Personal Cloud Market by Type, Hosted Type, Revenues, User Type, Vertical and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

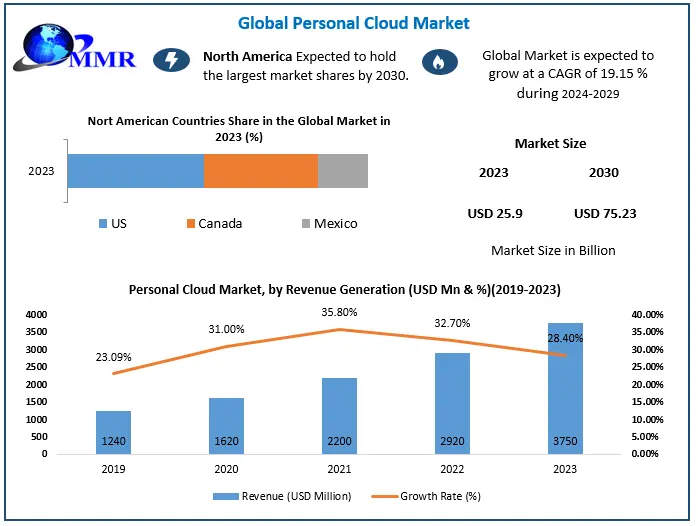

The Personal Cloud Market size was valued at USD 25.9 Billion in 2023 and the total Personal Cloud revenue is expected to grow at a CAGR of 19.15 % from 2024 to 2030, reaching nearly USD 75.23 Billion by 2030.

Personal Cloud Market Overview:

The Personal Cloud Market encompasses a dynamic industry focused on providing cloud-based solutions tailored for individual users to manage and store their digital content securely. Personal Cloud market segment emerged in response to the increasing need for individuals to seamlessly access, synchronize, and store personal data across multiple devices, fostering convenience and flexibility in the digital era. Central to the Personal Cloud Market is the provision of data storage solutions that allow users to store, organize, and access their digital content, including files, photos, videos, and documents, from anywhere with an internet connection. Personal cloud services enable synchronization across various devices, ensuring that changes made on one device are reflected on others in real-time. This feature contributes to a cohesive and integrated user experience.

Security is a paramount concern in the Personal Cloud Market. Leading providers implement robust security measures, including encryption, multi-factor authentication, and advanced data protection, to ensure the confidentiality and integrity of user data. The market emphasizes user-friendly interfaces, offering intuitive platforms that allow individuals to easily manage and customize their personal cloud environments according to their preferences. The detailed and constructive formation of key drivers, opportunities, and unique segmentation outputs structural and optimistic data. Validated using primary as well as secondary research methodology and scope of the Global Personal Cloud Market. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Personal Cloud Market Dynamics

Data Accessibility and Synchronization with Growing Adoption of Smart Devices Driving the Personal Cloud Market

The demand for personal cloud services is propelled by the fundamental need for seamless data accessibility and synchronization across multiple devices. Users increasingly desire the ability to access their files, photos, and documents from any location, fostering a widespread adoption of personal cloud solutions. This driver is rooted in the convenience and flexibility that users seek in managing their digital content. The growth of the Personal Cloud Market is closely tied to the increasing need for efficient data management and accessibility. The proliferation of smart devices, including smartphones, tablets, and smart TVs, plays a pivotal role in the increased demand for personal cloud services.

Users seek a unified platform that enables them to store and access their digital content seamlessly from various devices. The growing prevalence of smart devices enhances the importance of personal cloud solutions in providing a cohesive and integrated user experience. The potential of the Personal Cloud Market is closely tied to the enlarging ecosystem of smart devices.

With a heightened awareness of data security and privacy, individuals are turning to personal cloud solutions as a secure means to store and manage their data. Personal clouds are equipped with robust security features, including encryption and multi-factor authentication, addressing users' concerns and contributing to the growing adoption of these services as a trustworthy solution for safeguarding sensitive information. Security considerations play a crucial role in shaping the potential and penetration of the Personal Cloud Market. The rise of remote work and the increasing need for collaboration from different locations are significant drivers for personal cloud services.

