Online Travel Booking Market 2025–2032: Sustainable Transformation, Technical Online Travel Booking Expansion, and Global Manufacturing Shifts

Overview

The Online Travel Booking Market Size 2025–2032 is expected to grow from USD 700 billion in 2025 to USD 1024.56 billion by 2032, registering a CAGR of 5.54%, driven by sustainable travel adoption, technological expansion in online booking platforms, digital transformation, and evolving global supply chain strategies.

| 2025 Market Size | 2032 Forecast | CAGR (2026–2032) | Base Year | Forecast Period |

| USD 700 Billion | USD 1,024.56 Billion | 5.54% | 2025 | 2026–2032 |

To know about the Research Methodology :- Request Free Sample Report

Online Travel Booking Market Report Overview

The Global Online Travel Booking Market Growth Analysis highlights a structural transformation driven by digital adoption, technological innovation, and platform integration across travel services. The market is forecasted to grow from USD 700 billion in 2025 to USD 1,024.56 billion by 2032, supported by increasing demand for sustainable travel solutions, rapid digital adoption in emerging economies, and expansion of technical online booking platforms across leisure, corporate, and niche travel segments.

Key Highlights

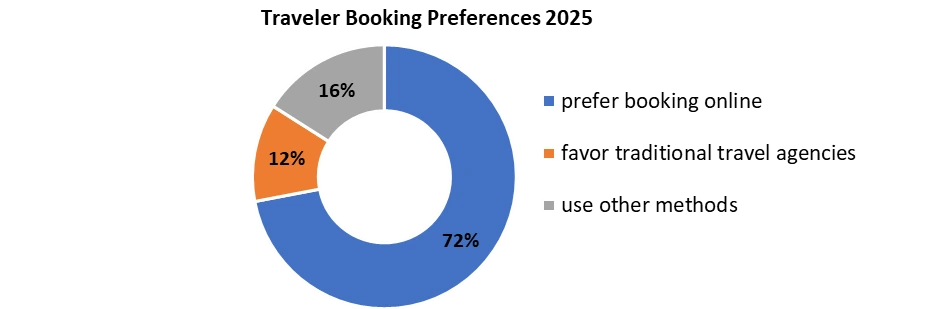

• In 2025, the majority of Americans (72%) prefer to book their travel through internet platforms. More than half of Americans 58% choose to use online travel agencies OTAs for their trip bookings.

• It is observed that in 2025, 60% of online travel traffic originates from mobile devices; however, desktop continues to generate ~62% of total booking revenue, indicating a mobile-browse, desktop-convert pattern.

• 55% of travelers expect AI-driven personalization from booking platforms by 2025; 28% of current bookings are already influenced by AI recommendations.

• 45% of OTAs in 2025, report intensifying pressure from metasearch engines, while 49% are investing in blockchain infrastructure to enhance pricing transparency.

• The global travel and tourism industry will receive 74% of its revenue from online sales channels by the year 2027.

• The travel segment of the application market generates global revenue of 1.45 billion dollars in 2025, which will increase to 1.96 billion dollars by 2027.

• The leading online travel agencies all charge between 15% to 25% commission fees, while the smaller OTAs provide commission rates that start at 4% in 2025.

Title: Online Travel Booking Market Size in 2025, Forecast (2026–2032)

| Worldwide Online Travel Market Size: 2020–2032 | In Billion US Dollars |

| 2020 | 396.08 |

| 2021 | 433.2 |

| 2022 | 474.89 |

| 2023 | 521.18 |

| 2025 | 700 |

| 2030 | XX |

| 2032 | 1,024.56 |

From Quick Getaways to Parisian Escapes: The Digital Travel Boom Redefines How the World Explores

The global online travel market points to an increasing appetite for ease, flexibility, and experience-led holidays. Domestic travel reigns supreme, representing 60% of all bookings and 55% of bookings for flights. 40% of bookings are for short stays of 1–2 nights. Among the accommodation options, hotels are taking the lead with 65%, while vacation rentals have a total share of 35%. Business travel accounts for 32% of sales, in addition to robust family (28%) and group (25%) demand. Bookings at the last-minute account for 42 percent, a sign of increasing spontaneity. The most booked city in 2023 was Paris, and the lowest one was Oslo. North America is leading globally, with luxury and international travel particularly strong post-pandemic growth.

