Battery Additives Market by Type, Application, End-User, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

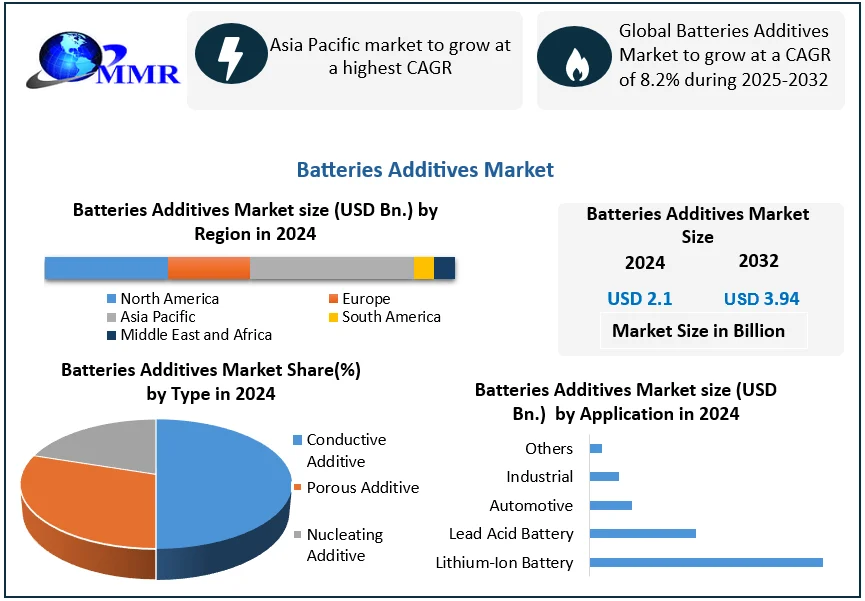

Global Batteries Additives Market size was valued at USD 2.1 Bn. in 2024, and the total Batteries Additives Market revenue is expected to grow by 8.2% from 2025 to 2032, reaching nearly USD 3.94 Bn.

Batteries Additives Market Overview:

Battery additives are chemical compounds and materials used in battery manufacturing to improve performance, enhance safety, and extend service life. According to the report, battery additives play a crucial role in modifying electrolyte properties, reducing sulfation, improving charge acceptance, preventing corrosion, and supporting other critical functions in lead-acid batteries, lithium-ion batteries, and next-generation battery technologies.

The report highlights a consistent supply of new additive formulations, including established consumables within a robust battery production supply chain. These additives are widely used in applications related to general battery production. The growing demand for electric vehicle (EV) batteries, renewable energy storage systems, and portable electronics is significantly driving the growth of the Batteries Additives Market.

Asia-Pacific holds the largest Batteries Additives market share, driven by strong battery manufacturing industries in countries like China, Japan, and South Korea. This region is followed by North America and Europe, where continued investments in clean energy storage solutions are fueling market growth.

Major key players mentioned in the report include Cabot Corporation, Hammond Group, 3M, Borregaard, and Orion Engineered Carbons. Automotive batteries remain the largest end-user segment, followed by industrial and consumer electronics. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Batteries Additives Market Dynamics

Performance and sustainable batteries to drive the Batteries Additives Market growth

The growth of the Batteries Additives Market is mainly driven by the growing demand for high-performance batteries in electric vehicles (EVs), consumer electronics, and renewable energy storage systems. By 2025, the rapid global transition to sustainable transportation, along with stringent emission regulations, is forcing automobile manufacturers and battery manufacturers to use additives that improve capacity, battery life, and battery charge time. Notably, improvements in additive technologies, especially new conductive and nucleating materials for better thermal stability and energy density, are expanding the usage of additives. Additionally, the report observed that continued R&D investment and partnerships between material suppliers and battery OEMs reinforce the upward trend.

Innovation Technologies to create Batteries Additives Markets Opportunity

Emerging economies, particularly in the Asia-Pacific region, along with countries such as Brazil, Mexico, and Chile in Latin America, are heavily investing in local battery manufacturing facilities. These investments are expected to create additional supplier opportunities by 2032. As the focus on solid-state and advanced lithium-sulfur batteries increases, there is significant potential for the development of new and innovative additive solutions that help mitigate dendrite formation and enhance safety.

Furthermore, with growing government support for clean energy storage projects, there is even greater opportunity for additive manufacturers to develop new products and expand into emerging markets.

High Capital Investments and Supply Chain Reliability to create Batteries Additives Market Challenges

High capital investments are required for the research and development of advanced additives and the formulation of specialty chemicals for new battery chemistries. The Batteries Additives Markets face challenges due to continuous pricing fluctuations, supply chain disruptions, and increased overall production costs driven by the development of new and innovative applications. Several pilot projects involving new battery chemistry formulations are currently in the pipeline.

The introduction of a regulatory standard in 2025, focused on quality and safety, is expected to significantly increase testing requirements. This delays battery readiness and reduces production profitability, as retailers are unlikely to adjust their margins, and manufacturing capacity may not improve due to these added challenges.

The Batteries Additives Market consists of both well-established chemical companies and new entrants, all operating under strong market commitments. This competitive landscape contributes to additional pricing pressure across the industry.

