Global Personal and Entry Level Storage (PELS) Market

1. Preface

1.1. Report Scope and Market Segmentation

1.2. Research Highlights

1.3. Research Objectives

2. Assumptions and Research Methodology

2.1. Report Assumptions

2.2. Abbreviations

2.3. Research Methodology

2.3.1. Secondary Research

2.3.1.1. Secondary data

2.3.1.2. Secondary Sources

2.3.2. Primary Research

2.3.2.1. Data from Primary Sources

2.3.2.2. Breakdown of Primary Sources

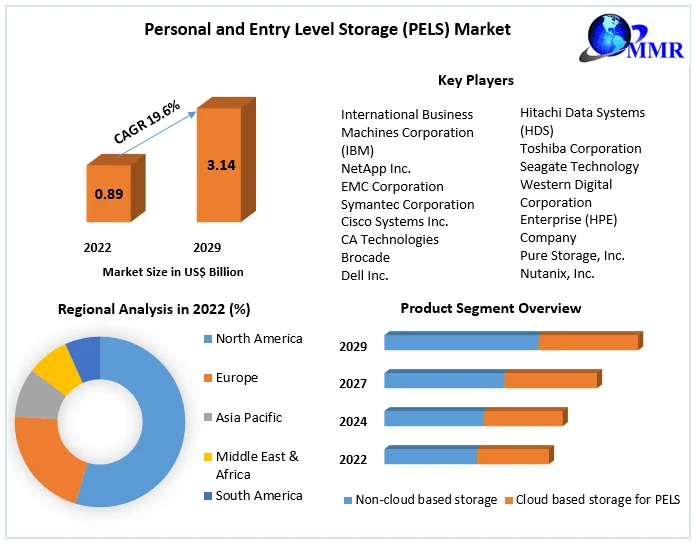

3. Executive Summary: Global Personal and Entry Level Storage (PELS) Market Size, by Market Value (US$ Bn)

4. Market Overview

4.1. Introduction

4.2. Market Indicator

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.2.4. Challenges

4.3. Porter’s Analysis

4.4. Value Chain Analysis

4.5. Market Risk Analysis

4.6. SWOT Analysis

4.7. Industry Trends and Emerging Technologies

5. Supply Side and Demand Side Indicators

6. Global Personal and Entry Level Storage (PELS) Market Analysis and Forecast

6.1. Global Personal and Entry Level Storage (PELS) Market Size & Y-o-Y Growth Analysis

6.1.1. North America

6.1.2. Europe

6.1.3. Asia Pacific

6.1.4. Middle East & Africa

6.1.5. South America

7. Global Personal and Entry Level Storage (PELS) Market Analysis and Forecast, by Product

7.1. Introduction and Definition

7.2. Key Findings

7.3. Global Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Product

7.4. Global Personal and Entry Level Storage (PELS) Market Size (US$ Bn) Forecast, by Product

7.5. Global Personal and Entry Level Storage (PELS) Market Analysis, by Product

7.6. Global Personal and Entry Level Storage (PELS) Market Attractiveness Analysis, by Product

8. Global Personal and Entry Level Storage (PELS) Market Analysis and Forecast, by Technology

8.1. Introduction and Definition

8.2. Key Findings

8.3. Global Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Technology

8.4. Global Personal and Entry Level Storage (PELS) Market Size (US$ Bn) Forecast, by Technology

8.5. Global Personal and Entry Level Storage (PELS) Market Analysis, by Technology

8.6. Global Personal and Entry Level Storage (PELS) Market Attractiveness Analysis, by Technology

9. Global Personal and Entry Level Storage (PELS) Market Analysis and Forecast, by End-Use Industry

9.1. Introduction and Definition

9.2. Key Findings

9.3. Global Personal and Entry Level Storage (PELS) Market Value Share Analysis, by End-Use Industry

9.4. Global Personal and Entry Level Storage (PELS) Market Size (US$ Bn) Forecast, by End-Use Industry

9.5. Global Personal and Entry Level Storage (PELS) Market Analysis, by End-Use Industry

9.6. Global Personal and Entry Level Storage (PELS) Market Attractiveness Analysis, by End-Use Industry

10. Global Personal and Entry Level Storage (PELS) Market Analysis, by Region

10.1. Global Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Region

10.2. Global Personal and Entry Level Storage (PELS) Market Size (US$ Bn) Forecast, by Region

10.3. Global Personal and Entry Level Storage (PELS) Market Attractiveness Analysis, by Region

11. North America Personal and Entry Level Storage (PELS) Market Analysis

11.1. Key Findings

11.2. North America Personal and Entry Level Storage (PELS) Market Overview

11.3. North America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Product

11.4. North America Personal and Entry Level Storage (PELS) Market Forecast, by Product

11.4.1. Non-cloud based storage

11.4.1.1. Recordable discs for PELS

11.4.1.2. Flash drives for PELS

11.4.1.3. Hard disk drives (HDD) for PELS

11.4.1.4. Solid state drives (SSD) for PELS

11.4.2. Cloud based storage for PELS

