Printed Circuit Boards (PCBs) Market Size by Segments,Country and Region – Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

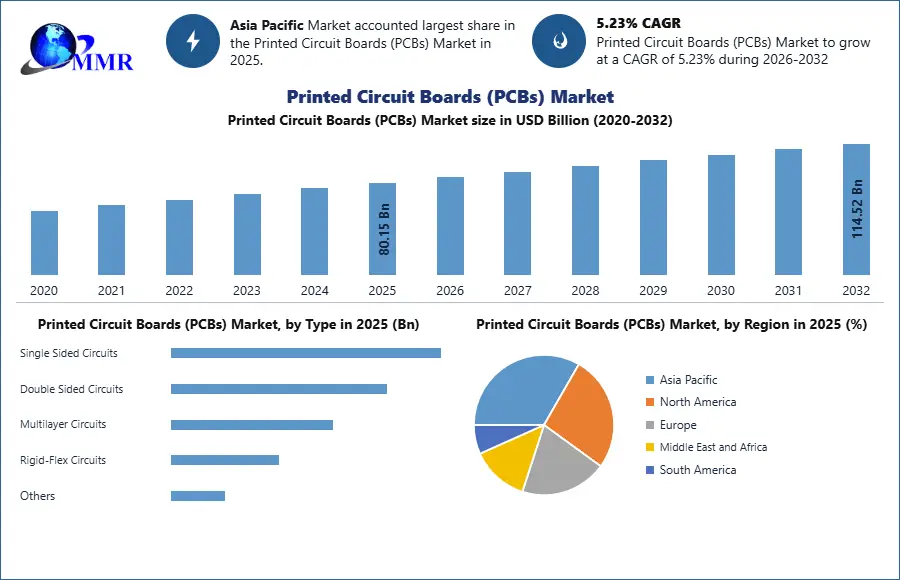

The Printed Circuit Boards (PCBs) Market size was valued at USD 80.15 Billion in 2025 and the total Printed Circuit Boards (PCBs) revenue is expected to grow at a CAGR of 5.23% from 2025 to 2032, reaching nearly USD 114.52 Billion by 2032.

Printed Circuit Boards (PCBs) Market Overview

A printed circuit board, or PCB, is a device that uses conductive paths, tracks, or signal lines etched from copper sheets laminated onto a non-conductive substrate to mechanically support and electrically connect electronic components. Printed wire (circuit) boards are now employed in almost all commercially produced electronic devices, allowing completely automated assembly procedures that were previously impossible or impractical with tag-type circuit assembly. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Printed Circuit Boards (PCBs) Market Dynamics:

Due to the growing demand for multi-functional systems, the PCB has become a significant factor in determining the functioning and look of high-tech smart device components. The global printed circuit board market is expected to grow due to the rising demand for electronic equipment and telecommunication devices.

The increased demand for electronic gadgets is the main driver of the global printed circuit board industry. Electronics such as cellphones, computers, and other devices have become a need for many people, and as technology progresses, people need to upgrade to the next level to keep up. PCB is used in industrial equipment such as cell towers, automated machinery, and other machines to achieve rapid operation and waste reduction/process improvement.

Due to social alienation, the demand for electronic devices has surged during the COVID-19 epidemic. Demand for smartphones, computers, and tablets has surged as a result of online classes and work from home; requirements for new medical equipment, among other things, have also increased. In addition, as the world's population grows, so does the market penetration of electronic goods, increasing demand for printed circuit boards.

Market growth is being hampered by stringent restrictions governing e-waste generated from printed circuit boards. Hazardous compounds used in printed circuit boards, including lead (Pb), epoxy resins, cadmium (Cd), and mercury (Hg) do not degrade effectively and may contribute to a considerable portion of e-waste around the world. Regulations have stifled the use of low-cost raw materials in PCB manufacturing, thus reducing the profitability of PCB manufacturers.

PCB Use in Various Industries:

Printed circuit boards serve the industrial sector considerably, particularly enterprises with production lines and manufacturing facilities. These electrical components are not only necessary for day-to-day operations, but they also enable automation, which can help organizations save money and eliminate human error. PCBs can be built specifically to handle high-power applications and the harsh environments that the industrial sector requires.

