Autopilot System Market Size by Platform, Target Group, Component, Application, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

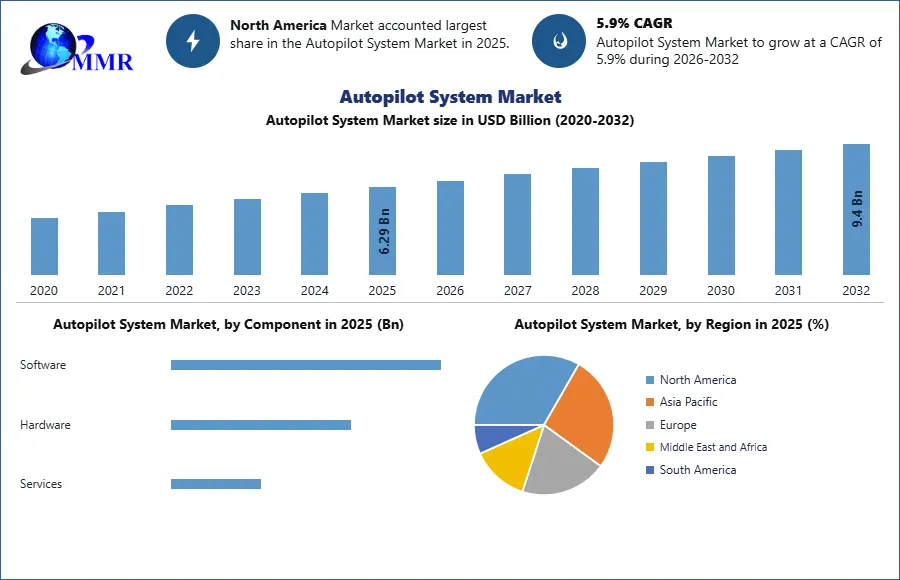

The Autopilot System Market size was valued at USD6.29 Billion in 2025 and the total Autopilot System revenue is expected to grow at a CAGR of 5.9% from 2026 to 2032, reaching nearly USD 9.40 Billion.

Autopilot System Market Overview:

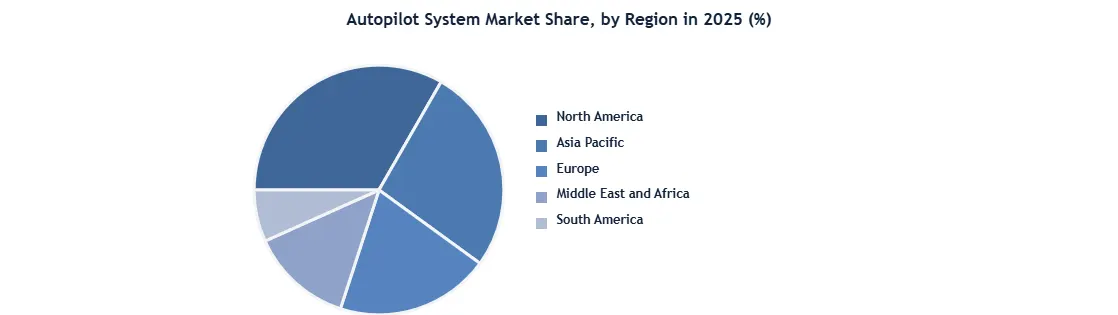

The Autopilot System Market is likely to be driven by rising demand for aircraft automation for increased fuel efficiency and to fulfill safety and security objectives, as well as the necessity for a precise navigation system. Research and development efforts to upgrade flying technology such as autopilot systems have seen a considerable increase, aided by increased expenditures in automation, resulting in various profitable growth opportunities for the market. The capacity to maintain a constant speed, position, and height of the aircraft heading, as well as reliable operation in low visibility or during flight system failures, is likely to boost the market penetration. Region-wise the North American region had a 38 percent share in 2025.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Autopilot System Market Dynamics

The demand for automation is increasing in every area to make processes easier, and autopilot systems are no exception. This feature is crucial in propelling the market for autopilot systems forward. One of the main drivers of market growth is the rising aerospace and defense sectors. Additionally, a large increase in air travel and water transportation operations, especially in developing countries, is boosting the market growth.

Autopilot systems improve situational awareness, navigational accuracy, as well as the vessel's operating and fuel economy. Another element driving growth is the growing use of autopilot systems in UAVs and drones. The Attitude and Heading Reference Systems (AHRS), airspeed, magnetometers, accelerometers, gyroscopes, and flight control algorithms in UAVs can all be managed by these systems. Drones utilize them to follow waypoints, monitor the course, and shoot high-definition overhead images and movies. Other factors like technological developments, the rising requirement for automation across sectors, and intensive research and development (R&D) efforts are expected to fuel the market growth during the forecast period (2025-2032).

