Glucose, Dextrose, and Maltodextrin Market Size by Product, Application, Form, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

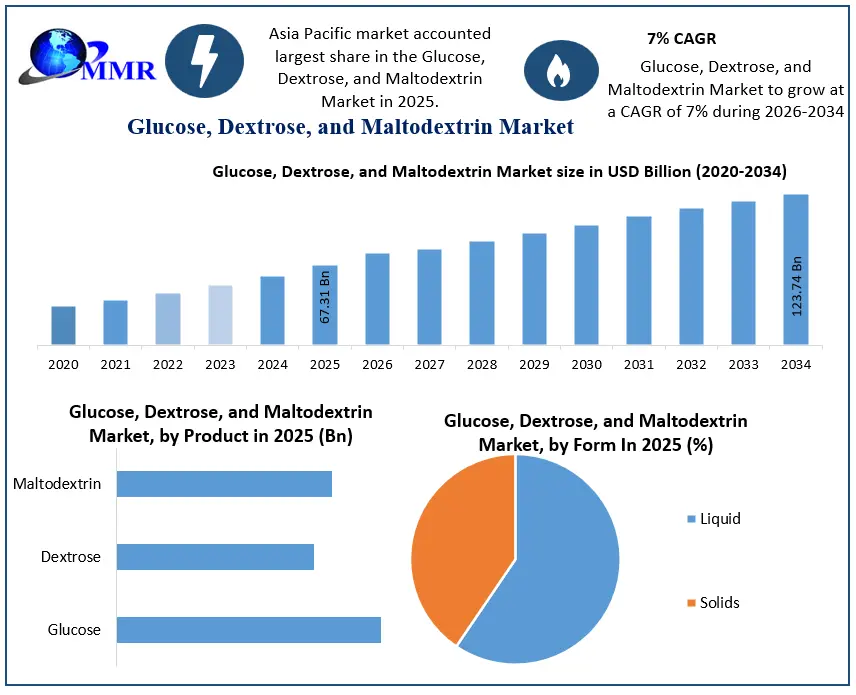

The Glucose, Dextrose, and Maltodextrin Market size was valued at USD 67.31 Billion in 2025 and the total Glucose, Dextrose, and Maltodextrin revenue is expected to grow at a CAGR of 7% from 2025 to 2034, reaching nearly USD 123.74 Billion.

Glucose, Dextrose, and Maltodextrin Market Overview:

The Glucose is the most common form of sugar and the body's primary source of energy. Dextrose is a natural sugar derived from corn, honey, and fruits. Maltodextrin is a carbohydrate used in the food industry. Demand for convenience meals is surging, increasing demand for food and beverages, and large corporations are increasing their investments are the factor which drive the growth of market.

To know about the Research Methodology :- Request Free Sample Report

Glucose, Dextrose, and Maltodextrin Market Dynamics:

Owing to increasing preference for convenience foods, increasing demand for maltodextrin, and the price effectiveness of glucose syrup, the increased demand for food and beverages are the factors drive the growth of market.

Moreover increase in personal disposable income, increasing R&D activities, increased consumer awareness, increased demand for low-calorie foods, and an increase in investment by major companies are factors driving the growth of the market.

Increasing demand for chewing gum as a substitute for glucose, dextrose, and maltodextrin is considered to be one of the main factors, and it is estimated that this will reduce the growth of the glucose, dextrose and maltodextrin market. Government regulations are one of the restraints factors for the growth of market.

Glucose, Dextrose, and Maltodextrin Market Segment Analysis:

In 2025, the Liquid segment holds the highest demand in the Glucose, Dextrose, and Maltodextrin Market. Liquid forms are widely used in the food and beverage industry due to their ease of handling, quick solubility, and efficient blending in applications such as beverages, syrups, and processed foods. The Solids segment, including powders and crystals, is also witnessing steady growth, particularly in bakery, confectionery, and pharmaceutical applications where longer shelf life and ease of storage are important.

Based on Grade, Food Grade dominates the market in 2025 owing to its extensive use in food processing, confectionery, bakery, and beverage industries. These ingredients are essential as sweeteners, stabilizers, and texture enhancers. Pharmaceutical Grade is experiencing notable growth due to its increasing application in drug formulations, intravenous solutions, and nutraceuticals, driven by rising healthcare demand and pharmaceutical production.

Based on Process, Enzymatic Hydrolysis is the most preferred and fastest-growing segment in 2025. This process is favored for its efficiency, higher yield, and ability to produce consistent quality products with fewer by-products. Acid Hydrolysis, although traditionally used, is gradually declining due to environmental concerns and less precise control over product characteristics compared to enzymatic methods.