Printed circuit boards and electronics play an important role in the medical industry. They're employed not only in appliances, but also in monitoring, diagnostic, and therapy equipment. The use of PCBs in the medical field is rapidly growing as technology progresses, opening up new possibilities. In scanning equipment - X-Ray screens, ultrasonic scans, and CT scanners, and some of the other scanners all use electronic components.

Various cutting-edge vehicles have a variety of innovative electronics and electrical equipment that provide more usefulness in the current automobile sector. Circuit boards have gone a long way from the days when automobiles just had a few electronic circuits for the fundamentals, and they have various applications in this industry. For instance, vehicles are increasingly incorporating navigation technologies such as satellite navigation. PCBs are used in all of these systems. Circuit boards are used to monitor and regulate advanced car control systems such as power supply, fuel regulators, and engine management.

Printed Circuit Boards (PCBs) Market Segmentation Analysis

Based on the type, the printed circuit boards (PCBs) market is segmented into single sided, double sided, multi-layer, and HDI. Double-sided printed circuit boards (PCBs) are widely utilized in everyday electronics and various applications. Double-sided PCBs have a conducting layer on either side, whereas single-sided PCBs only have one. On both sides, a dielectric layer is surrounded by circuit copper layers and a solder mask.

Double-sided PCBs are used by manufacturers for goods that require a beginner to advanced degree of circuit complexity. This type of PCB lacks the circuit intricacy and density of multilayer PCBs, but it serves as a cost-effective alternative in a variety of applications. ATS, Ibiden, Nippon Mektron, Sumitomo Electric, Shinko Electric, and Unimicron among others are leading vendors in the double sided PCB market. Multi-Layer PCB is expected to increase at the fastest pace of 6.1 % CAGR from 2026 to 2032, owing to developments in electromagnetic shielding and electronic design automation. PCBs are commonly utilized in automotive applications such as vehicle infotainment and audio systems, and they come in a variety of price points and uses.

The market for double-sided printed circuit boards is expected to increase fast in the Asia Pacific area. Latin America, on the other hand, is expected to grow at a moderate rate in the upcoming years. On the contrary, growth in the Middle East and Africa (MEA) is expected to be slower.

Printed Circuit Boards (PCBs) Market Regional Insights:

The Asia Pacific and North American markets dominated the global printed circuit boards (PCBs) market with a fragmented supply base. With the restoration of economic activity, demand for PCB fabrication is expected to increase. It is expected to be bolstered by the simplicity with which supply chain difficulties may be resolved. Consumer and communication industries are expected to be important sources of demand. On the other hand, the amount of electronics in vehicle and medical equipment manufacturing costs is steadily increasing, resulting in increased demand for PCB.

Asia Pacific market expected to grow at a CAGR of xx% during the forecast period, owing to the presence of various semi-conductor manufacturers and the rising adoption of smart devices. The demand for PCBs in India has steadily increased in recent years as a result of increased investment in digitization and favorable government initiatives. The Indian PCB industry is predicted to grow rapidly over the next five years. The Indian government is heavily supporting the production and use of printed circuit boards in the country including "Make in India" and "Digital India" projects.

By easing the tax regime and lowering bureaucratic barriers, the government hopes to encourage manufacturers to set up more local plants in the country. This is predicted to result in considerable progress in a variety of end-use industries (automotive, electrical, and so on), boosting overall PCB demand.

The automotive sector, aircraft for safe navigation and precise surveillance, and the medical sector for novel medical technology, diagnostics, and devices are among PCB's high-demand sectors in North America. Furthermore, rising sales of electric vehicles, as well as the implementation of innovative driver assistance system technology in them, are expected to boost the PCB market demand.

