Luxury Apparels Market Size by Product, Material Type, End User, Distribution Channel, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

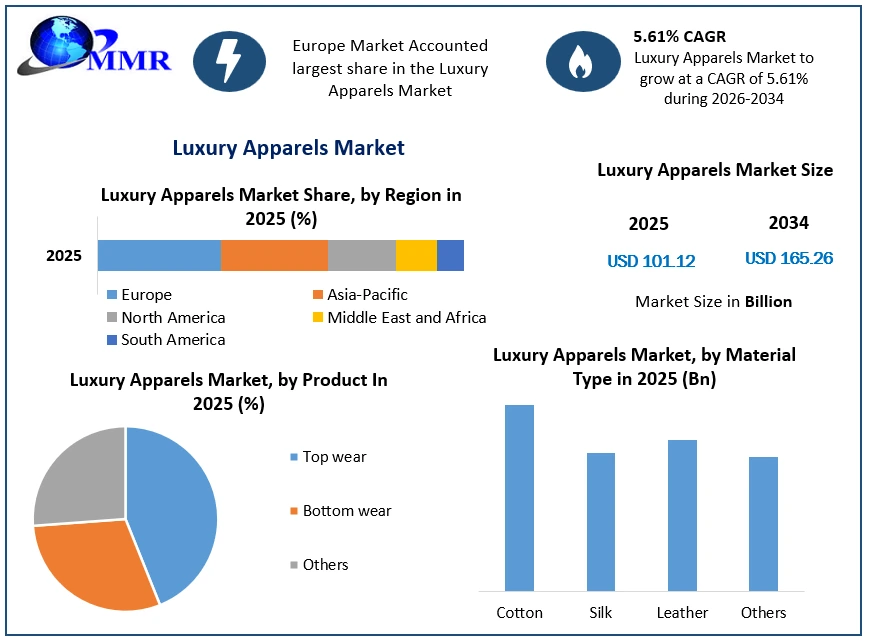

The Global Luxury Apparels Market size was valued at USD 101.12 Bn. in 2025, and the total Global Luxury Apparels Market revenue is expected to grow by 5.61% from 2026 to 2034, reaching nearly USD 165.26 Bn.

Global Luxury Apparels Market Overview

Luxury apparel refers to high-end clothing and accessories that are crafted from premium materials and are produced by prestigious fashion designers or luxury brands. These items in the Luxury Apparels Market are typically characterized by their exceptional quality, exquisite craftsmanship, meticulous attention to detail, and often their exclusive or limited availability. Luxury apparel commands premium prices due to the use of luxurious materials such as fine fabrics, rare leathers, and precious metals, as well as the brand's reputation and prestige. Examples of luxury apparel include designer clothing and clothing accessories that are made “ready-to-wear”.

Luxury Apparels Market Analysis from 2025 to 2034

To know about the Research Methodology :- Request Free Sample Report

The rise of disposable incomes and aspirational consumption, along with growing brand awareness, especially among millennials and Gen Z consumers, in the emerging Luxury Apparels Market. Digital transformation and omnichannel approaches to reaching customers enable luxury apparel to go into unsuspected market areas and reach a much larger global audience than before. There are new demands for personalized and ethical sourcing of garments, sustainable fashion, and innovative materials and transparent supply chains provide opportunities with new potential consumers.

Europe is the leader in the luxury apparel market, largely due to the presence of fashion capitals like Paris, Milan and London (as well as many heritage brands). The Asia-Pacific is the fastest growing region in terms of growth opportunity, specifically China, Japan and South Korea, driven by affluence growth and the increasing use of digital technologies. The competitive landscape is highly competitive, with global players such as LVMH (France) Gucci (Italy) and Prada (Italy), while new entrants are digitally first luxury players. Regarding luxury apparel, competitive offerings are based on craftsmanship, innovation, cultural, and sustainability leadership.

Global Luxury Apparels Market Dynamics

Prestige and Innovation to Drive Luxury Apparel Market Growth

Consumer perceptions of status and prestige are paramount drivers shaping purchasing behaviors. High-end brands evoke a sense of exclusivity and social status, appealing to consumers who seek to differentiate themselves and signal their wealth or sophistication. Luxury apparel serves as a form of conspicuous consumption, where owning and displaying items from prestigious brands becomes a means of expressing one's social standing and identity. In the Luxury Apparel Market, consumers are prepared to pay premium prices not only for superior quality and craftsmanship but also for the brand’s symbolic value and prestige, which convey exclusivity, social status, and a reflection of personal identity. Marketing strategies emphasizing the aspirational lifestyle and exclusivity enhance the allure of luxury apparel, driving demand among affluent consumers who prioritize luxury experiences and products.