11.5. North America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Technology

11.6. North America Personal and Entry Level Storage (PELS) Market Forecast, by Technology

11.6.1. SAS (serial attached SCSI)

11.6.2. DAS (direct attached storage) for PELS

11.6.3. NAS (network attached storage)

11.6.4. Cloud based storage

11.6.5. Others (IP based storage, fibre channel storage)

11.7. North America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by End-Use Industry

11.8. North America Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

11.8.1. Financial services

11.8.2. Media and entertainment

11.8.3. Healthcare and life sciences

11.8.4. Public sector

11.8.5. Others

11.9. North America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Country

11.10. North America Personal and Entry Level Storage (PELS) Market Forecast, by Country

11.10.1. U.S.

11.10.2. Canada

11.11. North America Personal and Entry Level Storage (PELS) Market Analysis, by Country

11.12. U.S. Personal and Entry Level Storage (PELS) Market Forecast, by Product

11.12.1. Non-cloud based storage

11.12.1.1. Recordable discs for PELS

11.12.1.2. Flash drives for PELS

11.12.1.3. Hard disk drives (HDD) for PELS

11.12.1.4. Solid state drives (SSD) for PELS

11.12.2. Cloud based storage for PELS

11.13. U.S. Personal and Entry Level Storage (PELS) Market Forecast, by Technology

11.13.1. SAS (serial attached SCSI)

11.13.2. DAS (direct attached storage) for PELS

11.13.3. NAS (network attached storage)

11.13.4. Cloud based storage

11.13.5. Others (IP based storage, fibre channel storage)

11.14. U.S. Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

11.14.1. Financial services

11.14.2. Media and entertainment

11.14.3. Healthcare and life sciences

11.14.4. Public sector

11.14.5. Others

11.15. Canada Personal and Entry Level Storage (PELS) Market Forecast, by Product

11.15.1. Non-cloud based storage

11.15.1.1. Recordable discs for PELS

11.15.1.2. Flash drives for PELS

11.15.1.3. Hard disk drives (HDD) for PELS

11.15.1.4. Solid state drives (SSD) for PELS

11.15.2. Cloud based storage for PELS

11.16. Canada Personal and Entry Level Storage (PELS) Market Forecast, by Technology

11.16.1. SAS (serial attached SCSI)

11.16.2. DAS (direct attached storage) for PELS

11.16.3. NAS (network attached storage)

11.16.4. Cloud based storage

11.16.5. Others (IP based storage, fibre channel storage)

11.17. Canada Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

11.17.1. Financial services

11.17.2. Media and entertainment

11.17.3. Healthcare and life sciences

11.17.4. Public sector

11.17.5. Others

11.18. North America Personal and Entry Level Storage (PELS) Market Attractiveness Analysis

11.18.1. By Product

11.18.2. By Technology

11.18.3. By End-Use Industry

11.19. PEST Analysis

11.20. Key Trends

11.21. Key Developments

12. Europe Personal and Entry Level Storage (PELS) Market Analysis

12.1. Key Findings

12.2. Europe Personal and Entry Level Storage (PELS) Market Overview

12.3. Europe Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Product

12.4. Europe Personal and Entry Level Storage (PELS) Market Forecast, by Product

12.4.1. Non-cloud based storage

12.4.1.1. Recordable discs for PELS

12.4.1.2. Flash drives for PELS

12.4.1.3. Hard disk drives (HDD) for PELS

12.4.1.4. Solid state drives (SSD) for PELS

12.4.2. Cloud based storage for PELS

12.5. Europe Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Technology

12.6. Europe Personal and Entry Level Storage (PELS) Market Forecast, by Technology

12.6.1. SAS (serial attached SCSI)

12.6.2. DAS (direct attached storage) for PELS

12.6.3. NAS (network attached storage)

12.6.4. Cloud based storage