The increased demand for decreasing operational expenses to gain more, improving the effectiveness and safety of flight operations, and enabling flight automation is expected to boost the worldwide autopilot systems market. As a result, major market participants are continually investing in the development of innovative architectural high-end autopilot systems. To acquire a competitive advantage in the market, they are also getting into strategic contracts. Honeywell, for example, has signed a deal with Indigo Airlines to install cockpit technology that will aid the autopilot and the pilot in having better situational awareness.

Restraints: Poor automation, which diminishes the operator's situational awareness, high cost of autopilot systems, and airline companies' reliance is expected to hamper the global Autopilot Systems Market's growth.

Autopilot System Market Segmentation Analysis

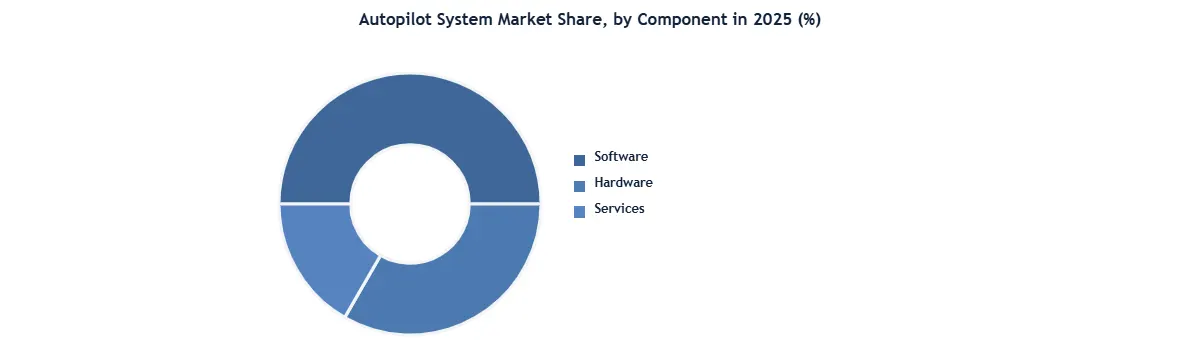

By Component :The software segment dominates the global autopilot system market, as advanced autonomous functions rely heavily on artificial intelligence, machine learning algorithms, navigation software, and sensor fusion platforms. Software manages route planning, obstacle detection, decision-making, and vehicle control across aviation, marine, and automotive applications. In 2025, software accounted for the largest market share because demand is increasing for higher levels of automation in commercial aircraft, unmanned aerial vehicles, and autonomous vehicles. Continuous upgrades in predictive analytics, real-time diagnostics, and cloud-based fleet management are strengthening this segment. Growing investments by aerospace and automotive companies in autonomous mobility systems continue to accelerate software adoption.

The hardware segment holds a substantial share, driven by increasing installation of sensors, radar, LiDAR, cameras, GPS modules, processors, and actuators required for autopilot operations. Hardware remains essential because autonomous systems depend on accurate environmental sensing and control execution. Rising production of commercial aircraft, military drones, and self-driving vehicles supports segment growth. Technological advances in compact sensors, semiconductor chips, and high-performance control units are improving reliability and supporting faster deployment globally.

The services segment is growing steadily due to rising demand for system integration, maintenance, calibration, software upgrades, and technical support. As autopilot systems become more complex, operators require regular monitoring, training, and cybersecurity services to ensure system efficiency and compliance. Expansion of autonomous transport networks is expected to increase service demand significantly during the forecast period.

By Platform, in 2025, the airborne segment had a market share of roughly 36.45%. This is due to the availability of advanced and developed autopilot systems for airplanes, airliners, and air taxis. Flight routes have grown in response to changes in the aviation sector. Long-distance flights need constant monitoring and control by the pilots, resulting in considerable weariness. The autopilot systems in airplanes assist the pilot in maintaining precise navigation control. The need for autopilot systems has grown in response to the rising requirement for reliable and precise navigation systems to enable safe transit by aerial vehicles.

The autopilot system is required for all aircraft and airlines with a capacity of more than 20 seats, according to international aviation law standards and regulations. The expansion of the airborne component has been aided by the strict application of international law. Increased expenditures in the development of autopilot systems to lower flight operating costs are expected to drive segment growth throughout the forecast period.

Autopilot System Market Regional Insight

In 2025, the North American region had a 38 percent share. This can be attributed to the region's growing aviation sector. The presence of a large number of aircraft and advancements in autopilot systems may be seen in the North American region. Technological advancements are paving the way for the creation of extremely efficient autopilot systems. Because of the increased need for flight safety, the North American autopilot systems industry has seen significant growth. The growing need for precise flight navigation and pilot assistance on long-distance flights is boosting the market for autopilot systems in the region. The growing need for autopilot systems is being driven by improvements in the defence and aviation industries. Because of the existence of well-established main market players in the region, the United States dominates the autopilot system market in North America.

