Smart Meters Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2030

Overview

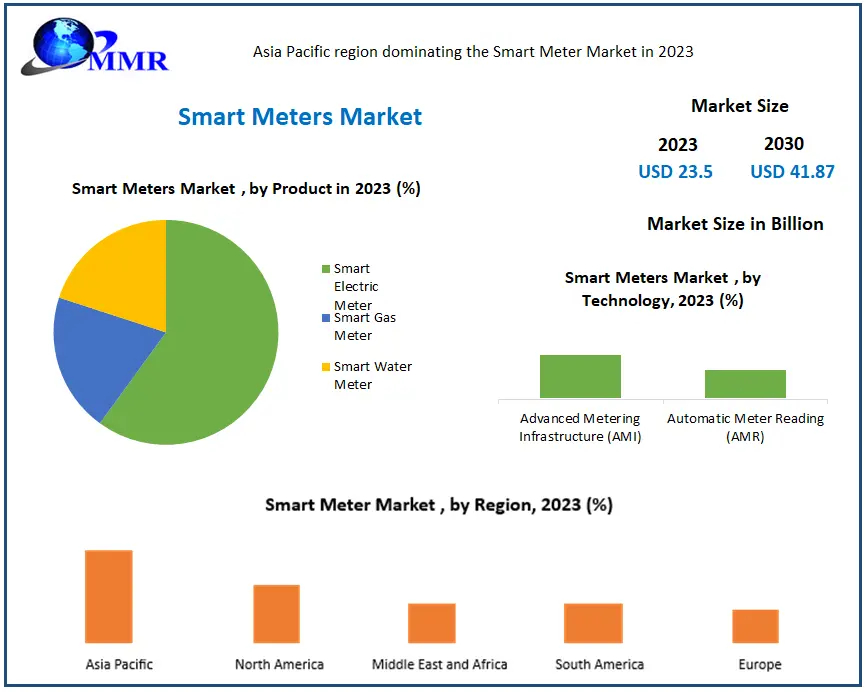

The Smart Meters Market size was valued at USD 23.5 Billion in 2023 and the total Smart Meter revenue is expected to grow at a CAGR of 8.6 % from 2024 to 2030, reaching nearly USD 41.87 Billion by 2030.

Smart Meters Market Overview

The Smart Meters Market is of paramount importance in the modern energy landscape, facilitating efficient energy management and promoting sustainability. Smart meters offer both qualitative and quantitative benefits, enabling consumers to monitor their energy usage in real-time and make informed decisions to reduce consumption and lower utility bills. Moreover, for utility providers, smart meters enhance operational efficiency by automating meter readings, detecting energy theft or tampering, and improving outage management. These devices Contributes its role in achieving research objectives related to energy conservation, grid optimization, and environmental impact reduction.

Smart meters find applications across various sectors, including residential, commercial, and industrial. In the residential sector, smart meters empower homeowners to monitor and manage their energy usage, optimize appliance usage, and reduce utility bills. In commercial and industrial settings, smart meters enable businesses to track energy consumption in real-time, identify inefficiencies, and implement energy-saving measures to improve operational efficiency and reduce costs.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

North America is a growing market for smart metering owing to increased adoption and regulatory support. Countries like the US and Canada are focusing on grid modernization and energy efficiency, offering opportunities for smart meter brands to expand their presence and capitalize on advanced solutions.

Key players such as Itron Inc., Landis+Gyr, and Siemens AG dominate the market, leveraging their brand reputation and technological expertise to maintain their foothold. However, emerging players and startups are also entering the market, offering innovative solutions and challenging established brands' market positions.

