HVAC Systems Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2034

Overview

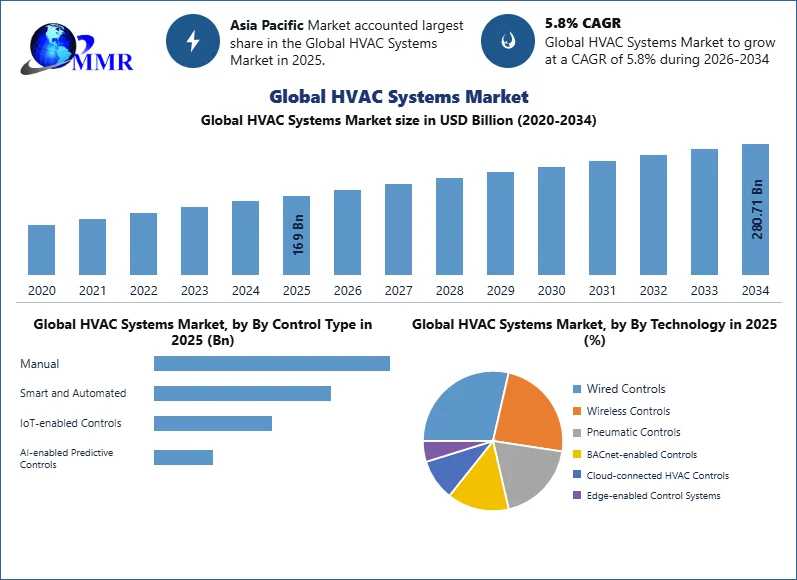

The HVAC Systems Market size was valued at USD 169 Billion in 2025 and the total HVAC Systems revenue is expected to grow at a CAGR of 5.8% from 2025 to 2034, reaching nearly USD 280.71 Billion by 2034.

HVAC Systems Market Overview:

HVAC stands for heating and cooling both residential and commercial buildings, as well as the many systems used to move air between indoor and outdoor locations. They are the systems that keep you warm and comfortable in the winter and cool and refreshing in the summer. Heat Pumps, Furnaces, Boilers, and Unitary Heaters are the types of heating equipment. Humidifiers, Dehumidifiers, Air Purifiers, Air Filters, Ventilation Fans, and Air Handling Units are the types of ventilation equipment. Room Air Conditioners, Unitary Air Conditioners, Chillers, Coolers, Cooling Towers, and VRF Systems are the types of cooling Equipment.

The value of the Global HVAC Systems Market was estimated at USD 169 Billion in 2025, with an expected value of USD 280.71 Billion by 2034, representing a CAGR of 5.8% during the forecast period. The main factors that drive the growth of the market include the increasing urbanization, rising construction activities, rising demand for energy efficient HVAC systems and increasing adoption of smart building technology. The development of Internet of Things based HVAC systems, artificial intelligence based predictive maintenance, wireless controls and integrated Building Management Systems (BMS) is revolutionizing the industry through enhanced efficiency and lower energy usage. The global HVAC Systems market is gaining momentum from increased focus on energy efficiency standards, adoption of lower GWP refrigerants and green building initiatives. The Asia-Pacific region is leading the market due to rapid infrastructural development and rising construction activities, whereas North America and Europe regions are experiencing robust growth due to building retrofits, decarbonization and upgrading commercial and industrial buildings. High competitive rivalry prevails in the market and companies strive for innovations and digitalization of products, partnership programs and building smart HVAC ecosystems.

To know about the Research Methodology :- Request Free Sample Report

HVAC Systems Market Dynamics:

The launch of new technologically enhanced products that are energy-efficient and can be remotely accessed is driving the growth of the global HVAC systems market. Moreover, the global market is expected to be driven by the usage of natural refrigerants such as CO2, as well as increased initiatives by governments throughout the world to promote energy-efficient products. A paradigm shift toward the use of energy-efficient air conditioners that minimize prices and power waste is expected to maintain HVAC demand.

The demand for HVAC systems has increased as customer’s preferences for comfort have shifted. Companies are manufacturing products that not only meet the customer's comfort demands, but also provide a number of additional benefits. IoT-enabled heating and cooling systems allow for real-time monitoring of the system's functionality and condition. These HVAC systems also notify consumers or management when a system fails, exhibits unexpected behaviour, or is nearing the end of its maintenance cycle, lowering repair costs.