12.6.5. Others (IP based storage, fibre channel storage)

12.7. Europe Personal and Entry Level Storage (PELS) Market Value Share Analysis, by End-Use Industry

12.8. Europe Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

12.8.1. Financial services

12.8.2. Media and entertainment

12.8.3. Healthcare and life sciences

12.8.4. Public sector

12.8.5. Others

12.9. Europe Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Country

12.10. Europe Personal and Entry Level Storage (PELS) Market Forecast, by Country

12.10.1. Germany

12.10.2. U.K.

12.10.3. France

12.10.4. Italy

12.10.5. Spain

12.10.6. Rest of Europe

12.11. Europe Personal and Entry Level Storage (PELS) Market Analysis, by Country

12.12. Germany Personal and Entry Level Storage (PELS) Market Forecast, by Product

12.12.1. Non-cloud based storage

12.12.1.1. Recordable discs for PELS

12.12.1.2. Flash drives for PELS

12.12.1.3. Hard disk drives (HDD) for PELS

12.12.1.4. Solid state drives (SSD) for PELS

12.12.2. Cloud based storage for PELS

12.13. Germany Personal and Entry Level Storage (PELS) Market Forecast, by Technology

12.13.1. SAS (serial attached SCSI)

12.13.2. DAS (direct attached storage) for PELS

12.13.3. NAS (network attached storage)

12.13.4. Cloud based storage

12.13.5. Others (IP based storage, fibre channel storage)

12.14. Germany Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

12.14.1. Financial services

12.14.2. Media and entertainment

12.14.3. Healthcare and life sciences

12.14.4. Public sector

12.14.5. Others

12.15. U.K. Personal and Entry Level Storage (PELS) Market Forecast, by Product

12.15.1. Non-cloud based storage

12.15.1.1. Recordable discs for PELS

12.15.1.2. Flash drives for PELS

12.15.1.3. Hard disk drives (HDD) for PELS

12.15.1.4. Solid state drives (SSD) for PELS

12.15.2. Cloud based storage for PELS

12.16. U.K. Personal and Entry Level Storage (PELS) Market Forecast, by Technology

12.16.1. SAS (serial attached SCSI)

12.16.2. DAS (direct attached storage) for PELS

12.16.3. NAS (network attached storage)

12.16.4. Cloud based storage

12.16.5. Others (IP based storage, fibre channel storage)

12.17. U.K. Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

12.17.1. Financial services

12.17.2. Media and entertainment

12.17.3. Healthcare and life sciences

12.17.4. Public sector

12.17.5. Others

12.18. France Personal and Entry Level Storage (PELS) Market Forecast, by Product

12.18.1. Non-cloud based storage

12.18.1.1. Recordable discs for PELS

12.18.1.2. Flash drives for PELS

12.18.1.3. Hard disk drives (HDD) for PELS

12.18.1.4. Solid state drives (SSD) for PELS

12.18.2. Cloud based storage for PELS

12.19. France Personal and Entry Level Storage (PELS) Market Forecast, by Technology

12.19.1. SAS (serial attached SCSI)

12.19.2. DAS (direct attached storage) for PELS

12.19.3. NAS (network attached storage)

12.19.4. Cloud based storage

12.19.5. Others (IP based storage, fibre channel storage)

12.20. France Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

12.20.1. Financial services

12.20.2. Media and entertainment

12.20.3. Healthcare and life sciences

12.20.4. Public sector

12.20.5. Others

12.21. Italy Personal and Entry Level Storage (PELS) Market Forecast, by Product

12.21.1. Non-cloud based storage

12.21.1.1. Recordable discs for PELS

12.21.1.2. Flash drives for PELS

12.21.1.3. Hard disk drives (HDD) for PELS

12.21.1.4. Solid state drives (SSD) for PELS

12.21.2. Cloud based storage for PELS

12.22. Italy Personal and Entry Level Storage (PELS) Market Forecast, by Technology

12.22.1. SAS (serial attached SCSI)

12.22.2. DAS (direct attached storage) for PELS

