1. Flight Inspection Market : Market Introduction

1.1. Executive Summary

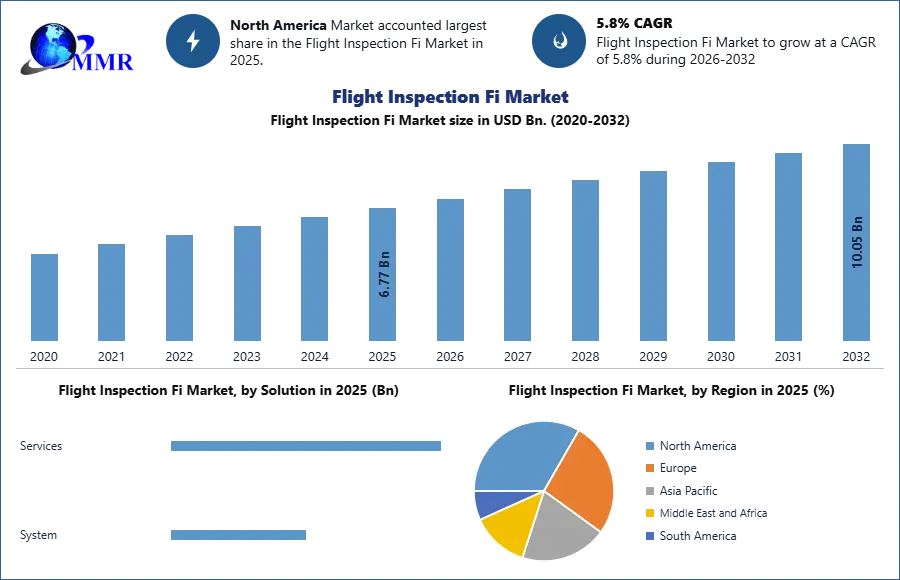

1.2. Market Size (2025) & Forecast (2026-2032)

1.3. Market Size (Value USD Billion) and Market Share (%) - By Segments, Regions, and Country

2. Flight Inspection Market Competitive Landscape

2.1. MMR Competition Matrix

2.2. Competitive Positioning of Top Key Players

2.3. Key Players Benchmarking

2.3.1 Company Name

2.3.2 Headquarter

2.3.3 Product Portfolio

2.3.4 End-User Segment

2.3.5 Revenue Details in 2025

2.3.6 Market Share (%)

2.3.7 Profit Margin (%)

2.3.8 Carbon Footprint Disclosure

2.3.9 Certifications

2.3.10 Technology Adoption

2.3.11 Maintenance & Support Capability

2.3.12 ESG / sustainability policies

2.3.13 Geographical Presence

2.4. Market Structure

2.4.1 Market Leaders

2.4.2 Market Followers

2.4.3 Emerging Players

2.5. Mergers and Acquisitions Details

2.6. Market Share by Player — Revenue & Fleet Deployment

2.6.1 Top 10 Companies by Global Flight Inspection Market Revenue, 2025 (USD Million)

2.6.2 Market Share (%) Comparison – Global Level

2.6.3 Regional Revenue Contribution by Top Players (NA, EU, APAC, MEA, SAM)

2.6.4 Share Evolution Trend (2020–2025)

2.6.5 Installed Base Growth Trend vs Fleet Replacement Cycles

2.7. Global vs Regional Flight Inspection Service Providers Comparative Analysis

2.7.1 Revenue Mix: Government vs Private Operators Exposure

2.7.2 R&D Spend as % of Revenue (Avionics & Calibration Tech Focus)

2.7.3 Global Manufacturing & Maintenance Network vs Regional Service Hubs

2.7.4 Certification & Compliance Strength (ICAO, FAA, EASA Standards)

2.7.5 Service Network Density Across Major Airspace Regions

2.7.6 Dependence on OEM vs Third-Party Equipment & Services

2.8. Advanced & Digital Flight Inspection Technology Providers

2.8.1 Vendors Supporting Next-Gen GNSS, GBAS & Remote Calibration Platforms

2.8.2 AI-based Signal Anomaly Detection & Predictive Calibration Readiness

2.8.3 Integration with Digital Flight Management & Ground Data Platforms

2.8.4 Automation & Reduced Human Intervention Capabilities

2.8.5 Cybersecurity & Data Integrity Frameworks

2.8.6 UAV-based Flight Inspection Adoption & Edge Platforms

2.9. Avionics & System Performance Capabilities

2.9.1 Navigation & Guidance Accuracy Benchmarking (ILS, GNSS, VOR, DME)

2.9.2 Communication & Surveillance System Performance (VHF, SATCOM, ADS-B, Radar)

2.9.3 Flight Management System (FMS) & Autopilot Integration Efficiency

2.9.4 Real-Time Data Acquisition & Processing Accuracy

2.9.5 Lifecycle & Retrofit Upgrade Capabilities

2.9.6 Regulatory Compliance & Certification Readiness

3. Flight Inspection Market Dynamics

3.1. Flight Inspection Market Trends

3.2. Flight Inspection Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Key Opinion Leader Analysis For the Global Industry

