Superluminescent Diodes Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

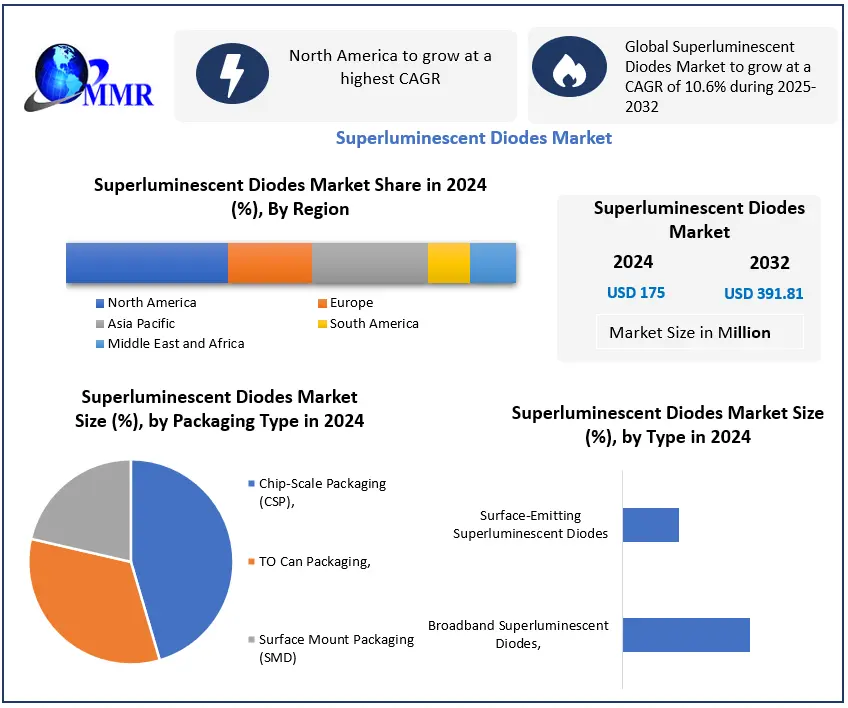

Superluminescent Diodes Market size was valued at USD 175 Million in 2024 and the total Global Superluminescent Diodes Market revenue is expected to grow at a CAGR of 10.6% from 2025 to 2032, reaching nearly USD 391.81 Million.

Superluminescent Diodes Market Overview

Superluminescent diodes (SLDs) are broadband light sources that emit light with a short coherence length and high brightness, making them ideal for applications such as spectral domain optical coherence tomography (SD-OCT), fiber optic gyroscopes (FOG), and optical sensing. Thorlabs offers visible-wavelength SLDs in TO-56 can or butterfly packages, as well as a selection of NIR-wavelength SLDs in butterfly packages that includes versions optimized for use in SD-OCT systems. SLD benchtop sources are also available, which are all-in-one solutions that integrate an SLD, controller, and TEC in one unit with either a single mode or polarization-maintaining FC/APC output. Additionally, a 4-channel laser/SLD source is configured with up to four user-selected laser diodes or SLDs, each with its own independent TEC and microcontroller.

In 2023, Mitsubishi Electric announced advancements in superluminescent diodes (SLDs) specifically designed to increase output power. These developments are aimed at improving the performance of LIDAR (Light Detection and Ranging) systems used in the automotive sector, particularly for autonomous vehicles and advanced driver assistance systems (ADAS) in the Superluminescent Diodes Market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Superluminescent Diodes Market Dynamics

Rising Demand for Diodes in communication technologies to boost Superluminescent Diodes Market growth

The rising demand for diodes in the superluminescent diodes market is being driven by significant advancements in imaging, sensing, and communication technologies. Superluminescent diodes, which combine the high brightness of lasers with the low coherence of LEDs, are increasingly essential for applications such as optical coherence tomography (OCT), fiber-optic gyroscopes, and LIDAR systems. In the healthcare sector, the growing use of OCT in medical diagnostics, especially in ophthalmology and cardiovascular imaging, is fuelling the demand for high-performance SLDs. Similarly, the automotive and aerospace industries are witnessing increased adoption of SLDs for advanced sensing technologies, including LIDAR, which is vital for autonomous vehicles. Additionally, the communication industry is leveraging SLDs for fiber-optic networks, where their broad emission spectrum enables more efficient and reliable data transmission over long distances.

In 2023, the value of silicon diodes produced in Japan amounted to approximately 12.46 Million Japanese yen, reflecting the growing importance of these components in the global Superluminescent Diodes market. Silicon diodes, a subset of discrete semiconductors, play a critical role in various electronic devices, from rectifiers and transistors to thermistors and thyristors. The production value of silicon diodes in Japan, which has shown steady growth from 2015 to 2023, highlights the increasing use of these diodes across the semiconductor industry. The increasing need for high-efficiency, reliable semiconductor components to power modern technologies, such as electric vehicles, renewable energy systems, and advanced manufacturing equipment, is expected to further drive the demand for silicon diodes. The combination of the growing demand for superluminescent diodes and the broader semiconductor market underscores the critical role these components play in the continued development of cutting-edge technologies.

