Pre-Insulated Pipes Market Size by End-use Industry, Installation, Type, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2029

Overview

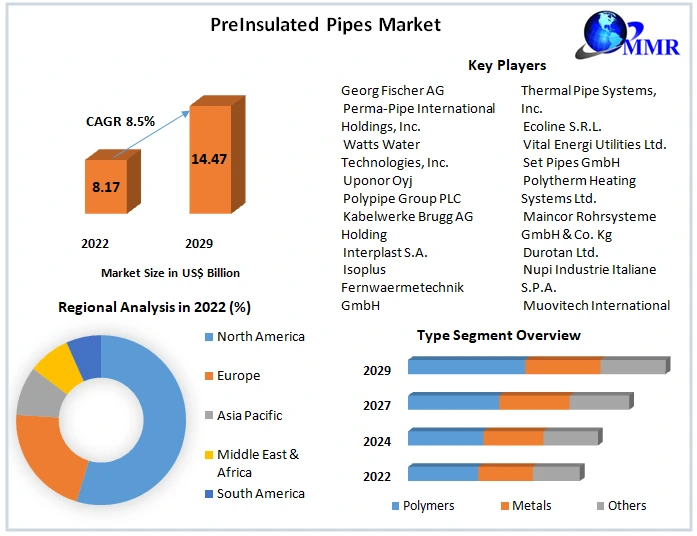

PreInsulated Pipes Market size is expected to reach 14.47 US$ Bn in year 2029, at a CAGR of 8.50% during the forecast period.

The report includes the analysis of impact of COVID-19 lock-down on the revenue of market leaders, followers, and disrupters. Since lock down was implemented differently in different regions and countries, impact of same is also different by regions and segments. The report has covered the current short term and long term impact on the market, same will help decision makers to prepare the outline for short term and long term strategies for companies by region.  To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

The pre-insulated pipes market is expected to grow at CAGR of 8.5 % in the forecast period thanks to driving factors such as increasing awareness regarding environment and government initiatives coupled with growth in district heating & cooling end-use industry. Additionally, the penetration of the product in niche applications further boosts the growth of the pre-insulated pipes market. Instead, untapped markets & emerging economies offer significant growth opportunity for the key players operating in the pre-insulated pipes market during the forecast period. The popularity of district heating and cooling systems is growing owing to its numerous advantages over individual heating and cooling of buildings.

However, volatility in raw material prices, hazards associated with manufacturing polyurethane insulation material for pre-insulated pipes, and long pre- and post-manufacturing certification process may hinder the growth of the pre-insulated pipes industry over the forecast period.

The report provides detailed, region-wise segmentation of the global pre-insulated pipes market and categorizes it at various levels, thereby providing valuable insights at micro and macro levels.

Based on the installation, below ground pre-insulated pipes segment is expected to grow during the forecast period. Below ground systems are also known as buried/ underground installations which are the most extensively used globally. Long straight below ground installations are preferred as they reduce the requirement for joints, fittings, & welding.

The European region is expected to register the highest incremental growth because of the increase in awareness and demand for energy-efficient buildings, stringent government regulations, and the growing demand for DHC in the region. District heating is used in commercial, industrial, and residential applications for space heating and domestic hot water supply. The growing replacement of old district heating systems is expected to drive the market during the forecast period.

A recent development in the Global Pre-Insulated Pipes Market: In September 2018, Perma-Pipe Saudi Arabia LLC, a subsidiary of Perma-Pipe International Holdings Inc., received a contract worth USD 15 Mn from Saipem (Italy). The contract includes provision of the Xtru-Therm insulation system, field joints, and a leak detection system for 2 55 km, 30-inch diameter fuel oil lines for the Kuwait Oil Company. This development determines to transport low sulfur fuel oil for Kuwait Oil Company's new refinery project in Kuwait.

The objective of the report is to present a comprehensive assessment of the market and contains thoughtful insights, facts, historical data, industry-validated market data and projections with a suitable set of assumptions and methodology. The report also helps in understanding Global Pre-Insulated Pipes Market dynamics, structure by identifying and analyzing the market segments and project the global market size. Further, the report also focuses on the competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence. The report also provides PEST analysis, PORTER’s analysis, and SWOT analysis to address the question of shareholders to prioritizing the efforts and investment in the near future to the emerging segment in Global Pre-Insulated Pipes Market.

Pre-Insulated Pipes Market Scope: Inquire before buying

| Global Pre-Insulated Pipes Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 8.17 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 8.5% | Market Size in 2029: | US $ 14.47 Bn. |

| Segments Covered: | by End-use Industry | District Heating & Cooling Oil & Gas Infrastructure & Utility Others Food Processing Pharmaceuticals Wineries Chemicals Water Treatment |

|

| by Installation | Below Ground Above Ground |

||

| by Type | Polymers Metals Others |

||

Pre-Insulated Pipes Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Pre-Insulated Pipes Market Key Players

1. Georg Fischer AG

2. Perma-Pipe International Holdings, Inc.

3. Watts Water Technologies, Inc.

4. Uponor Oyj

5. Polypipe Group PLC

6. Kabelwerke Brugg AG Holding

7. Interplast S.A.

8. Isoplus Fernwaermetechnik GmbH

9. Pem Korea Co., Ltd.

10.Thermaflex International

11.Zeco Aircon Ltd.

12.Logstor A/S

13.Aquatherm GmbH

14.Ke KELIT Kunststoffwerk Gesellschaft M.B.H.

15.KC Polymers Pvt. Ltd.

16.Thermal Pipe Systems, Inc.

17.Ecoline S.R.L.

18.Vital Energi Utilities Ltd.

19.Set Pipes GmbH

20.Polytherm Heating Systems Ltd.

21.Maincor Rohrsysteme GmbH & Co. Kg

22.Durotan Ltd.

23.Nupi Industrie Italiane S.P.A.

24.Muovitech International Group

25.Tece GmbH

26.Rovanco Piping Systems, Inc.

27.Rehau Unlimited Polymer Solutions

28.Brunata Ltd.

29.Thermacor Process Inc.

30.Simona AG

31.Geberit AG

Frequently Asked Questions:

1. Which region has the largest share in Global Pre-Insulated Pipes Market?

Ans: Europe region held the highest share in 2022.

2. What is the growth rate of Global Pre-Insulated Pipes Market?

Ans: The Global Pre-Insulated Pipes Market is growing at a CAGR of 8.5% during forecasting period 2023-2029.

3. What is scope of the Global Pre-Insulated Pipes market report?

Ans: Global Pre-Insulated Pipes Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Pre-Insulated Pipes market?

Ans: The important key players in the Global Pre-Insulated Pipes Market are – Georg Fischer AG, Perma-Pipe International Holdings, Inc., Watts Water Technologies, Inc., Uponor Oyj, Polypipe Group PLC, Kabelwerke Brugg AG Holding, Interplast S.A., Isoplus Fernwaermetechnik GmbH, Pem Korea Co., Ltd., Thermaflex International, Zeco Aircon Ltd., Logstor A/S, Aquatherm GmbH, and Ke KELIT Kunststoffwerk Gesellschaft M.B.H.

5. What is the study period of this market?

Ans: The Global Pre-Insulated Pipes Market is studied from 2022 to 2029.