4. Avionics Systems Analysis in Flight Inspection Market

4.1 Core Avionics Architecture in Flight Inspection Platforms

4.2 Navigation & Guidance Systems Performance Evaluation (ILS, GNSS, VOR, DME Integration)

4.3 Communication & Surveillance Avionics Assessment (VHF, SATCOM, ADS-B, Radar)

4.4 Flight Management Systems (FMS) & Autopilot Integration Efficiency

4.5 Real-Time Data Acquisition, Processing & Calibration Accuracy

4.6 Regulatory Compliance & Certification Requirements (ICAO / FAA / EASA Standards)

4.7 Retrofit vs Next-Generation Digital Avionics Adoption

5. Technology Advancements & Performance Optimization in Flight Inspection Avionics

5.1 AI-Based Signal Anomaly Detection & Predictive Calibration Algorithms

5.2 Software-Defined Avionics & Modular Open Systems Architecture (MOSA)

5.3 Integration with Digital Flight Inspection & Ground Data Platforms

5.4 Cybersecurity & Data Integrity Frameworks in Avionics Systems

5.5 Automation Level Enhancement & Reduced Human Intervention Models

5.6 Lifecycle Cost Optimization & Upgrade Pathway Analysis

6. Operational & Cost Structure Analysis 2025

6.1 Aircraft Acquisition & Modification Cost Analysis

6.2 Fuel, Crew & Operational Cost Benchmarking

6.3 Outsourced vs In-house Inspection Economics

6.4 Cost Sensitivity to Fuel Price & Aircraft Utilization Rates

6.5 Lifecycle Cost Assessment of Fixed-wing vs UAV Platforms

6.6 Maintenance & Downtime Cost Modeling

7. Infrastructure Modernization & Airport Upgrade Impact Analysis

7.1 Impact of Airport Expansion Programs on Inspection Demand

7.2 ILS to GBAS Transition & Inspection Implications

7.3 Digital Tower & Remote Navigation System Calibration Needs

7.4 Military Airbase Modernization Influence

7.5 Emerging Airport Markets & Greenfield Development Impact

7.6 CNS Infrastructure Replacement Cycles

7.7 Smart Airport Integration & Inspection Frequency Evolution

8. Demand Forecasting & Traffic-Linked Growth Analysis

8.1 Air Traffic Growth Correlation with Inspection Frequency

8.2 Regional Airport Density vs Inspection Fleet Demand

8.3 Navigation Aid Deployment Growth Modeling

8.4 UAV Adoption Impact on Future Fleet Requirements

8.5 Emerging Market Aviation Infrastructure Investment

8.6 Sensitivity Modeling Based on Air Traffic Volatility

8.7 Long-term Fleet Planning & Replacement Outlook

9. Training & Human Capital Development in Flight Inspection

9.1 Pilot & Crew Training Programs for Flight Inspection Missions

9.2 Avionics Operator Certification & Skill Benchmarking

9.3 Simulation-based Calibration & System Testing Modules

9.4 Workforce Transition Planning for UAV and Digital Platforms

9.5 Knowledge Transfer from Legacy to Next-Generation Systems

9.6 Training Cost vs Operational Efficiency Impact

9.7 Continuous Professional Development & Recertification Trends

10. Risk, Reliability & Safety Impact Assessment

10.1 Risk of Navigation Signal Degradation & Operational Impact

10.2 Impact of Delayed Calibration on Flight Safety

10.3 Redundancy Requirements in Critical Airspace

10.4 Weather & Terrain Challenges in Inspection Missions

10.5 Operational Disruption Risk Assessment

10.6 Reliability Modeling of Inspection Equipment

