxide price fell from $7.50/lb in 2023 to $5.45/lb in 2024, while Largo reported a 2024 European benchmark average of $5.86/lb and a year-end value close to $5.37/lb. Those swings matter because vanadium pentoxide production is capital-intensive, energy-intensive, and chemically complex. Producers must manage roasting, leaching, purification, precipitation, calcination, and residue handling, and these steps become even more expensive when customers require high-purity or battery-grade specifications.

Low-price periods create a double constraint. They suppress revenues for operating producers while also delaying financing for new mines, refineries, recycling plants, and electrolyte projects. This is especially challenging for junior developers and emerging processors that still need to prove scale, purity consistency, and commercial offtake reliability. Price weakness can therefore slow the exact investments the market needs for diversification. It also complicates long-term planning for customers, since downstream buyers want secure supply but remain cautious about paying a premium in a volatile commodity environment.

The restraint is broader than pure commodity pricing. High costs are embedded in logistics, environmental management, quality assurance, and the treatment of complex feedstocks such as spent catalysts or residues. As a result, the Vanadium Pentoxide Market often experiences a mismatch between strategic importance and near-term investment returns. Even when long-term demand fundamentals improve, project execution can remain slow because investors and operators need greater confidence in stable pricing, offtake certainty, and downstream value capture. That continues to limit how quickly new supply can come online.

Vanadium Pentoxide Market Constraints From Regulatory Complexity and Environmental Compliance

The Vanadium Pentoxide Market also faced regulatory and permitting complexity across mining, processing, waste management, transport, and end-use applications. Vanadium pentoxide is a chemically sensitive industrial material, and its production can involve hazardous intermediates, emissions control, waste streams, and occupational safety requirements. These constraints are amplified in markets that want to localize supply, because new projects often require long environmental assessments, water-use approvals, land access arrangements, residue-management systems, and air-emissions controls before commercial output begins.

On the demand side, regulatory tightening can help some applications while slowing others. For example, stricter emissions rules support catalyst demand and better materials testing, but the same broader compliance environment increases qualification costs for chemical plants, specialty materials customers, and new battery deployments. Battery-grade material especially requires more documentation, traceability, and technical validation. In aerospace and defense-linked use cases, suppliers may also need to satisfy procurement rules around domestic content, product consistency, and strategic sourcing, which lengthens commercialization cycles.

These regulatory layers do not eliminate market growth, but they do slow capacity expansion and add cost. That matters most for emerging producers outside established supply centers, since they must meet both environmental expectations and customer-specific qualification standards. In practical terms, this means the Vanadium Pentoxide Market cannot scale as quickly as demand headlines might imply. Commercial success requires not only resource availability but also permitting discipline, environmental engineering, processing know-how, and regulatory credibility across jurisdictions.

Vanadium Pentoxide Market Vulnerability to Supply Concentration and Alternative Material Competition

A further restraint came from supply concentration and competition from substitute materials. Vanadium supply remains geographically concentrated, with China dominating production and processing. This concentration creates exposure to trade policy, export behavior, regional oversupply, and pricing strategies that can affect producers and buyers elsewhere. When a large share of global processing sits in a narrow base of suppliers, non-integrated buyers face procurement uncertainty, while new entrants elsewhere struggle to compete with existing scale economics.

At the application level, vanadium pentoxide also competes with alternative chemistries and alloy systems. In steel, niobium and other microalloying approaches can sometimes reduce vanadium intensity depending on grade, specification, and local economics. In stationary storage, lithium-ion remains the dominant installed technology, which means vanadium flow battery adoption must compete on lifecycle economics, project bankability, and developer familiarity rather than only on technical suitability. In catalysts and specialty chemicals, procurement teams often optimize around total plant economics, which can delay shifts toward higher-specification vanadium products unless there is a clear performance payoff.

This competitive pressure keeps the Vanadium Pentoxide Market from expanding in a straight line. Even when vanadium offers clear technical advantages, customers do not always switch rapidly because supply security, installed-base familiarity, and capex discipline shape procurement decisions. The market therefore grows through targeted, performance-critical applications rather than universal substitution. That is a meaningful restraint because it limits pricing power and requires producers to prove value through quality, reliability, and application-specific performance rather than commodity availability alone.

Vanadium Pentoxide Market Opportunity in Emerging Economies and Localized Industrialization

One of the strongest opportunities lies in emerging economies that are simultaneously expanding infrastructure, refining capacity, sulfuric acid production, and grid investment. These markets are attractive because they can consume vanadium pentoxide through multiple channels at once: steel alloying for infrastructure, catalysts for chemicals and fertilizers, and energy storage for renewable integration. As governments in Asia, the Middle East, Latin America, and parts of Africa increase investment in industrial self-sufficiency, vanadium pentoxide becomes relevant not only as a traded oxide but as an enabling material for domestic manufacturing and power resilience.