Smart Meters Market Dynamics:

Increasing Mobile Device Management Activities Driving the Smart Meters Market

The increasing adoption of mobile device management (MDM) activities is playing a fundamental role in driving the growth of the Smart Meters Market. With the evolution of IoT and advanced smart metering solutions, MDM has become essential for efficiently managing and integrating these devices within existing infrastructure. Companies are increasingly turning to IoT platforms like ThingsBoard, which offer out-of-the-box solutions and templates tailored for smart metering applications. These platforms not only streamline data collection from diverse smart meters but also provide robust data processing capabilities, enabling companies to analyze consumption patterns and optimize resource usage. This streamlined approach to smart metering implementation significantly reduces time-to-market and mitigates risks associated with in-house development. As a result, companies leveraging MDM activities through IoT platforms are poised to gain a competitive edge, driving market growth and expanding their market share in the smart metering sector.

1. Tata Power Delhi Distribution Limited (Tata Power-DDL): The main goals of Tata Power-DDL's data processing via MDM were increased billing efficiency, improved customer services, and revenue protection. In addition to lowering the discom's AT&C losses, AMI offered a number of value-added services.

2. Low-power-wide-area-network (LPWAN) cellular technologies are key enablers of this, such as Narrowband-IoT (NB-IoT). NB-IoT combines efficient communication with low power demands that extend battery life for mass-distributed devices over wide geographical areas and deep within urban infrastructure — ideal for smart meter systems.

3. The “Internet Platform for Smart Manufacturing Industry for Electricity Metering Product (Intelligent manufacturing industrial interaction of electric energy metering products Internet platform) project of Wasion Group was listed as Hunan Provincial Industrial Internet Platform (Hunan Province Provincial Industrial Internet Platform)

Smart Meters Inclusion of Artificial Intelligence and Machine Learning

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into smart meters presents a significant opportunity for the Smart Meters Market. By leveraging AI and ML algorithms, smart meters analyze vast amounts of data collected from various sources, including consumer behavior, weather patterns, and energy consumption trends. This advanced analytics capability enables smart meters to optimize energy distribution, detect anomalies, and predict future demand more accurately. As a result, utility companies improve operational efficiency, reduce production costs, and enhance revenue trends by offering personalized energy solutions tailored to individual consumers' needs. Moreover, as the global population continues to rise and per capita energy consumption increases, the demand for smart meters equipped with AI and ML capabilities is expected to surge, further driving market growth and innovation in the smart metering sector.

Reduction in Investments for Infrastructure Development and Low Investment Returns Hindering the Smart Meters Market Growth.

One of the significant restraints facing the Smart Meters Market is the reduction in investments for infrastructure development and low investment returns. While the deployment of smart meters offers numerous benefits such as improved energy management and cost savings, the initial investment required for infrastructure development can be substantial. This is particularly challenging for regions or countries with limited financial resources or competing priorities for infrastructure spending. As well, the return on investment (ROI) for smart meter projects may not always meet initial expectation owing to factors such as regulatory constraints, unpredictable consumer behavior, or lengthy payback periods. As a result, some utility companies may hesitate to invest in large-scale smart meter deployments, leading to slower market growth and market concentration among larger players with greater financial capacity. Besides, uncertainties surrounding the regulatory landscape and evolving industry standards further complicate investment decisions, potentially dampening investor confidence in the Smart Meters Market.

1. According to three persons familiar with the subject, Eversource Capital is in discussions to fund $100 Billion for its smart meter technology with institutional investors and sizable family offices.

2. According to ICRA, the government is unlikely to be able to install 250 billion smart meters by 2025, despite the fact that the number of smart meter installations in the nation is expected to rise over the following two years.

Smart Meters Market Segment Analysis:

Based on End Users, the Smart Meters Market, segmented into residential, commercial, and industrial applications, is witnessing dynamic growth driven by diverse factors. With the residential sector commanding a significant customer base in terms of electricity and water consumption, supported by government initiatives like LPG supply through pipelines, its dominance is evident. Urbanization further fuels this growth, extending benefits to the commercial and industrial sectors where new constructions and small-scale industries drive smart meter installations. Additionally, technological advancements are enhancing the value proposition of smart meters, offering benefits beyond consumption monitoring, such as predictive maintenance and demand-side management. As a result, the Smart Meters Market is experiencing sustained expansion across all sectors, propelled by urbanization trends, regulatory mandates, and the imperative for resource optimization, thus reshaping energy management paradigms worldwide.