Thermal Management Issues are becoming obstacles in the Superluminescent Diodes Market

Superluminescent Diodes tend to generate considerable heat during operation, which degrade their performance and lifespan if not properly managed. Effective cooling solutions, such as advanced heat sinks or thermoelectric coolers, must be integrated to dissipate heat. However, these solutions add to the overall cost, size, and complexity of the device, making it less attractive for compact or cost-sensitive applications. Poor thermal management leads to early failure or reduced efficiency, hindering the widespread adoption of SLEDs, especially in industries that require long-lasting and stable light sources. The superluminescent diodes market is the complex and precise manufacturing process required to produce high-quality diodes. SLEDs involve intricate design specifications to ensure they deliver broad spectrum emission with low coherence, which is critical for applications like optical coherence tomography (OCT) and sensing. Achieving these parameters demands stringent quality control, advanced fabrication techniques, and high-purity materials, which increase production costs and time. This complexity makes it difficult for manufacturers to scale production efficiently, limiting the availability of these components, especially for emerging markets where cost and accessibility are key factors.

Superluminescent Diodes Market Segment Analysis

By Type the market is segmented into Broadband Superluminescent Diodes and Surface-Emitting Superluminescent Diodes. The Broadband Superluminescent Diodes segment dominated the market in 2024 & is expected to hold the largest market share during the forecast period. Due to their extensive use in optical coherence tomography (OCT), fiber optic gyroscopes, sensing, and imaging applications. Ability to provide a wide spectral range with high output power and low coherence makes them highly suitable for precision medical diagnostics and industrial inspection, accuracy and resolution are critical. Healthcare remains a leading end-user of SLDs, and broadband types are the preferred choice in OCT for ophthalmology and cardiology. Growing adoption in aerospace, defense, and telecom reinforces their market dominance over surface-emitting SLDs, remain more niche.

By Wavelength Range the market is segmented in to Infrared (IR) Superluminescent Diodes, Visible Superluminescent Diodes, Ultraviolet (UV) Superluminescent Diodes. They are widely used in optical coherence tomography (OCT), fiber optic gyroscopes, optical communication, and sensing applications. The IR range, particularly between 800 nm and 1550 nm, is ideal for medical imaging (especially ophthalmology), industrial metrology and defense navigation systems due tO deeper penetration and low scattering properties. Strong demand from telecommunications and aerospace sectors for high-performance IR-based devices drives this segment. While visible and UV SLDs are growing in niche imaging and scientific research applications, IR SLDs remain the mainstream choice, ensuring their leadership.

Superluminescent Diodes Market Regional Analysis

North America holds a dominant position in the global superluminescent diodes market, driven by its strong technological infrastructure, advanced medical diagnostic systems, and substantial investments in the aerospace and defense sectors. The North American regional share is bolstered by the significant adoption of SLDs in optical coherence tomography (OCT) applications, particularly in the U.S., where the demand for high-precision imaging in ophthalmology, cardiovascular diagnostics, and dermatology is rapidly growing. Additionally, the aerospace and defense industries in the region heavily utilize superluminescent diodes for fiber-optic gyroscopes and navigation systems. The strong presence of key players, coupled with government initiatives in R&D for advanced photonics technologies, further strengthens North America's leading market share. In 2023, North America accounted for approximately 38% of the global market, making it the dominating region. The U.S., in particular, is seeing substantial production and consumption of SLDs, positioning it as a key driver of market growth.

The Asia-Pacific region is rapidly developing in the superluminescent diodes market, showcasing impressive growth rates, particularly in China and Japan. China’s production rate of superluminescent diodes is accelerating due to the country’s burgeoning telecommunications industry and increasing investments in medical technologies. The Chinese market is also benefiting from government support for the development of optoelectronic technologies, making it a crucial hub for future development in the Superluminescent Diodes market. Meanwhile, Japan’s production rate is driven by the country’s focus on innovation in the optical technologies sector and its strong presence in the automotive and aerospace industries, where SLDs are being increasingly integrated into advanced navigation and sensor systems. The Asia-Pacific regional share is expected to grow significantly, currently contributing around 28% of the global market. With an emphasis on research and development in optoelectronics and favorable government policies, Asia-Pacific is emerging as the fastest-developing region in the superluminescent diodes market, poised for substantial growth in the next few years.

