Automotive Tailgate Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

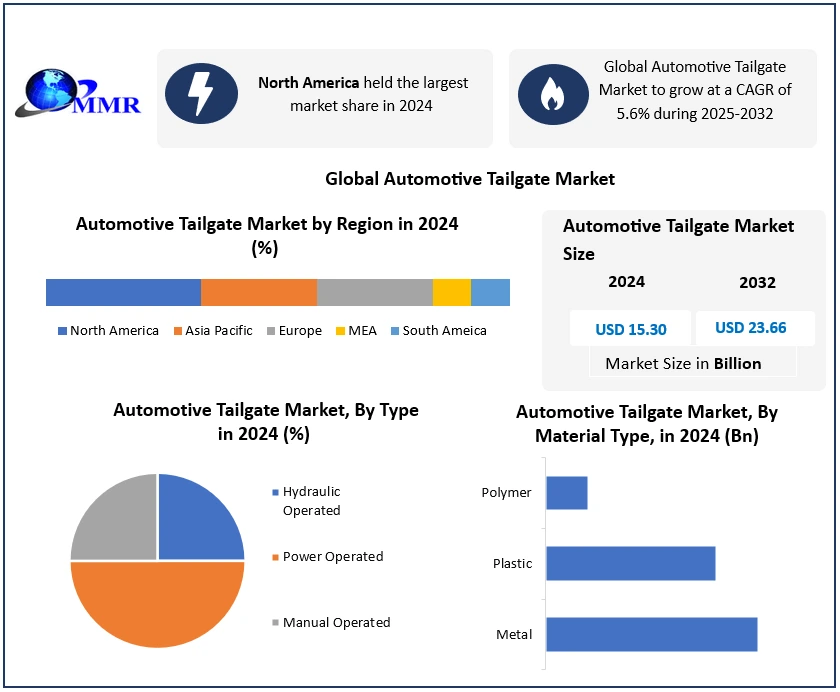

Automotive Tailgate Market was valued at USD 15.30 Billion in 2024, and total Automotive Tailgate Market revenue is expected to grow at a CAGR of 5.6% and reach nearly USD 23.66 Billion from 2025 to 2032.

Automotive Tailgate Market Overview

Automotive Tailgate Market, an important part of the global Automotive and Transportation industry, is witnessing rapid innovation with the shift toward power liftgates, hands-free access and sensor-enabled systems. Once viewed as simple utility components for SUVs, pickup trucks, and commercial vehicles, tailgates are now engineered with lightweight aluminum and composite materials to improve fuel efficiency, reduce emissions, and meet evolving consumer demand for convenience and safety.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

North America dominated the automotive tailgate market due to adoption of smart, automated tailgates, while Asia-Pacific, particularly China and India, is driving volume growth through rising SUV and EV production. Trade policies are also influencing market dynamics according to industry estimates, U.S. tariffs on imported automotive components increased average tailgate assembly costs by nearly 6% in 2023, while preferential trade agreements between the EU and Japan have reduced import duties by 4%, encouraging cross-border sourcing.

The competitive landscape of Automotive Tailgate market features global OEMs and suppliers such as Magna International, Plastic Omnium, Aisin Seiki, who are investing in R&D for power tailgate systems, lightweight composite structures, and aftermarket expansion. As mobility shifts toward electrification and smart vehicles, automotive tailgates are evolving into connected, technology-driven solutions that enhance vehicle design, safety, and consumer experience.

Automotive Tailgate Market Dynamics

Rising Vehicle Ownership and Financing Accessibility to Boost Automotive Tailgate Market Growth

Global automotive tailgate market is primarily driven by rising consumer demand for passenger vehicles, SUVs, and light commercial vehicles, supported by favourable financing options. Easy access to car loans, customized financial schemes from banks and dealers, and increasing per capita income have fueled vehicle ownership, thereby boosting tailgate installations. Moreover, the adoption of composite tailgates made from lightweight materials such as carbon fibre and polymers is accelerating. Leading suppliers like Plastic Omnium and Magna International provide advanced composite tailgate solutions to OEMs including Citroen, Range Rover, and Peugeot, helping automakers achieve weight reduction and improved fuel efficiency. In parallel, the growing shift toward power liftgates and smart tailgate systems with sensor-based automation is enhancing convenience and safety, making them increasingly popular in premium and electric vehicles. These technological innovations, coupled with rising demand in emerging markets, are expected to remain strong growth drivers.