Based on Product Type, Among the three types of smart meters, the Smart Electric Meter stands out as a leading segment owing to its widespread adoption and transformative impact on energy management. Smart electric meters enable utilities and consumers to monitor electricity consumption in real-time, facilitating efficient resource allocation and cost savings.

1. One notable example of a leading smart electric meter is the "Itron OpenWay Riva," which offers advanced functionalities such as grid optimization, outage detection, and voltage management.

By providing actionable insights into energy usage patterns, smart electric meters empower both utility providers and consumers to make informed decisions, enhance grid reliability, and promote sustainability.

Smart Meters Market Regional Analysis:

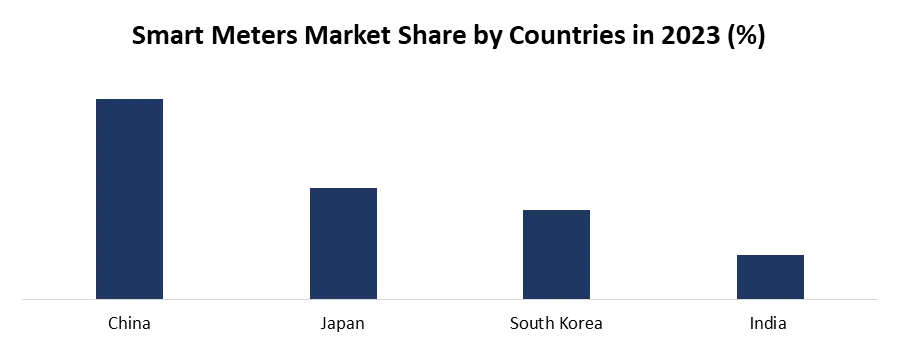

In the Smart Meters Market, The Asia-Pacific region contributes the highest market share during the forecast period, leading the global market with its rapid adoption and robust growth trajectory. Within this region, several countries are spearheading the market expansion, including China, Japan, South Korea, and India. China, boasting one of the world's largest populations and undergoing extensive urbanization, leads the charge with substantial investments in smart grid infrastructure and ambitious renewable energy targets. Japan and South Korea follow closely, driven by advanced technological capabilities and government initiatives promoting energy efficiency and sustainability.

1. Also, India is emerging as a key growth market, propelled by initiatives such as the Smart Cities Mission and the Ujwal DISCOM Assurance Yojana (UDAY), which aim to modernize electricity distribution and promote renewable energy integration.

2. More than 20% of the domestic market share of high-end metering products, has built up its leading position in China and Wasion Group Holdings is the only professional manufacturer in China which provides various advanced energy metering products, systems and services for electricity, water, gas and heat, as well as satisfies the demand of the whole process from energy production, transmission and distribution to consumers.

3. India gets 31% of its power from renewables (not including hydro). The US is at 25%

4. At current prices of solar and wind in India, coal-based power is 50% more expensive

5.India’s energy demand grew by 10% in 2022 and the country’s expected to account for 25% of global energy demand growth over next 20 years

Competitive Landscape of Smart Meters Market:

The competitive landscape of the Smart Meters Market is characterized by intense rivalry among key players striving to gain market share and establish dominance. Major companies such as Itron Inc., Landis+Gyr, and Siemens AG compete fiercely by offering innovative solutions, expanding their product portfolios, and pursuing strategic partnerships and acquisitions. These players focus on enhancing their technological capabilities, improving product quality, and providing comprehensive customer support to maintain a competitive edge. Additionally, emerging players and startups are entering the market with niche offerings and disruptive technologies, further intensifying competition. Regulatory compliance, pricing strategies, and geographic expansion are crucial factors influencing companies' positioning in this dynamic market landscape. As the demand for smart meters continues to rise globally, the competitive landscape is expected to evolve, driving innovation and consolidation among market players.

