Digital Therapeutics Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

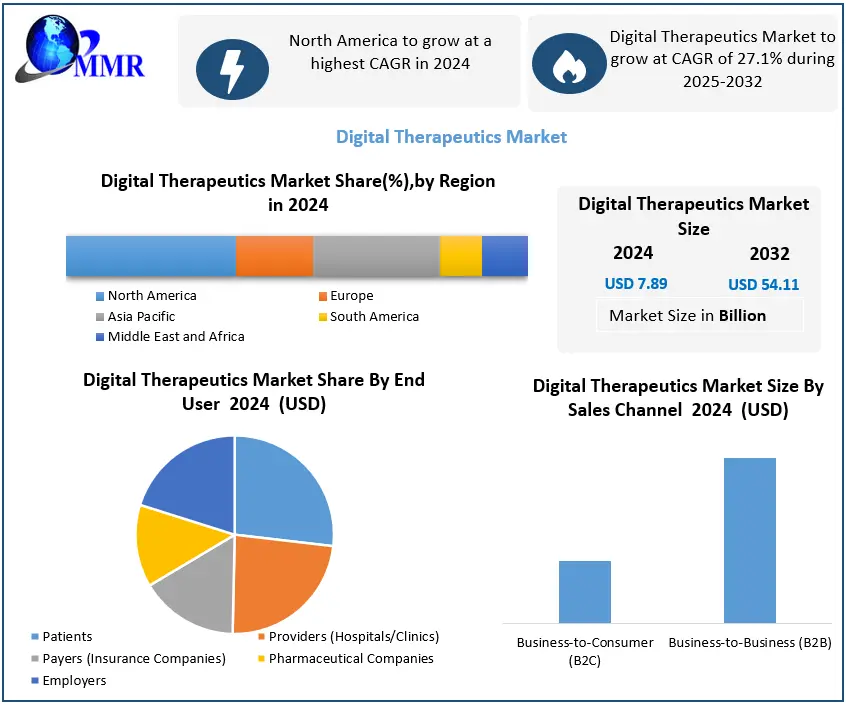

Digital Therapeutics Market was valued at USD 7.89 Bn. in 2024 and the total Global Digital Therapeutics Market revenue is Expected to grow at a CAGR of 27.1% from 2025 to 2032 reaching nearly USD 54.11 Bn. by 2032.

Digital Therapeutics Market Overview:

Patients benefit from evidence-based treatment interventions delivered through digital therapeutic interventions. It is delivered via software and gadgets to help prevent, manage, and treat medical diseases. To deliver patient care and health results, the digital treatment software program can be utilized alone or in conjunction with another device, drug, or therapy. Digital therapies' design, clinical validation, usability, and data security are all based on cutting-edge technology and best practices. Before usage, these items are assessed and authorized by regulatory organizations. Additionally, digital treatments give smart, accessible tools to patients, healthcare professionals, and payers to treat a wide range of illnesses through interventions such as high-quality, safe, and effective evidence-based cards.

The increasing adoption of smartphones in developed and emerging markets, the cost-effectiveness of digital health technology for providers and patients, and the rising need for integrated healthcare systems and patient-centric treatment are expected to increase market growth. According to Kepios, 4.27 billion people were using the internet, in April 2022, accounting for more than 60% of the global population. Besides that, the COVID-19 pandemic, supporting regulatory actions and early signs of reimbursement, as well as the rising prevalence of chronic illnesses, are expected to drive market growth.

The COVID-19 pandemic had a huge influence on the market. Demand for simple and accessible digital health solutions is a primary COVID-related motivator. According to the FDA's April 2020 rules, the distribution and use of digital health treatment devices for mental health illnesses would be permitted during the duration of the pandemic. Providers can thereby sell their solutions without having to conform to standard regulatory criteria, as long as the gadgets do not cause an unnecessary public health emergency. Growing regulatory activities are expected to drive market standardization and R&D throughout the forecast period.

In addition, Poor diet, cigarette use, drunkenness, and a lack of physical activity all raise the chance of having a chronic condition. Healthcare expenditures rise rapidly because most chronic illnesses do not exist in isolation and patients frequently have co-morbidities. Smartphone ownership is becoming increasingly important in strengthening global interconnection, both economically and socially. Smartphone penetration is a significant factor driving the market growth.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Digital Therapeutics Market Dynamics:

Increasing prevalence of chronic diseases

Chronic illnesses have raised the load on global healthcare systems. According to the American Heart Association's 2016 publication, Heart Diseases and Stroke Statistics at a Glance, cardiovascular disease (CVD) is the leading cause of mortality globally. The increased prevalence and incidence rate of chronic illnesses is a key concern for global healthcare systems. The management of chronic illness patients is a considerable problem since psychosomatic or bio-psychic variables frequently impact these individuals. Patients must adapt their behavior as part of a new self-care lifestyle since chronic illnesses are frequently accompanied by significant levels of uncertainty. However, many chronic diseases and illnesses are progressive, and their prevalence rises with age. As a result of the large increase in the global elderly population, chronic diseases are expected to increase during the forecast period.

