Data Center Power Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

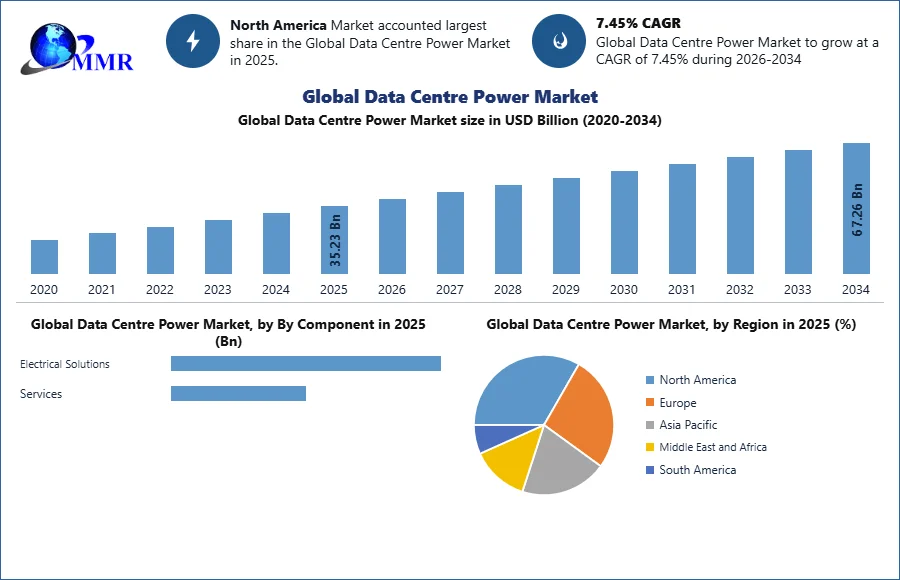

The Data Center Power Market size was valued at USD 35.23 Billion in 2025 and the total Data Center Power revenue is expected to grow at a CAGR of 7.45% from 2025 to 2034, reaching nearly USD 67.26 Billion by 2034.

Data Center Power Market Overview

An increase in the demand for cloud storage has led to an increase in the number of data centres throughout the world. These data centres need a lot of electricity. Market growth is expected to be fueled by the rise in the introduction of cutting. The need for data centres is being driven by the demand for software as a service (SaaS) and the opportunity for a work-from-home lifestyle during the epidemic. Power Distribution Units (PDUs) are used to distribute power within server racks and cabinets. They help manage and control the power supply to individual servers and networking equipment. Data centers require cooling systems to dissipate the heat generated by the servers and other equipment. These cooling systems consume additional power and are a crucial part of data center power management. To ensure high availability and fault tolerance, data centers often have redundant power systems. This means that if one power source fails, the data center automatically switch to another source without disruption.

Data centers demand high levels of power redundancy to ensure uninterrupted operation. This has driven the adoption of dual power feeds, backup generators, and sophisticated power distribution systems to safeguard against outages. The growth of edge computing, where data processing occurs closer to the data source, has led to the emergence of smaller, localized data centers. These edge data centers require efficient and reliable power solutions tailored to their unique needs.

To know about the Research Methodology :- Request Free Sample Report

Data Center Power Market Dynamics

Increasing need for intelligent PDUs to balance loads and supply rack power to boost the Data Center Power Market growth

Companies use sophisticated power management tools like intelligent rack power distribution units (PDU), smart uninterruptible power supplies (UPS), and battery monitoring systems to lower the power use efficiency (PUE) ratio and boost efficiency. During the forecast period, it is expected that this aspect will favour market expansion. Data center-driven technology and services have experienced unheard-of market growth. High computational power is needed for technologies like cloud computing, but they have advantages like improved scalability, efficiency, and flexibility of business operations. As a result, many medium-sized businesses now have efficient data centres like colocation and cloud web hosting facilities. Mega & cloud data centres are becoming more popular as a result of increased data centre utilisation. For peak data-intensive activities, these data centres need a lot of power, which raises the demand for UPS and PDUs.

A fundamental driving force for the Data Center Power Market is the unprecedented surge in data generation. The digital revolution across businesses, the proliferation of IoT devices, and the ever-expanding utilization of cloud-based services are generating colossal volumes of data daily. This data explosion necessitates the establishment of more data centers, each of which requires robust power solutions to ensure efficient and uninterrupted operations. The proliferation of edge computing, involving data processing in proximity to data sources rather than centralized data centers, presents both opportunities and challenges. Edge data centers necessitate compact, efficient, and robust power solutions to support their localized operations, driving innovations in power distribution and management, which is expected to boost the Data Center Power Market growth. Data centers are expected to deliver uninterrupted services, and any power disruptions can result in substantial financial losses and reputational damage. This requirement fuels the demand for redundant power systems, backup generators, and advanced uninterruptible power supplies (UPS) to ensure high availability and reliability. The proliferation of big data and analytics applications across various industries, including finance, healthcare, and retail, depends on extensive data processing. Data centers play an indispensable role in handling these workloads, thereby creating a need for robust power systems.

