Mobile Gaming Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

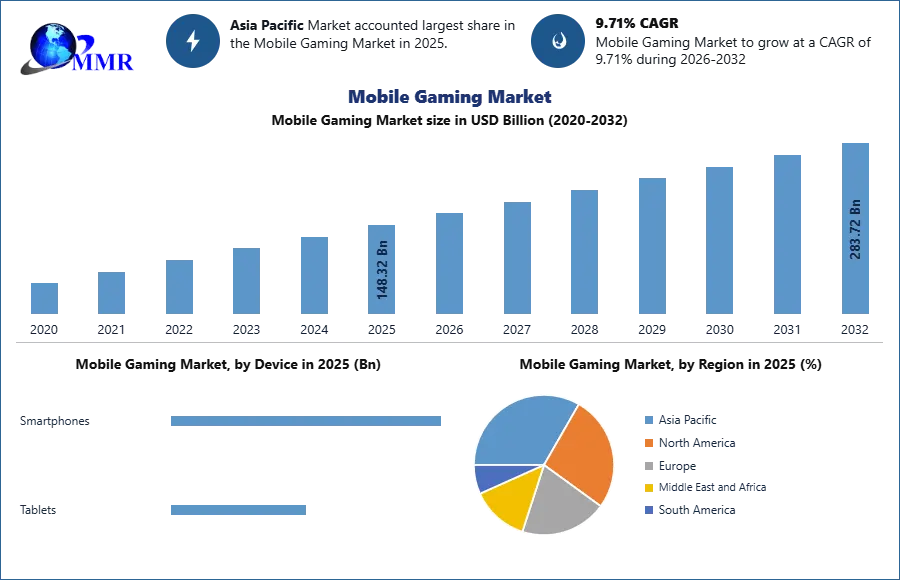

The Mobile Gaming Market was valued at USD 148.32 Billion in 2025 and is estimated to grow at a CAGR of 9.71% over the forecast period, reaching USD 283.72 Billion by 2032.

Mobile Gaming Market Overview:

The global mobile gaming market was valued at USD 139.38 Bn. in 2024. Games like BGMI, PUBG Mobile, Call of Duty Mobile, and others are very popular on mobile devices these days. Because of the growing popularity of smartphones, the global market for games will grow in value. Growing global internet service penetration, combined with easy availability and access to online games, is likely to keep growth prospects positive in the future years. With a growing desire to move away from physical games and toward online gaming, industry participants are focusing on device compatibility and efficiency. Free2Play (F2P), massively multiplayer online (MMO), and multiplayer games have all grown in popularity over the last eight years, and this trend is expected to continue.Mobile gaming refers to digital games played primarily on smartphones, tablets, and related portable connected devices through native apps, instant-play environments, or cloud-enabled delivery. The market has evolved into the largest and most commercially important segment of the global games industry, supported by smartphone penetration, low-friction app distribution, broad genre accessibility, and sophisticated live-service monetization. Growth has been driven by casual gaming adoption, competitive multiplayer formats, social and community features, and the ability of publishers to monetize through in-app purchases, advertising, subscriptions, and recurring events. Technology development has increasingly centered on cross-platform progression, cloud gaming access, AI-assisted content iteration, higher-performance mobile chipsets, and better analytics for retention and personalization. Demand outlook remained positive because mobile gaming continued to attract both mainstream and core players, while publishers expanded addressable audiences through better device optimization, regional content localization, and deeper integration of social, competitive, and creator-led engagement models.

To know about the Research Methodology :- Request Free Sample Report

Mobile Gaming Market Dynamics:

Smartphone-Centric User Expansion And Engagement Depth

The market continued to benefit from the widening global base of smartphone users, stronger mobile-first entertainment behavior, and deeper session frequency across casual and mid-core titles. Industry tracking showed mobile remained the largest gaming access point globally, while broader games-market reporting indicated that 3.6 billion players participated in gaming in 2025 and that the U.S. and China together accounted for 50% of consumer spend. This mattered for mobile gaming because those markets remained highly influential in user acquisition economics, live-ops design, and publisher monetization strategy. Developers also benefited from faster device replacement cycles, larger screens, better chipsets, and more stable broadband and 5G access, all of which improved gameplay quality and expanded addressable genres beyond simple casual formats.

