Gantry (Cartesian) Robot Market Size by Axis Type, End use Industry, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

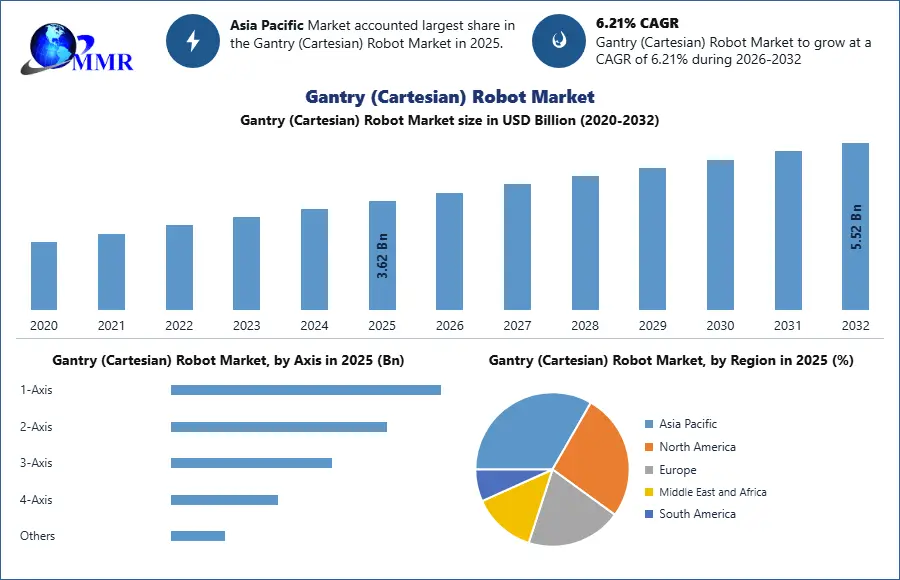

The Gantry Robot Market size was valued at USD 3.62Bn in 2025, and the Gantry Robot market revenue is growing at a CAGR of 6.21% from 2026 to 2032, reaching USD 5.52 Bn by 2032.

Gantry Robot Market Overview

Gantry robots, also known as Cartesian robots, are widely preferred for their high precision, repeatability, payload handling capability, and ability to operate in large work envelopes. The global Gantry Robot Market is witnessing strong growth due to increasing industrial automation across automotive, electronics, logistics, aerospace, and heavy manufacturing sectors. These robots are extensively used for pick-and-place operations, palletizing, welding, assembly, material handling, packaging, and CNC machine tending. The market is experiencing accelerated demand from smart factories and Industry 4.0 initiatives, where manufacturers are integrating AI-enabled robotics and IoT-based monitoring systems to improve productivity and reduce labor dependency. Rising warehouse automation in e-commerce and third-party logistics industries is also contributing significantly to market expansion. Companies are increasingly investing in multi-axis gantry systems for high-speed and high-load industrial applications.

Gantry Robot Market Snapshot

To know about the Research Methodology:-Request Free Sample Report

Gantry Robot Market Dynamics

Trend

One of the major trends shaping the Gantry Robot Market is the rapid integration of AI-driven smart automation and Industry 4.0 technologies into robotic systems. Manufacturers are increasingly deploying intelligent gantry robots equipped with machine vision systems, predictive maintenance software, cloud connectivity, and real-time analytics to improve manufacturing efficiency and minimize operational downtime. Multi-axis gantry robots are gaining traction in automotive and electronics manufacturing due to their ability to handle complex and repetitive tasks with high precision. Another emerging trend is the increasing adoption of gantry robots in warehouse automation and e-commerce fulfillment centers for high-speed sorting, packaging, and palletizing operations. Robotics manufacturers are also focusing on modular gantry systems that provide scalability and flexibility for customized industrial applications. Collaborative gantry robots integrated with AI sensors are helping industries improve human-machine interaction and workplace safety. Additionally, demand for lightweight and energy-efficient robotic systems is increasing as industries focus on sustainability and reduced energy consumption. The integration of digital twins and remote monitoring platforms is further transforming industrial robotic operations and predictive performance optimization across smart manufacturing ecosystems globally.

Driver

The increasing adoption of industrial automation across automotive, electronics, logistics, and manufacturing industries. Companies are investing heavily in robotic automation to improve productivity, operational efficiency, and product quality while minimizing labor dependency and operational costs. Gantry robots provide superior precision, high payload capacity, and continuous operation capability, making them highly suitable for repetitive industrial processes such as assembly, welding, machine loading, material handling, and packaging. The rapid growth of e-commerce and warehouse automation is further driving demand for high-speed robotic systems capable of handling bulk material movement and automated storage operations. Rising labor shortages and increasing labor costs in developed and emerging economies are encouraging manufacturers to shift toward automated production systems. Governments across China, Japan, South Korea, Germany, and the United States are also supporting smart manufacturing and robotics investments through Industry 4.0 initiatives and industrial modernization programs. Technological advancements in AI, IoT, motion control systems, and sensor technologies are improving gantry robot performance, flexibility, and accuracy, further enhancing market penetration across multiple industrial verticals worldwide.

