Thin Film Material Market by Deposition Process, Types, Applications and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

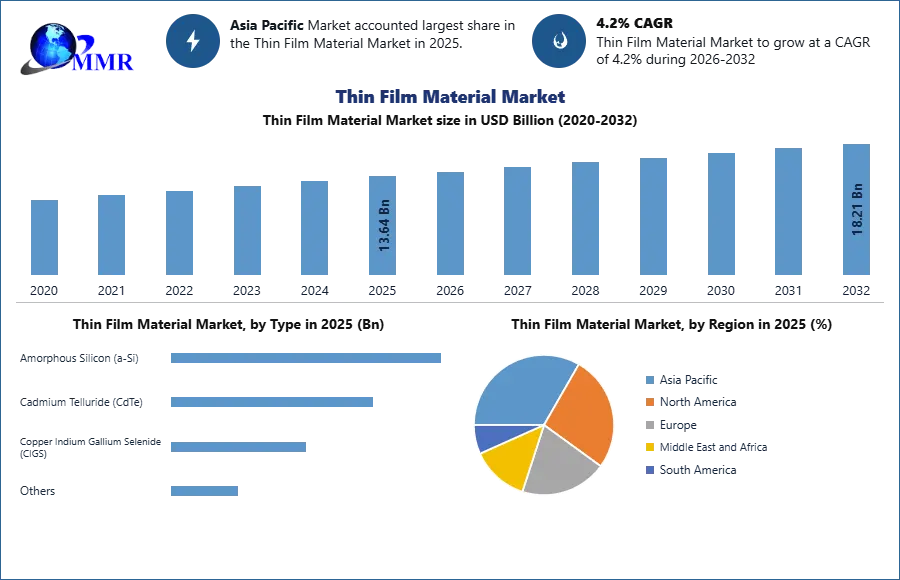

The Thin Film Material Market size was valued at USD 13.64 Billion in 2025 and the total Thin Film Material revenue is expected to grow at a CAGR of 4.2% from 2026 to 2032, reaching nearly USD 18.21 Billion.

Thin Film Material Market Overview:

Thin film materials are high-purity materials and chemicals utilized in the formation or modification of thin film deposits and substrates. Precursor gases, sputtering targets, and evaporation filaments are among the examples. A thin film is a layer of material that ranges in thickness from fractions of a nanometer (monolayer) to several micrometers. Thin film construction is mostly used in electronic semiconductor devices and optical coatings.

High demand from present and upcoming applications, growing desire for efficiency and miniaturization, technological innovation, government regulations, mandates, and subsidies are the drivers driving growth in the thin film material market. The poor conversion efficiency and large investments necessary in R&D and technology are factors restricting the growth of this industry.

Concerns about climate change and global warming have piqued the attention of numerous governments throughout the world in renewable and green energy sources. Countries such as Germany, India, the United States, and the United Kingdom are providing economic incentives and plans to stimulate and push the usage of renewable energy. Government subsidies have aided the growth of the solar power sector. Thin film materials, which are efficient, effective, and dependable, provide a solution to this challenge. One of the primary reasons for the MEMS industry's increased use of micro components is the ease with which these materials may be miniaturized.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Thin Film Material Market Dynamics:

Rising demand for Thin Films across various industries

Thin films have been used in a variety of applications in recent years, including biosensors, wearable electronics, organic field-effect transistors, infrared or microbolometer detectors, and optoelectronic and electrochromic devices in the electronics industry; solar panels and transistors in the energy industry; wound healing devices in the biomedical industry, and primary or secondary packaging and engineered plastics in the food package industry. As a result, it is increasing global demand for Thin Film Materials.

Thin films quickly found industrial uses in ornamental and optical applications. The evolution of thin film technology, aided by the development of vacuum technology and electric power facilities, has increased the range of applications to the point where almost every industrial sector now utilizes them to provide specific physical and chemical properties to the surface of bulk materials. The ability to tailor the film properties by varying the microstructure via the deposition parameters used in a specific deposition technique has recently enabled their entry from the most basic applications such as protective coatings against wear and corrosion to the most technologically advanced applications such as microelectronics and biomedicine.