Monetization Sophistication And Live-Service Operating Models

A major structural growth factor was the increasing sophistication of monetization design. Free-to-play remained the commercial backbone of the industry, and one public market disclosure stated that the free-to-play model held 78.9% share in 2024. That leadership reflected the ability of publishers to combine in-app purchases, ad monetization, battle passes, limited-time events, cosmetic content, and retention-driven progression systems. Mobile gaming increasingly operated as a live-service business rather than a one-time download business. The category therefore rewarded publishers that could continuously refresh content, segment players intelligently, and optimize user lifetime value without undermining player satisfaction. This also supported stronger publisher investment in analytics, personalization, CRM systems, and community-led event calendars.

Cloud Distribution, Cross-Platform Play, And AI-Led Development Tools

The market was also being reshaped by infrastructure and toolchain evolution. Samsung expanded its mobile cloud gaming platform into Europe in 2025, beginning in the U.K. and Germany, allowing Galaxy users to access games without downloads. Google continued expanding Google Play Games on PC, enabling cross-platform gameplay across mobile, tablets, Chromebooks, and Windows PCs. Unity also announced expanded platform support and new AI-powered workflows in its 2025 engine roadmap. Together, these developments showed that mobile gaming was no longer limited to app-store-only distribution. Instead, the market was moving toward device continuity, lighter installation friction, faster content testing, and broader multi-screen engagement models.

Mobile Gaming Market Segment Analysis:

Mobile Gaming Market Segmentation, By Platform

Based on platform, the market has been divided into Android, iOS, Hybrid Cross-Platform, and Progressive Web Apps. Among these, the Android sub-segment was projected to generate the maximum revenue. The Android sub-segment witnessed the highest market share in the global mobile gaming market in 2025. This segment dominated because Android had the broadest global device installed base, stronger reach across price-sensitive markets, and deeper penetration in emerging economies where mobile gaming often served as the primary form of digital entertainment. Android also benefited from a large publisher ecosystem, wide hardware availability, flexible distribution economics, and better scalability for free-to-play titles designed for mass adoption. In 2025, Android remained the most commercially important platform because publishers prioritized scale, acquisition efficiency, regional accessibility, and monetization breadth across diverse consumer spending profiles. Its leadership was further supported by the continuing expansion of mobile-first gaming across Asia, Latin America, and other high-volume Android-led markets.

Mobile Gaming Market Segmentation, By Monetization Model

Based on monetization model, the market has been divided into Free To Play, In-App Purchases, Premium Paid Games, Subscription Based, Advertising Based, and Play To Earn. Among these, the Free To Play sub-segment generated the maximum revenue in 2025. This segment dominated because it removed purchase barriers at the point of download and allowed publishers to monetize a wider player funnel through content upgrades, battle passes, advertising, digital goods, and live-event participation. Free-to-play titles were also better aligned with viral growth, influencer visibility, and large-scale community building. In 2025, this model remained commercially superior because mobile gaming success increasingly depended on long-term engagement rather than one-time transactions. Publishers that operated strong live-service models could continuously optimize progression, pricing, content cadence, and player segmentation. That operating structure made free-to-play the most scalable and strategically resilient business model across both casual and competitive mobile gaming categories.

Mobile Gaming Market Regional Analysis

Asia Pacific dominated the market in the year 2025, and was expected to continue its dominance during the forecast period. The region led because it combined the world’s largest base of mobile gamers with strong smartphone penetration, powerful app-store ecosystems, highly active esports and creator communities, and deep publisher concentration across China, Japan, South Korea, and Southeast Asia. Asia Pacific held 47.04% share in 2024 in one market view, while another public view placed the region above 63% share in 2024 under a different scope definition. Broader gaming-market reporting also highlighted Asia as the principal growth center for digital gaming demand. In 2025, Asia Pacific maintained its leadership because mobile remained the default gaming device for large parts of the region, and publishers continued to benefit from massive player communities, strong live-ops adoption, and regional expertise in free-to-play monetization, social competition, and localized content strategies.

Recent Developments

March 2025: Scopely announced an agreement to acquire Niantic’s games business, including Pokémon GO, Pikmin Bloom, Monster Hunter Now, Campfire, and Wayfarer. Scopely later confirmed the deal closed on May 29, 2025. The transaction materially strengthened Scopely’s scale in location-based and community-driven mobile gaming, while expanding its global player reach and live-service portfolio.