AI Ambitions Meet Pricing Pressures: The New Balancing Act for Digital Travel Platforms

The online travel ecosystem is evolving amid rising consumer expectations and operational pressures. While 55% of travelers expect AI-driven personalization by 2025 and 28% of bookings are already influenced by AI recommendations, challenges persist. Price fluctuations (60%) and dynamic pricing concerns (39%) significantly impact booking decisions, with 32% abandoning purchases due to hidden fees. Privacy (41%), sustainability (62%), and contactless experiences (57%) now shape traveler preferences, while 33% of bookings occur via voice assistants and 24% rely on chatbots for support. Meanwhile, 45% of OTAs face metasearch competition, 36% struggle with supply disruptions, and 49% are investing in blockchain to enhance transparency and trust.

Online Travel Booking: Growth Trends

• The global online travel industry reached a market size of USD 654 billion in 2024, which demonstrates strong development since previous years.

• Digital adoption plus new travel platforms will drive market growth to exceed $1 trillion by 2031, according to current market projections.

• The U.S. online travel industry saw a strong recovery in 2024 after it reached a pandemic low of $58.6 billion in 2020, which brought the market to almost $144 billion.

U.S. online travel industry growth (2020–2024)

• The mobile travel booking market had a value of $228 billion in 2024, which will grow to more than $526 billion by 2032

• The market in North America holds approximately 35% share because of high smartphone usage, widespread internet availability, and strong mobile commerce activity.

Leading Travel Websites and Companies

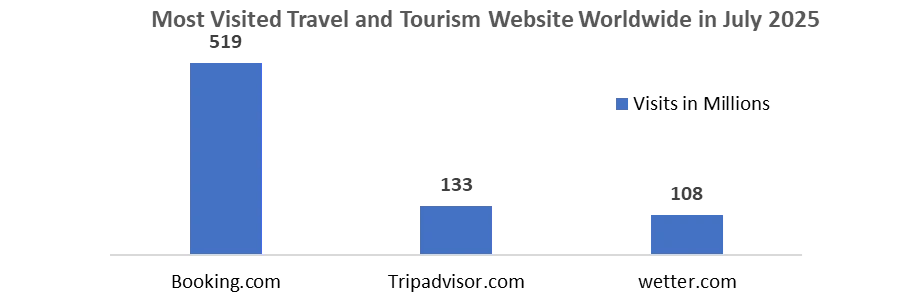

• Booking.com kept its status as the most popular travel website in the world during July 2025 when users made almost 519 million visits to the site. Tripadvisor.com received approximately 133 million visits, while wetter.com received around 108 million visits to become the second most visited website.

Most visited travel and tourism website worldwide in July 2025

• In 2024, Booking Holdings reported its highest-ever revenue of nearly $24 billion.

• Expedia Group generated nearly $14 billion in revenue in 2024.

Market Cap and Bookings

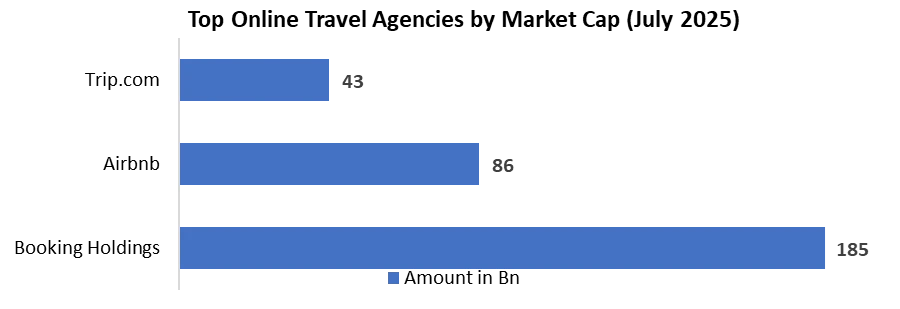

Booking Holdings was considered to be the online travel agency with the highest market Capitalization Until Mid-2025, At Almost USD 185 Billion.

• Booking Holdings experienced a 10% rise in booking volumes during 2024 when compared to the previous year, as room nights reached more than 1.1 billion.

• Airline ticket bookings achieved their highest annual growth rate since 2024, which resulted in a 36% increase from the previous year.

Online Travel Booking Market Segment Analysis

The segmentation framework below is structured hierarchically — from booking channel through service type to travel purpose and end-user — enabling precise market sizing at every intersection and facilitating decision-making at the product, distribution, and investment levels.