Trends that are most affecting the data centre industry:

Data Localization: Data localization simply refers to limiting the transfer of data from one nation to another. The Indian government has published rules emphasizing the necessity to keep user data within the nation's borders. Companies that gather sensitive consumer data must now store and handle it in nearby data centres as a result of data localization. Local data centres have seen a substantial increase as a result. India is an important hub for data centres in Asia because of its cost advantage and easy availability to skilled workers.

Sustainable Data Centers: It is well known that data centres use a lot of non-renewable resources. Employing cutting-edge technology like AI, ML, and cloud, businesses have reconfigured their facilities to significantly reduce the amount of power and water they use. Less servers are used in cloud data centres, which lowers their carbon footprint. In order to reduce significant losses caused by the transmission of electrical energy over long distances, they are typically situated closer to the facilities that supply them with electricity.

Edge Connectivity: Edge data centres are compact data centres placed closer to a network's edge. Usually, they are connected to a sizable central data centre or a number of data centres. Edge computing enables businesses to lower latency and enhance the user experience by processing data and services closer to the end user. These data centres are very helpful for sectors that require real-time data processing, including medical, communications, OTT platforms, and smart wearables.

High Energy Consumption to restrain the Data Center Power Market growth

Data centers are voracious consumers of electricity. The power required to support their operations is immense, contributing to high operational costs and environmental concerns. Energy consumption is a restraint, particularly for small and medium-sized data centers that often struggle to manage these costs effectively. Physical space constraints in data center facilities can hinder the deployment of power solutions. The need for additional power infrastructure can conflict with space allocated for servers and IT equipment. Data centers must strike a delicate balance between power infrastructure and computing resources. Data centers generate a significant amount of heat due to the operation of servers and power equipment. Effective heat dissipation and cooling are essential to prevent overheating and equipment damage. Developing efficient cooling solutions while maintaining environmental sustainability can be a significant restraint for the Data Center Power Market growth. While battery technology has evolved, providing reliable backup power, it is essential to acknowledge the finite lifespan of batteries. Lithium-ion batteries, while more advanced, eventually degrade and need replacement. The ongoing cost and maintenance of backup power systems is a restraint for data center operators.

Data Center Power Market Segment Analysis

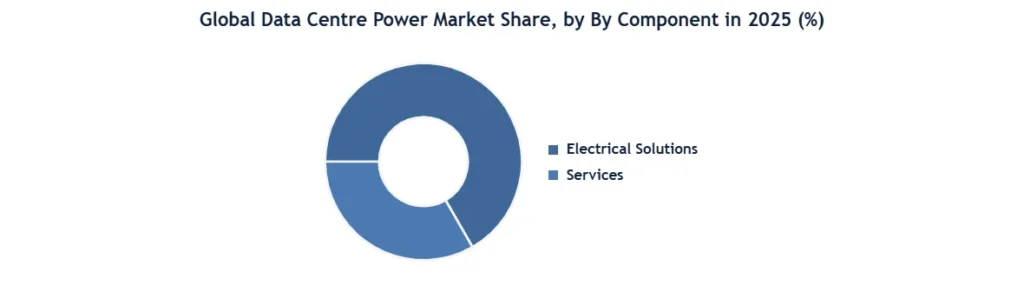

Based on Component ,The market is segmented into Electrical Solutions and Services. The Electrical Solutions segment is dominating the Global Data Power Center Market in 2025. Due to the growing need for reliable and uninterrupted power supply across hyperscale, colocation, and enterprise data centers. UPS Systems holds a significant share it ensure the continuous operations during the power outages. Power Distribution Units (PDUs) support efficient power allocation and monitoring. Demand for On-Site Power Generation & Energy Storage solutions is increasing because operators are focusing on energy resilience and sustainability. Additionally, Power Management Software & DCIM solutions are gaining adoption due to their real-time monitoring, energy optimization, and infrastructure management.

Based On the Data Centre Type , The market is segmented into On-premise, Hyperscale, HPC, Colocation, Edge. Hyperscale segment is dominated the market in 2024 & expected to hold the largest market share during the forecast period. Because Rapid growth of cloud computing, big data, AI and content streaming services, all of which require massive computing power and storage capacity. Major tech companies like Amazon, Microsoft, and Google are investing heavily in hyperscale data centers to meet global digital demand. Facilities offer scalability, energy efficiency and cost advantages at scale. Enterprises increasingly shift workloads to the cloud, hyperscale data centers continue to expand rapidly, making the leading segment in the global data center market.

