Nanofiltration Membrane Market Size by Type, Application, Membrane Type, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

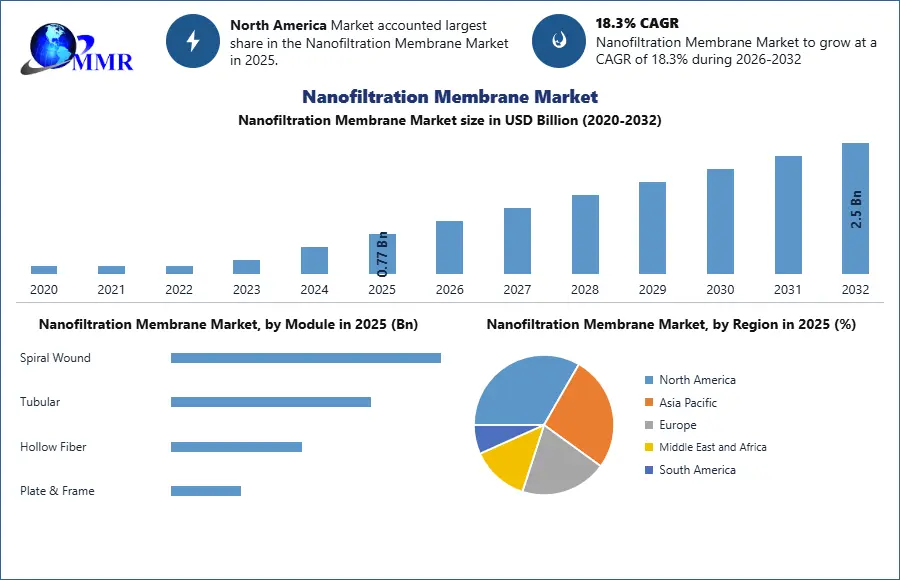

Nanofiltration Membrane Market size is expected to reach 2.5 US$ Bn in year 2032, at a CAGR of 18.3% during the forecast period.

Nanofiltration is the recent advancement in the membrane filtration process in surface water filtration and fresh groundwater filtration process. This type of filtration helps in water softening and sterilisation of water. The global nanofiltration membrane market is driven by its applications and demand from end users, which include water & wastewater treatment, food & beverages, chemical & petrochemicals, pharmaceutical & biomedical, textile and metalworking industry. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

In the food & beverage industry, nanofiltration membrane is used to concentrate food & beverages naturally without degrading the products. At the same time, increase in disposable income of individual and high standard of living across developed and emerging economies leads to an increase in demand for fast food & beverages. This makes way for an increase in demand for nanofiltration membrane for the concentration of food & beverages.The report study has analyzed revenue impact of COVID -19 pandemic on the sales revenue of market leaders, market followers and market disrupters in the report and same is reflected in our analysis.

Nanofiltration membrane finds application in water and wastewater treatment that includes water softening and colour removal, industrial wastewater treatment, water reuse, and desalination. Rapid urbanization and industrialization across emerging economies such as India and China and an increase in demand for water for domestic and industrial purposes are expected to boost the growth of the market. Expansion of the pharmaceutical industry across developing nations such as India, China, and Brazil also increase the demand for nanofiltration membrane in the market. In addition, an increase in sales of generic medicines, developments in medical infrastructure, and the rise in demand for low-cost drugs are expected to drive boost the growth of the nanofiltration membrane market.

At the same time, high installation costs and lack of funds in the emerging economies such as India restrict market growth. Furthermore, nanofiltration membranes are highly sensitive to free chlorine inability in treatment of chlorine concentration is expected to hinder the growth of the market. Increase in the use of chemical free water treatment procedures across various industries provides potential growth opportunities for market expansion.

According to type, the polymeric segment dominated the market in 2023, on account of its demand in wastewater treatment and water purification plants as these membranes operate on low pressure and provide higher filtration rate. There is a significant increase in the demand for water filtration techniques due to the increase in scarcity for pure water in regions such as North America and the Middle East. This, in turn, increases the requirement of nanofiltration membrane in the water filter technology.