Luxury brands continuously strive to differentiate themselves through cutting-edge design, innovative materials, and craftsmanship. Unique design elements, exclusive collaborations, and limited-edition collections captivate consumers seeking novelty and individuality. Innovation extends beyond aesthetics to include sustainability initiatives, technological advancements, and personalized shopping experiences. By pushing the boundaries of creativity and setting new trends, luxury apparel brands maintain their allure and relevance in a competitive Luxury Apparels Market landscape. Investment in research and development, along with partnerships with renowned designers and artisans, enables luxury brands to deliver products that resonate with discerning consumers who value authenticity, creativity, and superior quality. Product development in the fashion industry is an essential part of the overall manufacturing process, and luxury apparels manufacturers continuously improve their product designs.

Economic Disparities Expected to Restrain the Luxury Apparel Market

The Luxury Apparel Market relies heavily on affluent and high-net-worth individuals who possess significant disposable income to purchase premium clothing and accessories. However, widening income inequality is creating a structural challenge for market expansion. While the wealthiest segment continues to grow richer, the overall middle-class population, traditionally a secondary target for aspirational luxury purchases, is shrinking in many regions.

This economic polarization reduces the number of potential buyers who can afford high-end fashion, leading to a contraction in the overall consumer base. In emerging economies, where luxury brands once saw untapped growth potential, rising inflation, currency fluctuations, and uneven income distribution have limited purchasing power among broader populations. Even in developed markets, stagnant wage growth for middle-income households, coupled with increasing living costs, has led to prioritization of essentials over discretionary luxury spending.

Online Customization and Ethical Practices to Create Opportunities in the Luxury Apparel Market

The online customization and personalization present a significant opportunity for brands to enhance customer engagement and loyalty. With advancements in technology, such as virtual fitting rooms and AI-driven styling algorithms, brands offer bespoke experiences tailored to individual preferences and measurements. In the Luxury Apparel Market, such personalization enhances the overall luxury shopping experience, reinforcing brand exclusivity while empowering customers to showcase their individuality through bespoke, custom-designed garments. Online customization enables luxury brands to gather valuable data on consumer preferences, which informs product development and marketing strategies. By leveraging customer insights, brands create exclusive offerings that resonate with their target audience, driving sales and fostering brand loyalty.

The growing consumer awareness and concern for environmental and social issues, there is a rising demand for responsibly sourced and eco-friendly luxury products. This presents a significant opportunity in the Luxury Apparels Market that lies in embracing sustainability and ethical practices. Luxury brands have the opportunity to lead the industry in adopting sustainable practices across the supply chain, from sourcing raw materials to manufacturing and distribution. The prioritizing sustainable materials, such as organic cotton, recycled polyester, and cruelty-free alternatives, luxury apparel brands reduce their environmental footprint and appeal to eco-conscious consumers. Implementing ethical labor practices and transparent supply chains enhances brand reputation and improves trust among consumers.

Global Luxury Apparels Market Segment Analysis

Based on the product, the topwear segment held the largest Luxury Apparels Market share in 2025. The topwear segment encompasses shirts, blouses, and jackets, which command attention and are highly visible. Versatile and easily paired with various bottoms, accessories, and footwear, topwear offers diverse styling possibilities and applications, making it a cornerstone of luxury fashion. Luxury brands excel in offering a plethora of topwear options suitable for different climates, ensuring year-round appeal and accessibility. Luxury brands are innovating in materials, introducing technical fabrics and blends to enhance the performance and comfort of bottomwear. This appeals to fashion-forward consumers seeking cutting-edge style. The adaptability of luxury bottomwear allows for seamless transitions from casual to semi-formal settings, making it a coveted addition to upscale wardrobes. Luxury brands continue to explore new materials and design concepts, and bottomwear emerges as a significant category shaping the future of luxury apparel.