Online Travel Booking Market Scope: Inquire before buying

| Segmentation Axis | Sub-segments |

| By Device | Desktop | Mobile (App & Browser) |

| By Booking Method | Online Travel Agencies (OTAs) | Direct Supplier Booking | Corporate / B2B Travel Platforms |

| By Service Type | Accommodation Booking | Flight & Transportation | Vacation Packages | Car Rentals | Activities & Experiences |

| By Travel Purpose | Leisure Travel | Business Travel | MICE (Meetings, Incentives, Conferences & Exhibitions) |

| By End-User | Individual Consumers (B2C) | Corporate Accounts (B2B) | Travel Management Companies (TMCs) |

| By Region | North America | Europe | Asia Pacific | Middle East & Africa | South America |

By Device

• Desktop: Continues to dominate booking revenue (~62% of total) despite representing a minority of browsing sessions. Preferred for complex, high-value bookings such as international packages and business travel.

• Mobile (App & Browser): Commands 60% of traffic volume. Growth driven by app-native OTA experiences (Booking.com, MakeMyTrip, Trip.com), push-notification retargeting, and BNPL integration.

By Booking Method

• Online Travel Agencies (OTAs): Dominant channel; platforms such as Booking Holdings, Expedia, and Trip.com collectively command the largest share of online transactions.

• Direct Supplier Booking: Growing as hotel chains (Marriott, Hilton) and airlines invest in loyalty-linked direct channels to reclaim OTA commission fees (15–25%).

• Corporate / B2B Travel Platforms: Expanding segment driven by TMC digitization, expense integration, and policy-compliant booking tools.

By Service Type

• Accommodation Booking: Hotels hold 65% share of accommodation bookings; vacation rentals (Airbnb-category) account for 35% and are growing.

• Flight & Transportation: Airline ticket bookings posted their highest annual growth in 2024 (+36% YoY), reflecting pent-up demand and low-cost carrier expansion.

• Vacation Packages: Bundled offerings are recovering as consumer confidence stabilizes and demand for stress-free trip planning rises.

• Car Rentals: Digital-first platforms (Hertz, Enterprise) and EV rental entrants are driving segment digitization.

• Activities & Experiences: Fastest-growing sub-segment; platforms such as GetYourGuide and KKday are scaling rapidly.

By Travel Purpose

• Leisure Travel: Largest segment; domestic leisure bookings represent 60% of all transactions. 28% is family travel, 25% group travel.

• Business Travel: Accounts for 32% of total bookings; recovery supported by hybrid work policies and the re-normalization of in-person conferences.

• MICE: Premium-value segment; corporate event platforms are increasingly integrated with OTA infrastructure.

Online Travel Booking Consumer Preferences

Understanding the behavioural economics of the online traveller is a core differentiator of this study. The following insights move beyond surface-level statistics to identify decision-driving patterns that platforms and brands can act on:

• 53% of online bookers cite fast trip planning as the primary reason for choosing online platforms; 47% prioritise price comparison, and 42% seek better pricing options — indicating that speed-to-decision and price confidence are the two dominant conversion levers.

• 76% of travelers seek travel applications that demonstrably reduce planning friction and streamline the end-to-end journey — a clear mandate for UX investment.

• 56% of travelers research destination content before booking; 25% begin activity planning more than four weeks ahead, revealing a long consideration window that platforms can leverage through content marketing and early-bird incentives.

• 42% of bookings are last-minute (same day to 7 days before travel), creating a structurally important flash-sale and dynamic pricing opportunity.

• Paris was the most booked international city destination in 2023; Oslo ranked the least booked among major European cities — offering a clear signal for destination marketing investment.

Online Travel Booking Market Regional Analysis

North America

North America holds approximately 35% of global online travel booking revenue, underpinned by the highest per-capita travel spend globally, near-universal internet penetration, and mature OTA infrastructure. The US market — valued at approximately USD 144 billion in 2024 — recovered decisively from its pandemic low of USD 58.6 billion in 2020. Premium leisure travel and corporate travel recovery are the two dominant growth vectors. The region is also the global leader in AI-driven travel personalization investment.

Asia Pacific

Asia Pacific is the fastest-growing regional market, propelled by China's outbound travel normalization, India's digital infrastructure boom (UPI-enabled payments, app-native consumer behaviour), and Southeast Asia's expanding middle class. The mobile-first booking behaviour of APAC consumers is structurally advantageous for OTA platforms with strong app ecosystems.