Data Center Power Market Regional Insight

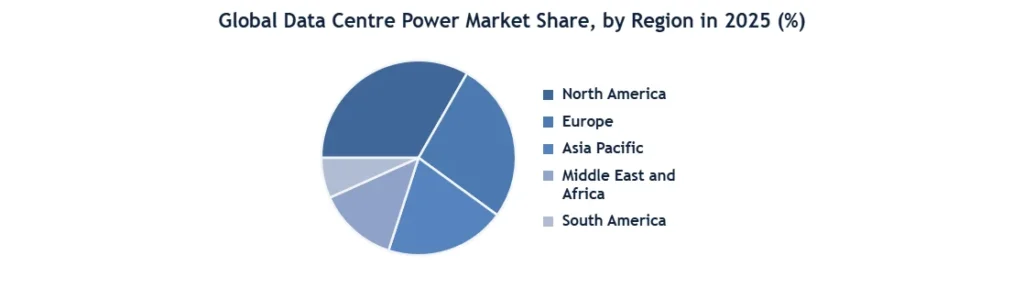

North America Dominated the Data Centre Power Market in 2025 whereas ,Asia Pacific is to grow at the fastest growth in the Data Center Power market over the forecast period

The proliferation of edge computing has created new opportunities and challenges in the Asia Pacific Data Center Power Market. Edge data centers, which are located closer to end-users or IoT devices, require compact and resilient power solutions. These facilities are instrumental in processing data locally and reducing latency, a critical requirement for applications like autonomous vehicles and industrial automation. Energy efficiency and sustainability have become key drivers in the APAC Data Center Power Market. Data centers are known for their significant power consumption. To reduce operating costs and minimize their environmental footprint, data center operators are investing in energy-efficient technologies and exploring renewable energy sources. Governments and environmental organizations are also pushing for greener data center operations.

The importance of business continuity and disaster recovery solutions has become increasingly recognized in the Asia Pacific region. Businesses are investing in data centers with redundancy features and backup power systems to ensure uninterrupted operations, especially in areas prone to natural disasters. With the increasing awareness of cybersecurity threats and data privacy concerns, organizations are investing in secure data center facilities. These facilities require robust power solutions to maintain security and ensure data integrity. The Asia Pacific Data Center Power Market benefits from ongoing technological advancements. Innovations in power distribution, cooling techniques, and energy-efficient solutions are driving the market forward. Government regulations and compliance standards related to data center operations, safety, and environmental impact are pushing data center operators to adopt more energy-efficient power solutions and sustainable practices.

Data Center Power Market Competitive Insight

With the increasing awareness of environmental concerns, energy efficiency has become a significant competitive factor. Data center operators are looking for power solutions that offer high efficiency, lower power consumption, and reduced environmental impact. This trend is driving innovation in power technology. Compliance with government regulations and industry standards is vital. Data Center Power Companies that offer power solutions that meet these standards and provide thorough documentation have a competitive edge, particularly in markets with strict regulatory requirements. Continuous research and development efforts to enhance power solutions' performance and efficiency are vital for competitiveness. Companies investing in innovation and staying at the forefront of technology have an advantage. The increasing concern over cybersecurity and data protection drives the demand for secure power solutions. Companies that integrate security features into their power infrastructure gain a competitive edge. Technological advancements in power distribution, cooling techniques, and energy-efficient solutions drive competition. Companies that stay updated with these advancements maintain their competitiveness.

Continuous research and development efforts to enhance power solutions' performance and efficiency are vital for competitiveness. Companies investing in innovation and staying at the forefront of technology have an advantage. The increasing concern over cybersecurity and data protection drives the demand for secure power solutions. Companies that integrate security features into their power infrastructure gain a competitive edge. Technological advancements in power distribution, cooling techniques, and energy-efficient solutions drive competition. Companies that stay updated with these advancements maintain their competitiveness.

