Global Cosmetics Surgery Products Market Size by Types , End User, Application and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

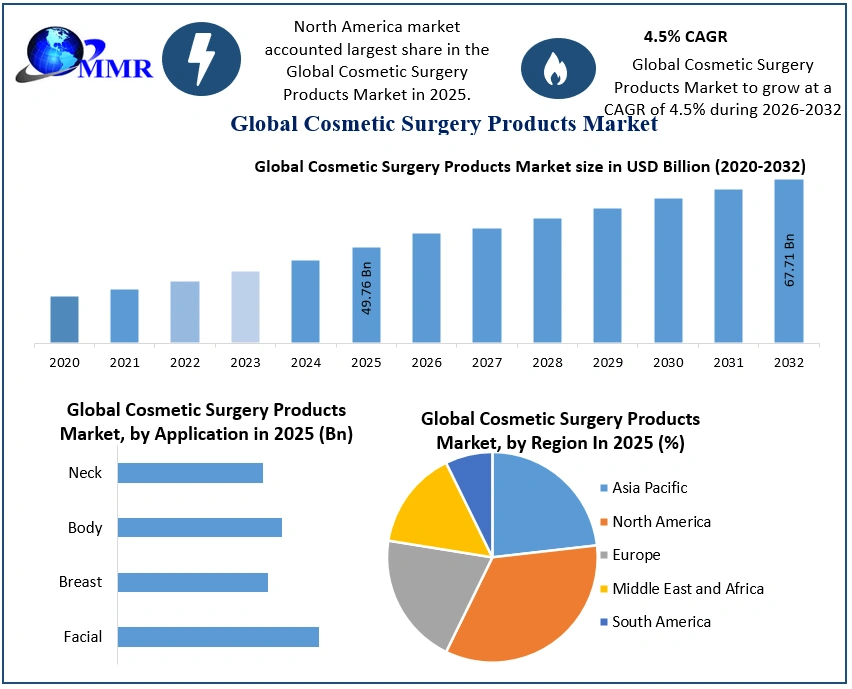

The Cosmetic Surgery Products Market size was valued at USD 49.76 Billion in 2025 and the total Cosmetic Surgery Products revenue is expected to grow at a CAGR of 4.5% from 2025 to 2032, reaching nearly USD 67.71 Billion by 2032.

Cosmetics Surgery ProductsMarket Overview & Dynamics:

Cosmetic surgery is a unique discipline of medicine, which is focused on enhancing physical appearance through surgical and medical techniques. Cosmetic surgery can be performed on all areas of the head, neck, and body. Cosmetic surgery continues to grow in popularity, with xx million cosmetic procedures carried out in the United States in 2019, an increase of 3 percent on the previous year.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Rise in the demand for minimally invasive surgical procedures is expected to boost the market growth.

The demand for cosmetics surgeries using minimally invasive methods, like botulinum toxin and facial filler injections have increased dramatically over the past decade and which is anticipated to drive the market during the forecast period. Major demand for these procedures has been observed in the US for the past few years. The main benefit of cosmetic surgery is that it helps to align your natural appearance with your desired appearance, resulting in an improved version of yourself. It also sometimes benefits in enhancing physical health, for example, a rhinoplasty surgery, not only will enhance the look and shape of your nose but may also help with respiratory issues that you may have. Along with physical health, it also helps in improving the psychological health of an individual, which helps him socialize due to an improved state of mind regarding how you feel towards yourself.

Another key advantage to cosmetic surgery is that it produces results that often last a long time or are permanent. Due to the higher demand for cosmetic surgeries, it has become easily accessible and many clinics have been set up. These key benefits for cosmetic surgeries contribute to the growth of the market. Other driving factors for the market also include rising disposable income, increasing social awareness, rising demand for these procedures in the entertainment industry, and an increase in the number of traumatic injuries requiring reconstructive changes.

High cost of cosmetic surgeries may hamper the market growth.

Expensive cosmetic surgeries become ‘not so easily accessible’ in many developing and middle-income economies. This proves as the main factor which may hamper the market growth. Many times, recovery time can be long about 2-3 weeks, which may restrain the market from growing. Also, no availability of reimbursement policies in developed nations slows down the growth rate.

The report covers the detailed analysis of global Cosmetic Surgery Products industry with the classifications of the market. Analysis of past market dynamics from 2020 to 2025 is given in the report, which will help readers to benchmark the past trends with current market scenarios with the key players contribution in it.