Restraint

One of the major restraints affecting the Gantry Robot Market is the high initial investment and integration cost associated with robotic automation systems. Small and medium-sized enterprises often face challenges in adopting gantry robots due to the substantial capital expenditure required for robot installation, programming, infrastructure modification, software integration, and workforce training. The complexity of integrating robotic systems into existing manufacturing lines also creates operational challenges, particularly for industries with legacy equipment and limited automation expertise. Maintenance and repair costs of advanced gantry systems can further increase overall ownership expenses for end users. Additionally, industries operating in low-volume or highly customized production environments may find it difficult to justify automation investments due to uncertain return on investment.

Gantry Robot Market Segment Analysis

By Axis

The 3-Axis segment dominates the Gantry Robot Market due to its widespread utilization across industrial manufacturing, assembly, material handling, packaging, and pick-and-place applications. These robots provide movement along the X, Y, and Z axes, enabling high operational flexibility, accurate positioning, and efficient handling of complex manufacturing tasks. Industries such as automotive, electronics, food & beverage, pharmaceuticals, and logistics extensively deploy 3-axis gantry robots because of their balance between functionality, speed, and cost-effectiveness. Compared to 1-axis and 2-axis systems, 3-axis robots can perform more advanced operations including CNC machine tending, palletizing, welding support, and automated inspection.

Manufacturers prefer 3-axis gantry systems due to their ease of integration with conveyor systems and smart factory environments. Their capability to operate continuously with minimal human intervention significantly improves productivity and reduces operational errors. In addition, advancements in servo motors, AI-based controls, and motion guidance technologies are enhancing the efficiency and precision of 3-axis systems.

By Payload

The 51–350 Kg payload segment is expected to dominate the Gantry Robot Market over the forecast period due to its extensive use in medium-to-heavy industrial applications requiring balanced speed, flexibility, and load-handling capability. These gantry robots are widely utilized in automotive manufacturing, logistics, heavy machinery handling, packaging, palletizing, and warehouse automation operations. The segment offers an ideal combination of operational efficiency and cost optimization, making it highly suitable for industries handling moderately heavy components and bulk materials. Automotive manufacturers extensively deploy 51–350 Kg gantry robots for engine assembly, welding support, component transfer, and chassis handling applications. In logistics and e-commerce warehouses, these robots are increasingly adopted for automated sorting, packaging, and material movement processes. Compared to lightweight payload systems, medium payload robots provide greater versatility and productivity for industrial operations.

Gantry Robot Market Regional Insights

Asia Pacific dominated the global Gantry Robot Market in 2025 due to rapid industrialization, expanding manufacturing infrastructure, and strong adoption of automation technologies across China, Japan, South Korea, and India. The region serves as a global manufacturing hub for automotive, electronics, semiconductors, consumer goods, and industrial machinery, which significantly drives demand for gantry robotic systems. China remains the leading contributor owing to massive investments in smart factories, warehouse automation, and advanced robotics under government-supported industrial modernization initiatives. Japan and South Korea continue to lead in robotics innovation, AI-enabled manufacturing, and precision engineering technologies. Rising labor costs and increasing focus on production efficiency are encouraging manufacturers across Asia Pacific to integrate automated material handling and assembly solutions into production facilities. The rapid expansion of e-commerce and logistics infrastructure is also accelerating demand for gantry robots in warehousing and fulfillment centers. Furthermore, government support for Industry 4.0, growing foreign direct investment in manufacturing, and increasing electronics production capacity are strengthening regional market growth.

Gantry Robot Market Recent Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 11 February 2025 | Jacobi Robotics | The company collaborated with Unlimited Electro Group to launch Palletize AI, an advanced artificial intelligence-driven robotic control system. | The integration optimizes conveyor and gantry robot path-planning, facilitating high-efficiency warehouse and automated material sorting execution. |

| 25 April 2025 | Mobility Foresights | The platform recorded the commercial product debut of the AF-PLT Gantry Robot Palletizing System, built featuring a highly compact and heavy-duty structural layout. | The system deployment drives ideal load handling and enhanced spatial orientation accuracy within high-density production lines. |

| 30 September 2025 | Bosch Rexroth | The company hosted its official trade press conference to unveil strategic partnerships and advancements for its Linux-based ctrlX OS operating platform tailored for overhead linear and cartesian robots. | The upgrade enhances multi-axis gantry software-centric control, cybersecurity protocols, and real-time operational data processing via edge-integrated artificial intelligence. |

| 29 January 2026 | KENGIC | The organization officially detailed the widespread global deployment of its Heavy-Load High-Precision Gantry Robot portfolio engineered to disrupt traditional Western market monopolies. | The newly refined system executes extreme weight manipulation with a payload capacity up to 2000kg alongside a precise action accuracy of 1mm. |

| 03 May 2026 | Liebherr | The firm developed and introduced LHDismantle, a specialized overhead automation system engineered to process the automated teardown of high-voltage electric vehicle batteries. | The technology combines modular and scalable gantry handling turnkey infrastructure to dramatically accelerate safe, sustainable recycling throughput for electric mobility sectors. |