Based on the distribution channel, the offline segment dominated the largest Luxury Apparels Market share in 2025. The segment growth is driven by the premium pricing and superior quality of luxury products. Consumers often prefer physical inspections for factors like material and fit before committing to high-value purchases, driving the preference for offline channels. The multi-branded shops and specialist stores offer added benefits such as free alterations, enhancing the appeal of offline shopping. However, the online retail channel is poised for rapid growth, projected to achieve the fastest compound annual growth rate (CAGR) in the forecast period. Both multi-brand e-retailers and brand-owned online stores engage with consumers, offering convenience and accessibility. Online platforms provide access to a wider range of luxury apparel, which not be readily available in local shops, thus catering to a broader audience, including international customers. The convenience of online shopping appeals to busy consumers, driving the expansion of the online retail segment in the luxury apparels Industry.

Global Luxury Apparels Market Regional Insights

Europe held the largest Luxury Apparels Market share in 2025, with prominent countries like Germany, the U.K., and France leading the way. Renowned for its allure as a tourist destination, Europe attracts millions of global travelers annually. Among them, business magnates and affluent tourists indulge in lavish clothing purchases, contributing to robust product sales. The region's allure is further enhanced by innovative retail concepts and business models, driving continuous growth.

Europe is home to some of the world’s biggest and most renowned apparel companies and has a large apparel sector that performs well. the EU is the world’s largest importer of apparel and textiles. The European market has some key differences with the USA, the second most popular destination for apparel exports. It is more diverse than the USA market, and suppliers offer a higher level of service and flexibility. The US market, on the other hand, is relatively homogenous and follows more traditional, less direct retail and distribution models (wholesale and private label). It is highly price-driven and volume-driven. Many US buyers have offices located in production countries and source and nominate their raw materials. Manufacturing is done on a CMT (cut, make and trim) basis, which leaves little room for suppliers to add value.

Global Luxury Apparels Market Competitive Landscape

The global Luxury Apparels Market is highly competitive and controlled by several multinational corporations(MNCs) that control multiple brands. These key players sell their products at a premium price and differentiate their products based on brand history, quality design, exclusivity, novelty, and sustainability. Luxury Apparels Leading companies LVMH (France) and Kering(France) can accommodate several markets with a vast and diversified luxury portfolio and retail replenishment in both the emerging markets and development markets. They spent a lot of money on endorsement partnerships with celebrities, on some of the leading fashion weeks, digital campaigns, and reproductive distribution in some cases with a retail footprint.

Prada (Italy) and Chanel (France) sustain a strong market presence by focusing on artisanal craftsmanship, enduring design, and growing their e-commerce abilities. Brands like Ralph Lauren (USA) and Burberry (UK) are benefiting from digital innovation and premium casualwear trends appeal to younger demographics. Asian players such as Shandong Ruyi (China) are gaining global relevance through acquisitions and rising domestic demand. Omnichannel continues to provide new dimensions to staying competitive and sustainable sourcing aligns with emerging consumer expectations regarding the consumption of luxury goods, with their lifestyle perspectives.

Global Luxury Apparels Market Recent Development

• Capri Holdings & Prada S.p.A. (USA), On April 10, 2025, Capri Holdings entered into a definitive agreement with Prada S.p.A. to sell the luxury fashion brand Versace for USD 1.375 billion in cash. This strategic acquisition strengthens Prada’s luxury portfolio and positions the group for expansion into new, high-growth markets. The deal also reflects Prada’s ambition to diversify its brand offerings while enhancing global competitiveness. For Capri Holdings, the sale provides substantial liquidity and strategic flexibility to focus on its other core brands.

• Prada Group & UNESCO (Italy): On June 9, 2025, Prada Group partnered with UNESCO to launch the SEA BEYOND Multi-Partner Trust Fund, committing an initial USD 2.32 million to support global ocean preservation initiatives. This partnership expands Prada’s sustainability leadership by promoting marine conservation, environmental education, and cross-sector collaboration. The program leverages public-private engagement to address pressing ecological challenges while strengthening Prada’s brand identity as a responsible luxury leader. Through SEA BEYOND, Prada aims to foster awareness among future generations about ocean health, aligning its business strategy with environmental stewardship and the United Nations’ Sustainable Development Goals. This initiative reflects the growing demand for eco-conscious luxury brands.

• LVMH (France): On May 22, 2024, LVMH showcased its innovation leadership at VivaTech 2024 by unveiling the Dream Garden pavilion. This immersive space highlighted advancements in artificial intelligence (AI), generative AI (genAI), sustainable craftsmanship, and logistics optimization. By combining cutting-edge technology with artisanal expertise, LVMH emphasized its commitment to “digital sustainability,” ensuring luxury remains innovative and environmentally responsible. The initiative reflects LVMH’s broader strategy of integrating technology to enhance customer experience, streamline operations, and strengthen brand equity.