One of the major factors driving the rising adoption of heating and cooling technology is climate change. This is due to the uncertainty of weather and rising temperatures, many consumers see HVAC equipment as a good investment. Furthermore, HVAC systems enhance the aesthetic value of both residential and commercial buildings. Companies are manufacturing the products that are attractive to the eye and provide a variety of design possibilities. During the forecast period, increased product demand is expected as a result of improved designs and changing client preferences. These are the key drivers that are expected to boost the growth of the global HVAC Systems market during the forecast period 2025-2034.

HVAC Systems Market Segment Analysis:

Based on the Cooling Equipment, the market is segmented into Room Air Conditioners, Unitary Air Conditioners, Chillers, Coolers, Cooling Towers, and VRF Systems. VRF Systems segment is expected to hold the largest market share of xx% by 2034. Many commercial buildings, from small stores and cafes to major office buildings and public places, use VRF systems. VRF zoning ensures that energy is only used to cool or heat occupied offices. This is due to the VRF systems have silent indoor units and can maintain exact temperature control, they provide the most comfortable and productive working environment. These are the key benefits that are expected to boost the growth of the VRF Systems segment in the global market during the forecast period 2025-2034.

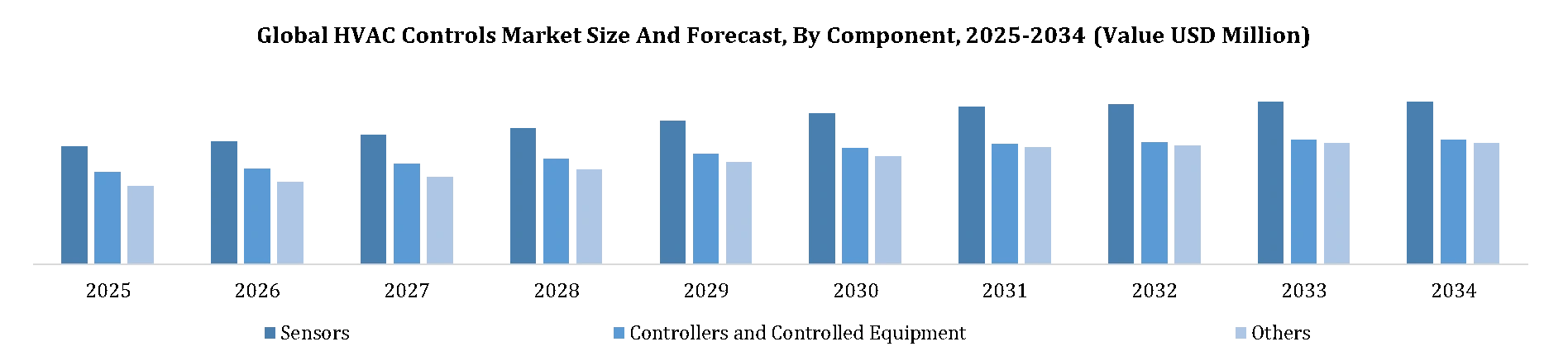

The Components are the basis for the segmentation of the market into Sensors, Controllers and Controlled Equipment, Actuators, Smart Vents, Thermostats, and Others. The Controllers and Controlled Equipment segment is projected to dominate the market with the largest market share of xx%. The dominance of this segment is attributed to its importance in ensuring proper monitoring, control, and optimization of HVAC systems performance in commercial, industrial, and residential buildings. Components such as control valves, programmable controllers, VAV controllers, FCU controllers, AHU controllers, and valve actuators offer accurate regulation of airflow, temperature, and pressures along with energy efficiency and occupant comfort. Increasing popularity of smart building technology, increased adoption of BAS, strict energy efficiency norms, and growing demand for intelligent HVAC control solutions will drive the growth of the Controllers and Controlled Equipment segment.

On the basis of the Control Type, the market is categorized as Manual, Smart and Automated, Internet of Things (IoT) Controlled, and Artificial Intelligence (AI) Controlled Predictive Controls. Smart and Automated Control segment holds the maximum market share of xx% in 2034. This segment is experiencing high growth because of the increasing use of intelligent HVAC control systems which help in saving energy, improving occupant comfort level, and reducing operating costs. Real-time monitoring, automatic temperature adjustments, remote system control, and integration with BMS and smart building software solutions can be achieved through smart and automated control technology. Increasing investment in energy-efficient infrastructure, strict energy efficiency regulations in buildings, and rising need for smart and automated commercial buildings are likely to drive the growth of the Smart and Automated Control segment during the forecast period 2025–2034.