The opportunity is especially strong where industrial policy supports critical minerals localization. Countries that want domestic long-duration storage, fertilizer-chain resilience, and stronger structural steel standards can support vanadium pentoxide demand through procurement, project finance, or public-private investment. Because V2O5 sits upstream of several strategic sectors, new industrial zones or processing hubs can generate broad multiplier effects. This is why announcements tied to electrolyte facilities, domestic flake production, and localized processing are commercially important even when absolute tonnage is still moderate. They signal the formation of regional ecosystems rather than isolated sales contracts.

For suppliers, the implication is clear: the best growth may come from region-building strategies rather than spot-market exports alone. Producers that can combine feedstock access, refining capability, and downstream partnerships in emerging industrial regions are likely to capture better margins and stronger customer stickiness than those relying only on commodity sales. That creates a meaningful long-term opening for the Vanadium Pentoxide Market in markets that are still underpenetrated but policy-active.

Vanadium Pentoxide Market Opportunity Through Recycling, Secondary Feedstocks, and Circular Processing

A major commercial opportunity is the expansion of secondary vanadium recovery. USGS highlighted that U.S. secondary production already processes petroleum residues, spent catalysts, and utility ash into ferrovanadium, vanadium-bearing chemicals, and vanadium pentoxide. This matters because recycling can improve supply resilience, lower dependence on primary mining concentration, and align with environmental and circular-economy policy goals. In a market where geopolitical diversification matters, secondary recovery is not just a sustainability story; it is a strategic supply-chain tool.

The economics of recycling can become particularly attractive in regions with large refining, petrochemical, or chemical-processing footprints, where vanadium-bearing waste streams are already generated. Recovering V2O5 from these streams can reduce import reliance, create domestic chemical-processing jobs, and give end users access to shorter, more traceable supply chains. For customers in catalysts, aerospace, and batteries, recycled or secondary-origin V2O5 can become more attractive if purity is consistent and carbon-accounting expectations rise. That opens room for specialized refiners and processors, not just miners.

This opportunity also improves industry resilience. Unlike greenfield mining, secondary-processing projects can sometimes scale faster because feedstock already exists in industrial ecosystems. If supported by policy incentives and environmental permitting frameworks, circular vanadium processing could become one of the fastest ways to expand available vanadium pentoxide supply in North America and Europe. That gives the Vanadium Pentoxide Market a practical, commercially relevant pathway to grow without waiting entirely on new mine development cycles.

Vanadium Pentoxide Market Opportunity Through Premium High-Purity and Aerospace-Linked Product Differentiation

The high-value opportunity lies in premium, high-purity vanadium pentoxide for catalysts, vanadium electrolyte, and titanium-alloy applications. U.S. Vanadium’s 2025 expansion into high-purity vanadium pentoxide flake for aerospace-grade titanium alloys shows that the market is not limited to bulk oxide demand; there is also room for differentiated products tied to defense, commercial aviation, space, and advanced manufacturing. High-purity material commands strategic attention because qualification standards are stricter and customers place greater value on supply assurance, impurity control, and domestic sourcing.

This opportunity is commercially attractive because premium markets are less exposed to pure tonnage competition. Producers able to supply consistent high-purity V2O5 can serve multiple specialized sectors at once, including sulfuric acid catalysts, advanced chemicals, and battery electrolytes. That improves portfolio resilience and reduces dependence on the lowest-priced segments of the market. It also encourages investment in refining technology, quality systems, and customer-specific product development, which can raise barriers to entry for lower-specification competitors.

Strategically, premiumization can reshape the Vanadium Pentoxide Market over the next decade. Instead of competing only on bulk oxide availability, leading firms can compete on purity, traceability, downstream integration, and application engineering. That is especially important in defense-aligned and critical-infrastructure sectors where customers value security of supply as much as commodity price. The opportunity therefore extends beyond product mix; it supports a broader shift toward value-added vanadium pentoxide business models

Vanadium Pentoxide Market Segment Analysis:

By Method

- Dry

- Wet

In 2025, the Wet segment was the largest in the Vanadium Pentoxide Market because wet processing remained the most commercially established route for recovering vanadium from slags, ores, spent catalysts, and secondary residues. The wet route was widely preferred by producers as it supported better impurity removal, higher recovery flexibility, and stronger suitability for producing technical-grade as well as high-purity vanadium pentoxide. This method typically involved leaching, solution purification, precipitation, and calcination, making it particularly suitable where feedstock quality varied across primary and recycled sources. Britannica’s processing reference notes that vanadium-bearing intermediates can be further purified through solution-based routes before precipitation into vanadium compounds, which supports the dominance of wet chemistry in commercial refining. The segment also benefited from the increasing need for controlled purity in catalyst-grade and battery-oriented applications. Compared with dry processing, the wet route offered more process adaptability for producers handling complex raw materials and industrial by-products. Its broader industrial acceptance, stronger purification capability, and compatibility with both metallurgical and specialty applications allowed the Wet segment to dominate the Vanadium Pentoxide Market in 2025.