Individuals and professionals are actively seeking efficient ways to share and collaborate on documents and projects through cloud-based platforms. The ability to access, edit, and share files in real-time from diverse locations enhances the appeal and utility of personal cloud solutions. The Personal Cloud Market's potential is influenced by the evolving trends in remote work and collaboration.

The development of high-speed internet connectivity globally is a key contributor to the popularity of personal cloud services. Faster internet speeds not only improve the overall user experience but also enable quick and reliable access to personal data stored in the cloud. This driver emphasizes the importance of internet infrastructure in supporting the widespread adoption of personal cloud solutions. The growth of the Personal Cloud Market is intricately linked to the global expansion of high-speed internet access.

Concerns about Data Privacy and Limited Storage Capacity with Reliability and Downtime Restraining the Personal Cloud Market Growth

Despite the implementation of security measures, concerns about data privacy persist among users. The fear of unauthorized access or data breaches can act as a restraint, preventing some individuals from fully embracing personal cloud services. Addressing and mitigating these concerns is essential to fostering broader adoption. Concerns about data privacy can impact the growth and share of the Personal Cloud Market. Many personal cloud services offer limited free storage, and increasing storage often comes with additional costs. The restriction on storage capacity may discourage users with extensive data storage needs, leading to a potential limitation in the scalability and attractiveness of personal cloud solutions.

Storage capacity considerations are crucial in pricing analysis and can influence the competitiveness of the Personal Cloud Market. Users rely on personal cloud services for continuous access to their data. Downtime or service interruptions can have a significant impact on user trust and satisfaction. Reliability is, therefore, a crucial factor in the adoption and retention of personal cloud solutions, and providers must ensure consistent and uninterrupted service. The fluctuation in reliability and downtime can influence the perception of the Personal Cloud Market among users.

Integrating personal cloud services with other applications and platforms can pose a challenge. The lack of seamless integration with commonly used software and services may hinder the overall user experience, requiring solutions that offer easy interoperability to enhance user convenience. Integration challenges can impact the market share and innovation in the Personal Cloud Market. Personal cloud services heavily depend on internet connectivity. In regions with poor or unreliable internet infrastructure, users may face difficulties accessing their data, limiting the practicality of personal cloud solutions. This dependency underscores the importance of addressing connectivity challenges to broaden the accessibility of personal cloud services.

Internet connectivity is a key factor influencing the penetration and potential of the Personal Cloud Market. The competitive landscape in the personal cloud market may lead to vendor lock-in issues. Users heavily invested in one provider's ecosystem may find it challenging to switch to another provider due to compatibility and migration challenges. This potential lock-in effect raises considerations regarding user flexibility and choice in the personal cloud market. Competitive landscape dynamics and vendor lock-in considerations are essential aspects in the pricing analysis and opportunity assessment for the Personal Cloud Market.

Personal Cloud Market Segment Analysis

Type:

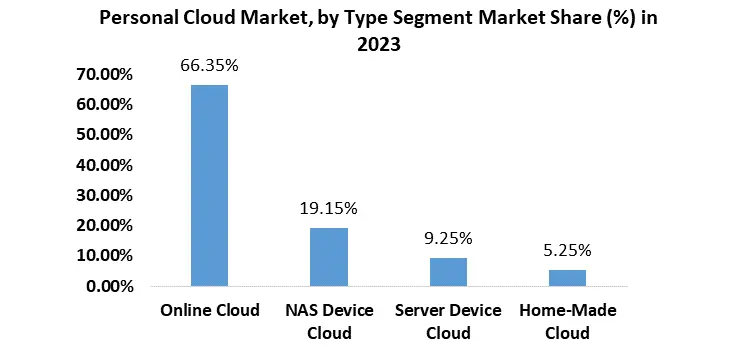

The Online Cloud segment stands out as a dominant force, wielding significant influence and leading the Personal Cloud Market. Users gravitate towards internet-based platforms, attracted by the accessibility, synchronization, and storage capabilities offered by this major market force. The Online Cloud segment is currently undergoing a boom, reflecting the escalating preference among users for cloud-based solutions. This surge underscores the increasing reliance on online platforms for personal data management. The NAS Device Cloud solutions carve a substantial niche, catering to users who opt for network-attached storage devices to fulfil their personal cloud needs. This major segment caters to those seeking localized storage solutions. The Server Device Cloud solutions stand as a dominant force, providing users with personal cloud capabilities hosted on dedicated servers. This segment's dominance highlights the importance of dedicated server infrastructure in the personal cloud landscape.