10.7 Contingency Planning & Emergency Calibration Framework

11. Platform Optimization & Fleet Analysis

11.1 Fleet Age Profile & Replacement Cycle Assessment

11.2 Aircraft Modification Requirements for Inspection Equipment

11.3 Utilization Rate Benchmarking Across Regions

11.4 Fixed-Wing vs UAV Efficiency Trade-off Analysis

11.5 Fleet Standardization vs Mixed Platform Strategy

11.6 Leasing vs Ownership Model Evaluation

11.7 Long-term Fleet Capacity Planning Framework

12. Data Analytics & Digital Transformation Assessment

12.1 Shift from Manual Calibration to Automated Digital Reporting

12.2 Real-time Signal Performance Monitoring Integration

12.3 Cloud-based Data Storage & CNS Data Archiving Trends

12.4 AI-based Anomaly Detection in Navigation Aids

12.5 Big Data Utilization for Predictive Maintenance

12.6 Integration with Air Traffic Management (ATM) Systems

12.7 Digital Reporting Compliance & Audit Trail Requirements

13. Investment & Budget Allocation Analysis

13.1 Government Aviation Infrastructure Budget Trends

13.2 Public vs Private Funding Models

13.3 ROI Assessment of UAV Adoption in Inspection

13.4 Cost Recovery Models for ANSPs

13.5 Capital Allocation Trends in Developing Economies

13.6 Impact of Defense Budget on Military Inspection Programs

13.7 Long-term Aviation Safety Investment Priorities

14. Outsourcing & Service Model Transformation Analysis

14.1 Growth of Third-party Flight Inspection Providers

14.2 Long-term Service Agreements (LTSA) Trends

14.3 Performance-based Contracting Models

14.4 Cross-border Inspection Service Provision

14.5 Risk-sharing Agreements & SLA Framework

14.6 Hybrid Public–Private Operational Models

14.7 Service Revenue vs Equipment Revenue Contribution

15. Sustainability & Environmental Impact Assessment

15.1 Carbon Emissions from Inspection Aircraft Operations

15.2 Transition to Sustainable Aviation Fuel (SAF)

15.3 Electric & Hybrid Inspection Aircraft Potential

15.4 UAV-based Low-emission Inspection Advantage

15.5 Environmental Compliance & Green Aviation Policies

15.6 Noise Regulation Impact on Inspection Scheduling

15.7 Sustainability-driven Fleet Modernization Strategy

16. Geopolitical & Airspace Policy Impact Analysis

16.1 Cross-border Airspace Inspection Protocols

16.2 Impact of Airspace Restrictions & Geopolitical Tensions

16.3 Sanctions & Export Controls on Inspection Equipment

16.4 Defense-driven Air Navigation Modernization

16.5 Aviation Liberalization & Regional Integration Effects

16.6 Infrastructure Funding Linked to National Aviation Strategy

16.7 Regulatory Delays & Policy Risk Assessment

17. Future Technology Disruption Outlook

17.1 Satellite-based Navigation Reducing Ground Aid Dependency

17.2 Ground-based Augmentation System (GBAS) Adoption Outlook

17.3 Remote & Autonomous Calibration Platforms

17.4 Blockchain-based Compliance Tracking

17.5 Integration with NextGen & SESAR Programs

17.6 Transition Toward Continuous Signal Monitoring Systems

17.7 Long-term Replacement Risk for Traditional Inspection Fleets

18. Supply Chain & Ecosystem Analysis

18.1 Value Chain Mapping & Key Stakeholders

18.2 Critical Component & Avionics Sourcing Dependencies