1. In January 2023, Badger Meter Inc. declared the strategic acquisition of Syrinix Ltd., a provider of intelligent water monitoring solutions. Through this acquisition, the company aims to add the hardware-enabled software capabilities of Syrinix to our smart water solutions portfolio. Similarly, it has also acquired Analytical Technology, Inc. (Ati) and Scan GmbH, leaders in intelligent measurement and smart water quality monitoring.

2. In January 2023, Diehl Stiftung & Co. KG proclaimed that the Water and Sanitation Corporation (WASAC) in Rwanda's capital, Kigali, chose Diehl Metering for meter technology to modernize its network for its sustainability efforts. WASAC recognized the suitability of AURIGA to achieve its primary objective of reducing non-revenue water by installing reliable meters. The AURIGA water meter will form the basis for a future AMR solution.

3. In December 2022, Apator SA presented the smartESOX pro, which was specially designed for industrial applications, and the OTUS 3, a bidirectional smart electricity meter. Other smart options were presented, such as the Ultrimis W ultrasonic water meter and the iSMART2 gas meter.

4. Smart meter installations are a key component of the revamped distribution sector scheme (RDSS) launched by the Centre in July 2021, which follows the design, build, finance, own, operate, and transfer (DBFOOT) model for the installation of smart meters to bring down aggregate technical and commercial (AT&C) losses and reduce the gap between the cost of supply and tariff to zero.

Global Smart Meters Market Scope: Inquire before buying

| Smart Meters Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 23.5 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 8.3% | Market Size in 2030: | US $ 41.87 Bn. |

| Segments Covered: | by Product Type | Smart Electric Meter Smart Gas Meter Smart Water Meter |

|

| by Technology | Advanced Metering Infrastructure (AMI) Automatic Meter Reading (AMR) |

||

| by End-Use | Residential Commercial Industrial |

||

Global Smart Meters Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Smart Meters Market Key Players:

North America:

1. Aclara Technologies LLC - USA

2. Itron Inc. - USA

3. Sensus USA Inc. - USA

4. Neptune Technology Group Inc. - USA

5. Badger Meter – USA

6. General Electric Ltd - USA

Europe:

1. Elster Group SE - Germany

2. Kamstrup A/S - Denmark

3. Diehl Stiftung & Co. KG - Germany

4. IGL Genesis Technologies - Germany

5. Pietro Fiorentini - Italy

6. Sagemcom SAS - France

7. Apator S.A - Poland

8. Honeywell International - USA

9. EDMI - UK

Asia-Pacific:

1. Jiangsu Linyang Energy Co. Ltd - China

2. Ningbo Sanxing Electric Co. Ltd - China

3. Hexing Electric Company Ltd - China

4. Holley Metering Limited - China

5. Shenzhen Hemei Group Co. Ltd – China

6. Wasion Group Holdings - China

FAQs:

1. What are the growth drivers for the Smart Meters market?

Ans. Increasing mobile device management activities driving the Smart Meters Market

2. What are the major restraining factors for the Smart Meters Market growth?

Ans. Reduction in Investments for Infrastructure Development and Low Investment Returns is a restraining factor of Smart Meters Market

3. Which region is expected to lead the Smart Meters Market during the forecast period?

Ans. Asia Pacific is expected to lead the Smart Meters Market during the forecast period

4. What is the projected market size and growth rate of the Smart Meters Market?

Ans. The Smart Meters Market size was valued at USD 23.5 Billion in 2023 and the total Smart Meters revenue is expected to grow at a CAGR of 8.6 % from 2024 to 2030, reaching nearly USD 41.87 Billion.

5. What segments are covered in the Smart Meters Market report?

Ans. The segments covered in the Smart Meters Market report are Product Type, Technology, End Use, and Region.