Medical Polymer Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

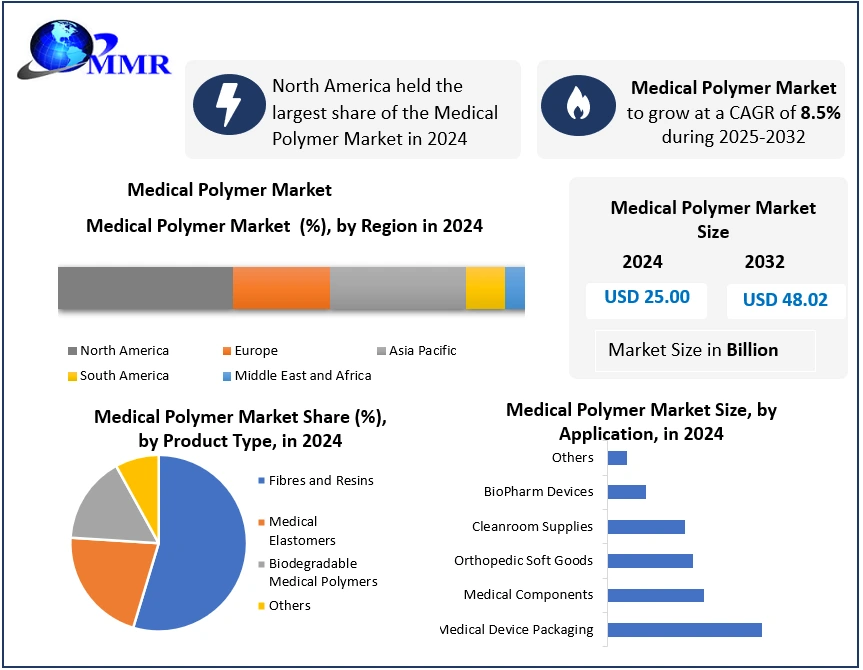

The Global Medical Polymer Market size was valued at USD 25.00 Bn in 2024, and the total Medical Polymer Market revenue is expected to grow by 8.5% from 2025 to 2032, reaching nearly USD 48.02 Bn.

Medical Polymer Market Overview

Medical polymers are core materials in the healthcare field, being the functionality aspects of devices, implants, disposables, and packaging. Medical polymers benefit from the most important characteristics, such as biocompatibility, flexibility, sterilizability, and chemical resistance. Medical Polymers have changed from basic plastics to engineered & specialty compounds, which have substantial avenues of applications specifically in surgical instruments, orthopaedic implants, drug delivery systems, and prostheses. The increased desire for more "safer, lighter, and less expensive" medical devices warrants the usage of more advanced polymers, especially in countries with growing elderly populations in need of advanced medical care and with dynamic healthcare systems such as the U.S.A., Germany, China, Japan, and India.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Medical Polymer Manufacturers continue to innovate with biodegradable, antimicrobial, and high-performance polymers in an attempt to specify healthcare needs and regulatory requirements. The market continues to see increasing usage of polyethylene, polypropylene, PVC, polystyrene, and high-performance thermoplastics, i.e., PEEK, PEBA, among others, in medical applications.

The report includes a detailed analysis related to the major growth drivers, including advancements in polymer technology, rising demand for minimally invasive surgical procedures, and the global trend towards home healthcare. The report includes an analysis of the market by polymer type, applications, Manufacturing Technology, and end-user. The primary participants in the medical polymer industry include BASF SE, Evonik Industries AG, Celanese Corporation, SABIC, and Arkema S.A., all known for their R&D investments and products developed for the healthcare industry. The report discusses how changes in regulations, sustainability, and increased healthcare spending are influencing the development of the medical polymer marketplace worldwide.

Medical Polymer Market Dynamics

Increasing Demand for Advanced Medical Devices and Implants to Boost Market Growth

The accelerating advancements in the medical device and healthcare sectors are significantly boosting the demand for medical polymers. manufacturers focus on producing lightweight, biocompatible, and high-performance materials for applications such as surgical instruments, prosthetics, orthopedic implants, catheters, and dental devices has made medical polymers an indispensable choice. Their versatility in medical tubing, packaging for pharmaceuticals, and drug delivery systems is driving adoption across hospitals, clinics, and research laboratories. The increasing usage of minimally invasive surgeries and diagnostic equipment, combined with the trend toward patient-specific solutions, is boosting the Medical Polymer Market Growth.

High Production Costs and Stringent Regulatory Approvals to Restrain Market Growth

The Medical Polymer Market faces challenges due to the high production and processing costs associated with specialized grades like bioresorbable polymers, silicone elastomers, and engineering thermoplastics. Strict regulatory requirements from bodies such as the FDA and EMA, along with lengthy clinical trial timelines, can slow product commercialization. the need for specialized polymer processing equipment and skilled technical expertise may limit adoption among smaller medical device manufacturers. Competition from alternative materials, including advanced metals and ceramics in certain implantable applications, could also hinder faster Medical Polymer Market penetration.