The Home-Made Cloud segment is in an emerging phase, as users explore personalized solutions for creating and managing their personal cloud environments. This segment reflects the increasing desire for customized and user-controlled cloud setups.

Hosted Type:

Hosted Type:

Personal clouds hosted from providers' premises secure a substantial personal cloud market share, offering users the convenience and professionalism associated with outsourced management of their cloud services. Hosting personal clouds from users' premises is a growing segment, mirroring a trend where individuals and enterprises prefer increased control over their personal cloud solutions. This segment reflects a desire for localized management and oversight.

Vertical:

The BFSI sector critically adopts personal cloud solutions for secure data management, accessibility, and compliance with regulatory standards. The critical adoption reflects the sector's emphasis on data security and compliance. The IT & ITeS sector pioneers the adoption of personal cloud services, leveraging these solutions for collaborative work environments and efficient data handling. The sector's reliance on cutting-edge technologies contributes to its pioneering role in the personal cloud market. Telecommunications strategically integrates personal cloud solutions to offer enhanced services, including data storage, backup, and accessibility. This integration reflects the sector's recognition of personal clouds as an integral part of their service offerings.

Retail & e-Commerce experience a growing demand for personal cloud services, supporting online businesses with secure data management. The demand underscores the role of personal clouds in facilitating efficient online retail operations in the personal cloud market. Media & Entertainment extensively uses personal cloud services for collaborative content creation, storage, and distribution. The extensive usage reflects the role of personal clouds in facilitating collaborative and distributed content creation.

The government and public sector prioritize personal cloud services with a strong emphasis on data security, accessibility, and collaborative governance. The personal cloud market sector's focus on security aligns with the sensitive nature of government data. Manufacturing sectors adopt personal cloud solutions to enhance operational efficiency, data collaboration, and remote access. The adoption reflects a strategic move towards digitization and enhanced efficiency in manufacturing processes. Energy & Utilities sectors leverage personal cloud services for managing critical infrastructure data, fostering efficiency and reliability.

The critical infrastructure management highlights the importance of personal clouds in ensuring reliability in the energy and utilities sector. Healthcare & Life Sciences benefit from precision data management in personal clouds, supporting research, patient care, and compliance. The precision data management addresses the sector's need for secure and accurate data handling. Other verticals, including education, logistics, and non-profit organizations, adopt personal cloud services for diverse applications depending on their specific needs. The diverse applications signify the adaptability of personal clouds across various industries and sectors.

Personal Cloud Market Regional Analysis

North America asserts its dominance in the Personal Cloud Market as a powerhouse with high internet penetration rates and a tech-savvy population. The region's advanced IT infrastructure and widespread adoption of cloud-based solutions contribute significantly to the prevalence of personal cloud services. Boasting booming adoption, North America is a key driver in the growth of personal cloud services. This surge is propelled by the escalating demand for seamless data accessibility, heightened awareness of data security, and the presence of a robust ecosystem of smart devices. The region is a focal point for personal cloud providers aiming to meet the evolving needs of users. With a substantial user base, North America accommodates individual users, small enterprises, and large corporations leveraging personal cloud services for data management, collaboration, and remote access.

The mature market in this region reflects a high level of awareness and widespread acceptance of personal cloud solutions. The Personal Cloud Market experiences significant regional growth in the US, driven by a tech-savvy population and robust internet infrastructure. The US serves as a key contributor to the overall market development, with users demanding advanced personal cloud solutions. The market share of personal cloud services is well-distributed across the US, Canada, and Mexico. Each country contributes to the overall regional market share, with users in these countries embracing personal cloud solutions for diverse applications.