Growing awareness for Nanoparticles and Thin Films

Nanoparticles and thin films are currently among the most active materials science research domains for technological applications. The attraction in nanoscale systems derives not only from the goal of miniaturization, but also from the fact that novel characteristics emerge at this length scale, and that these properties fluctuate with size, surface-to-volume ratio, and form. Understanding and controlling nanoscale characteristics have enabled scientists and engineers to develop, theoretically model, manufacture, and describe materials as well as improved functional and multifunctional gadgets of current significance.

They would then continue to contribute many applications and a vast body of research, such as information technology, electronics, spintronics, displays, memory units, sensors, biosensors, actuators, active surfaces with various properties, catalysis, energy harvesting, energy storage, environmental and safety concerns, healthcare, bioengineering, medicine, the drug industry, and so on. The advancement of these systems of organic or inorganic nanomaterials has also resulted in the advancement of technical equipment and methodologies for their production and characterization, even down to the atomic and single molecular scale.

Rising demand for Thin Films in Microelectronics

Thin films, which may be made in a variety of ways, are used in a diverse range of microelectronic applications due to their adaptability, for example, transistors, sensors, memories, energy devices, and coatings. Additionally, the electronics sector has benefited the most from thin-film technology, which helps to advance microelectronics by shrinking the sizes of semiconductor devices.

These thin-film devices have excellent mechanical deformability, sensitivity to multifunctional responses, and intelligent control capabilities. This Special Issue includes fourteen papers that highlight materials synthesis, manufacturing procedures, and potential applications that address recent advances in microelectronic systems.

Thin films are utilized in semiconductor devices to generate the conducting lines that connect individual devices, as well as the contact pads to which wires connect the circuit to the encapsulating structure. They are also utilized to create insulating layers that separate conducting films from the underlying device structure.

High-quality optical thin films are relatively thick

The growth of laser technologies has significantly boosted the need for high-quality optical thin films with adjustable and well-defined physical features. Such coatings are commonly produced in thicknesses much shorter than visible light wavelengths, posing obstacles for characterization using standard microscopy. Due to their wide variety of refractive indices, optical absorption, and frequently near-complete reflectivity in the visible spectrum, metal films in particular highlight these challenges. The bulk optical characteristics of metal thin films, on the other hand, are mostly determined by their thickness due to their relatively uniform crystalline structure.

Thin Film Material Market Segment Analysis:

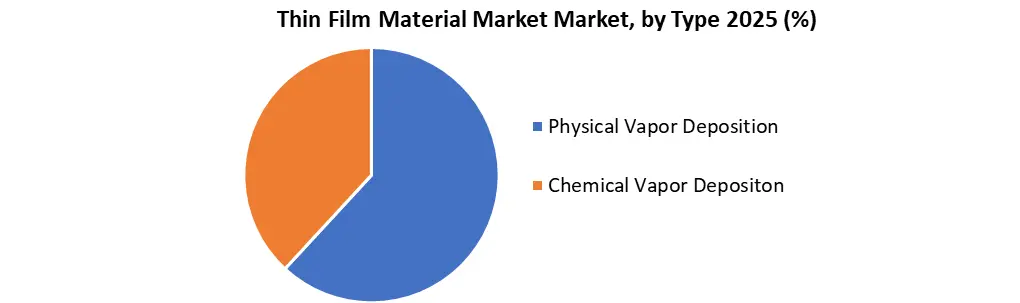

By Deposition Process, the Physical Vapor deposition (PVD) process segment held the largest market share in 2025 and is expected to dominate the market at the end of the forecast period. PVD Coating refers to a class of thin film deposition processes in which a solid material is vaporized in a vacuum atmosphere and deposited as a pure material or alloy composition coating on surfaces. It evaporates or sputters a substance, resulting in a gaseous plume or beam that deposits a coating on the substrate. It refers to a class of thin-film deposition processes that require vaporizing a solid material in a vacuum before depositing it on a substrate. These coatings are extremely robust and resistant to abrasion and corrosion.