Regulatory and Environmental Constraints to Restrain Batteries Additives Market

The main restraints affecting the Battery Additives Market include environmental concerns related to the disposal and recyclability of chemical additives. Additionally, regulatory agencies worldwide are implementing stricter standards to reduce the ecological footprint of battery manufacturing. This compels additive suppliers to develop greener alternatives, which directly impacts their ability to scale production in the short term. Limited knowledge and implementation of the distinct additives by smaller battery producers, particularly in developing markets, also restricts wider market penetration.

The report study has analyzed the revenue impact of the COVID-19 pandemic on the sales revenue of market leaders, market followers, and disrupters in the report, and the same is reflected in our analysis. The additive treatments may be most effective with older battery models, extending their life by a few months until a replacement. Current batteries already contain additives that diminish sulfation and corrosion. Industrial users seldom depend on helpful additives to prolong battery life as the system becomes maintenance-prone. In past years, the global lithium-ion battery market has experienced strong growth. This can be attributed to the increasing applications of lithium-ion batteries in the production of electric vehicles and solar electric systems, owing to their lightweight, high-energy density, and small memory impact.

The battery electric vehicle is boosting the growth of the market because of the strong interest of the private sector to invest in electric vehicle charging infrastructure globally. Also, increasing investments in renewable energy increase market growth. Underdeveloped support infrastructure for EVs and severe safety issues related to batteries are hampering the progress of the global Batteries Additives Market.

Rules and safety issues related to lead-acid batteries are the major challenges to the growth of the market. The global Batteries Additives Market is expected to create opportunities owing to technical advancements in Li-ion batteries. In 2023, the lead-acid application segment held the largest share of the global Batteries Additives Market. But lithium-ion battery is expected to grow rapidly during the forecast period owing as Li-ion batteries are usually used in many applications like smartphones, tablets, laptops, wearable devices, and other home applications.

Battery additives used in the Li-ion application upsurge storage stability, safety, and performance of batteries. According to the global market analysis, the market of Asia Pacific is anticipated to dominate during the upcoming years, owing to the high demand for battery additives in developing economies such as China and India. The progress of the Batteries Additives Market in the Asia Pacific is mostly driven by high demand in portable devices and electric vehicle applications. Also, increasing population and growing end-user industries have led to invention and improvement, which are building the Asia Pacific into an industrial center, and worldwide is driving the market growth.

Batteries Additives Market Segment Analysis:

Based on Type, Conductive additives dominate this category because they are essential for improving the electrical conductivity of battery electrodes. This directly enhances the overall battery performance, enabling higher power output, faster charging, and better efficiency, features that are critical for modern applications such as electric vehicles and portable electronics.

Based on Application, Lithium-ion batteries hold the largest share among applications because they are widely used in electric vehicles, smartphones, laptops, and renewable energy storage. Their high energy density, long cycle life, and lightweight nature make them the preferred choice for most new-age power storage solutions, driving robust demand for specialized additives.

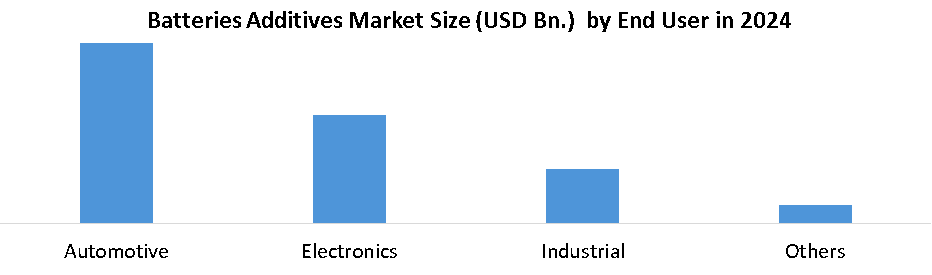

Based on End User, the automotive segment is the dominant end user because the rapid global adoption of electric and hybrid vehicles requires advanced batteries with longer life, better performance, and enhanced safety. To meet these requirements, manufacturers rely heavily on battery additives, cementing the automotive industry as the largest contributor to market revenue.

Batteries Additives Market Regional Analysis

The Asia-Pacific area has the largest market share for the global Battery Additives Market by already forming a strong battery manufacturing ecosystem and increasing demand for battery technology with electric vehicles (EVs), consumer electronics, and energy storage systems. The Asia-Pacific has manufacturers from China, South Korea, Japan, and India all together producing greater than 60% of lithium-ion batteries placed on the market, already establishing itself as the leader of the battery ecosystem. As the Asia-Pacific has government support of EV subsidies, clean energy policies, and substantial investments in battery research and development (R&D) investments along with supporting infrastructure, while also many other large battery manufacturers and raw material suppliers continue to. This all together forms continues to integrate the Asia-Pacific as the sole focal point for battery additives.