Data Center Power Market Scope: Inquiry Before Buying

| Data Center Power Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 35.23 USD Billion |

| Forecast Period 2026-2032 CAGR: | 7.45% | Market Size in 2034: | 67.26 USD Billion |

| Segments Covered: | By Component | Electrical Solutions Uninterruptible Power Supply (UPS) Systems Power Distribution Units (PDU) On-Site Power Generation & Energy Storage Power Management Software & DCIM Services Design & Consulting Integration & Deployment Support & Maintenance |

|

| By Tier Type | Tier I & Il Tier III Tier IV |

||

| By Data Center Type | Enterprise Hyperscale Colocation Edge Others |

||

| By Data Center Size (Power Capacity) | Small-sized Data Center (less than 1 MW) Mid-sized Data Center (1 MW TO 5 MW) Large Data Center (5MW TO 10 MW) Mega-sized Data Center (10 MW TO 100 MW) Massive Data Center (over 100 MW) |

||

| By Application | Cloud Computing Big Data Analytics Internet of Things (IoT) Artificial Intelligence and Machine Learning Content Delivery Networks (CDNs) High Performance Computing (HPC) Disaster Recovery & Backup Others |

||

| By End Use Industry | IT and Telecommunications BFSI (Banking, Financial Services, and Insurance) Media and Entertainment Healthcare and Life Sciences Government, Military, and Defense Retail and E-commerce Manufacturing and Industrial Automation Others |

||

Data Center Power Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Data Center Power Key Players include

- Schneider Electric

- Eaton Corporation

- Vertiv Group Corp.

- Siemens AG

- ABB Ltd.

- Huawei Technologies Co., Ltd.

- Delta Electronics, Inc.

- Legrand SA

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Fuji Electric Co., Ltd.

- Socomec Group

- Riello UPS

- Piller Power Systems

- AEG Power Solutions

- CyberPower Systems, Inc.

- Active Power

- Cummins Inc.

- Generac Power Systems, Inc.nVent

- Panduit Corporation

- Rittal GmbH & Co. KG

- Hitec Power Protection

- Clary Corporation

- Zigor Corporation

- Borri S.p.A.

- EnersyOthers

Frequently Asked Questions

1. What is driving the growth of the Data Center Power Market?

Ans: The growth of the Data Center Power Market is primarily driven by the exponential growth in data generation, increasing demand for cloud computing, the expansion of edge computing, and the need for high availability and reliability in data centers.

2. How are data centers ensuring high availability and reliability in power solutions?

Ans: Data centers ensure high availability and reliability by implementing redundant power systems, backup generators, and advanced uninterruptible power supplies (UPS). These measures help prevent power disruptions that could lead to financial losses and reputational damage.

3. What are the key trends affecting the data center industry today?

Ans: Some of the key trends affecting the data center industry include data localization, sustainable data centers, and the rise of edge connectivity. Data localization is driven by government regulations, while sustainable data centers aim to reduce environmental impact. Edge data centers enhance user experience by processing data closer to the end user.

4. How has data localization impacted the Data Center Power Market in India?

Ans: Data localization rules in India emphasize the need to store sensitive consumer data within the country's borders. This has led to an increase in the demand for local data centers. India's cost advantage and access to skilled workers make it a prominent hub for data centers in the Asia Pacific region.

5. What role does energy efficiency play in data centers?

Ans: Energy efficiency is crucial in data centers due to their high power consumption. Data center operators are investing in energy-efficient technologies, renewable energy sources, and advanced cooling solutions to reduce operational costs and minimize environmental impact.

Table of Contents

- Global Data Center Power Market Size (Value in USD Mn,), 2025–2032

- Comprehensive Overview of Global Data Center Space and Power Availability Trends

- Key Insights on Power Constraints Impacting Data Center Expansion Globally

- Strategic Importance of Europe in the Global Data Center Infrastructure Ecosystem