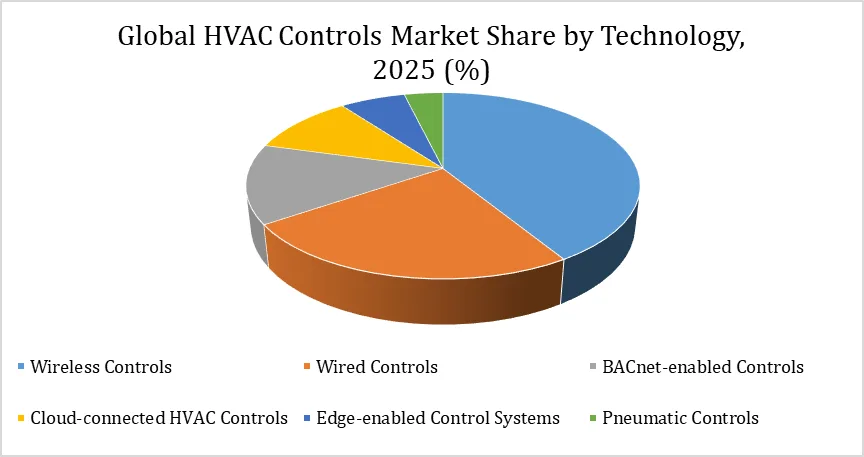

According to the Technology, the market can be categorized into Wired Controls, Wireless Controls, Pneumatic Controls, BACnet-compatible Controls, Cloud Connected HVAC Controls, and Edge-enabled Control Systems. Wireless Controls will dominate the segment with the market share of xx%. The Wireless Controls segment is being driven by the increased use of smart buildings, wireless communication systems, and IoT-based HVAC systems. Wireless control systems provide easier installations, lower costs of infrastructure, flexibility, and better integration with the building management systems, which allows users to monitor HVAC equipment remotely and in real time. Increased need for energy efficient buildings, predictive maintenance, and scalable automation solutions are expected to drive the demand for wireless control systems. Furthermore, developments in cloud computing, IoT connections, and intelligent automation are aiding the growth of the Wireless Controls segment over the forecast period of 2025-2034.

As per the System, the market segments include Temperature Control Systems, Ventilation Control Systems, Humidity Control Systems, Integrated Control Systems, Airflow & Pressure Control Systems, Hydronic Control Systems, and Data Center Cooling Control Systems. The Integrated Control Systems segment is estimated to be the largest market, holding xx% market share in 2034. The segment will experience growth due to the rising need for centralized HVAC systems that ensure efficient energy consumption, improved system operations, and increased occupant comfort in various types of buildings such as commercial, industrial, health care, and institutions. This segment provides an integrated solution for temperature, ventilation, humidity, airflow, and pressure controls through the use of a single BMS system, allowing real-time monitoring and maintenance of the entire building. The increasing trend towards smart buildings, strict laws for energy efficiency, and higher investments in intelligent building automation systems are some of the major factors fueling the growth of this segment from 2025 to 2034.

Based on the End User, the market is segmented into Residential, Commercial, and Industrial. Commercial segment is expected to hold the largest market share of xx% by 2034. The segment is driven by the increasing deployment of advanced HVAC control systems across office buildings, retail spaces, educational institutions, healthcare facilities, hospitals, commercial complexes, and smart buildings. Commercial facilities require intelligent HVAC controls to optimize energy consumption, maintain indoor air quality, enhance occupant comfort, and comply with stringent building energy regulations. The growing adoption of Building Management Systems (BMS), IoT-enabled HVAC solutions, and smart building technologies is further accelerating demand for automated control systems in the commercial sector. Additionally, increasing investments in green buildings, energy-efficient infrastructure, and digital facility management are expected to drive the growth of the Commercial segment throughout the forecast period 2025–2034.