The report has profiled nineteen key players in the market from different regions. However, report has considered all market leaders, followers and new entrants with investors while analyzing the market and estimation the size of the same. Increasing R&D activities in each region are different and focus is given on the regional impact on the cost, availability of advanced technology are analyzed and report has come up with recommendations for future hot spot in APAC region.

Regional Insights:

North America is expected to hold a dominant share of xx% during forecast period.

Owing to the rising number of people focusing on the external aesthetics, rising geriatric population pool, and the improvements that is being done in cosmetic procedures, North America is expected to dominate the global market by holding a significant share of xx%. Rising number of trauma cases and accidents, increasing awareness, advancements in R&D for improving and addition of the new advanced techniques and new product launches are few key factors responsible to raise the bar of the market in the region.

Asia Pacific is expected as the fastest growing region during forecast period at a CAGR of xx%.

The Asia Pacific will command the global market owing to the drivers like improved medical infrastructure, presence of large target population, for example, rising demand for these procedures in the entertainment industry, adaptation of minimally invasive techniques, increased awareness, development of innovative and cost-effective solutions, improved standard of living, and rise in disposable income. The market is anticipated to experience fast development in demand for Cosmetic Surgery Products in emerging countries such as Japan, China, Brazil, India, Indonesia, and South Korea over the forecast period.

Segment Analysis:

The global Cosmetic Surgery Products Market is segmented based on types, applications, and end-users. On the basis of type, it is sub-segmented into Injectables, implants, equipment, and others. The implants segment accounted for the major share of the market, with almost xx% of the total market in 2025, and is expected to show steady growth over the next five years. The implants segment consists of surgeries such as breast implants, facial implants, nose implants, and ear implants. Both invasive and non-invasive surgical procedures are used to embed cosmetic implants in an individual’s body.

Patients are opting to replace their damaged/missing body parts, recover their normal appearance, and enhance their aesthetic beauty owing to the development of cosmetic implants. The cosmetic implants market has witnessed several acquisitions & mergers in recent years. For instance, in February 2016, DENTSPLY International Inc. and Sirona Dental Systems, Inc. merged together to form DENTSPLY Sirona Inc. to provide a strong and wide range of professional dental products and technologies to customers across 120 countries globally.

Based on the applications segment, it is diversified into facial, breasts, body, neck, and others. The facial implants segment is the fastest-growing segment due to the growing demand for chin and cheek plastic surgeries. They are available in a wide range of sizes and styles and restore contour and proportion to your face. Along with this, the increasing prevalence of breast cancer has increased the demand for breast augmentation and breast lift procedures.

Scope of the report: Inquire before Buying

| Global Cosmetics Surgery Products Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2025-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 49.76 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.5% | Market Size in 2032: | USD 67.71 Bn. |

| Segments Covered: | by Types | Injectables Implants Equipments Others |

|

| by End User | Hospitals Ambulatory Surgical Centers Clinics |

||

| by Application | Facial Breast Body Neck |

||

Cosmetic Surgery Products Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Cosmetic Surgery Products Market, Key Players are

1. Allergan

2. Mentor Corporation

3. Candela Corp

4. Cutera Inc

5. Lumenis Ltd.

6. Palomar Medical

7. Iridex Corp

8. Solta Medical

9. DermaMed Pharmaceutical Inc

10. Medtronic plc

11. Johnson & Johnson Services Inc.

12. Syneron Medical Ltd.

13. Cynosure Inc.

14. Alma Lasers, Ltd

15. Genesis Biosystems

16. Merz Aesthetics

17. Sanofi S.A.

18. Smith & Nephew plc

19. DENTSPLY Sirona plc.

Frequently Asked Questions:

1] What segments are covered in Global Cosmetic Surgery Products Market report?

Ans. The segments covered in Market report are based on Product, Type, and End-Use.

2] Which region is expected to hold the highest share in the Global Cosmetic Surgery Products Market?

Ans. North America is expected to hold the highest share in the Burn Ointment Market.

3] Which segment holds the largest market share in the Global Cosmetic Surgery Products Market by 2032?

Ans. Topical Antibiotics segment hold the largest market share in the market by 2032.

4] What is the market size of the Global Cosmetic Surgery Products Market by 2032?

Ans. The market size of the market is expected to reach USD 67.71 Bn. by 2032.

5] What was the market size of the Global Cosmetic Surgery Products Market in 2025?

Ans. The market size of the market was worth USD 49.76 Bn. in 2025.