- Summary of Demand-Supply Imbalance Across Major Data Center Markets

- Identification of Emerging Investment Hotspots Based on Power Availability

- Analyst Recommendations for Data Center Expansion and Infrastructure Strategy

- Analysis of Installed Data Center Capacity in Megawatts Across Global Regions

- Evaluation of Total White Space Availability and Utilization Rate Trends

- Growth Analysis of Hyperscale and Colocation Data Center Segments Worldwide

- Historical Trends in Data Center Capacity Expansion Across Major Markets

- Forecast of Data Center Capacity Additions Through 2032 Timeline

- Regional Contribution to Global Data Center Capacity Growth and Expansion

- Market Trends

- Market DROC Analysis

- Market Drivers

- Market Restraints

- Opportunities

- Challenges

- PORTER’S Five Forces Analysis

- PESTLE Analysis

- Assessment of Total Energy Consumption by Data Centers at Global Level

- Impact of Artificial Intelligence and Cloud Growth on Power Demand

- Regional Variation in Power Usage Intensity Across Data Center Facilities

- Influence of High-Performance Computing Workloads on Energy Consumption

- Future Projections of Global Data Center Electricity Demand Growth

- Role of Energy Efficiency Improvements in Managing Power Consumption

- Analysis of Rack Space Availability and Occupancy Trends Across Global Markets

- Evaluation of Vacancy Rates in Tier I and Tier II Data Center Locations

- Assessment of Land Availability Constraints in Major Data Center Hubs

- Comparison of Expansion Challenges in Urban Versus Remote Locations

- Adoption of Modular and Vertical Data Center Designs to Optimize Space

- Future Outlook for Data Center Space Availability Across Global Regions

- Evaluation of Power Availability Across Major Global Data Center Regions

- Analysis of Grid Infrastructure Limitations Impacting Data Center Growth

- Assessment of Time-to-Power Delays in Key Data Center Markets

- Examination of Utility Dependency and Grid Connectivity Challenges

- Availability of Renewable Energy Sources Across Global Data Center Regions

- Planned Upgrades and Investments in Global Power Infrastructure Networks

- Comparative Analysis of Data Center Demand Versus Available Capacity Globally

- Identification of Regions Experiencing Critical Power Supply Shortages

- Evaluation of Markets with Underutilized Capacity and Excess Infrastructure

- Impact of AI and Cloud Growth on Resource Demand Imbalance

- Forecast of Supply-Demand Gap Trends Across Global Markets

- Strategic Implications of Resource Gaps for Investors and Operators

- Overview of Europe’s Role in Global Data Center Infrastructure Development

- Analysis of Installed Capacity Across Key European Data Center Markets

- Key Growth Drivers Including Cloud, AI and Digital Transformation Trends

- Impact of Regional Policies on Data Center Development and Expansion

- Competitive Positioning of Europe Compared to US and APAC Markets

- Future Outlook for Europe’s Data Center Market Growth

- Evaluation of Power Availability Across Major European Data Center Hubs

- Analysis of Grid Congestion Challenges in FLAP-D Markets

- Integration of Renewable Energy into European Data Center Operations

- Government Restrictions Impacting Power Allocation for Data Centers

- Impact of Power Connection Delays on Project Timelines

- Future Grid Expansion Plans Across European Countries

- Analysis of Colocation and Hyperscale Space Availability Across Europe

- Assessment of Land Scarcity in Major European Data Center Cities

- Regulatory Challenges Impacting Land Acquisition and Development

- Shift Toward Secondary Markets Due to Space Constraints

- Adoption of Vertical Expansion Strategies in Dense Urban Locations

- Future Outlook for Space Availability in European Data Center Market

- Detailed Analysis of Frankfurt Data Center Capacity and Power Constraints

- Evaluation of London Market Expansion and Grid Limitations

- Assessment of Amsterdam Regulatory Restrictions and Growth Challenges

- Analysis of Paris Data Center Capacity and Infrastructure Development

- Impact of Power Shortages and Moratoriums in Dublin Market

- Comparative Benchmarking of FLAP-D Markets Across Key Metrics

- Growth Trends in Emerging Markets Including Milan, Madrid and Warsaw

- Availability of Land and Power Resources in Secondary European Locations

- Investment Attractiveness of Eastern Europe Data Center Markets

- Cost Advantages Compared to Primary Data Center Hubs

- Strategic Shift of Operators Toward Less Saturated Markets

- Future Growth Outlook for Secondary European Data Center Locations

- Abundant Availability of Renewable Energy in Nordic Data Center Markets

- Role of Hydropower and Wind Energy in Supporting Data Center Growth

- Cost Advantages Due to Low Electricity Prices in Nordic Countries

- Climate Benefits Supporting Energy Efficient Data Center Operations