Global HVAC Systems Market Regional Insights:

Asia Pacific dominates the Global HVAC Systems market during the forecast period 2025-2034. Asia Pacific is expected to hold the largest market share of xx% by 2034. China, India, and Japan are the key countries that boost the growth of the HVAC systems market in the Asia Pacific region. This is due to the growing population and increasing construction activities in China, India, and Japan. These are the major factors that drive the growth of this region in the Global market during the forecast period 2025-2034.

North America and Europe are expected to grow rapidly at a CAGR of xx% and xx% during the forecast period 2025-2034. This is due to the region's thriving tourist and real estate industries. Subsidies and tax breaks are being offered by the governments of both regions to support the usage of energy-efficient systems. Due to this reasons, present customers are upgrading to new energy-efficient systems in addition to new developments.

The objective of the report is to present a comprehensive analysis of the Global HVAC Systems Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Global HVAC Systems Market dynamic, structure by analyzing the market segments and project the Global HVAC Systems Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Global HVAC Systems Market make the report investor’s guide.

Competitive Analysis HVAC Systems Market 2025

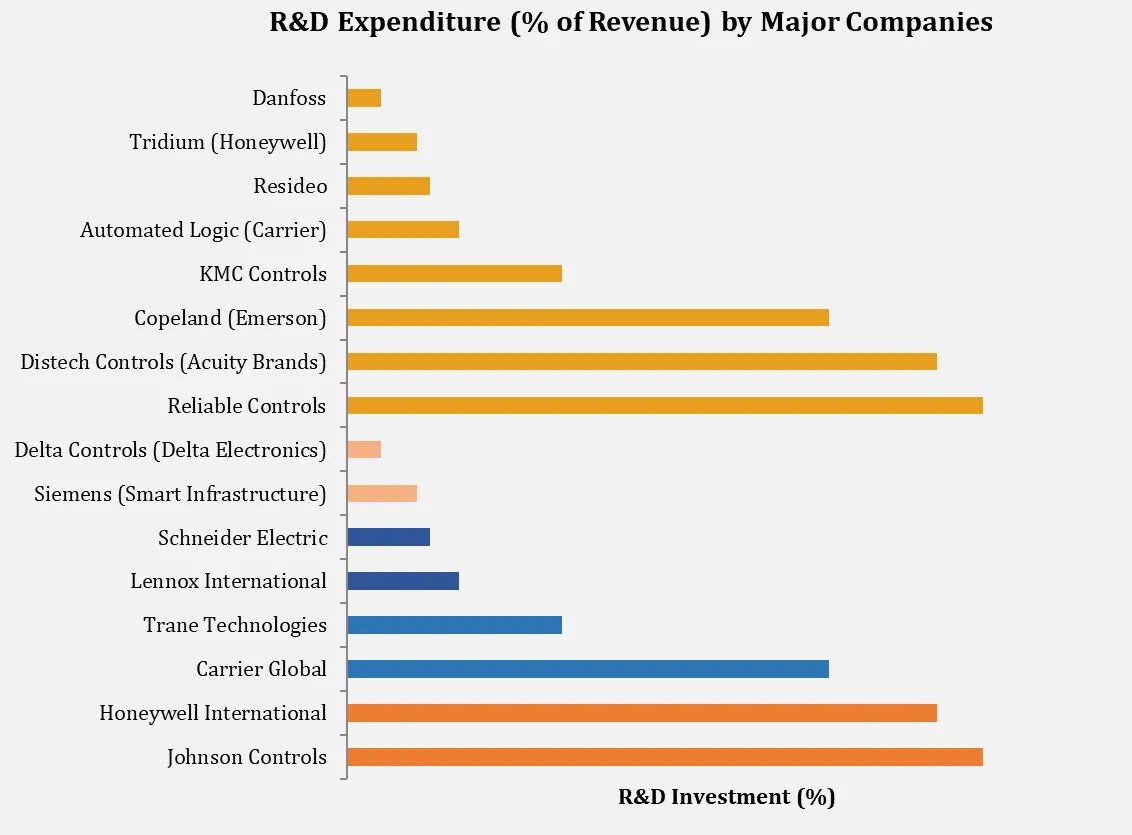

Competitive landscape of the HVAC Systems market can be described as highly competitive, where players are competing on the basis of energy efficiency, smart building technologies, and digitalization. The companies differentiate their products in terms of HVAC controls, internet of things (IoT) connected HVAC equipment, building management platforms based in the cloud, predictive maintenance systems, and use of low GWP refrigerants. Investments made are directed at decarbonization, electrification using heat pumps, data centers cooling systems, and Building Management Systems (BMS). These systems aim to provide optimized energy consumption along with improved comfort for the occupants of buildings.