12.22.3. NAS (network attached storage)

12.22.4. Cloud based storage

12.22.5. Others (IP based storage, fibre channel storage)

12.23. Italy Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

12.23.1. Financial services

12.23.2. Media and entertainment

12.23.3. Healthcare and life sciences

12.23.4. Public sector

12.23.5. Others

12.24. Spain Personal and Entry Level Storage (PELS) Market Forecast, by Product

12.24.1. Non-cloud based storage

12.24.1.1. Recordable discs for PELS

12.24.1.2. Flash drives for PELS

12.24.1.3. Hard disk drives (HDD) for PELS

12.24.1.4. Solid state drives (SSD) for PELS

12.24.2. Cloud based storage for PELS

12.25. Spain Personal and Entry Level Storage (PELS) Market Forecast, by Technology

12.25.1. SAS (serial attached SCSI)

12.25.2. DAS (direct attached storage) for PELS

12.25.3. NAS (network attached storage)

12.25.4. Cloud based storage

12.25.5. Others (IP based storage, fibre channel storage)

12.26. Spain Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

12.26.1. Financial services

12.26.2. Media and entertainment

12.26.3. Healthcare and life sciences

12.26.4. Public sector

12.26.5. Others

12.27. Rest of Europe Personal and Entry Level Storage (PELS) Market Forecast, by Product

12.27.1. Non-cloud based storage

12.27.1.1. Recordable discs for PELS

12.27.1.2. Flash drives for PELS

12.27.1.3. Hard disk drives (HDD) for PELS

12.27.1.4. Solid state drives (SSD) for PELS

12.27.2. Cloud based storage for PELS

12.28. Rest of Europe Personal and Entry Level Storage (PELS) Market Forecast, by Technology

12.28.1. SAS (serial attached SCSI)

12.28.2. DAS (direct attached storage) for PELS

12.28.3. NAS (network attached storage)

12.28.4. Cloud based storage

12.28.5. Others (IP based storage, fibre channel storage)

12.29. Rest Of Europe Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

12.29.1. Financial services

12.29.2. Media and entertainment

12.29.3. Healthcare and life sciences

12.29.4. Public sector

12.29.5. Others

12.30. Europe Personal and Entry Level Storage (PELS) Market Attractiveness Analysis

12.30.1. By Product

12.30.2. By Technology

12.30.3. By End-Use Industry

12.31. PEST Analysis

12.32. Key Trends

12.33. Key Developments

13. Asia Pacific Personal and Entry Level Storage (PELS) Market Analysis

13.1. Key Findings

13.2. Asia Pacific Personal and Entry Level Storage (PELS) Market Overview

13.3. Asia Pacific Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Product

13.4. Asia Pacific Personal and Entry Level Storage (PELS) Market Forecast, by Product

13.4.1. Non-cloud based storage

13.4.1.1. Recordable discs for PELS

13.4.1.2. Flash drives for PELS

13.4.1.3. Hard disk drives (HDD) for PELS

13.4.1.4. Solid state drives (SSD) for PELS

13.4.2. Cloud based storage for PELS

13.5. Asia Pacific Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Technology

13.6. Asia Pacific Personal and Entry Level Storage (PELS) Market Forecast, by Technology

13.6.1. SAS (serial attached SCSI)

13.6.2. DAS (direct attached storage) for PELS

13.6.3. NAS (network attached storage)

13.6.4. Cloud based storage

13.6.5. Others (IP based storage, fibre channel storage)

13.7. Asia Pacific Personal and Entry Level Storage (PELS) Market Value Share Analysis, by End-Use Industry

13.8. Asia Pacific Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

13.8.1. Financial services

13.8.2. Media and entertainment

13.8.3. Healthcare and life sciences

13.8.4. Public sector

13.8.5. Others

13.9. Asia Pacific Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Country

13.10. Asia Pacific Personal and Entry Level Storage (PELS) Market Forecast, by Country