• Burberry (UK), On November 12, 2024, Burberry introduced its first augmented reality (AR) virtual scarf try-on, developed in collaboration with AR partner Wanna. This innovation allows customers to virtually try on scarves both online and in-store, enhancing digital engagement and reducing purchase hesitation. By integrating immersive technology into its retail experience, Burberry aims to increase e-commerce conversion rates while maintaining its personalized touch. The initiative reflects Burberry’s strategy to blend tradition with digital innovation, appealing to younger, tech-savvy consumers.

• Chanel (France): In 2024, Chanel expanded its Culture Fund to support cultural innovators worldwide, strengthening its role as a patron of the arts. This expansion includes partnerships with institutions such as the Leeum Museum in Seoul, among others, fostering cross-cultural creative exchange. The Culture Fund supports artists, curators, and cultural organizations, ensuring that artistic innovation continues to thrive globally. By investing in the arts, Chanel reinforces its brand narrative rooted in creativity, heritage, and cultural influence.

Global Luxury Apparels Market Trends

| Trend | Description | Example | Impact Area |

| Immersive Digital Luxury Experiences | Luxury brands are investing in AR, VR, and metaverse platforms to enhance digital engagement. | Burberry launched virtual scarf try-on and NFTs on Roblox (2024–2025). | Brand engagement, Gen Z targeting, and digital retail growth |

| Art & Culture Integration in Branding | Brands are aligning with cultural institutions and artists to elevate brand prestige and authenticity. | Chanel expanded its Culture Fund with MCA Chicago & Leeum Museum (2024). | Cultural capital, market prestige, global collaboration |

| Supplier Transparency Forums | Focus on ethical sourcing and traceable supply chains with direct supplier engagement. | Chanel hosted a global supplier forum in Dubai to promote traceability (2024). | ESG compliance, ethical luxury, supply chain governance |

Luxury Apparels Market Scope: Inquiry Before Buying

| Global Luxury Apparels Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 101.12 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 5.61% | Market Size in 2034: | USD 165.26 Bn. |

| Segments Covered: | by Product | Top wear Bottom wear Others |

|

| by Material Type | Cotton Silk Leather Others |

||

| by End User | Men Women |

||

| by Distribution Channel | Children Offline Online |

||

Global Luxury Apparels Market, by Region

North America (United States, Canada, Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Philippines, Thailand, Vietnam, Rest of Asia Pacific)

Middle East and Africa (MEA) (South Africa, GCC, Nigeria, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Rest of South America)

Global Luxury Apparels Market, Key Players

North America

1. Ralph Lauren (USA)

2. PVH Corp. (USA)

3. Tapestry Inc. (USA)

4. Capri Holdings (USA)

5. Canada Goose (Canada)

Europe

1. LVMH (France)

2. Kering (France)

3. Chanel (France)

4. Prada (Italy)

5. Armani (Italy)

6. Burberry (UK)

7. Hermès (France)

8. Hugo Boss (Germany)

9. Dolce & Gabbana (Italy)

Asia-Pacific

1. Shandong Ruyi (China)

2. E-Land Group (South Korea)

3. Fast Retailing – Theory (Japan)

4. Li-Ning (China)

5. Shanghai Tang (Hong Kong)

6. MCM Worldwide (South Korea)

Middle East & Africa

1. Chalhoub Group (UAE)

2. Al Tayer Group (UAE)

3. Majid Al Futtaim Fashion (UAE)

4. Rivoli Group (UAE)

5. Boutique 1 (UAE)

6. Jashanmal Group (UAE)

Frequently Asked Questions

1. Which region has the largest share in the Global Luxury Apparels Market?

Ans: Europe held the largest Luxury Apparels Market Share in 2025.

2. What is the growth rate of the Global Luxury Apparels Market?

Ans: The Global Luxury Apparels Market is expected to grow at a CAGR of 5.61% during the forecast period 2026-2034.

3. What is the scope of the Global Luxury Apparels Market report?

Ans: The Global Luxury Apparels Market report helps with the PESTEL, Porter's, Recommendations for Investors and leaders, and market estimation for the forecast period.

4. Who are the key players in the Global Luxury Apparels Market?

Ans: The key players in the Global Luxury Apparels Market are LVMH (France), Kering (France), Chanel (France), Prada (Italy), Armani (Italy), Burberry (UK), and Hermès (France).

5. What is the study period of this market?

Ans: The Global Luxury Apparels Market is studied from 2025 to 2034.