By Application

- Sulfuric Acid Preparation

- Metal Alloys

- Oxalic Production

- Oxidation Catalyst

- Energy Storage

- Others

In 2025, the Metal Alloys segment was the largest in the Vanadium Pentoxide Market because vanadium demand remained overwhelmingly connected to metallurgical applications, especially as a feedstock for ferrovanadium used in steel production. USGS reported that metallurgical use accounted for more than 90% of domestic reported vanadium consumption in 2025, confirming that alloy-related demand continued to dominate the commercial market. Vanadium pentoxide was extensively used as an intermediate raw material in producing alloying agents that improved steel strength, wear resistance, toughness, and fatigue performance. This made it highly valuable across construction materials, pipelines, transport equipment, industrial machinery, and tool steels. The segment dominated not only because of volume demand but also because of its deep integration into established steelmaking and alloy-conversion supply chains. Compared with chemical and energy applications, metal-alloy usage had a broader industrial base and a stronger recurring demand profile. As infrastructure development, structural steel performance requirements, and industrial material optimization remained central to end-user industries, the Metal Alloys segment continued to lead the Vanadium Pentoxide Market in 2025.

Vanadium Pentoxide Market Regional Insights:

In 2025, Asia Pacific was the leading region in the Vanadium Pentoxide Market. The region dominated because it combined the world’s largest steelmaking base, the strongest concentration of vanadium production and processing, and the broadest industrial demand for vanadium-bearing materials. China remained the pivotal market, supported by its scale in steel output, vanadium mining and refining, and downstream alloy consumption. Publicly available assessments and USGS-linked market commentary consistently showed China as the largest vanadium-producing country, with processing strength that extended into vanadium pentoxide and related chemicals. This gave Asia Pacific a structural advantage in both supply and demand.

The region’s dominance was also supported by industrial policy and infrastructure intensity. Large construction programs, transportation networks, manufacturing activity, and heavy-industry demand supported strong uptake of vanadium-bearing steel and alloy products. At the same time, the region maintained an established ecosystem for vanadium processing from ore, slag, and industrial intermediates, allowing it to operate at commercial scale more efficiently than less integrated regions. This mattered because vanadium pentoxide competitiveness depends not only on resource availability but also on roast-leach refining capability, logistics, and customer proximity. Asia Pacific had all of those advantages in 2025.

Technology leadership and infrastructure added another layer of strength. The region continued to build relevance in vanadium redox flow battery deployment and upstream electrolyte development, while also serving mature catalyst and metallurgy customers. Australia’s push toward an integrated vanadium battery supply chain further strengthened regional positioning by linking mining, electrolyte manufacturing, and energy-storage use cases. As a result, Asia Pacific led the Vanadium Pentoxide Market in 2025 because it offered the most complete industrial ecosystem: resource base, refining scale, policy alignment, downstream demand, and commercialization momentum.

The objective of the report is to present a comprehensive analysis of the global Vanadium Pentoxide Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the global market dynamics, structure by analyzing the market segments and project the global market size. Clear representation of competitive analysis of key players by Grade, price, financial position, Grade portfolio, growth strategies, and regional presence in the global market make the report investor’s guide.

Global Vanadium Pentoxide Market Recent Development

August 2025: U.S. Vanadium expanded its product portfolio to include high-purity vanadium pentoxide flake, explicitly targeting aerospace-grade titanium alloys used in defense, commercial aerospace, space, and advanced manufacturing. The company stated that the new product was enabled with support from the U.S. Defense Logistics Agency and Traxys North America. This development was commercially important for the Vanadium Pentoxide Market because it highlighted a shift from commodity-grade oxide toward premium, strategically sourced, high-purity material.

September 2025: The Queensland Government announced a USD 6.87 million investment to support Vecco Group’s mine and commercial-scale vanadium electrolyte facility in Townsville, alongside partnership activity involving Idemitsu Australia. The government said the initiative would help establish Australia’s first vanadium battery supply chain and create around 600 jobs. This was a major development for the Vanadium Pentoxide Market because it moved the value chain closer to vertically integrated commercialization, linking vanadium feedstock with electrolyte production and downstream energy-storage deployment. The announcement also demonstrated that policy-backed industrialization is becoming a real demand catalyst for V2O5, especially battery-grade and electrolyte-oriented material. Strategically, the project strengthened Australia’s role inside the broader Asia-Pacific vanadium ecosystem and showed that governments increasingly view vanadium pentoxide not just as a mineral output, but as a precursor for advanced manufacturing, long-duration storage, and regional critical-minerals competitiveness.