13.10.1. China

13.10.2. India

13.10.3. Japan

13.10.4. ASEAN

13.10.5. Rest of Asia Pacific

13.11. Asia Pacific Personal and Entry Level Storage (PELS) Market Analysis, by Country

13.12. China Personal and Entry Level Storage (PELS) Market Forecast, by Product

13.12.1. Non-cloud based storage

13.12.1.1. Recordable discs for PELS

13.12.1.2. Flash drives for PELS

13.12.1.3. Hard disk drives (HDD) for PELS

13.12.1.4. Solid state drives (SSD) for PELS

13.12.2. Cloud based storage for PELS

13.13. China Personal and Entry Level Storage (PELS) Market Forecast, by Technology

13.13.1. SAS (serial attached SCSI)

13.13.2. DAS (direct attached storage) for PELS

13.13.3. NAS (network attached storage)

13.13.4. Cloud based storage

13.13.5. Others (IP based storage, fibre channel storage)

13.14. China Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

13.14.1. Financial services

13.14.2. Media and entertainment

13.14.3. Healthcare and life sciences

13.14.4. Public sector

13.14.5. Others

13.15. India Personal and Entry Level Storage (PELS) Market Forecast, by Product

13.15.1. Non-cloud based storage

13.15.1.1. Recordable discs for PELS

13.15.1.2. Flash drives for PELS

13.15.1.3. Hard disk drives (HDD) for PELS

13.15.1.4. Solid state drives (SSD) for PELS

13.15.2. Cloud based storage for PELS

13.16. India Personal and Entry Level Storage (PELS) Market Forecast, by Technology

13.16.1. SAS (serial attached SCSI)

13.16.2. DAS (direct attached storage) for PELS

13.16.3. NAS (network attached storage)

13.16.4. Cloud based storage

13.16.5. Others (IP based storage, fibre channel storage)

13.17. India Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

13.17.1. Financial services

13.17.2. Media and entertainment

13.17.3. Healthcare and life sciences

13.17.4. Public sector

13.17.5. Others

13.18. Japan Personal and Entry Level Storage (PELS) Market Forecast, by Product

13.18.1. Non-cloud based storage

13.18.1.1. Recordable discs for PELS

13.18.1.2. Flash drives for PELS

13.18.1.3. Hard disk drives (HDD) for PELS

13.18.1.4. Solid state drives (SSD) for PELS

13.18.2. Cloud based storage for PELS

13.19. Japan Personal and Entry Level Storage (PELS) Market Forecast, by Technology

13.19.1. SAS (serial attached SCSI)

13.19.2. DAS (direct attached storage) for PELS

13.19.3. NAS (network attached storage)

13.19.4. Cloud based storage

13.19.5. Others (IP based storage, fibre channel storage)

13.20. Japan Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

13.20.1. Financial services

13.20.2. Media and entertainment

13.20.3. Healthcare and life sciences

13.20.4. Public sector

13.20.5. Others

13.21. ASEAN Personal and Entry Level Storage (PELS) Market Forecast, by Product

13.21.1. Non-cloud based storage

13.21.1.1. Recordable discs for PELS

13.21.1.2. Flash drives for PELS

13.21.1.3. Hard disk drives (HDD) for PELS

13.21.1.4. Solid state drives (SSD) for PELS

13.21.2. Cloud based storage for PELS

13.22. ASEAN Personal and Entry Level Storage (PELS) Market Forecast, by Technology

13.22.1. SAS (serial attached SCSI)

13.22.2. DAS (direct attached storage) for PELS

13.22.3. NAS (network attached storage)

13.22.4. Cloud based storage

13.22.5. Others (IP based storage, fibre channel storage)

13.23. ASEAN Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

13.23.1. Financial services

13.23.2. Media and entertainment

13.23.3. Healthcare and life sciences

13.23.4. Public sector

13.23.5. Others

13.24. Rest of Asia Pacific Personal and Entry Level Storage (PELS) Market Forecast, by Product

13.24.1. Non-cloud based storage

13.24.1.1. Recordable discs for PELS

13.24.1.2. Flash drives for PELS