Gantry (Cartesian) Robot Market Scope: Inquire before buying

| Gantry (Cartesian) Robot Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 3.62 USD Billion |

| Forecast Period 2026-2032 CAGR: | 6.21% | Market Size in 2032: | 5.52 USD Billion |

| Segments Covered: | by Axis | 1-Axis 2-Axis 3-Axis 4-Axis Others |

|

| by Payload | Up to 50 Kg 51–350 Kg Above 350 Kg |

||

| by Support | End Effector Robot |

||

| by Application | Handling Assembling & Disassembling Dispensing Welding & Soldering Processing Others |

||

| by Industry | Automotive Metals & Machinery Electronics & Semiconductors Pharmaceuticals & Cosmetics Food & Beverages Plastics, Rubber & Chemicals Others |

||

Gantry (Cartesian) Robot Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/Competitors profiles covered in the Gantry (Cartesian) Robot Market report in strategic perspective

Gantry Robot Market

1. Single-Axis Gantry Robots

Single-axis gantry robots operate along one linear axis and are mainly used for simple pick-and-place operations, material transportation, positioning, and repetitive movement tasks in manufacturing and assembly lines.

Key Players:

1. Bosch Rexroth AG (Germany)

2. Thomson Industries, Inc. (United States)

3. IAI Corporation (Japan)

4. HIWIN Technologies Corp. (Taiwan)

5. Parker Hannifin Corporation (United States)

2. Two-Axis Gantry Robots

Two-axis gantry robots provide movement along two directions and are used for loading/unloading, palletizing, machine tending, and component handling where wider operational coverage is required.

Key Players:

1. Festo SE & Co. KG (Germany)

2. Yamaha Motor Co., Ltd. (Japan)

3. Bosch Rexroth AG (Germany)

4. Mitsubishi Electric Corporation (Japan)

5. Parker Hannifin Corporation (United States)

3. Three-Axis & Multi-Axis Gantry Robots

Three-axis and multi-axis gantry robots provide complete movement in X, Y, and Z directions with enhanced flexibility and precision. They are extensively used for automotive assembly, welding, CNC machine loading, electronics manufacturing, and automated production lines.

Key Players:

1. FANUC Corporation (Japan)

2. ABB Ltd. (Switzerland)

3. KUKA AG (Germany)

4. Yaskawa Electric Corporation (Japan)

5. Kawasaki Heavy Industries, Ltd. (Japan)

6. Mitsubishi Electric Corporation (Japan)

4. Heavy-Duty Gantry Robots

Heavy-duty gantry robots are designed to handle large components, heavy payloads, and oversized materials. They are commonly deployed in automotive manufacturing, aerospace, metal fabrication, shipbuilding, and heavy engineering applications.

Key Players:

1. KUKA AG (Germany)

2. ABB Ltd. (Switzerland)

3. FANUC Corporation (Japan)

4. Güdel Group AG (Switzerland)

5. Güdel AG (Switzerland)

6. Dürr AG (Germany)

5. Pick-and-Place Gantry Robots

Pick-and-place gantry robots are optimized for high-speed handling, sorting, packaging, and assembly operations. These robots improve productivity and reduce manual labor in manufacturing and warehouse environments.

Key Players:

1. Omron Corporation (Japan)

2. Epson Robots (Japan)

3. Yamaha Motor Co., Ltd. (Japan)

4. ABB Ltd. (Switzerland)

5. Festo SE & Co. KG (Germany)

6. Gantry Robots for Packaging & Palletizing

Description:

These gantry systems are specifically designed for packing, stacking, palletizing, and logistics automation in food & beverage, pharmaceuticals, e-commerce, and consumer goods industries.

1. KUKA AG (Germany)

2. FANUC Corporation (Japan)

3. ABB Ltd. (Switzerland)

4. Yaskawa Electric Corporation (Japan)

5. Daifuku Co., Ltd. (Japan)

6. Swisslog Holding AG (Switzerland)

Frequently Asked Questions:

1. Which region has the largest share in Global Gantry Robot Market?

Ans: Asia Pacific region held the highest share in 2025.

2. What is the growth rate of Global Gantry Robot Market?

Ans: The Global Gantry Robot Market is growing at a CAGR of 4.5% during forecasting period 2026-2032.

3. What is scope of the Global Gantry Robot Market report?

Ans: Global Gantry Robot Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. What is the study period of this Market?

Ans: The Global Gantry Robot Market is studied from 2025 to 2032.