December 2024: Stryten Energy and Largo launched Storion Energy, a joint venture designed to build a domestic supply chain for vanadium flow battery components and scalable vanadium electrolyte in North America. The companies said the platform would support a fully integrated vertical supply chain for utility-scale vanadium redox flow battery long-duration energy-storage solutions. This development mattered for the Vanadium Pentoxide Market because it connected upstream vanadium supply with downstream electrolyte commercialization, which is one of the clearest pathways for higher-value demand creation. Rather than treating vanadium pentoxide as a standalone commodity, the joint venture advanced a model in which oxide availability, electrolyte production, leasing structures, and battery deployment are commercially coordinated.

Vanadium Pentoxide Market Scope: Inquire before buying

| Vanadium Pentoxide Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 1.38 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.8% | Market Size in 2032: | 2.05 USD Billion |

| Segments Covered: | by Method | Dry Wet |

|

| by Application | Sulfuric Acid Preparation Metal Alloys Oxalic Production Oxidation Catalyst Energy Storage, Others |

||

Vanadium Pentoxide Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Vanadium Pentoxide Market Key Players

North America

1. Largo Inc. (Canada)

2. U.S. Vanadium LLC (United States)

3. Western Uranium & Vanadium Corp. (United States)

4. Energy Fuels Inc. (United States)

5. American Vanadium Corp. (United States)

6. Prophecy Development Corp. (Canada)

7. VanadiumCorp Resource Inc. (Canada)

8. Silver Elephant Mining Corp. (Canada)

Europe

9. Treibacher Industrie AG (Austria)

10. Neometals Ltd (United Kingdom)

11. Bushveld Minerals Ltd (United Kingdom)

12. Australian Strategic Materials Europe s.r.o. (Czech Republic)

13. Strategic Minerals Europe Corp. (Spain)

14. Pangang Group Vanadium Titanium & Resources Co., Ltd. – European Office (Germany)

15. Ferro-Alloy Resources Ltd (United Kingdom)

Asia-Pacific

16. HBIS Group Co., Ltd. (China)

17. Chengde Steel Group Co., Ltd. (China)

18. Pangang Group Vanadium Titanium & Resources Co., Ltd. (China)

19. TNG Limited (Australia)

20. Australian Vanadium Limited (Australia)

21. Yilmaden Holding (Turkey)

22. CNNC Huayuan Titanium Dioxide Co., Ltd. (China)

23. Hunan Valin Xiangtan Iron & Steel Co., Ltd. (China)

South America

24. Vmeta Resources S.A. (Brazil)

25. Mineração Caraíba S.A. (Brazil)

26. Largo Vanádio do Brasil S.A. (Brazil)

27. Andean Precious Metals Corp. (Bolivia)

Middle East & Africa

28. Vanchem Vanadium Products (South Africa)

29. Bushveld Vametco Alloys (South Africa)

30. Afritin Mining Ltd. (Namibia)

Frequently Asked Questions

1.What is the projected size and growth of the Global Vanadium Pentoxide Market?

Ans. The market was valued at USD 1.38 Billion in 2025 and is projected to reach USD 2.05 Billion by 2032, reflecting a 5.8% CAGR.

2. Which region currently leads the Vanadium Pentoxide Market Share Analysis?

Ans. Asia Pacific dominates due to China’s massive steel production, established refining infrastructure, and aggressive regional investment in vanadium redox flow battery energy storage systems.

3. How is the energy transition impacting Vanadium Pentoxide Market Trends 2026?

Ans. Demand is surging for battery-grade V2O5 as long-duration energy storage and vanadium flow batteries become critical for grid resilience and renewable energy integration strategies.

4. What role does high-purity material play in Industry Growth Drivers?

Ans. High-purity vanadium pentoxide flake is essential for aerospace-grade titanium alloys and advanced catalysts, allowing producers to capture premium margins beyond traditional bulk metallurgical sales.

5. How does critical minerals policy influence the Global Vanadium Pentoxide Market?

Ans. The EU’s Critical Raw Materials Act and US domestic sourcing mandates drive localized refining, strategic stockpiling, and recycling projects to ensure diversified supply chain security.

6. What are the primary production methods influencing Vanadium Pentoxide Industry Growth?

Ans. The wet processing segment leads because its superior purification capabilities enable the high-purity outputs required for battery electrolytes, catalysts, and specialized chemical-grade vanadium applications.

7. How is circular economy adoption affecting Vanadium Pentoxide Supply Chain Challenges?

Ans. Secondary recovery from spent catalysts and petroleum residues provides a sustainable, traceable supply, reducing dependence on primary mining while meeting strict environmental compliance standards.