13.24.1.3. Hard disk drives (HDD) for PELS

13.24.1.4. Solid state drives (SSD) for PELS

13.24.2. Cloud based storage for PELS

13.25. Rest of Asia Pacific Personal and Entry Level Storage (PELS) Market Forecast, by Technology

13.25.1. SAS (serial attached SCSI)

13.25.2. DAS (direct attached storage) for PELS

13.25.3. NAS (network attached storage)

13.25.4. Cloud based storage

13.25.5. Others (IP based storage, fibre channel storage)

13.26. Rest of Asia Pacific Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

13.26.1. Financial services

13.26.2. Media and entertainment

13.26.3. Healthcare and life sciences

13.26.4. Public sector

13.26.5. Others

13.27. Asia Pacific Personal and Entry Level Storage (PELS) Market Attractiveness Analysis

13.27.1. By Product

13.27.2. By Technology

13.27.3. By End-Use Industry

13.28. PEST Analysis

13.29. Key Trends

13.30. Key Developments

14. Middle East & Africa Personal and Entry Level Storage (PELS) Market Analysis

14.1. Key Findings

14.2. Middle East & Africa Personal and Entry Level Storage (PELS) Market Overview

14.3. Middle East & Africa Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Product

14.4. Middle East & Africa Personal and Entry Level Storage (PELS) Market Forecast, by Product

14.4.1. Non-cloud based storage

14.4.1.1. Recordable discs for PELS

14.4.1.2. Flash drives for PELS

14.4.1.3. Hard disk drives (HDD) for PELS

14.4.1.4. Solid state drives (SSD) for PELS

14.4.2. Cloud based storage for PELS

14.5. Middle East & Africa Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Technology

14.6. Middle East & Africa Personal and Entry Level Storage (PELS) Market Forecast, by Technology

14.6.1. SAS (serial attached SCSI)

14.6.2. DAS (direct attached storage) for PELS

14.6.3. NAS (network attached storage)

14.6.4. Cloud based storage

14.6.5. Others (IP based storage, fibre channel storage)

14.7. Middle East & Africa Personal and Entry Level Storage (PELS) Market Value Share Analysis, by End-Use Industry

14.8. Middle East & Africa Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

14.8.1. Financial services

14.8.2. Media and entertainment

14.8.3. Healthcare and life sciences

14.8.4. Public sector

14.8.5. Others

14.9. Middle East & Africa Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Country

14.10. Middle East & Africa Personal and Entry Level Storage (PELS) Market Forecast, by Country

14.10.1. GCC

14.10.2. South Africa

14.10.3. Rest of Middle East & Africa

14.11. Middle East & Africa Personal and Entry Level Storage (PELS) Market Analysis, by Country

14.12. GCC Personal and Entry Level Storage (PELS) Market Forecast, by Product

14.12.1. Non-cloud based storage

14.12.1.1. Recordable discs for PELS

14.12.1.2. Flash drives for PELS

14.12.1.3. Hard disk drives (HDD) for PELS

14.12.1.4. Solid state drives (SSD) for PELS

14.12.2. Cloud based storage for PELS

14.13. GCC Personal and Entry Level Storage (PELS) Market Forecast, by Technology

14.13.1. SAS (serial attached SCSI)

14.13.2. DAS (direct attached storage) for PELS

14.13.3. NAS (network attached storage)

14.13.4. Cloud based storage

14.13.5. Others (IP based storage, fibre channel storage)

14.14. GCC Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

14.14.1. Financial services

14.14.2. Media and entertainment

14.14.3. Healthcare and life sciences

14.14.4. Public sector

14.14.5. Others

14.15. South Africa Personal and Entry Level Storage (PELS) Market Forecast, by Product

14.15.1. Non-cloud based storage

14.15.1.1. Recordable discs for PELS

14.15.1.2. Flash drives for PELS

14.15.1.3. Hard disk drives (HDD) for PELS

14.15.1.4. Solid state drives (SSD) for PELS