Growing concerns about Data Privacy

Many governments reject proper permissions to various health applications, raising issues about product and data quality, dependability in treatment decisions, patient privacy, security, and responsible data usage. Digital therapy providers have access to patient information and are not permitted to share it with anybody who is not involved in the patient's treatment. However, with data integration utilizing digital technologies, the patient's data may be viewed by any healthcare provider unrelated to the patient's treatment program.

Several countries, such as the United States (through the Health Insurance Portability and Accountability Act (HIPAA) and the Health Information Technology for Economic and Clinical Health (HITECH) Act), have legislation addressing data security. Despite such federal actions, digital therapeutics consumers are vulnerable to infringement and data breaches, which may restrict the market's growth.

Emerging markets offer lucrative growth opportunities

Emerging markets like India, China, and the Middle East offer growth possibilities for digital therapeutics growth. Due to a lack of knowledge, the limited availability of these solutions, a lack of IT infrastructure, and financial and societal restraints, the industry is still in its infancy in most geographies. On the other hand, chronic illness incidence is high in most rising economies. According to WHO predictions, chronic illnesses would account for 74% of all over the world by 2023. By 2025, emerging nations would face 60% of the global burden of chronic illnesses.

Besides that, the scarcity of trained medical practitioners in developing countries emphasizes the significance of connected healthcare. However, emerging nations such as India and China lack sufficient standards and government regulations for digital health solutions, which provide an enormous opportunity to providers that are unable to fulfill the high criteria required by the US federal government. In these areas, the patient-to-doctor ratio is generally substantially higher, necessitating alternate healthcare options.

These countries have also registered widespread adoption of smartphones and related technologies due to their growing affordability. Globally, China and India are the top two countries in terms of smartphone penetration. Additionally, the growing availability of smart devices and the Internet has driven the production of health applications. Additionally, government agencies in these locations are working to develop HCIT infrastructure. China, for example, planned to enhance healthcare quality by integrating HCIT solutions in its five-year strategy from 2015 to 2020.

Patients' reluctance to use digital treatments

Motivating consumers to utilize digital medicines and gaining their trust is a significant challenge for digital therapeutic providers. While elderly and underprivileged groups have the highest illness susceptibility and incidence rates, they are the least likely to employ digital therapy products due to low levels of technological literacy. Additionally, the amount of behavioral change that may be noticed with digital treatments is currently unknown.

The clinical validation and implementation of digital treatments are done on self-selected or volunteer patients, but their effect on patients who demonstrate resistance is undetermined. However, it is uncertain if digital treatments can be sustained over extended periods of time, and there is limited data on total patient retention and long-term effects. Many patients still rely on established methods of diagnosis and therapy, making these revolutionary approaches unappealing. This presents a significant challenge to the digital therapies business.

Digital Therapeutics Market Segment Analysis:

Based on Application, the Treatment/Care-related Applications segment dominated the market with the highest market share in 2024 and is expected to maintain its dominance at the end of the forecast period. The Diabetes segment is expected to lead the market during the forecast period. According to the CDC, almost 38.1 million individuals had diabetes in 2023. The growing prevalence of diabetes and various other chronic conditions is one of the factors driving the segment's growth. Digital therapies can help healthcare doctors examine patients' lifestyles and enhance treatment plans depending on their unique therapeutic needs.

Based on Sales Channel market is segmented into Business-to-Consumer (B2C) and Business-to-Business (B2B). Business to Business segment dominated the market in 2024 and is expected to hold largest share during the forecast period. Dominance is driven by growing partnerships between DTx providers and employers, insurance companies, and healthcare organizations aiming to improve patient outcomes and reduce treatment costs. The B2B model ensures wider patient reach, better reimbursement frameworks, and integration into existing healthcare systems, making it a preferred channel for scaling digital therapeutic solutions.