Batteries Additives Market Competitive Analysis

The battery additives are competitive and moderately consolidated, with key players: Cabot Corporation, 3M, Imerys, SGL Carbon, Borregaard, HOPAX, and PENOX. Larger players coexist with emerging Asian manufacturers like Tinci Materials and Capchem. The market is fiercely competitive, as companies devote substantial resources to innovation and investment in advanced types of electrolytes and conductive additives to produce longer-lasting and higher-performing batteries of all types, influenced more recently by the prevalence of more sustainable technologies used for Lithium-ion and lead-acid batteries.

Competition strategies include forming strategic collaborations with battery & electric vehicle OEMs, regional expansions, more recently of new capacities in Asia-Pacific, and new product developments that factor in sustainability. Companies in the battery additives market continue to rely on mergers and acquisitions to build a strong portfolio, streamline and secure raw materials supply sources, and stay compliant with internationally applicable, more stringent environmental regulations and guidelines. Overall, competition and technology will continue to flourish, continuously influencing product differentiation and expansion geographically within the substrate market.

Key Developments in the Batteries Additives Market

• April 2025, China, CATL

CATL launched its Naxtra sodium-ion battery brand, with mass production planned for December 2025. This reflects the company’s move to diversify battery chemistries and reduce additive-related safety risks

• October 2024, India, Asahi Kasei

At the Battery Show in Noida, Asahi Kasei unveiled a novel acetonitrile-based electrolyte additive designed to improve low-temperature performance, thermal durability, and energy density in lithium-ion batteries. It’s slated for global commercialization in 2025

• October 2023, Germany, Orion (via U.S. facility)

Orion broke ground on a U.S. plant in La Porte, Texas, dedicated to producing acetylene-based conductive additives for lithium-ion applications, featuring a significantly reduced carbon footprint compared to conventional alternatives.

Key Trends in Batteries Additives Market

• Shift Towards Advanced Conductive Additives for High-Performance Batteries

Manufacturers are increasingly focusing on high-efficiency conductive additives such as carbon nanotubes, graphene, and acetylene black to meet the performance demands of next-generation lithium-ion batteries.

For example:

1. Over 50% of battery additive demand by volume is projected to come from conductive additives by 2025, driven by the rapid adoption of electric vehicles (EVs).

2. Companies like Orion and Cabot Corporation have expanded production capacity for specialty conductive carbons by 30–40% in the past two years to cater to growing EV and portable electronics demand.

• Rising Demand for Eco-Friendly and Sustainable Additives

Environmental regulations and sustainability goals are pushing manufacturers to develop additives with lower environmental impact and improved recyclability. For instance:

1. Over 60% of new R&D spending in major battery additive companies now targets green and recyclable formulations.

2. Several companies, such as Asahi Kasei and Borregaard, have launched bio-based or less-toxic electrolyte additives, aiming for a 20–25% market share in green battery solutions by 2026.

Battery Additives Market Scope: Inquire before buying

| Global Batteries Additives Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 2.1 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 8.2% | Market Size in 2032: | USD 3.94 Bn |

| Segments Covered: | by Type | Conductive Additive Porous Additive Nucleating Additive |

|

| by Application | Lithium-Ion Battery Lead Acid Battery Automotive Industrial Others |

||

| by End User | Electronics Automotive Industrial Others |

||

Batteries Additives Market, by Region

North America (United States, Canada and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam, Indonesia, Philippines, Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America)

Batteries Additives Market, Key Players

North America

1. Cabot Corporation (Massachusetts, USA)

2. Orion Engineered Carbons (Texas, USA — with global HQ in Luxembourg)

3. 3M (Minnesota, USA)

4. Hammond Group, Inc. (Indiana, USA)

5. Superior Graphite (Illinois, USA)

Europe

6. Orion Engineered Carbons (European operations — HQ Luxembourg, production in Germany)

7. Borregaard (Sarpsborg, Norway)

8. Imerys S.A. (Paris, France)

9. Arkema S.A. (Colombes, France)

10. BASF SE (Ludwigshafen, Germany)

Asia-Pacific

11. Asahi Kasei Corporation (Tokyo, Japan)

12. Mitsubishi Chemical Holdings (Tokyo, Japan)

13. Shenzhen Sinuo Industrial Development Co., Ltd. (China)

14. Imerys Graphite & Carbon (Switzerland, but significant operations in Asia)

15. LG Chem Ltd. (Seoul, South Korea)

Frequently Asked Questions:

1. Which region has the largest share in the Global Batteries Additives Market?

Ans: The Asia Pacific region held the highest share in 2024.

2. What is the growth rate of the Global Market?

Ans: The Global Market is growing at a CAGR of 8.2% during the forecasting period 2025-2032.

3. What is the scope of the Global Batteries Additives Market report?

Ans: Global Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in the Global Batteries Additives Market?

Ans: The important key players in the Global Market are – Cabot Corporation, Hammond Group, Orion Engineered Carbons, IMERYS, 3M, ALTANA, Borregaard, HOPAX, PENOX, SGL Group, Colonial Chemical Corp, US Research Nanomaterials, MSC Industrial Supply, GETSOME Products, Tab-Pro LLC, Atomized Products Group, Fastenal, and Battery Equaliser USA

5. What is the study period of this market?

ANs: The Global Batteries Additives Market is studied from 2024 to 2032.