Based on Process, Enzymatic Hydrolysis is the most preferred and fastest-growing segment in 2025. This process is favored for its efficiency, higher yield, and ability to produce consistent quality products with fewer by-products. Acid Hydrolysis, although traditionally used, is gradually declining due to environmental concerns and less precise control over product characteristics compared to enzymatic methods.

Glucose, Dextrose, and Maltodextrin Market Scope: Inquire before buying

| Glucose, Dextrose, and Maltodextrin Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 67.31 USD Bn |

| Forecast Period 2026-2034 CAGR: | 7% | Market Size in 2034: | 123.74USD Bn |

| Segments Covered: | by Product | Glucose Dextrose Maltodextrin |

|

| by Form | Liquid Solids |

||

| by Grade | Food Grade Pharmaceutical Grade |

||

| by Process | Acid Hydrolysis Enzymatic Hydrolysis |

||

| by Packaging Type | Bags Bulk Drums Sachets |

||

| by Application | Food and Beverages Confectionery products Bakery products Dairy products Beverages Soups, Sauces Others Pharmaceuticals Personal Care products Paper & pulp Others |

||

| by Distribution Channel | Direct Sales Distributors E-Commerce |

||

Regional Insights:

Based on Region, Asia Pacific leads the Glucose, Dextrose, and Maltodextrin Market in 2025, driven by strong demand from the food and beverage industry, expanding population, and rapid industrialization in countries like China and India. North America follows with significant demand due to advanced food processing industries and high consumption of packaged foods. Europe shows steady growth supported by established food and pharmaceutical sectors. Meanwhile, regions such as Latin America and Middle East & Africa (MEA) exhibit moderate growth, influenced by increasing urbanization and rising demand for processed food products.

Glucose, Dextrose, and Maltodextrin Market Recent Industry Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 27 February 2025 | Ingredion Incorporated | The company announced a major investment of $150 million to upgrade and automate its North American starch processing plants in Cedar Rapids and Indianapolis. | This initiative will directly enhance production efficiency and yield for high-purity, starch-based texture solutions like maltodextrin. |

| 15 April 2025 | D&H Food and Nutrition | The company officially launched DexSteady, a specialized, plant-based wholewheat snack designed to offer a slow, sustained release of dextrose into the bloodstream for up to five hours. | This product broadens the commercial application of dextrose from instant energy drinks into long-acting clinical hypoglycemia management and sports nutrition. |

| 02 June 2025 | Ingredion Germany GmbH | The company finalized a joint venture agreement with Agrana Stärke GmbH, acquiring a 49% equity stake to scale up manufacturing infrastructure in Țăndărei, Romania. | Backed by a joint €35 million investment, the project expands localized starch and sweetener capacity to meet growing clean-label food demands across Europe, the Middle East, and Africa. |

| 13 September 2025 | Caplin Steriles Limited | The pharmaceutical manufacturer secured official U.S. FDA approval for its milrinone lactate injection pre-mixed formulation utilizing 5% dextrose as the drug carrier solution. | This regulatory greenlight accelerates the integration of high-purity pharmaceutical-grade dextrose solutions within critical intensive care and emergency cardiovascular treatments. |

| 15 January 2026 | Ingredion Incorporated | The ingredient provider successfully deployed full process automation loops across its North American processing lines to maximize starch-to-dextrose conversion rates. | The upgrade directly mitigates supply volatile spikes by optimizing raw material utilization efficiency for high-demand, clean-label sweeteners. |

| 12 April 2026 | Archer Daniels Midland (ADM) | The agricultural processing giant fully optimized its corn wet-milling operational infrastructure to enhance output yields of its high-purity dextrose segments. | The strategic realignment expands supply availability to satisfy accelerating volume demand coming from the biopharmaceutical and clinical nutraceutical sectors. |

Recent development:

• In 2019, Taylor expanded its non-GMO maltodextrin production line, which is a nutritional sweetener made from non-GMO corn. -Genetically modified corn to meet the growing global demand for food grade.

The objective of the report is to present a comprehensive analysis of the global market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analysed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the global market dynamics, structure by analyzing the market segments and projects the global market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the global market make the report investor’s guide.

Glucose, Dextrose, and Maltodextrin Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Glucose, Dextrose, and Maltodextrin Market Key Players

- Archer Daniel Midland Company (ADM)

- AGRANA

- AVEBE

- Cargill Incorporated

- COPAM

- Fooding Group Limited

- Grain Processing Corporation

- Gulshan Polyols Ltd.

- Ingredion Incorporated

- Luzhou Bio-Chem Technology Ltd.

- Matsutani Chemical Industry Co., Ltd.

- Roquette Frères

- Shandong Xiwang Sugar Industry Co. Ltd.

- Xingmao

- Südzucker AG

- Tate & Lyle PLC

- Tereos S.A.

- Gujarat Ambuja Exports Limited

- Qinhuangdao Lihua Starch Co., Ltd.

- Pruthvi Foods Pvt Ltd