Europe

Europe is chracterized by high platform maturity, strong regulatory oversight (GDPR, Package Travel Directive), and increasing demand for sustainable travel options. Booking.com's European dominance and the strength of regional low-cost carriers (Ryanair, EasyJet) create a distinctive competitive dynamic centred on price sensitivity and loyalty.

Middle East & Africa

The GCC region — led by Saudi Arabia's Vision 2030 tourism ambitions and the UAE's established hub position — is the standout growth market within ME&A. Halal-friendly travel platforms and Arabic-language OTA customisation are emerging competitive differentiators.

South America

Brazil and Chile lead South American online travel adoption. Local payment complexity (instalment-based purchasing), currency volatility, and airline capacity limitations remain structural constraints, but digital penetration is rising rapidly.

Technology Innovation & Platform Development

- AI-Powered Travel Planning: Generative AI integrations (LLM-based itinerary builders, real-time fare prediction) are transitioning from novelty to standard platform feature.

- Personalised Booking Engines: Behavioural data, loyalty programme integration, and real-time inventory signals are enabling hyper-personalised search and sort algorithms.

- Mobile UX & Super-App Convergence: Leading APAC platforms (Ctrip, MakeMyTrip) are building super-app ecosystems that bundle travel, payments, insurance, and lifestyle services.

- Blockchain for Trust Infrastructure: Smart contracts are being piloted for transparent price-lock guarantees, dispute resolution, and loyalty point portability.

- Metasearch & Price Comparison Evolution: Google's deepening integration of flight and hotel search into its core SERP (Search Engine Results Page) is the single largest structural threat to traditional OTA discovery models.

Regulatory & Compliance Environment

- North America: FTC consumer protection guidelines, state-level privacy laws (CCPA), and DOT consumer protection rules for airlines shape digital platform conduct.

- Europe: GDPR compliance is the dominant regulatory overhead for European OTAs and any global platform serving EU consumers. The EU Package Travel Directive mandates specific consumer protection standards for bundled travel products.

- Asia Pacific: India's Digital Personal Data Protection Act (DPDPA 2023) and China's PIPL introduce significant data localisation requirements for OTA operators.

- Middle East & Africa: Saudi Arabia's NDC (New Distribution Capability) mandate for airlines and the UAE's emerging consumer protection regulations are shaping OTA distribution models.

Actionable Strategic Takeaways

The following recommendations are derived from the intelligence compiled in this study and are intended to directly inform platform strategy, investment positioning, and market entry decisions:

- OTAs must prioritise AI investment to stay relevant: Platforms that fail to embed AI-driven personalization, dynamic pricing optimisation, and conversational booking interfaces risk losing share to tech-native entrants. The TripAdvisor–OpenAI partnership is an industry benchmark.

- Direct booking channels are a strategic necessity for accommodation providers: With OTA commissions running at 15–25%, hotel chains and independent properties should invest in loyalty-linked direct booking infrastructure to protect margin — not merely as a long-term aspiration, but as an immediate competitive response.

- Mobile UX is a growth enabler, not just a channel: The browse-on-mobile, book-on-desktop pattern signals a specific friction point in the mobile booking flow. OTAs that eliminate this friction — through saved searches, one-click checkout, and biometric authentication — will capture a materially higher share of impulse and last-minute bookings.

- Emerging markets demand localised strategies: Indian, Indonesian, and Brazilian OTA growth cannot be unlocked with North American playbooks. Local payment methods, vernacular-language interfaces, and regionally relevant loyalty mechanics are prerequisites for market entry success.

- Sustainability is a monetisable differentiator: 62% of travelers factor sustainability into booking decisions. Platforms that surface verified eco-certified properties and offer carbon-offset options at checkout can command a premium and differentiate in a price-saturated market.

- Metasearch pressure requires a dual response: OTAs should simultaneously invest in Google Hotels/Flights visibility and in building direct app engagement that bypasses metasearch entirely — reducing structural dependency on the channel they cannot control.

Travel Industry Revenue and Future Outlook

- The global travel and tourism industry depends on digital platforms, which generated about 70 percent of industry revenue in 2024.

- The industry will continue to grow because new technologies and changes in consumer behavior and digital platforms will drive market expansion, according to future predictions.

Online bookings are expected to reach 73 % of total travel sales by 2029 because of digital technology progress and AI-powered customized services.