Asia Pacific witnesses rapid growth in the Personal Cloud Market, driven by factors such as an increasing middle-class population, increased smartphone adoption, and a surge in internet connectivity. Emerging economies in the region significantly contribute to this growth, with a rising number of individuals and businesses adopting personal cloud solutions. Emerging trends in Asia Pacific, such as home-made cloud setups and a preference for hosting personal clouds from users' premises, align with the region's diverse technological landscape. Users in Asia Pacific exhibit a preference for customized and localized solutions for their personal data management needs.

Catering to diverse applications across verticals including retail, telecommunications, and manufacturing, the Personal Cloud Market in Asia Pacific thrives on the region's varied economic landscape and unique user behaviours. The demand for personal cloud services in the region is characterized by its diversity and continual evolution. China and South Korea contribute significantly to the personal cloud market share in Asia Pacific. These countries exhibit unique user behaviours and preferences, shaping the overall landscape of personal cloud adoption in the region.

Europe showcases a tech-driven adoption of personal cloud services, emphasizing data privacy and security. Stringent data protection regulations, such as GDPR, contribute to heightened user awareness, fostering the adoption of secure and compliant personal cloud solutions in the region. European businesses strategically integrate personal cloud services to enhance operational efficiency, collaboration, and data accessibility. The region's focus on technological innovation and digital transformation drives the seamless integration of personal clouds into various industry sectors. The Personal Cloud Market in Europe experiences a growing market share, reflecting a maturing market with an increasing number of users recognizing the benefits of cloud-based data management.

Stable economic conditions in the region contribute to the sustained growth of personal cloud services. Germany and France play pivotal roles in shaping the personal cloud market share in Europe. These countries exhibit strong technological infrastructures and high levels of user awareness, contributing significantly to the regional market dynamics.

The Personal Cloud Market in the Middle East and Africa is witnessing increasing penetration, driven by rising internet connectivity and a growing awareness of digital solutions. Governments and businesses in the region are actively investing in digital infrastructure, creating an environment conducive to the adoption of personal cloud services. Security considerations play a pivotal role in MEA's adoption of personal cloud services. Users in the region prioritize secure data management solutions, leading to the traction of personal clouds with robust security features in the market. MEA experiences industry-specific adoption of personal cloud services, with sectors such as telecommunications, government, and healthcare leveraging these solutions for sector-specific needs. The unique challenges and opportunities in MEA contribute to a diverse landscape of personal cloud applications. Brazil contributes significantly to the personal cloud market share in MEA, reflecting a growing demand for digital solutions and data management services in the region.

Personal Cloud Market Competitive Landscape

In June 2021, Wisekey International Holding SA, a leading player in the cybersecurity and IoT sector, introduced a noteworthy addition to its suite of services the WISeID Cloud Storage, enhancing the WISeID platform dedicated to digital identity and cybersecurity solutions. The WISeID Cloud Storage empowers users to safeguard their files by storing them in the cloud, utilizing servers fortified by Swiss technologies from WISeKey. This development marks a strategic move within the Personal Cloud Market, providing users with secure and accessible storage solutions.

In September 2021, Microsoft and global travel technology company OYO unveiled a comprehensive, multi-year strategic alliance to collaboratively develop cutting-edge travel and hospitality products and technologies. Microsoft Azure plays a pivotal role as a key enabler, driving innovations in the cloud and reshaping the landscape of the hospitality and travel tech industries. This collaboration reflects the synergies in the development of advanced solutions within the Personal Cloud Market, emphasizing the role of cloud-based technologies in shaping the future of travel and hospitality.

In July 2023, Microsoft introduced Dynamics 365 Copilot, heralded as the world's first AI copilot seamlessly integrated into cloud-based CRM and ERP applications. This innovative solution is designed to enhance processes, deliver valuable insights, guide optimal decision-making, and streamline administrative tasks. Microsoft's unveiling of Dynamics 365 Copilot underscores the continuous evolution and advancements within the Personal Cloud Market, where AI integration becomes a key driver for enhanced business functionalities.