14.15.2. Cloud based storage for PELS

14.16. South Africa Personal and Entry Level Storage (PELS) Market Forecast, by Technology

14.16.1. SAS (serial attached SCSI)

14.16.2. DAS (direct attached storage) for PELS

14.16.3. NAS (network attached storage)

14.16.4. Cloud based storage

14.16.5. Others (IP based storage, fibre channel storage)

14.17. South Africa Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

14.17.1. Financial services

14.17.2. Media and entertainment

14.17.3. Healthcare and life sciences

14.17.4. Public sector

14.17.5. Others

14.18. Rest of Middle East & Africa Personal and Entry Level Storage (PELS) Market Forecast, by Product

14.18.1. Non-cloud based storage

14.18.1.1. Recordable discs for PELS

14.18.1.2. Flash drives for PELS

14.18.1.3. Hard disk drives (HDD) for PELS

14.18.1.4. Solid state drives (SSD) for PELS

14.18.2. Cloud based storage for PELS

14.19. Rest of Middle East & Africa Personal and Entry Level Storage (PELS) Market Forecast, by Technology

14.19.1. SAS (serial attached SCSI)

14.19.2. DAS (direct attached storage) for PELS

14.19.3. NAS (network attached storage)

14.19.4. Cloud based storage

14.19.5. Others (IP based storage, fibre channel storage)

14.20. Rest of Middle East & Africa Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

14.20.1. Financial services

14.20.2. Media and entertainment

14.20.3. Healthcare and life sciences

14.20.4. Public sector

14.20.5. Others

14.21. Middle East & Africa Personal and Entry Level Storage (PELS) Market Attractiveness Analysis

14.21.1. By Product

14.21.2. By Technology

14.21.3. By End-Use Industry

14.22. PEST Analysis

14.23. Key Trends

14.24. Key Developments

15. South America Personal and Entry Level Storage (PELS) Market Analysis

15.1. Key Findings

15.2. South America Personal and Entry Level Storage (PELS) Market Overview

15.3. South America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Product

15.4. South America Personal and Entry Level Storage (PELS) Market Forecast, by Product

15.4.1. Non-cloud based storage

15.4.1.1. Recordable discs for PELS

15.4.1.2. Flash drives for PELS

15.4.1.3. Hard disk drives (HDD) for PELS

15.4.1.4. Solid state drives (SSD) for PELS

15.4.2. Cloud based storage for PELS

15.5. South America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Technology

15.6. South America Personal and Entry Level Storage (PELS) Market Forecast, by Technology

15.6.1. SAS (serial attached SCSI)

15.6.2. DAS (direct attached storage) for PELS

15.6.3. NAS (network attached storage)

15.6.4. Cloud based storage

15.6.5. Others (IP based storage, fibre channel storage)

15.7. South America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by End-Use Industry

15.8. South America Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

15.8.1. Financial services

15.8.2. Media and entertainment

15.8.3. Healthcare and life sciences

15.8.4. Public sector

15.8.5. Others

15.9. South America Personal and Entry Level Storage (PELS) Market Value Share Analysis, by Country

15.10. South America Personal and Entry Level Storage (PELS) Market Forecast, by Country

15.10.1. Brazil

15.10.2. Mexico

15.10.3. Rest of South America

15.11. South America Personal and Entry Level Storage (PELS) Market Analysis, by Country

15.12. Brazil Personal and Entry Level Storage (PELS) Market Forecast, by Product

15.12.1. Non-cloud based storage

15.12.1.1. Recordable discs for PELS

15.12.1.2. Flash drives for PELS

15.12.1.3. Hard disk drives (HDD) for PELS

15.12.1.4. Solid state drives (SSD) for PELS

15.12.2. Cloud based storage for PELS

15.13. Brazil Personal and Entry Level Storage (PELS) Market Forecast, by Technology