Cardiovascular diseases, smoking cessation, and obesity segment expected to increase at considerable rates throughout the forecast period. The growing use of digital therapeutic goods to treat respiratory disorders is driving the market growth. Hailie by Adherium, Respiro by Amiko, Propeller by Propeller Health, Breathe Smart by Cohero Health, and CareTRx by Teva are among these products. Digital medicines have the potential to change the course of COPD and asthma treatment. This is because poor drug adherence is a significant concern while treating respiratory disorders. Digital therapy solutions can aid in the efficient resolution of this issue.

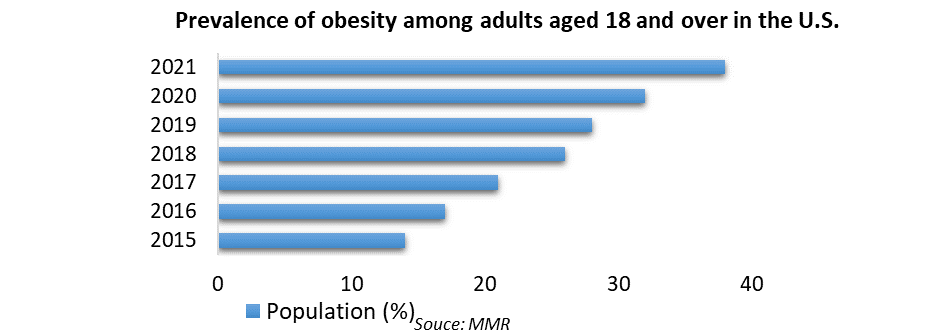

The relatively rapid and significant increase in the prevalence of obesity has been largely attributed to a changing lifestyle that promotes increased caloric intake and reduced physical activity. A high-fat diet, excessive use of sugar-sweetened drinks, and increased fast food consumption may all contribute to the continued rise in obesity prevalence.

In the United States, obesity has reached epidemic proportions. More than two-thirds of people are overweight or obese, with one in every three Americans being obese. Obesity has become increasingly common among youngsters. Obesity has also been rapidly increasing over the world, with the prevalence of obesity nearly doubling between 1991 and 1998. In the United States in 2015, about 40% of adults were obese. Obesity causes around 112,000 fatalities in the United States each year, with the majority of these deaths occurring in people with a BMI greater than 30. Patients with a BMI greater than 40 have a lower life expectancy. Digital therapeutics play an essential role in the treatment of obesity. Digital health is crucial in the development of a new strategy for obesity prevention and treatment that understands the complexities of obesity and delivers a more patient-centered, precise approach to obesity care. Telehealth and mHealth are already widely utilized in healthcare delivery, and they present new potential to lower obstacles to effective obesity care, enhance access to care, and, ultimately, improve long-term weight management and obesity-related health outcomes.

Digital therapeutics play an essential role in the treatment of obesity. Digital health is crucial in the development of a new strategy for obesity prevention and treatment that understands the complexities of obesity and delivers a more patient-centered, precise approach to obesity care. Telehealth and mHealth are already widely utilized in healthcare delivery, and they present new potential to lower obstacles to effective obesity care, enhance access to care, and, ultimately, improve long-term weight management and obesity-related health outcomes.

The most major digital advancement in obesity care during the forecast period is expected to be the growing use of telehealth. Over time, this will be increasingly supported by mHealth applications and gadgets, with interventions and support being supplied by proxy via an avatar or a chatbot powered by AI technology.

Digital Therapeutics Market Regional Insights:

North American regional market dominated the digital therapeutics market with the highest market share in 2023 and is expected to maintain its dominance at the end of the forecast period. This dominance is due to several factors, including the growing utilization of digital health devices and advantageous reimbursement scenarios that emphasize enhancing quality of life through enhanced tracking and diagnostics. The market is expected to be influenced by an increase in the prevalence of chronic diseases and the region's geriatric population. Proteus Digital Health, Inc., Omada Health, Inc., WellDoc, Inc., and Livongo Health, Inc. are some of the leading firms in this region. The majority of these organizations are headquartered in the United States, which contributes to their local dominance.