Printed Circuit Boards (PCBs) Market Recent Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 03 February 2026 | AT&S | AT&S reported a 10% revenue increase to €1.3 billion for the first three quarters of 2025/26, driven by new production capacities at its Kulim and Leoben facilities. | The expansion successfully scales IC substrate and high-end PCB production to meet surging demand for Generative AI and high-performance computing applications. |

| 01 February 2026 | AT&S | The company restructured its Management Board, appointing Gerrit Steen as CFO and reducing the board to three members to streamline strategic execution. | This reorganization focuses on cost optimization and efficiency, aiming for an additional €160 million in sustainable cost reductions through the 2026 fiscal year. |

| 06 January 2026 | Jabil Inc. | Jabil completed the acquisition of Hanley Energy Group, a provider of energy management and critical power systems for data center infrastructure. | The acquisition integrates specialized power electronics and PCB assembly capabilities, positioning Jabil as a primary hardware partner for AI hyperscale data centers. |

| 01 January 2026 | Shenzhen Kinwong Electronic | Shenzhen Kinwong Electronic submitted its preliminary prospectus to the Hong Kong Stock Exchange for a "A+H" dual-primary listing. | The listing aims to fund the expansion of high-end PCB capacity, targeting the 45.7% revenue share currently driven by its automotive electronics segment. |

| 22 December 2025 | Jabil Inc. | Jabil entered a multi-year manufacturing partnership with a global automotive OEM to support PCB assembly for EV power electronics and battery management. | This partnership underscores the industry shift toward vehicle digitalization, where electric vehicles require 3-5 times more PCBs than conventional internal combustion engines. |

| 04 November 2025 | TTM Technologies | TTM Technologies reported a 19% year-on-year increase in net sales to $774.3 million, fueled by Data Center Computing and Networking demand. | The strong financial performance reflects the strategic pivot toward high-complexity interconnects and an Aerospace & Defense backlog reaching a record $1.6 billion. |

The objective of the report is to present a comprehensive analysis of the Global Printed Circuit Boards (PCBs) Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analysed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Global Printed Circuit Boards (PCBs) Market dynamics, structure by analyzing the market segments and project the global Printed Circuit Boards (PCBs) market size. Clear representation of competitive analysis of key players By Type, price, financial position, product portfolio, growth strategies, and regional presence in the Global Printed Circuit Boards (PCBs) Market make the report investor’s guide.

Printed Circuit Boards (PCBs) Market Scope: Inquire before buying

| Printed Circuit Boards (PCBs) Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 80.15 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.23% | Market Size in 2032: | 114.52 USD Billion |

| Segments Covered: | by Type | Single Sided Circuits Double Sided Circuits Multilayer Circuits Rigid-Flex Circuits Others |

|

| by Material | Polyimide (PI) Polyester (PET) Polyethylene Naphthalate (PEN) Others |

||

| by Component | Conductors Dielectric Materials Adhesives Others |

||

| by Process | Semi-Additive Process Full Additive Process Etch Back Process Others |

||

| by End-User | Industrial Electronics Medical & Instrumentation Computer & Data Storage Aerospace & Defense IT & Telecom Automotive Consumer Electronics Others |

||

| by Distribution Channel | Direct Sales Distributors & Resellers Online Platforms Others |

||

Printed Circuit Boards (PCBs) Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Printed Circuit Boards (PCBs) Market, Key Players:

- NOK CORPORATION

- Zhen Ding Technology Holding Limited (ZDT)

- Sumitomo Electric Industries, Ltd.

- Fujikura Ltd.

- Flexium Interconnect, Inc.

- Multi-Fineline Electronix, Inc. (MFLEX)

- Career Technology (Mfg.) Co., Ltd.

- Interflex Co., Ltd.

- Nitto Denko Corporation

- Daeduck Electronics Co., Ltd

- AT&S (Austria Technologie & Systemtechnik AG)

- TTM Technologies, Inc.

- Suzhou Dongshan Precision Manufacturing Co., Ltd. (DSBJ)

- BHflex Co., Ltd.

- ICHIA Technologies Inc.

- NewFlex Technology Co., Ltd.

- Tripod Technology Corporation

- Unimicron Technology Corporation

- Oki Electric Cable Co., Ltd.

- Shenzhen Kinwong Electronic Co., Ltd.

- Shenzhen FastPrint Circuit Tech Co., Ltd.

- Suntak Technology Co., Ltd.

- Young Poong Electronics Co., Ltd.

- Sunflex Tech Co., Ltd.

- Cirexx International, Inc.

- MFS Technology

- Compeq Manufacturing Co., Ltd.

- Sierra Circuits, Inc.

- Jabil Inc.

- Rigao Electronics

- A-TECH Circuits

- LEDYi Lighting

- KingSong Technology

- ZAPON Technology

- Elecrow

Others