18.3 Aircraft Platform Integration & Modification Cycle

18.4 Regional Manufacturing & Assembly Footprint

18.5 Lead Time, Procurement & Certification Bottlenecks

18.6 Aftermarket, MRO & Lifecycle Support Network

19. Regulatory & Compliance Framework Analysis By Region

19.1 ICAO Flight Inspection Standards & Annex 10 Compliance

19.2 FAA, EASA & Regional Regulatory Mandates

19.3 Calibration Frequency Requirements by Aid Type

19.4 Certification & Airworthiness Requirements for Inspection Aircraft

19.5 Regulatory Impact on Replacement Cycles

19.6 Harmonization Challenges Across Regions

19.7 Impact of Emerging Performance-Based Navigation (PBN) Standards

20. Flight Inspection Market : Global Flight Inspection Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

20.1. Global Flight Inspection Market Size and Forecast, by System Type

20.1.1 Communication Aids

20.1.2 Satellite Comm

20.1.3 VHF

20.1.4 Navigation Aids

20.1.5 DME

20.1.6 GNSS

20.1.7 ILS

20.1.8 VOR

20.1.9 Surveillance Aids

20.1.10 ADS-B

20.1.11 Radar

20.1.12 Weather Radar

20.1.13 Doppler

20.1.14 Pulse

20.2. Global Flight Inspection Market Size and Forecast, By Platform Type

20.2.1 Fixed Wing

20.2.2 Business Jet

20.2.3 Narrow Body

20.2.4 Regional Jet

20.2.5 Turboprop

20.2.6 Rotary Wing

20.2.7 Single Rotor

20.2.8 Twin Rotor

20.2.9 Unmanned Aerial System

20.2.10 Fixed Wing Drone

20.2.11 Multirotor Drone

20.3. Global Flight Inspection Market Size and Forecast, by Inspection Type

20.3.1 Commissioning / Site Acceptance

20.3.2 Periodic Routine

20.3.3 Special / Emergency

20.4. Global Flight Inspection Market Size and Forecast, By Application

20.4.1 Civil & Commercial

20.4.2 Military

20.5. Global Flight Inspection Market Size and Forecast, by End User

20.5.1 Air Navigation Service Providers (ANSPs)

20.5.2 Airport Operators

20.5.3 Private / Business Aviation Operators

20.5.4 Others

20.6. Global Flight Inspection Market Size and Forecast, by Region

20.6.1 North America

20.6.2 Europe

20.6.3 Asia Pacific

20.6.4 Middle East and Africa

20.6.5 South America

21. North America Flight Inspection Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

21.1. North America Market Size and Forecast, by System Type

21.2. North America Market Size and Forecast, By Platform Type

21.3. North America Market Size and Forecast, by Inspection Type

21.4. North America Market Size and Forecast, By Application

21.5. North America Market Size and Forecast, by End User

21.6. North America Market Size and Forecast, by Country

21.6.1 United States

21.6.2 United States Market Size and Forecast, by System Type

21.6.3 United States Market Size and Forecast, By Platform Type

21.6.4 United States Market Size and Forecast, by Inspection Type

21.6.5 United States Market Size and Forecast, By Application

21.6.6 United States Market Size and Forecast, by End User

21.6.7 Canada

21.6.8 Mexico

22. Europe Flight Inspection Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

22.1. Europe Market Size and Forecast, by System Type

22.2. Europe Market Size and Forecast, By Platform Type

22.3. Europe Market Size and Forecast, by Inspection Type

22.4. Europe Market Size and Forecast, By Application

22.5. Europe Market Size and Forecast, by End User