- Increasing Investments by Hyperscale Operators in Nordic Region

- Future Expansion Potential of Nordic Data Center Infrastructure

- Analysis of Data Center Capacity Growth Across Asia-Pacific Region

- Evaluation of Power Availability Challenges in Major APAC Cities

- Government Incentives Supporting Data Center Infrastructure Development

- Land Constraints in High-density Urban Locations Across APAC

- Comparative Analysis with European and North American Markets

- Future Outlook for Data Center Growth in APAC Region

- Overview of North America’s Dominance in Global Data Center Capacity

- Availability of Large-scale Power Infrastructure in the United States

- Expansion Trends in Secondary Data Center Markets Across North America

- Adoption of Renewable Energy Across Data Center Facilities

- Land Availability Advantages Compared to European Markets

- Comparative Analysis of Resource Availability Across Regions

- Detailed Cost Breakdown of UPS, PDUs, Switchgear and Generator Systems

- Impact of Energy Cost Inflation on Data Center Profitability Margins

- Comparative Analysis of Cost per Megawatt Across Global Regions

- Influence of Logistics, Installation and Import Duties on Cost Structure

- Profitability Comparison Across OEMs, EPCs and System Integrators

- Impact of Power Availability Constraints on Overall Infrastructure Costs

- Global Benchmarking of Power Usage Effectiveness Across Data Centers

- Key Factors Impacting PUE Including Cooling and Load Distribution

- Strategies Adopted by Operators to Achieve Low PUE Levels

- Role of Artificial Intelligence in Optimizing Energy Efficiency

- Comparative Analysis of PUE Across Regions and Data Center Tiers

- Impact of Power Constraints on Achieving Optimal Efficiency Levels

- Increasing Power Demand Due to High-density AI and GPU Workloads

- Analysis of Rack-level Power Requirements in Modern Data Centers

- Differences Between AI Training and Inference Power Consumption

- Impact of Liquid Cooling Adoption on Power and Space Efficiency

- Infrastructure Upgrades Required for Supporting AI-driven Workloads

- Impact of AI Growth on Regional Power Demand Imbalance

- Analysis of Buyer Priorities Including Reliability and Efficiency

- Evaluation Criteria Used in Vendor Selection and Procurement Processes

- Increasing Adoption of Prefabricated and Modular Power Solutions

- Role of ESG Considerations in Procurement Decision-making

- Sensitivity to Downtime Costs in Hyperscale and Colocation Markets

- Preference for Locations with Reliable Power Availability

- Evolution from Traditional to Modular Data Center Power Architectures

- Analysis of Redundancy Configurations for High Availability Systems

- Comparison of Rack-level, Row-level and Room-level Power Distribution

- Mapping of Power Losses and Heat Generation Across Systems

- Integration of DC Power Systems and Busway Architectures

- Design Considerations for High-density and AI-driven Workloads

- Impact of PUE Optimization on Power Infrastructure Design

- Adoption of High-efficiency UPS Systems and Advanced Technologies

- Integration of Renewable Energy Sources in Data Center Operations

- Transition Toward Advanced Battery Technologies for Sustainability

- Implementation of Waste Heat Recovery and Energy Reuse Systems

- Role of Smart Power Management in Reducing Carbon Footprint

- Comparison of Power Strategies Across Hyperscale, Colo and Enterprise

- Power Requirements for AI and Machine Learning Workloads

- Operational Benchmarks for Efficiency and Uptime Performance

- Adoption of Multi-source Energy Procurement Models

- Comparison of In-house Versus Outsourced Power Management

- Importance of Location Selection Based on Space and Power Availability

- Adoption of AI-driven Power Monitoring and Predictive Analytics

- Advancements in UPS Technologies and Battery Chemistries

- Development of Intelligent Power Distribution Units

- Emergence of Software-defined Power Infrastructure Systems

- Growth of Modular and Plug-and-play Power Solutions

- Innovation Focus on Addressing Power Constraints and Efficiency

- Analysis of Common Failure Risks in Data Center Power Systems

- Root Causes of Power Outages and Cascading Failures

- Battery Degradation and Thermal Runaway Challenges

- Cybersecurity Risks in Connected Power Infrastructure

- Reliability Metrics Including MTBF and MTTR Analysis

- Impact of Grid Dependency on Operational Risks

- Assessment of Raw Material and Battery Supply Chain Risks

- Overview of OEM, EPC and System Integrator Ecosystem

- Lead-time Challenges for Critical Power Infrastructure Components

- Installation Bottlenecks in Large-scale Data Center Projects

- Spare Parts Management and Lifecycle Support Strategies

- Regional Supply Chain Gaps Impacting Project Execution

- Evaluation of Market Attractiveness Across Data Center Segments

- Identification of High-growth Investment Hotspots Globally