15.13.1. SAS (serial attached SCSI)

15.13.2. DAS (direct attached storage) for PELS

15.13.3. NAS (network attached storage)

15.13.4. Cloud based storage

15.13.5. Others (IP based storage, fibre channel storage)

15.14. Brazil Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

15.14.1. Financial services

15.14.2. Media and entertainment

15.14.3. Healthcare and life sciences

15.14.4. Public sector

15.14.5. Others

15.15. Mexico Personal and Entry Level Storage (PELS) Market Forecast, by Product

15.15.1. Non-cloud based storage

15.15.1.1. Recordable discs for PELS

15.15.1.2. Flash drives for PELS

15.15.1.3. Hard disk drives (HDD) for PELS

15.15.1.4. Solid state drives (SSD) for PELS

15.15.2. Cloud based storage for PELS

15.16. Mexico Personal and Entry Level Storage (PELS) Market Forecast, by Technology

15.16.1. SAS (serial attached SCSI)

15.16.2. DAS (direct attached storage) for PELS

15.16.3. NAS (network attached storage)

15.16.4. Cloud based storage

15.16.5. Others (IP based storage, fibre channel storage)

15.17. Mexico Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

15.17.1. Financial services

15.17.2. Media and entertainment

15.17.3. Healthcare and life sciences

15.17.4. Public sector

15.17.5. Others

15.18. Rest of South America Personal and Entry Level Storage (PELS) Market Forecast, by Product

15.18.1. Non-cloud based storage

15.18.1.1. Recordable discs for PELS

15.18.1.2. Flash drives for PELS

15.18.1.3. Hard disk drives (HDD) for PELS

15.18.1.4. Solid state drives (SSD) for PELS

15.18.2. Cloud based storage for PELS

15.19. Rest of South America Personal and Entry Level Storage (PELS) Market Forecast, by Technology

15.19.1. SAS (serial attached SCSI)

15.19.2. DAS (direct attached storage) for PELS

15.19.3. NAS (network attached storage)

15.19.4. Cloud based storage

15.19.5. Others (IP based storage, fibre channel storage)

15.20. Rest of South America Personal and Entry Level Storage (PELS) Market Forecast, by End-Use Industry

15.20.1. Financial services

15.20.2. Media and entertainment

15.20.3. Healthcare and life sciences

15.20.4. Public sector

15.20.5. Others

15.21. South America Personal and Entry Level Storage (PELS) Market Attractiveness Analysis

15.21.1. By Product

15.21.2. By Technology

15.21.3. By End-Use Industry

15.22. PEST Analysis

15.23. Key Trends

15.24. Key Developments

16. Company Profiles

16.1. Market Share Analysis, by Company

16.2. Competition Matrix

16.2.1. Competitive Benchmarking of key players by price, presence, market share, Applications and R&D investment

16.2.2. New Product Launches and Product Enhancements

16.2.3. Market Consolidation

16.2.3.1. M&A by Regions, Investment and Applications

16.2.3.2. M&A Key Players, Forward Integration and Backward

Integration

16.3. Company Profiles: Key Players

16.3.1. International Business Machines Corporation (IBM)

16.3.1.1. Company Overview

16.3.1.2. Financial Overview

16.3.1.3. Product Portfolio

16.3.1.4. Business Strategy

16.3.1.5. Recent Developments

16.3.1.6. Development Footprint

16.3.2. NetApp Inc.

16.3.3. EMC Corporation

16.3.4. Symantec Corporation

16.3.5. Cisco Systems Inc.

16.3.6. CA Technologies

16.3.7. Brocade

16.3.8. Dell Inc.

16.3.9. Hewlett-Packard Company

16.3.10. Hitachi Data Systems (HDS)

16.3.11. Toshiba Corporation

16.3.12. Seagate Technology

16.3.13. Western Digital Corporation

16.3.14. Enterprise (HPE) Company

16.3.15. Pure Storage, Inc.

16.3.16. Nutanix, Inc.

16.3.17. Tintri, Inc.

16.3.18. Simplivity Corp.

16.3.19. Scality, Inc.

17. Primary Key Insights

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report