The Asia Pacific region is expected to grow at a CAGR of 7.6% during the forecast period. This growth is attributed to the region's rapid increase in aviation traffic. The aircraft industry is said to be dominated by China due to an increase in the number of air passengers and air transportation. India is considered to be the world's third-biggest aviation market, trailing after China. The exponential growth of the Indian aviation sector is being aided by increased investment and increasing privatization of the market, both of which are driving the growth of the autopilot systems market. Thailand and Indonesia, for example, are moving the market forward. The growth of the autopilot market in the APAC region is being fuelled by the implementation of international aviation legislation for passenger safety. The need for autopilot systems in contemporary fighter aircraft is increasing as China and India increase their defence sector expenditures.

Autopilot System Market Recent development

- March 2025 – Garmin Ltd. introduced enhanced autonomous flight control software upgrades for business aviation platforms, improving navigation precision, terrain awareness, and real-time flight path optimization.

- April 2025 – Honeywell International Inc. expanded its advanced avionics and autopilot portfolio with AI-powered predictive flight management solutions for commercial and defense aircraft.

- May 2025 – Collins Aerospace launched next-generation integrated autopilot systems with improved sensor fusion and automated landing assistance for regional and commercial aircraft.

- June 2025 – Airbus announced upgrades to autonomous flight technologies focused on pilot assistance systems and enhanced automated cockpit decision-support capabilities.

- July 2025 – Boeing accelerated investment in autonomous flight research and testing programs to strengthen next-generation autopilot functionality for both commercial aviation and defense applications.

- August 2025 – Thales Group introduced enhanced digital autopilot control systems integrated with cybersecurity protection and real-time aircraft health monitoring.

- September 2025 – Northrop Grumman Corporation expanded autonomous drone autopilot capabilities through advanced AI-enabled navigation systems for military surveillance and unmanned operations.

Autopilot System Market Scope: Inquire before buying

| Autopilot System Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 6.29 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.9% | Market Size in 2032: | 9.4 USD Billion |

| Segments Covered: | by Component | Software Hardware Sensors (LiDAR, cameras, gyros) GPS / GNSS modules Control units / processors Actuators Others Services |

|

| by Platform | Airborne Commercial aircraft Military aircraft UAVs / drones Marine Platforms Commercial Vessels Naval/Defense Marine Platforms Autonomous Marine Vehicles Subsea Autonomous Underwater Vehicles (AUVs) Remotely Operated Vehicles (ROVs) Land-based Autonomous Passenger Vehicles Commercial and Industrial Vehicles (Trucks, Vans, Forklifts) |

||

| by System | Attitude and Heading Reference System Flight Control System Flight Director System Avionics System Others |

||

| by Axis Control | Single-Axis Autopilot Two-Axis Autopilot Three-Axis Autopilot Four-Axis / Advanced Systems |

||

| by Deployment Model | OEM (Original Equipment Manufacturer) Fitment Aftermarket / Retrofit |

||

| By Application | Civil Aviation Military & Defense Marine & Maritime Autonomous Vehicles UAVs / Drones Others |

||

Autopilot System Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (razil, Argentina Rest of South America)

Autopilot System Market, Key Players are:

- Collins Aerospace

- Bae Systems PLC

- Furuno Electric Co. Ltd.

- Genesys Aerosystems Group Inc.

- Honeywell International Inc.

- Lockheed Martin Corporation

- Micropilot Inc.

- Trimble Inc.

- AGCO Corporation and Precision Planting LLC.

- Honeywell International, Inc.

- Garmin Ltd.

- Embention

- Comnav Marine Ltd.

- Raymarine UK Ltd

- Anschütz GmbH

- Navico Group

- Safran SA

- Genesys Aerosystems Group, Inc.

- TMQ Electronics International Pty Ltd.

- Sperry Marine B.V.

- Century Flight Systems, Inc.

- Moog Inc.

- Thales Group

- Avidyne Corporation

- Dynon Avionics

- West Marine

- Kobelt Manufacturing Co. Ltd.

- Brunswick Corporation

- Octopus Autopilot Drives Systems

- Robosys Automation

- Parker Meggitt

- Airborne Technologies Inc

- UAV Navigation

- 3D Robotics, Inc

- Tesla, Inc.

- Volvo Penta

- Kongsberg Maritime

- Bosch Mobility Solutions

- Honeycomb Aeronautical Inc.

- Mobileye

- Ardupilot

- DJI

Others