- ROI Analysis for Power Infrastructure Modernization Projects

- Key Risk Factors Including Energy Costs and Grid Limitations

- Government Incentives Supporting Data Center Investments

- Investment Feasibility Based on Space and Power Availability

- Assessment of Carbon Neutrality Targets Across Regions

- Adoption of Circular Energy Models Including Heat Reuse

- Lifecycle Carbon Footprint Analysis of Data Center Infrastructure

- Impact of Green Certifications on Market Positioning

- Role of AI in Achieving Sustainability Objectives

- Regional Comparison of ESG Performance in Data Center Markets

- Overview of Power Consumption Regulations Across Global Markets

- Renewable Energy Mandates and Government Incentive Programs

- Carbon Emission Targets and Compliance Requirements

- Grid Reliability Standards and Utility Regulations

- Data Sovereignty Policies Impacting Infrastructure Deployment

- Impact of European Policy Restrictions on Data Center Growth

- Assessment of Utility Power Availability Across Key Regions

- Analysis of Grid Interconnection Timelines and Approval Processes

- Development of On-site Substations and High-voltage Access

- Participation in Demand Response and Grid Stabilization Programs

- Risk of Power Curtailment in Constrained Markets

- Comparative Analysis of Grid Accessibility Across Regions

- Differences Between Core and Edge Data Center Power Architectures

- Power Requirements for Micro Data Centers and Edge Deployments

- Deployment Challenges in Low-grid Stability Locations

- Adoption of DC Power Systems in Edge Infrastructure

- Modular and Containerized Power Solutions for Edge Facilities

- Role of Edge Computing in Reducing Core Data Center Load

- Comparison of Greenfield and Brownfield Expansion Strategies

- Power Density Upgrades in Existing Data Center Facilities

- Replacement Cycles for Legacy Power Infrastructure Systems

- Constraints on Expansion Due to Limited Power Availability

- Future Pipeline of Data Center Capacity Additions

- Long-term Outlook for Global Space and Power Availability

- Global Data Center Power Market Size and Forecast, by Component

- Electrical Solutions

- Uninterruptible Power Supply (UPS) Systems

- Power Distribution Units (PDU)

- On-Site Power Generation & Energy Storage

- Power Management Software & DCIM

- Services

- Design & Consulting

- Integration & Deployment

- Support & Maintenance

- Global Data Center Power Market Size and Forecast, by Tier Type

- Tier I & Il

- Tier III

- Tier IV

- Global Data Center Power Market Size and Forecast, By Data Center Type

- Enterprise

- Hyperscale

- Colocation

- Edge

- Others

- Global Data Center Power Market Size and Forecast, by Data Center Size (Power Capacity)

- Small-sized Data Center (less than 1 MW)

- Mid-sized Data Center (1 MW TO 5 MW)

- Large Data Center (5MW TO 10 MW)

- Mega-sized Data Center (10 MW TO 100 MW)

- Massive Data Center (over 100 MW)

- Global Data Center Power Market Size and Forecast, by Application

- Cloud Computing

- Big Data Analytics

- Internet of Things (IoT)

- Artificial Intelligence and Machine Learning

- Content Delivery Networks (CDNs)

- High Performance Computing (HPC)

- Disaster Recovery & Backup

- Others

- Global Data Center Power Market Size and Forecast, by End Use Industry

- IT and Telecommunications

- BFSI (Banking, Financial Services, and Insurance)

- Media and Entertainment

- Healthcare and Life Sciences

- Government, Military, and Defense

- Retail and E-commerce

- Manufacturing and Industrial Automation

- Others

- Global Data Center Power Market Size and Forecast, by Region

- North America

- United States

- Mexico

- Canada

- Europe

- United Kingdom

- France

- Germany

- Italy

- Spain

- Sweden

- Russia

- Poland

- Rest of Europe

- Asia Pacific

- China

- South Korea

- Japan

- India

- Australia

- New Zealand

- Indonesia

- Philippines

- Malaysia

- Vietnam

- Thailand

- Rest of Asia Pacific

- Middle East and Africa

- South Africa

- GCC

- Turkey

- Egypt

- Nigeria

- Rest of ME&A

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest Of South America

- Company Overview

- Financial Overview

- SWOT Analysis

- Strategic Analysis

- Recent Developments

- Schneider Electric

- Eaton Corporation

- Vertiv Group Corp.

- Siemens AG

- ABB Ltd.

- Huawei Technologies Co., Ltd.

- Delta Electronics, Inc.

- Legrand SA

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Fuji Electric Co., Ltd.

- Socomec Group

- Riello UPS

- Piller Power Systems

- AEG Power Solutions

- CyberPower Systems, Inc.

- Active Power

- Cummins Inc.

- Generac Power Systems, Inc.

- nVent

- Panduit Corporation

- Rittal GmbH & Co. KG

- Hitec Power Protection

- Clary Corporation

- Zigor Corporation

- Borri S.p.A.

- Enersys

- Comprehensive Overview of Leading Global Data Center Power Infrastructure Providers