Current developments within the strategic arena reinforce the trend towards digitalization and sustainability in HVAC products and services. Johnson Controls continues adding new elements to its OpenBlue digital ecosystem, such as connected building solutions based on artificial intelligence that incorporate predictive maintenance, remote diagnostics, and net-zero optimization features as well as streamlining its portfolio of commercial buildings by prioritizing smart and sustainable infrastructures. Carrier Global adds to its portfolio of climate solutions by acquiring Viessmann Climate Solutions, thereby increasing the range of heat pumps and energy transition services as well as investments in high-performance cooling equipment for AI-powered data centers. Trane Technologies moves forward with its innovations in electrified heating and thermal management systems and sustainable HVAC solutions in accordance with its decarbonization strategy. Honeywell is broadening its portfolio of connected buildings through its Honeywell Forge platform that provides for advanced analytics and building performance optimization. Schneider Electric and Siemens Smart Infrastructure are enhancing their interoperable building automation ecosystems through integration of HVAC control solutions with energy management and smart buildings platforms.

Global HVAC Systems Market Scope: Inquire before buying

| Global HVAC Systems Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 169Bn. |

| Forecast Period 2026 to 2032 CAGR: | 5.8% | Market Size in 2032: | USD 250.77 Bn. |

| Segments Covered: | By Component | Sensors Temperature Sensors Humidity Sensors Occupancy Sensors Pressure Sensors Flow Sensors Others Controllers and Controlled Equipment Controlled Equipment Smart Vents Controllers Thermostats Others |

|

| By Technology | Wired Controls Wireless Controls Pneumatic Controls BACnet-enabled Controls Cloud-connected HVAC Controls Edge-enabled Control Systems |

||

| by Cooling Equipment | Room Air Conditioners Unitary Air Conditioners Chillers Coolers Cooling Towers VRF Systems |

||

| by Implementation Type | New Construction Retrofit |

||

| By System | Temperature Control Systems Ventilation Control Systems Humidity Control Systems Integrated Control Systems Airflow & Pressure Control Systems Hydronic Control Systems Data Center Cooling Control Systems |

||

HVAC Systems Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

HVAC Systems Market, Key Players

- Honeywell International

- Belimo

- Vertiv

- Carrier Global

- Trane Technologies

- Lennox International

- Schneider Electric

- Siemens (Smart Infrastructure)

- Delta Controls

- Reliable Controls

- Distech Controls

- Copeland (Emerson)

- KMC Controls

- Automated Logic (Carrier)

- Resideo

- Tridium

- Danfoss

- Daikin Industries

- Mitsubishi Electric

- ABB

- Fr. Sauter AG

- Bosch Building Technologies (Bosch)

- Eaton

- Azbil Corporation

- Regin Controls

- OJ Electronics

- LG Electronics (HVAC Controls Division)

- Computrols

- Sontay

- Trend Controls (Honeywell)

- Emerson Electric

- Midea Building Technologies

- Swegon (Latour Industries)

- Systemair

- Priva

- Others

Frequently Asked Questions:

1] What segments are covered in Global Market report?

Ans. The segments covered in Global HVAC Systems Market report are based on Heating Equipment, Ventilation Equipment, Cooling Equipment, Implementation Type, and Application.

2] Which region is expected to hold the highest share in the Global Market?

Ans. Asia Pacific is expected to hold the highest share in the Global HVAC Systems Market.

3] Who are the top key players in the Global Market?

Ans. Daikin, United Technologies, Johnson Controls, Ingersoll-Rand, LG Electronics, and Electrolux are the top key players in the Global HVAC Systems Market.

4] Which segment holds the largest market share in the Global market by 2034?

Ans. VRF Systems segment hold the largest market share in the Global HVAC Systems market by 2032.

5] What is the market size of the Global HVAC Systems market by 2034?

Ans. The market size of the Global HVAC Systems market is USD 280.71 Bn. by 2034.

6] What was the market size of the Global HVAC Systems market in 2025?

Ans. The market size of the Global HVAC Systems market was worth USD 169 Bn. in 2025.