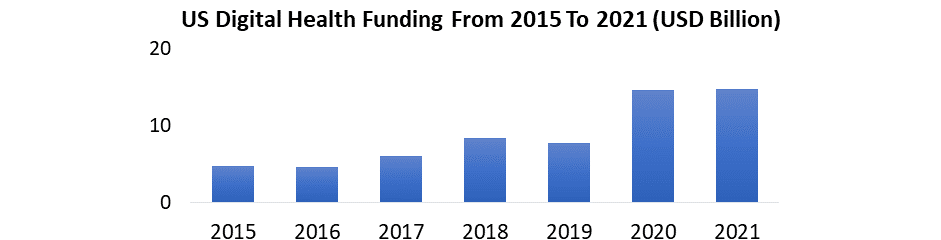

In addition, the rising emergence of new startups, the evolving reimbursement system for digital medicines, and investments in digital therapeutics are increasing and increasing government initiatives to support technical development. The United States would be the dominant country in the market during the forecast period due to reasons such as an increasing elderly generation, an increase in chronic diseases among individuals, etc. According to the C.D.C., chronic illness would affect 6 in 10 persons in the United States in January 2021. Every year, these disorders cost the country's healthcare system over USD 3.8 trillion in healthcare expenses. In the United States, the Federal government adopted a new rule in 2020 that allows all medical professionals to practice beyond state boundaries, hence increasing access to treatment and providing a bigger supply of healthcare providers for digital health enterprises. This, in combination with higher reimbursement rates for telehealth set by CMS (Centers for Medicare & Medicaid Services), should help solve the problem of insufficient numbers of medical professionals using DTx platforms.

In the United States, the Federal government adopted a new rule in 2020 that allows all medical professionals to practice beyond state boundaries, hence increasing access to treatment and providing a bigger supply of healthcare providers for digital health enterprises. This, in combination with higher reimbursement rates for telehealth set by CMS (Centers for Medicare & Medicaid Services), should help solve the problem of insufficient numbers of medical professionals using DTx platforms.

The Asia Pacific region is expected to grow at the highest growth rate of about 19.8% during the forecast period. This significant growth can be attributed to increased demand for effective healthcare, increased adoption of smartphones, and enhanced internet connectivity. As a result of increasing government expenditure on healthcare, demand for personal care devices and related services is expected to increase the market growth.

Digital Therapeutics Industry Ecosystem

Digital Therapeutics Market Scope: Inquire before buying

| Global Digital Therapeutics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 5 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 4.5% | Market Size in 2032: | USD 10 Bn. |

| Segments Covered: | by Product Type | Software-only Digital Therapeutics Device-based Digital Therapeutics |

|

| by Sales Channel | Business-to-Consumer (B2C) Business-to-Business (B2B) |

||

| by Application | Preventive Applications Prediabetes Obesity Nutrition Lifestyle Management Other Preventive Applications Treatment/Care-related Applications Diabetes CNS Disorders Chronic Respiratory Disorders Musculoskeletal Disorders Cardiovascular Diseases Smoking Cessation Medication Adherence Gastrointestinal Disorders Substance Use & Addiction Management Rehabilitation & Patient Care Other |

||

| by End-User | Patients Providers (Hospitals/Clinics) Payers (Insurance Companies) Pharmaceutical Companies Employers |

||

Digital Therapeutics Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Digital Therapeutics Market, Key Players are:

1. Noom(US)

2. Livongo Health(US)

3. Omada Health(US)

4. Virta Health(US)

5. Cognoa(US)

6. Ayogo Health(US)

7. Mindstrong Health(US)

8. 2Morrow(US)

9. Hinge Health(US)

10. BehaVR(US)

11. WellDoc(US)

12. Pear Therapeutics(US)

13. Proteus Digital Health(US)

14. Propeller Health(US)

15. Akili Interactive Labs(US)

16. Better Therapeutics(US)

17. Happify(US)

18. Kaia Health(US)

19. Mango Health(US)

20. Click Therapeutics(US)

21. Canary Health(US)

22. Wellthy Therapeutics(India)

23. Ginger( Australia)

24. Mindable Health(Germany)

25. Doktor.se( Sweden)

FAQs:

1. What is the major driver for the Digital Therapeutics market growth?

Ans. The rising smartphone prevalence in developed and emerging nations, the cost-effectiveness of digital health technology for providers and patients, and the rising demand for integrated healthcare systems and patient-centric treatment are expected to be a major driver for market growth.

2. What are the restraints in the Digital Therapeutics market?

Ans. Growing concerns about data privacy are the key factors for restraining market growth.

3. Which region is expected to lead the global Digital Therapeutics market during the forecast period?

Ans. The North American market is expected to lead the global Digital Therapeutics market during the forecast period due to the growing utilization of digital health devices and advantageous reimbursement scenarios that emphasize enhancing quality of life through enhanced tracking and diagnostics.

4. What is the projected market size & growth rate of the Digital Therapeutics Market?

Ans. Digital Therapeutics Market size was valued at USD 7.89 Bn. in 2024 and the total Digital Therapeutics revenue is expected to grow at a CAGR of 27.1% from 2025 to 2032, reaching nearly USD 54.11 Bn.

5. What segments are covered in the Digital Therapeutics Market report?

Ans. The segments covered are Sales Channel, Component, Application, and Region.