May 2025: Dream Games announced a strategic investment from CVC to support its next growth phase and continued leadership in mobile games. The deal highlighted the attractiveness of top-performing mobile publishers with durable live-ops economics, strong franchise retention, and global monetization scale, especially in puzzle and casual categories with long lifetime value profiles.

August 2025: Samsung expanded its mobile cloud gaming platform into Europe, beginning with the U.K. and Germany. The rollout allowed Galaxy users to access mobile titles without downloads or installations and signaled growing momentum behind cloud-based mobile distribution. This development was important because it reduced install friction and expanded alternative discovery pathways beyond app stores.

March 2025: Supercell launched mo.co globally, bringing a new mobile monster-hunting experience to market. The release was significant because it demonstrated continued appetite for original mobile IP beyond established franchises. It also showed that major publishers were still willing to invest in fresh gameplay loops and community-led live-service ecosystems in a crowded market.

August 2025: NetEase Games released Destiny: Rising worldwide for iOS and Android. The title, set in the Destiny universe, reinforced the commercial importance of premium mobile adaptations of established gaming IP. Its launch reflected the market’s increasing move toward deeper, console-style mobile experiences with broader content scope, more modes, and stronger franchise-based user acquisition.

July 2025: Zynga expanded Top Eleven through an official Bundesliga integration for the 2025/26 season, adding all 18 clubs, themed campaigns, and limited-time events. The partnership illustrated how sports licensing continued to strengthen retention and monetization in mobile gaming by combining live calendar relevance, fan engagement, and deeper in-game event programming.

Mobile Gaming Market Scope: Inquire before buying

| Mobile Gaming Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 148.32 Billion |

| Forecast Period 2026-2032 CAGR: | 9.71% | Market Size in 2032: | USD 283.72 Billion |

| Segments Covered: | by Platform | Android iOS |

|

| by Device | Smartphones Tablets |

||

| by Game Genre | Action And Adventure Puzzle Role-Playing Strategy And Simulation Sports And Racing Arcade Casino Casual Others |

||

| by Monetization Model | Free To Play In-App Purchases Premium Paid Games Subscription Based Advertising Based Play To Earn |

||

| by Age Group | Gen Z Millennials Gen X Baby Boomers Children Teenagers Adults |

||

| by Distribution Channel | App Stores Cloud Gaming Platforms Web-Based Instant Play |

||

Mobile Gaming Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Mobile Gaming Market, Key Players

1. Kabam Games, Inc.

2. Tencent Holdings Limited

3. Activision Blizzard, Inc

4. GungHo Online Entertainment, Inc.

5. Nintendo Co., Ltd.

6. Electronic Arts Inc.

7. Glu Mobile LLC

8. Rovio Entertainment Corporation

9. The Walt Disney Company

10. Zynga, Inc.

11. Supercell Oy

12. The Game Storm Studio

13. Ubisoft

14. Gameloft SE

15. 2K Games, Inc.

16. 37Games

17. Pocket Gems

18. Kingsoft Corporation

19. MiHoYo Co., Ltd.

20. NetEase Games

21. Perfect World Games

22. NCsoft Corporation

23. Riot Games, Inc.

24. MobilityWare

25. SciPlay

26. Other Key Players

Table of Contents

10.3. Tencent Holdings Limited

10.4. Activision Blizzard, Inc.

10.5. GungHo Online Entertainment, Inc.

10.6. Nintendo Co., Ltd.

10.7. Electronic Arts Inc.

10.8. Glu Mobile LLC

10.9. Rovio Entertainment Corporation

10.10. The Walt Disney Company

10.11. Zynga Inc.

10.12. Supercell Oy

10.13. The Game Storm Studio

10.14. Ubisoft Entertainment SA

10.15. Gameloft SE

10.16. 2K Games, Inc.

10.17. 37Games

10.18. Pocket Gems, Inc.

10.19. Kingsoft Corporation

10.20. MiHoYo Co., Ltd.

10.21. NetEase Games

10.22. Perfect World Games

10.23. NCSoft Corporation

10.24. Riot Games, Inc.

10.25. MobilityWare

10.26. SciPlay Corporation

10.27. Other Key Players