Biodegradable and Smart Polymer Innovations Unlock New Opportunities in the Medical Polymer Market

Growing research in biodegradable polymers, antimicrobial coatings, and shape-memory materials is opening new avenues for innovation in the Medical Polymer Market. These materials hold strong potential in next-generation wound care products, tissue engineering scaffolds, and controlled drug release systems. The increasing demand for customized 3D-printed medical devices and the expansion of telemedicine-driven home healthcare solutions are further enhancing market opportunities. Technological innovations aimed at enhancing polymer strength, sterilization resistance, and patient comfort, drives Medical Polymer Market growth.

Medical Polymer Market Segment Analysis

By Product, the Medical Polymer Market is categorized into Fiber and Resin, Biodegradable Medical Polymer, and Medical Elastomers. The Fibers and Resins Segment held the largest market share in 2024. Their dominance in the industry is driven by a strong combination of versatility, affordability, and high performance. These materials serve as the workhorses of the market, finding essential applications in sutures, catheters, syringes, and prosthetics, leveraging the strength, flexibility, and biocompatibility inherent in fibers and resins such as polyethylene and polypropylene. Their cost-effectiveness positions them as champions when compared to traditional materials, making them accessible to a broader spectrum of healthcare providers and patients.

The "Biodegradable Medical Polymers" segment is noteworthy for its eco-friendly nature, gaining traction in response to the growing emphasis on sustainability. Medical Elastomers, with their flexibility and resilience, find applications in products like catheters and surgical gloves. Overall, the Fibres and Resins segment's dominance is attributed to its versatility, durability, and continuous innovations, making it a key driver in the evolving landscape of the Medical Polymer Market. The “other” segments, such as Medical Elastomers and Biodegradable Polymers, exhibit promising growth; Fibres & Resins steadfastly remain the bedrock of the Medical Polymer Market. Their affordability, versatility, and perpetual innovation secure their dominant position for years to come, defining the industry's narrative.

By Manufacturing Technology, By Manufacturing Technology in 2024, the Blow Fill Seal segment dominated the Medical Polymer Market and is expected to hold the largest market share over the forecast period, driven by its efficiency in producing sterile, single-use containers for pharmaceuticals. The Injection Molding segment held a strong share, driven by demand for precise, scalable production of syringes, surgical tools, and diagnostic devices. Extrusion Tubing is growing steadily, supported by rising needs for medical-grade tubing in catheters, IV sets, and dialysis systems. Compression Molding remains important for durable components such as orthopedic implants, while the other segment, including 3D printing and rotational molding, caters to niche, customized applications.

Medical Polymer Market Regional Analysis

North America held the largest market share in 2024 and is expected to continue throughout the forecast period, supported by advanced healthcare infrastructure, significant R&D investments, and a strong presence of leading medical device manufacturers. The region’s high adoption of innovative medical technologies, coupled with favorable regulatory frameworks, has accelerated demand for medical-grade polymers in applications such as implants, drug delivery systems, and diagnostic equipment. Europe followed closely, driven by a robust pharmaceutical industry, strong manufacturing capabilities, and a growing focus on sustainable and biocompatible polymer solutions.

Asia Pacific emerged as the fastest-growing region, driven by rapid industrialization, expanding healthcare infrastructure, and rising demand for cost-effective medical devices in countries like China, India, and Japan. The Middle East and Africa showed steady growth, supported by improving healthcare facilities and increasing investment in advanced medical solutions. South America experienced growth, driven by growing awareness of advanced medical technologies and the gradual modernization of healthcare systems in markets such as Brazil and Argentina.

Medical Polymer Market Competitive Landscape

The Medical Polymer Market is competitive and relies on innovation regarding biocompatible materials, regulatory compliance, and in meeting the increasing demand for weight-reduced and durable medical parts. Players such as BASF SE (Germany) and Evonik Industries AG (Germany) have an established market with solid supply chains and R&D organizations. For example, BASF SE reported roughly USD 410 million dollars revenue from healthcare polymers in 2024, on the back of the engineering plastics segment associated with diagnostics and drug delivery. Evonik Industries reported approximately USD 385 million revenue in 2024 from their healthcare sector, representing 17% growth with the largest segment growth among biodegradable and high-performance polymers for surgical and orthopedic applications. Both have begun investing in sustainable and AI-optimized material technologies to be prepared for the changing needs of the healthcare sector, while maintaining their leadership position as healthcare advances rapidly.