Among the regions, North America is a leading region in the market. It is expected to maintain its dominance in the nanofiltration membrane market during the forecast period and Asia-Pacific is expected to be the fastest growing region because of increase in usage of nanofiltration membranes in water treatment systems and high government regulations regarding water pollutions and environment safety.

The nanofiltration membranemarket report contains in-depth analysis of major drivers, opportunities, challenges, industry trends and their impact on the market. The nanofiltration membrane Market report also provides data about the company and its strategy. This report also provides information on the competitive landscape section of the report provides a clear insight into the market share analysis of key industry players. The nanofiltration membrane Market report also provides a company overview, financial overview, product portfolio, new project launched, and recent development analysis is the parameters included in the report. This research report also adds a snapshot of key competition, market trends during the forecast period, expected growth rates and the primary factors driving and impacting growth market data. This information will be beneficial or helpful to the decision makers.

The objective of the report is to present a comprehensive assessment of the market and contains thoughtful insights, facts, historical data, industry-validated market data and projections with a suitable set of assumptions and methodology. The report also helps in understanding the global nanofiltration membrane market dynamics, structure by identifying and analysing the market segments and project the global market size. Further, the report also focuses on the competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence. The report also provides PEST analysis, PORTER’s analysis, and SWOT analysis to address questions of shareholders to prioritizing the efforts and investment in the near future to the emerging segment in the global nanofiltration membrane market.

Nanofiltration Membrane Market Scope: Inquire before buying

| Nanofiltration Membrane Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 0.77 USD Billion |

| Forecast Period 2026-2032 CAGR: | 18.3% | Market Size in 2032: | 2.5 USD Billion |

| Segments Covered: | by Type | Polymeric Polyamide Polysulfone & Polyethersulfone Others Ceramic Zircon ia Alumina Titania Others Composite Others |

|

| by Module | Spiral Wound Tubular Hollow Fiber Plate & Frame |

||

| by Application | Municipal Treatment Desalination Utility Water Treatment Wastewater Reuse Industrial Treatment Food & Beverage Processing Pharmaceutical & Biotechnology Chemical & Petrochemical Others |

||

Nanofiltration Membrane Market, by Region:

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Nanofiltration Membrane Market, Key Players:

1. DuPont

2. Toray Industries

3. NX Filtration

0. Pentair Plc

5. LG Chem (LG Water Solutions)

6. Hydranautics (Nitto Denko Corporation)

7. ALFA LAVAL

8. Applied Membranes Inc.

9. GE Water & Process Technologies

10.Aquatech

11.Koch Membrane Systems Inc.

12.Microdyn-Nadir (MANN+HUMMEL Group)

13.Inopor GmbH

14.Solecta Inc.

15.Seppure Technologies

16.Sitration Inc.

17.Nematiq

18.MOLYMEM

19.Trucent

20.UltraClean Membrane Technology

21.Vontron Membrane Technology

22.Envirogen Technologies

23.Wigen Water Technologies

24.Pall Corporation

25.GEA Group

26.Synder Filtration

27.Veolia Water Technologies

28.Others

Frequently Asked Questions:

1. Which region has the largest share in Global Nanofiltration Membrane Market?

Ans: North America region held the highest share in 2025.

2. What is the growth rate of Global Nanofiltration Membrane Market?

Ans: The Global Nanofiltration Membrane Market is growing at a CAGR of 18.3% during forecasting period 2026-2032.

3. What is scope of the Global Nanofiltration Membrane market report?

Ans: Global Nanofiltration Membrane Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Nanofiltration Membrane market?

Ans: The important key players in the Global Nanofiltration Membrane Market are – Alfa Laval, Applied Membranes, Inc., Argonide Corporation, Danaher, DowDuPont Inc., GEA Group Aktiengesellschaft, Inopor, Koch Membrane Systems, Inc., Nitto Denko Corporation, Toray Industries, Inc., Pall Water, Synder Filtration, DOW Chemical, Toray Water, Culligan, Synder Filtration, and Linde.

5. What is the study period of this market?

Ans: The Global Nanofiltration Membrane Market is studied from 2025 to 2032.