PVD may be used to make everything from solar cells to eyewear to semiconductors. PVD has various advantages, including the development of a strong coating that is resistant to corrosion and scratches, which is driving segment growth over the forecast period. PVD can also produce thin coatings that can withstand high temperatures. Physical Vapor Deposition is the technology of choice for the surgical and medical implant industries due to its ability to produce very pure, clean, and durable coatings. Evaporation and magnetron sputtering are the most prevalent kinds of physical vapor deposition (PVD) and are commonly utilized by numerous end-user industries.

Cost is one of the potential drawbacks of PVD, since these technologies may demand a bigger investment than other thin film deposition procedures. The cost of PVD processes can also vary, which is a key restriction to segment growth.

The Chemical Vapor Deposition (CVD) segment is expected to grow substantially during the forecast period. Chemical approaches include gas phase and liquid phase deposition. Chemical vapor deposition (CVD) and atomic layer epitaxy (ALE) are gas-phase procedures, whereas spray pyrolysis, sol-gel, and spin- and dip-coating are liquid-phase approaches. CVD utilizes reactive, volatile chemicals that disintegrate on a heated substrate. The starting ingredients are frequently oregano or hydrido-compounds, which pyrolyze at low temperatures into a nonvolatile (film) component and a pumpable vapor/gas component.

Both approaches are subdivided into several ways that use auxiliary processes to attain a certain purpose. The substrate is put in a vacuum chamber, and two chemical precursors are heated, causing them to evaporate. When they collide on the substrate surface, a chemical reaction ensues, resulting in the formation of a high-performance thin film coating.

Chemical vapor deposition's key qualities and distinctive properties include its ability to produce both simple and complicated chemicals with relative ease at typically low temperatures, good throwing power, and formation of a uniform thickness coating. CVD coating growth rate is high, with ease of epitaxial layer formation and strong repeatability of coating with same or nearly identical mechanical, optical, chemical, and physical characteristics. Additionally, CVD may deposit materials with low porosity that are difficult to evaporate on a substrate of intricate forms that are difficult to manufacture using conventional deposition processes.

CVD coatings are beneficial for a broad range of applications, including medical devices, automotive components, and silicon wafers. The capacity to cover complicated or complex topographies is one of the benefits of CVD procedures, as is the flexibility to apply these processes on a broad range of substrates. Thin films formed by CVD often retain their bonds effectively in high-stress settings.

Thin Film Material Market Regional Insights:

The Asia-Pacific region accounts for the largest market share in the thin film material market globally in 2025 and is expected to be the fastest-growing region over the forecast period. The region's growth is being driven by the increasing acceptance of technical breakthroughs, as well as increased industrial and assembly operations. Additionally, rising population, changing consumer lifestyles, rising solar photovoltaic cells for solar power production plants, rising demand for electronic products, and growing awareness of finite resources are expected to drive regional growth during the forecast period.

In terms of capacity, India and China control the majority of the largest solar photovoltaic power facilities. The Tengger solar park in China, located in Zhongwei, Ningxia, spans over 1,200 kilometers and generates 1,547 megawatts of power. The Bhadla solar farm in India, located in the Jodhpur area of Rajasthan, is scheduled to open in 2025. The plant's capacity is expected to be 2,255 megawatts of power and is distributed across 45 square kilometers. Innovative regional initiatives, such as the Thin-Film Solar Wall Project in Heyuan City, Guangdong Province, China, are expected to open up new doors for the market under consideration.

In addition, key businesses are utilizing methods such as new product releases and corporate expansions to strengthen their position in the global market. For example, Kaneka Corporation (Japan) announced the development of PixeoTM IB, a heat-resistant polyimide film, in November 2025. This new material introduction would allow the firm to increase its product portfolio and sales of 5G-supporting items, allowing digital gadgets to achieve improved functionality.

North America is seeing significant growth as a result of the region's sales output and industrial capacity. The easy availability of revolutionary technology, tight regulatory rules to reduce carbon emissions, and increased usage and deployment of solar panels are the primary drivers of the thin film industry's growth. Additionally, rising demand for thin film material from the IC manufacturing sectors is driving regional growth throughout the forecast period.