Automotive Tailgate Market Faces Restraint Related to High Maintenance Costs of Power-Operated Tailgates

These advanced systems rely on sensors, actuators, and mechatronic components, which increase overall ownership costs compared to manual tailgates. Additionally, aftermarket service expenses remain higher for smart and electric tailgate systems, limiting their penetration in cost-sensitive markets. Intense price competition among manufacturers is also placing pressure on profit margins, while the need for continuous R&D investment in lightweight and connected solutions adds further constraints. As a result, while power tailgates are gaining traction in premium vehicles, adoption in mass market and developing regions may remain slow due to affordability concerns.

Automotive Tailgate Market Segment Analysis

Based on sales channels, the global automotive tailgate market is broadly segmented into OEM and aftermarket channels. The OEM segment dominated the market, driven by the integration of automotive tailgates as a primary component by major car manufacturers, including Citroën, Range Rover, and Peugeot, ensuring superior product quality, durability and performance compared to aftermarket options. The OEM tailgates, including power liftgates, smart tailgates, and lightweight composite tailgates, benefit from advanced material innovations such as aluminum and carbon-based composites, which reduce vehicle weight and improve fuel efficiency, resulting in minimal replacements over the vehicle’s life cycle.

Based on type, the global automotive tailgate market is segmented into hydraulic operated tailgates, power operated tailgates and manual operated tailgates. The power operated tailgate segment dominated the market, driven by rising demand for high performance, efficient and technologically advanced tailgate solutions. These smart tailgates and sensor enabled liftgates provide hands free operation, automated locking and unlocking, and enhanced safety features, making them highly preferred in premium vehicles, SUVs and electric vehicles. The adoption of lightweight composite materials and integration with mechatronic systems further enhances their appeal, reducing vehicle weight while improving fuel efficiency. Additionally, OEMs are increasingly incorporating connected tailgate technologies that allow remote operation and diagnostics, positioning power operated tailgates as a key differentiator in modern vehicle design.

Automotive Tailgate Market Regional Analysis

North America dominated the global automotive tailgate market, driven by strong demand for premium vehicles, SUVs, pickup trucks, and electric vehicles equipped with power-operated and smart tailgate systems. Leading OEMs and suppliers such as Magna International, Plastic Omnium, and Aisin Seiki are heavily investing in lightweight composite tailgates, sensor-enabled liftgates, and connected smart tailgate technologies, enhancing vehicle safety, convenience, and fuel efficiency. Advanced manufacturing infrastructure, high consumer purchasing power, and increasing preference for hands-free, automated tailgates have accelerated Automotive Tailgate market penetration. Nearly 60% of new SUVs and premium vehicles in the U.S. now feature power operated tailgates, highlighting rapid adoption trends. Additionally, the presence of innovative aftermarket solutions and growing EV adoption further reinforce North America’s leadership in the global automotive tailgate market, making it the most influential region for technological advancements and Automotive Tailgate market growth.

Automotive Tailgate Market Competitive Landscape

Automotive Tailgate Market is highly competitive, led by global players such as Magna International, Plastic Omnium and Aisin Seiki, alongside regional vendors offering cost effective, durable, and lightweight tailgate solutions. These companies focus on power-operated and smart tailgates, sensor-enabled liftgates, lightweight composite designs, and mechatronic automation systems to meet the growing demand from OEMs, SUV manufacturers, and electric vehicle producers. Strategic initiatives such as R&D in composite material technology, electric actuation systems, and IoT-enabled connected tailgates are shaping the competitive landscape. Companies are also investing in hands-free operation, anti-pinch safety features, and remote access control to improve convenience and vehicle integration. The increasing shift toward sustainable manufacturing practices, recyclable materials, and energy-efficient components is driving innovation across the industry. Automotive tailgate market players are leveraging mergers & acquisitions, joint ventures with OEMs, and regional production expansion to strengthen their global presence and enhance technological differentiation. Focus on high-performance designs, advanced safety features, and aftermarket service optimization is enabling companies to remain competitive in a market driven by innovation, connectivity, and smart mobility trends.

