Atomic Layer Deposition Market Size by Product, Type, Application, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

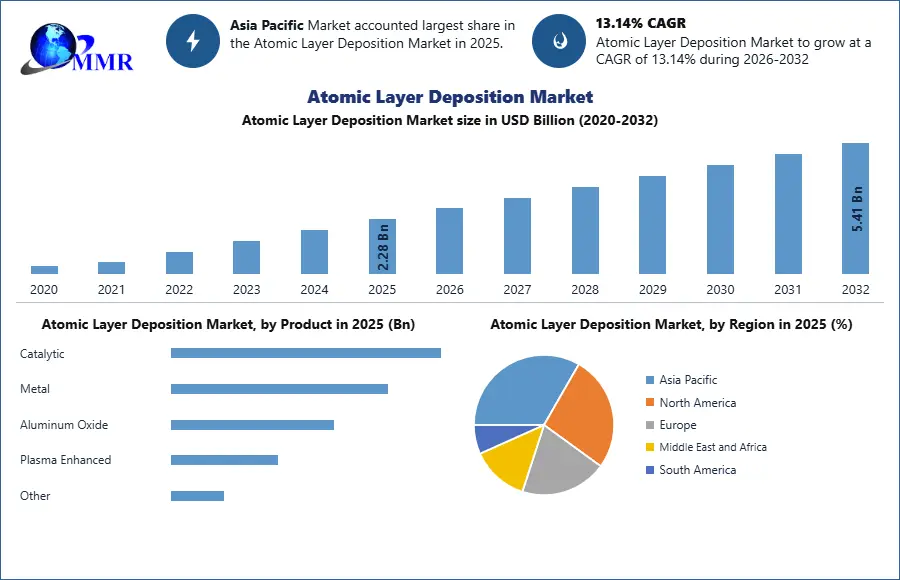

Atomic Layer Deposition Market was valued US$ 2.28 Bn in 2025 and is expected to reach US$ 5.41 Bn by 2032 and will grow at a 13.14% CAGR during the forecast period.

The report includes the analysis of impact of COVID-19 lock-down on the revenue of market leaders, followers, and disrupters. Since lock down was implemented differently in different regions and countries, impact of same is also different by regions and segments. The report has covered the current short term and long term impact on the market, same will help decision makers to prepare the outline for short term and long term strategies for companies by region.

To know about the Research Methodology:-Request Free Sample Report

Increasing demand from end use industries like automotive, industrial, and medical sectors drives the atomic layer deposition market. Growing application of atomic layer deposition in nanotechnology and 3D NAND memory systems is further accelerating the growth of atomic layer deposition market. Application of atomic layer deposition in power devices, energy storage systems, hydrophobic coatings, flexible electronics, and electronic textiles provide several growth opportunities for the atomic layer deposition market. However, high cost of initial investment and stringent export procedures and policies act as a barrier for the market. At present, market is experiencing scarcity of skilled professionals thereby posing a challenge for market.

Solar device & medical equipment segment are the two fastest-growing applications for the atomic layer deposition market owing to the growth of each industry globally. Semiconductor & electronics segment dominated the market with 68% in 2023. Atomic layer deposition is used in IC (Integrated Circuit) and Non-IC components for miniaturizing device’s dimension and generate high durability which influences the growth of the semiconductor & electronics market.

Aluminum oxide segment is dominating the atomic layer deposition (ALD) market. Plenty availability of aluminum, exceptional properties offerings, stability to numerous substrates, easy accessibility of precursor material and economic base metal prices, has resulted into increased demand for aluminum oxide. While, plasma enhanced- atomic layer deposition is expected to be the fastest growing product type. Plasma enhanced- atomic layer deposition delivers excellent output properties and fastest surface reaction mechanism rate. Atomic layer deposition is surface-sensitive deposition process, and enhances the surface modification through plasma exposure, which enables to alter nucleation.

Asia Pacific held 46% of the overall revenue in 2023 owing to strong presence of manufacturing base and growing semiconductor & electronics, solar, and medical device industries, especially, in China, Japan, South Korea, and Taiwan. Presence of cheap skilled labor & land, and government subsidies further accelerate the market growth. Europe and North America are mature market hence is anticipated to grow at steady pace. North America accounted for the second largest market share of 23.8% in 2023, driven by technological advancement and growing application of atomic layer deposition equipment across automotive, semiconductor, and industrial sectors, among others.

The objective of the report is to present a comprehensive assessment of the market and contains thoughtful insights, facts, historical data, industry-validated market data and projections with a suitable set of assumptions and methodology.

The report also helps in understanding atomic layer deposition market dynamics, structure by identifying and analyzing the market segments and project the market size. Further, the report also focuses on a competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence.

The report also provides PEST analysis, PORTER's analysis, SWOT analysis to address questions of shareholders to prioritizing the efforts and investment in the near future to the emerging segment in atomic layer deposition market.

Scope of Global Atomic Layer Deposition Market: Inquire before buying

| Atomic Layer Deposition Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 2.28 USD Billion |

| Forecast Period 2026-2032 CAGR: | 13.14% | Market Size in 2032: | 5.41 USD Billion |

| Segments Covered: | by Product | Catalytic Metal Aluminum Oxide Plasma Enhanced Other |

|

| by Type | Film Type Precursor Type Material Type Polymers Sulfides Nitrides Oxides Other |

||

| by Application | Medical Devices Optical Devices Sensors Solar Panels & Devices Thermoelectric Materials Integrated Circuit Applications Fuel Cells Batteries Other |

||

| by End-User | Healthcare Chemicals Energy Semiconductors & Electronics Other |

||

Atomic Layer Deposition Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Atomic Layer Deposition Market, Key Players are:

01.AIXTRON SE

02.Adeka Corporation

03.Air Liquide S.A.

04.Air Products and Chemicals, Inc

05.Applied Materials, Inc.

06.Adeka Corp

07.Applied Materials Inc

08.ASM International N.V

09.ATMI Inc

10.Beneq Oy

11.Cambridge NanoTech Inc

12.Hitachi Kokusai Electric Inc

13.Kurt J. Lesker Co

14.Metryx Ltd

15.Novellus Systems Inc

16.Oxford Instruments plc

17.Picosun Oy

18.Praxair Technology Inc

19.Sigma-Aldrich Co.

20.Lam Research Corporation

21.Tokyo Electron Limited

22.Denton Vacuum

23.Kurt J. Lesker Company

24.Veeco Instruments.

25.Ultratech Inc.

26.Centrotherm Photovoltaics AG

27.Tosoh Corporation

Frequently Asked questions

1. What is the market size of the Global Atomic Layer Deposition Market in 2025?

Ans. The market size Global market in 2025 was US$ 2.28 Billion.

2. What are the different segments of the Global Atomic Layer Deposition Market?

Ans. The Global market is divided into Product, Type, Application and End-User.

3. What is the study period of this market?

Ans. The Global market will be studied from 2025 to 2032.

4. Which region is expected to hold the highest Global market share?

Ans. The Asia Pacific dominates the market share in the market.

5. What is the Forecast Period of Global Atomic Layer Deposition Market?

Ans. The Forecast Period of the market is 2026-2032 in the market.