However, emerging industrial and electronic lines of business in developing economies such as the United Kingdom, Germany, France, Italy, and Spain are driving the European market. The rapid use of artificial illumination such as LEDs to boost crop performance, particularly in northern Europe, is driving the regional market growth. In addition, increased PV panel installation in Germany for greater energy independence would boost demand for thin films for PV material. Rooftop installations in the United States were increased by 20% in 2025, owing to lower solar technology prices, improved subsidy conditions, and other reasons.

The Middle East and Africa are anticipated to experience consistent growth as a result of hardware sector restructuring paired with growing development in the microelectronics industry, driving company growth. Latin America is facing significantly slower growth as a result of increased material production costs. Brazil is expected to be the most important market for thin film materials in Latin America during the forecast period, owing to increased demand for thin films in a variety of sectors.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 17 March 2026 | Sono-Tek Corporation | Entered a technical collaboration with Diamond Quanta to integrate precision ultrasonic coating for engineered diamond thin films on glass. | This partnership advances thermal management and semiconductor performance by commercializing high-conductivity diamond-on-glass substrates. |

| 11 March 2026 | Sono-Tek Corporation | Secured an $820,000 order for advanced thin-film coating systems specifically designed for diagnostic medical devices. | Strengthens the company's market share in the high-growth medical coating segment, improving yield for bio-functional thin films. |

| 14 January 2026 | Samsung Display | Announced the transition to Atomic Layer Deposition (ALD) for its 8.6-generation IT OLED lines to enhance thin-film encapsulation. | This technological shift provides superior moisture barriers, significantly extending the lifespan of foldable and automotive display panels. |

| 29 October 2025 | First Solar, Inc. | Commissioned a new R&D center focused on tandem perovskite-silicon thin-film modules to push commercial efficiency past 25%. | Accelerates the commercialization of high-efficiency PV, reducing the levelized cost of energy (LCOE) for utility-scale solar projects. |

| 13 October 2025 | Sono-Tek Corporation | Awarded a $2.8 million contract for the delivery of multiple ultrasonic deposition systems for next-generation electronics. | Expands industrial capacity for functional thin films, meeting the surge in demand for miniaturized semiconductor components. |

| 12 August 2025 | Kaneka Corporation | Launched a mass-production facility for flexible polyimide thin films optimized for high-speed 6G communication hardware. | Positions the firm as a primary supplier for the next wave of ultra-high-frequency telecommunications and flexible circuit boards. |

Thin Film Material Market Scope: Inquire before buying

| Thin Film Material Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 13.64 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.2% | Market Size in 2032: | 18.21 USD Billion |

| Segments Covered: | by Deposition Process | Physical Vapor Deposition (PVD) Chemical Vapor Deposition (CVD) |

|

| by Type | Amorphous Silicon (a-Si) Cadmium Telluride (CdTe) Copper Indium Gallium Selenide (CIGS) Others |

||

| by Application | Photovoltaic Solar Cells MEMS Semiconductors & Electronics Optical Coatings Others |

||

| by End-User | Video Surveillance Traffic Monitoring Security & Monitoring Industrial Monitoring Others |

||

Thin Film Material Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Thin Film Material Market Report in Strategic Perspective:

- Anwell Solar

- Ascent Solar Technologies Inc.

- Avancis GmbH

- Cicor Technologies Ltd.

- First Solar Inc.

- Hanergy Thin Film Power Group

- Kaneka Solar Energy

- Masdar PV GmbH

- Solar Frontier K.K.

- Suntech Power Holdings Co., Ltd.

- Trony Solar Holdings Co., Ltd.

- Moser Baer India Limited

- Stanford Advanced Materials

- Umicore Group

- JX Nippon Mining & Metals Corporation

- American Elements

- Corning Incorporated

- Global Solar Energy, Inc.

- MiaSolé Hi-Tech Corp.

- Solibro GmbH

- Oxford PV

- Samsung SDI Co., Ltd.

- Delta Optical Thin Film A/S

- China Singyes Solar Technologies Holdings Ltd.

- Kyocera Corporation