22.6. Europe Market Size and Forecast, by Country

22.6.1 United Kingdom

22.6.2 France

22.6.3 Germany

22.6.4 Italy

22.6.5 Spain

22.6.6 Sweden

22.6.7 Russia

22.6.8 Rest of Europe

23. Asia Pacific Flight Inspection Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

23.1. Asia Pacific Market Size and Forecast, by System Type

23.2. Asia Pacific Market Size and Forecast, By Platform Type

23.3. Asia Pacific Market Size and Forecast, by Inspection Type

23.4. Asia Pacific Market Size and Forecast, By Application

23.5. Asia Pacific Market Size and Forecast, by End User

23.6. Asia Pacific Market Size and Forecast, by Country

23.6.1 China

23.6.2 S Korea

23.6.3 Japan

23.6.4 India

23.6.5 Australia

23.6.6 Indonesia

23.6.7 Malaysia

23.6.8 Philippines

23.6.9 Thailand

23.6.10 Vietnam

23.6.11 Rest of Asia Pacific

24. Middle East and Africa Flight Inspection Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

24.1 Middle East and Africa Market Size and Forecast, by System Type

24.2.Middle East and Africa Market Size and Forecast, By Platform Type

24.3 Middle East and Africa Market Size and Forecast, by Inspection Type

24.4.Middle East and Africa Market Size and Forecast, By Application

24.5.Middle East and Africa Market Size and Forecast, by End User

24.6. Middle East and Africa Market Size and Forecast, by Country

24.6.1 South Africa

24.6.2 GCC

24.6.3 Egypt

24.6.4 Nigeria

24.6.5 Rest of ME&A

25. South America Flight Inspection Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

25.1. South America Market Size and Forecast, by System Type

25.2. South America Market Size and Forecast, By Platform Type

25.3. South America Market Size and Forecast, by Inspection Type

25.4. South America Market Size and Forecast, By Application

25.5. South America Market Size and Forecast, by End User

25.6. South America Market Size and Forecast, by Country

25.6.1 Brazil

25.6.2 Argentina

25.6.3 Colombia

25.6.4 Chile

25.6.5 Peru

25.6.6 Rest Of South America

26. Company Profile: Key Players

26.01.Textron Aviation Inc.

26.01.1 Company Overview

26.01.2 Business Portfolio

26.01.3 Financial Overview

26.01.4 SWOT Analysis

26.01.5 Strategic Analysis

26.01.6 Recent Developments

26.02.Bombardier Inc.

26.03.Aerodata AG

26.04.Norwegian Special Mission AS

26.05.Saab AB

26.06.Safran S.A.

26.07.Cobham Limited

26.08.Airways International

26.09.Airfield Technology Inc.

26.10.Radiola Limited

26.11.ENAV S.p.A.

26.12.Flight Calibration Services Ltd.

26.13.Flight Precision Ltd.

26.14.Singapore Technologies Engineering Ltd

26.15.Honeywell International Inc.

26.16.Thales Group

26.17.Isavia ANS ehf.

26.18.Airports Authority of India (AAI)

26.19.NAV CANADA

26.20.Samana Special Mission

26.21.Teledyne Controls

26.22.Airways Corporation of New Zealand Limited

26.23.Aeronautical Radio of Thailand Ltd.

26.24.Bulgaria Air Traffic Services Authority

26.25.Embraer S.A.

26.26.Rohde & Schwarz GmbH & Co KG

26.27.Trimble Inc.

26.28.Sky KG Airlines

26.29.Omni Aircraft Maintenance

26.30.Lufthansa Technik

26.30.1 Others

27. Key Findings

28. Future Outlook & Analyst Recommendations

29. Flight Inspection Market : Research Methodology