Medical Polymer Market Trends

• Increasing Demand for Biodegradable and Biocompatible Polymers

There has been a strong movement toward materials that are safe for internal use and have the potential to have a natural degradation pattern in the human body, especially with implants and drug delivery systems.

• Miniaturization and Lightweight Designs

Manufacturers of medical devices are seeking polymers that enable compact and lightweight design without sacrificing strength, especially in portable and wearable medical devices.

• The Rise of Home Healthcare/Wearable Devices

The growing adoption of home-based healthcare and wearable monitoring devices is boosting demand for flexible, durable, and biocompatible medical polymers. These materials are essential for producing lightweight, comfortable, and long-lasting components in devices like glucose monitors, infusion pumps, and portable diagnostics. With the shift toward remote care and device miniaturization, advanced polymers offering high performance in compact designs are becoming increasingly important, creating new growth opportunities for manufacturers.

Medical Polymer Market Recent Development

• January 2025: Pharmapack Paris, U.S.-based Avient showcased its Mevopur bio-based healthcare colorants and functional additives, including white/black PCR plate formulations optimized for fluorescence diagnostics, emphasizing performance, compliance, and sustainability.

• In May 2024, Eastman Chemical Company demonstrated a strategic push in the Medical Polymer Market by collaborating with Lubrizol to deliver a breakthrough in sustainable multi-material adhesion. Utilizing Tritan Renew and ESTANE ECO, the partnership yielded a remarkable 124% increase in TPE over molding adhesion strength, reinforcing Eastman’s commitment to innovation in sustainable materials tailored for complex medical device applications.

Medical Polymer Industry Ecosystem:

Medical Polymer Market Scope: Inquire before buying

| Global Medical Polymer Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 25 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 8.5% | Market Size in 2032: | USD 48.02 Bn. |

| Segments Covered: | by Product Type | Fibres and Resins PVC PP PE Others Medical Elastomers Styrene Block Copolymer Rubber latex Others Biodegradable Medical Polymers Polylactic Acid (PLA) Polyhydroxyalkanoate (PHA) Others |

|

| by Manufacturing Technology | Blow Fill Seal Injection Molding Extrusion Tubing Compression Molding Others |

||

| by Application | Medical Device Packaging Medical Components Orthopedic Soft Goods Cleanroom Supplies BioPharm Devices Others |

||

| by End-User | Hospitals & Clinics Pharmaceutical & Biotechnology Companies Diagnostic Centers |

||

Global Medical Polymer Market, by Region

North America (United States, Canada, Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Philippines,

Thailand, Vietnam, Rest of Asia Pacific)

Middle East and Africa (MEA) (South Africa, GCC, Nigeria, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Rest of South America)

Medical Polymer Market Key Players

North America

1. Eastman Chemical Company (USA)

2. The Dow Chemical Company (USA)

3. Formosa Plastics Corporation USA (USA)

4. Celanese Corporation (USA)

5. DuPont (USA)

6. Lubrizol Corporation (USA)

7. ExxonMobil (USA)

8. Celanese (USA)

9. Kraton Performance Polymers (USA)

Europe

1. Evonik Industries AG (Germany)

2. Arkema SA (France)

3. BASF SE (Germany)

4. Covestro AG (Germany)

5. DSM N.V. (Netherlands)

6. Solvay S.A (Belgium)

7. Bayer (Germany)

8. Borealis (Austria)

9. Victrex Plc. (United Kingdom)

10. DSM (Netherlands)

Asia Pacific

1. Tianjin Plastics Research Institute Co. Ltd (China)

2. Huizhou Foryou Medical Devices (China)

Frequently Asked Questions:

1] What is the growth rate of the Global Medical Polymer Market?

Ans. The Global Medical Polymer Market is growing at a significant rate of 8.5 % during the forecast period.

2] Which region is expected to dominate the Global Medical Polymer Market?

Ans. North America held a significant share in the global Medical Polymer market, primarily due to advanced healthcare infrastructure, a higher prevalence of respiratory diseases, and a well-established market for medical devices.

3] What is the expected Global Medical Polymer Market size by 2032?

Ans. The Medical Polymer Market size is expected to reach USD 48.02 Bn by 2032.

4] Which are the top players in the Global Medical Polymer Market?

Ans. The major top players in the Global Medical Polymer Market are Eastman Chemical Company (USA), The Dow Chemical Company (USA), Formosa Plastics Corporation USA (USA), Celanese Corporation (USA), DuPont (USA), and Lubrizol Corporation (USA).

5] What was the market size of the Global Medical Polymer Market in 2024?

Ans. The market size of the Global Medical Polymer Market in 2024 was valued at USD 25 Bn.

6] Which country held the largest Global Medical Polymer Market share in 2024?

Ans. The United States held the largest Medical Polymer Market share in 2024.