In October 2022, Seagate Technology announced a significant enhancement for Lyve Mobile customers—a new data transfer feature named cloud import. This feature enables users to expedite large-scale data transfers from edge or core locations to various cloud destinations such as Amazon S3, Google Cloud Platform, Microsoft Azure, and Lyve Cloud. The introduction of cloud import responds to the growing demand for secure, quick, and efficient data transfer mechanisms within the Personal Cloud Market, catering to diverse cloud service preferences.

In December 2022, Apple reaffirmed its commitment to providing robust options for data protection by unveiling three cutting-edge security capabilities. These capabilities are designed to thwart threats to user data in the cloud. Noteworthy features include iMessage Contact Key Verification, allowing users to confirm secure communication; Security Keys for Apple ID, providing an additional layer of security and Advanced Data Protection for iCloud, offering end-to-end encryption for critical iCloud data. Apple's continuous efforts underscore the commitment to delivering the highest level of cloud data protection within the Personal Cloud Market.

Global Personal Cloud Market Scope: Inquire before buying

| Global Personal Cloud Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 25.9 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 19.15% | Market Size in 2030: | US $ 75.23 Bn. |

| Segments Covered: | By Type | Online Cloud NAS Device Cloud Server Device Cloud Home-Made Cloud |

|

| By Hosted Type | Hosted From Providers Premises Hosted from Users Premises |

||

| By Revenues | Direct Revenues Indirect Revenues |

||

| By User Type | Indivisual Small Enterprises Medium Enterprises |

||

| By Vertical | BFSI IT & ITeS Telecommunications Retail & e-Commerce Government & Public Sector Manufacturing Energy & Utilities Healthcare & Life Sciences Media & Entertainment Other Verticals |

||

Global Personal Cloud Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Personal Cloud Market Key Players:

Major Global Key Players:

1. Amazon Web Services, Inc. (U.S.)

2. Microsoft (U.S.)

3. Oracle (U.S.)

4. Google L.L.C. (U.S.)

5. Palo Alto Networks. (U.S.)

6. IBM Corporation (U.S.)

Leading Key Players in North America:

1. Zscaler, Inc. (U.S.)

2. Cisco Systems, Inc. (U.S.)

3. Cloud flare Inc., (U.S.)

4. Workday, Inc. (U.S.)

5. PTC (U.S.)

6. AWS (U.S.)

7. Check Point Software Technologies Ltd. (U.S.)

8. Broadcom. (U.S.)

9. Qualys,Inc. (U.S.)

10. Apple (US)

11. Dropbox (US)

12. Box (US)

13. Seagate Technology (US)

14. Western Digital (US)

15. Synchronoss (US)

16. Egnyte (US)

17. Funambol (US)

18. SugarSync (US)

19. ElephantDrive (US)

20. Cloudike (US)

21. SpiderOak (US)

Market Follower key Players in Europe:

1. SAP SE (Germany)

2. Siemens (Germany)

3. Sophos Ltd. (U.K.)

4. Foreseeti (Sweden)

Prominent Key player Asia Pacific:

1. Fujitsu (Japan)

2. Trend Micro Incorporated. (Japan)

3. BUFFALO Technology (Japan)

4. ASUS Cloud (Taiwan)

FAQ’s:

1. What is the Personal Cloud Market?

Ans: The Personal Cloud Market refers to the industry that provides cloud-based storage and computing services tailored for individual users, offering a secure and accessible platform for personal data storage and management.

2. What are the key drivers of the Personal Cloud Market?

Ans: Key drivers include the demand for seamless data accessibility, growing adoption of smart devices, rising concerns about data security, remote work trends, and increased internet penetration.

3. What types of personal cloud services are available?

Ans: Personal cloud services include Online Cloud, NAS Device Cloud, Server Device Cloud, and Home-Made Cloud, catering to diverse user preferences.

4. How are personal clouds hosted?

Ans: Personal clouds can be hosted either from providers' premises or from users' premises, offering flexibility in management and control.

5. What are the revenue models in the Personal Cloud Market?

Ans: The market relies on both Direct Revenues (subscription fees, premium features) and Indirect Revenues (partnerships, advertising) to sustain growth and innovation.