- Market Share Analysis Across UPS, Switchgear and Power Management Segments

- Regional Presence and Operational Footprint of Key Industry Participants

- Competitive Positioning Based on Capacity, Technology and Service Capabilities

- Strategic Differentiation Approaches Adopted by Leading Market Players

- Future Outlook for Competitive Dynamics in Data Center Power Market

- Business Models and Revenue Streams of Global Colocation Providers

- Strategies to Optimize Space Utilization and Power Efficiency

- Expansion Plans Across High-demand and Emerging Data Center Markets

- Pricing Models Based on Power Consumption and Rack Space Allocation

- Customer Acquisition Strategies in Competitive Colocation Market

- Competitive Positioning Based on Reliability and Infrastructure Capabilities

- Overview of Key Data Center Operators Active in European Market

- Capacity Distribution Across FLAP-D and Secondary European Markets

- Strategies to Address Power Constraints and Grid Limitations in Europe

- Expansion Strategies Beyond Primary Markets into Emerging Locations

- Adoption of Renewable Energy and Sustainability Initiatives in Europe

- Competitive Benchmarking of European Data Center Service Providers

- Adoption of Renewable Power Purchase Agreements by Data Center Operators

- Investment in Captive Power Generation and On-site Energy Infrastructure

- Strategies to Reduce Dependency on Grid-based Power Supply Systems

- Energy Cost Optimization Approaches Across Global Data Center Operators

- Long-term Sustainability Goals and Carbon Neutrality Commitments

- Comparative Analysis of Power Procurement Strategies Across Companies

- Planned Investments in New Data Center Infrastructure Developments

- Regional Capacity Expansion Strategies Across Global Markets

- Strategic Partnerships with Governments and Utility Providers

- Role of Mergers, Acquisitions and Joint Ventures in Expansion

- Focus on High-growth Regions Based on Power Availability

- Future Outlook for Capacity Expansion by Leading Operators

- Carbon Neutrality and Net-zero Commitments by Leading Operators

- Adoption of Renewable Energy Sources Across Data Center Facilities

- Implementation of Energy-efficient Technologies and Cooling Solutions

- ESG Reporting Standards and Sustainability Performance Metrics

- Green Building Certifications and Environmental Compliance Practices

- Future Roadmap for Sustainable Data Center Infrastructure Development

- Deployment of AI-driven Infrastructure Monitoring and Automation Systems

- Adoption of Advanced Cooling Technologies for High-density Workloads

- Integration of Intelligent Power Distribution and Load Management Systems

- Implementation of Software-defined Power Infrastructure Solutions

- Investment in Edge Computing and Distributed Data Center Architectures

- Future Technology Roadmap of Leading Data Center Operators

- Entry Strategies into Emerging Markets with High Growth Potential

- Expansion Beyond Tier I Cities Driven by Space and Power Constraints

- Investment Focus Across Europe, APAC and North America Regions

- Location Selection Strategies Based on Power and Land Availability

- Collaboration with Local Governments and Infrastructure Providers

- Future Regional Expansion Plans of Major Data Center Companies

- Analysis of Recent Mergers and Acquisitions in Data Center Industry

- Strategic Partnerships Between Operators and Cloud Service Providers

- Joint Ventures with Energy Companies for Power Infrastructure Development

- Impact of M&A Activities on Market Consolidation Trends

- Partnerships Focused on Renewable Energy and Sustainability Goals

- Future Outlook for Strategic Alliances in Data Center Market

- Pricing Models Based on Power Consumption and Rack Space Allocation

- Regional Variations in Pricing Across Major Data Center Markets

- Impact of Energy Costs on Pricing Strategies and Profit Margins

- Revenue Segmentation Across Hyperscale and Colocation Services

- Competitive Pricing Strategies Adopted by Leading Providers

- Future Trends in Data Center Pricing and Monetization Models

- Comparative Analysis of Data Center Capacity Across Leading Operators

- Benchmarking of Infrastructure Capabilities and Service Offerings

- Evaluation of Power Efficiency Metrics and Utilization Rates

- Regional Distribution of Capacity Across Key Industry Players

- Competitive Advantages Based on Scale and Technological Capabilities

- Future Trends in Capacity Benchmarking and Performance Metrics

- Strategies to Mitigate Power Supply Risks and Grid Dependencies

- Management of Regulatory and Environmental Compliance Challenges

- Investment in Resilient and Redundant Infrastructure Systems

- Cybersecurity Risk Management in Smart Power Infrastructure

- Operational Risk Mitigation Through Diversification of Locations

- Future Risk Management Approaches Across Data Center Operators

- Investment in Next-generation Data Center Power Technologies

- Development of Energy-efficient and Sustainable Infrastructure Solutions

- Research in Advanced Cooling and Power Management Systems

- Innovation in Modular and Scalable Data Center Designs

- Collaboration with Technology Providers for Continuous Innovation

- Future R&D Focus Areas in Data Center Power Infrastructure

- Long-term Strategic Priorities of Leading Data Center Companies

- Expansion Plans Aligned with Power and Space Availability Trends

- Increasing Focus on Sustainability and Energy Efficiency Initiatives

- Competitive Positioning in Evolving Global Data Center Market

- Anticipated Shifts in Market Leadership and Competitive Landscape

- Future Outlook for Growth and Investment Strategies

- C1. Key Findings

- C2.Analyst Recommendation

- C3. Research Methodology