Superluminescent Diodes Market Competitive Landscape

The competitive landscape between Superlum and Thorlabs, Inc. in the superluminescent diodes market is marked by intense rivalry, driven by both companies’ pursuit of innovation and technological advancement. Superlum, a pioneer in SLD technology, has established a strong presence through its extensive portfolio of high-performance superluminescent diodes used in applications like optical coherence tomography (OCT), fiber-optic gyroscopes, and interferometry. Superlum’s focus has been on the continuous enhancement of its products, with recent launches aimed at increasing wavelength ranges and improving output power, catering to the medical diagnostics and industrial sectors. Thorlabs, on the other hand, is a formidable competitor, leveraging its broader photonics expertise to dominate the global market. Thorlabs' product launches, such as high-power SLDs with integrated controllers and broadband sources, have targeted industries requiring precision in imaging and sensing. This rivalry has pushed both companies to rapidly innovate, offering solutions that meet the growing demand for compact, high-efficiency SLDs in both medical and aerospace markets.

In addition to product launches, partnerships, mergers, and acquisitions have been key strategies in maintaining a competitive edge. Thorlabs, with its expansive reach and vertically integrated business model, has strategically acquired smaller firms in the photonics space, enhancing its product portfolio and broadening its market share. For instance, Thorlabs' acquisition of Covega Corporation expanded its capabilities in semiconductor devices, boosting its presence in the SLD segment. Superlum, however, has focused more on partnerships to enhance its global distribution and innovation. The company has collaborated with key medical device manufacturers to integrate SLD technology into next-generation imaging systems, securing its foothold in the healthcare sector. While Thorlabs' mergers and acquisitions strategy has helped it achieve global expansion, Superlum's partnerships have enabled it to remain competitive in niche markets like high-precision medical diagnostics. This strategic rivalry between the two companies continues to shape the competitive landscape of the superluminescent diodes market, driving innovation and market growth.

Superluminescent Diodes Market Ecosystem:

Superluminescent Diodes Market Scope: Inquire before Buying

| Global Superluminescent Diodes Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 175 Mn. |

| Forecast Period 2025 to 2032 CAGR: | 10.6% | Market Size in 2032: | USD 391.81 Mn. |

| Segments Covered: | by Type | Broadband Superluminescent Diodes Surface-Emitting Superluminescent Diodes |

|

| by Wavelength Range | Infrared (IR) Superluminescent Diodes Visible Superluminescent Diodes Ultraviolet (UV) Superluminescent Diodes |

||

| by Packaging Type | Chip-Scale Packaging (CSP) TO Can Packaging, Surface Mount Packaging (SMD) |

||

| by Application | Optical Coherence Tomography (OCT) Communication Systems Spectroscopy, Industrial Applications |

||

| by Vertical | Healthcare Telecommunications Consumer Electronics Aerospace and Defense |

||

Superluminescent Diodes Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, and Rest of APAC)

Middle East and Africa (South Africa, GCC, and Rest of the MEA)

South America (Brazil, Argentina, and Rest of South America)

Superluminescent Diodes Key Players

North America:

1. Thorlabs, Inc. (USA)

2. Innolume GmbH (USA)

3. QPhotonics, LLC (USA)

4. Frankfurt Laser Company (USA)

5. Exalos AG (USA)

6. Anritsu Corporation (USA)

Europe:

7. Superlum (Ireland)

8. Sacher Lasertechnik GmbH (Germany)

9. Innolume GmbH (Germany)

10. NKT Photonics A/S (Denmark)

11. TopGaN Lasers (Poland)

12. Denmark Photonics (Denmark)

13. AMS Technologies AG (Germany)

14. G&H (Gooch & Housego PLC) (UK)

Asia-Pacific:

15. Thorlabs Japan, Inc. (Japan)

16. QPhotonics, LLC (Japan)

17. Hamamatsu Photonics K.K. (Japan)

18. Kyocera Corporation (Japan)

19. OZ Optics Ltd. (China)

20. Altechna R&D (Lithuania)

21. Fuji Electric Co., Ltd. (Japan)

South America:

22. BrPhotonics (Brazil)

23. Opton Laser International (Brazil)

Middle East & Africa:

24. Eblana Photonics Ltd. (South Africa)

25. Lightwave Logic, Inc. (UAE)

Frequently Asked Questions:

1. What are the major drivers influencing the growth of the superluminescent diode market?

Ans: The major drivers for this market are the growing need for optical coherence tomography (OCT) imaging systems and fiber optic gyroscopes (FOG), increasing usage of super luminescent diode (SLDs) in automotive headlight and taillight systems, as well as, rising demand for ultraviolet (UV) and infrared (IR) LEDs.

2. Which region held the largest market share in the Superluminescent Diodes market?

Ans: North America held the largest position in the Superluminescent Diodes market.

3. Who are the key players in the Superluminescent Diodes market?

Ans: Thorlabs, Inc. (USA), Innolume GmbH (USA), QPhotonics, LLC (USA), Frankfurt Laser Company (USA), Exalos AG (USA), Anritsu Corporation (USA).

4. What are the major segments for the superluminescent diode market?

Ans: The future of the superluminescent diode market looks promising with opportunities in the medical diagnostics, aerospace-gyroscopes, navigators, and light band interferometry markets.

5. What is the superluminescent diode market size?

Ans: The global superluminescent diode market is expected to reach an estimated 391.81 million by 2032.