Automotive Tailgate Market Key Trends

• Increasing Adoption of Power and Smart Tailgates

Growing preference for power-operated and sensor-enabled tailgates is transforming the automotive tailgate industry. These systems offer hands-free operation, remote control access, and advanced safety sensors, enhancing user convenience and vehicle functionality. OEMs are integrating these technologies, particularly in SUVs, premium vehicles, and EVs, to improve comfort and brand value.

• Lightweight Materials and Sustainable Design Innovations

Manufacturers are increasingly focusing on lightweight materials such as composites, aluminium, and thermoplastics to reduce vehicle weight and improve fuel efficiency. This trend aligns with global emission regulations and supports sustainability goals, driving innovation in design, manufacturing, and recyclability of tailgate components.

• Integration of Mechatronics and Connectivity Features

Adoption of mechatronic systems, IoT sensors, and electronic control units (ECUs) is enabling the development of connected and intelligent tailgates. These systems offer automatic opening based on proximity detection, diagnostics, and integration with vehicle connectivity platforms, enhancing convenience, safety, and the overall user experience.

Automotive Tailgate Market Recent Development

• On August 12, 2025, Magna International Inc. unveiled its next-generation composite power tailgate system, integrating lightweight materials and advanced mechatronic control units to enhance energy efficiency and durability in electric and hybrid vehicles.

• On June 3, 2025, Aisin Seiki Co., Ltd. announced a strategic collaboration with Toyota Motor Corporation to develop smart tailgate systems featuring AI-based gesture recognition and connected vehicle integration for premium SUVs and EVs.

• On May 14, 2025, Plastic Omnium introduced a fully recyclable thermoplastic tailgate solution, aimed at reducing carbon emissions and production costs while improving design flexibility for OEM manufacturers.

Scope of the Global Automotive Tailgate Market:Inquire before Buying

| Global Automotive Tailgate Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 15.30 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.6% | Market Size in 2032: | USD 23.66 Bn. |

| Segments Covered: | by Type | Hydraulic Operated Power Operated Manual Operated |

|

| by Material | Metal Plastic Polymer |

||

| by Vehicle Type | Passenger vehicle Commercial Vehicle |

||

| by Sales Channel | OEMs Aftermarket |

||

Global Automotive Tailgate Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Global Automotive Tailgate Market, Key Players

North America

1. Magna International (Canada)

2. Woodbine Manufacturing (Canada)

3. Go Industries (USA)

4. Gordon Auto Body Parts (USA)

5. Rockland Manufacturing Company (USA)

Europe

6. Robert Bosch (Germany)

7. Faurecia (France)

8. Plastic Omnium (France)

9. Hella GmbH & Co. KGaA (Germany)

10. Huf Hulsbeck & Fürst GmbH & Co. KG (Germany)

11. Gestamp Automoción (Spain)

12. Stabilus (Germany)

13. Brose Fahrzeugteile (Germany)

14. ZF Friedrichshafen (Germany)

Asia-Pacific

15. Denso Corporation (Japan)

16. Aisin Seiki Co., Ltd. (Japan)

17. Mitsuba Corp. (Japan)

18. OMRON Corporation (Japan)

19. Zhejiang Yuanchi Holding Group Co., Ltd. (China)

20. Autoease Technology (China)

21. CARBODY (China)

22. Hyundai Mobis (South Korea)

Frequently Asked Questions

1. Which companies are leading in Automotive Tailgate market?

Ans: Magna, Robert Bosch, Plastic Omnium, Faurecia, Aisin Seiki are the leading key players in Automotive Tailgate market.

2. Which tailgate type dominated the Automotive Tailgate market?

Ans: Power-operated tailgates dominated the Automotive Tailgate market.

3. What are the main tailgate materials?

Ans: Metal, plastic, and polymer materials for durability and lightweight design.

4. Which region leads the Automotive Tailgate Market?

Ans: North America, due to high demand for SUVs, EVs, and premium vehicles.

5. What are key Automotive Tailgate market trends?

Ans: Smart tailgates, lightweight materials, IoT integration, EV adoption, and hands-free operation.