Agricultural Robots Market by Type, Application, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

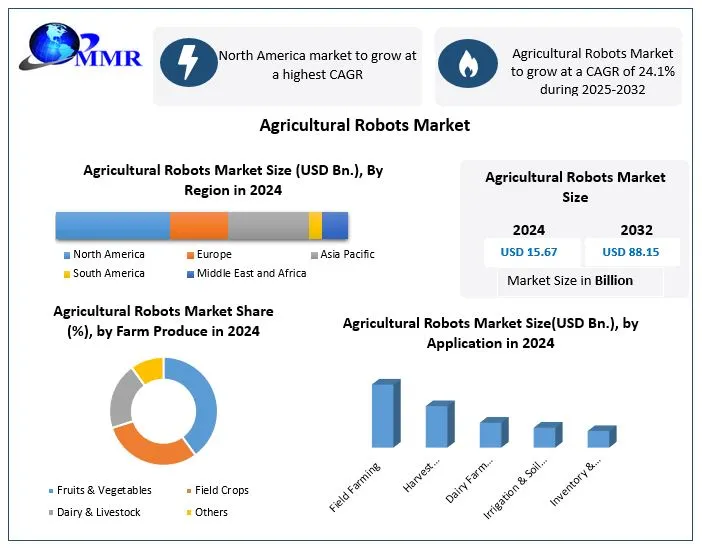

Global Agricultural Robots Market size was valued at USD 15.67 Bn. in 2024, and the total Agricultural Robots Market revenue is expected to grow by 24.1% from 2025 to 2032, reaching nearly USD 88.15 Bn.

Agricultural Robots Market Overview:

Agricultural robots are mechanical devices that perform various jobs on a farm, including planting, weeding, harvesting, and milking cows or sheep, even just monitoring the health of a crop. Agricultural robots have started to emerge in all types of agriculture for productivity results, cost of labor, and precision agriculture for efficiency. The push of agricultural robots is influenced by population and food demand, labor costs, and environmental awareness towards more sustainable and efficient farming practices. A good example of this is the French start-up called Meropy, which developed a crop surveying robot that runs autonomously and incorporates artificial intelligence technology to provide real-time reports on the plant's health, which saves time and chemicals. The other form of robots that evolved from agricultural architecture is drones, for both aerial spraying and health monitoring of crops. Drones offer new ways of improving farming systems that we see mostly in China, the U.S., and India, where large land area agricultural systems demand more efficient data-driven management systems. These areas also highlight the benefits of drones and robots to alleviate labor shortage as well as better welfare/disease detection of crops, allowing for better yielding and lower-cost crops.

Top companies in the agricultural robots market such as John Deere, DJI Technology, Trimble, AGCO Corporation, and Naïo Technologies are continuing to take technological leaps in making the use of AI, computer vision, GPS, and IoT in robotics even greater at a time when agriculture needs it to be smarter, more fluid, and adaptable to the modern farm. These companies are also pushing towards agricultural robotics that is increasingly more sustainable, with initiatives to reduce pesticide use and develop low-emission systems. This is allowing farmers to address environmental compliance and attain organic certification standards. The boost from supportive policies, such as the EU’s Common Agricultural Policy (CAP) to support EU farmers in their choice of agricultural inputs, and India’s Precision Agriculture Development Programme (PADP) to promote high-tech farming, continue to act upon the uptake of robotic solutions across farms today, supported through automation technologies, as well as driving farmers towards digital agriculture. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Global Agricultural Robots Market Dynamics:

RisAutomation and Labor Shortages to Drive Agricultural Robots Market Growth Amid Growing Food Demand and Sustainability Concerns

The growing demand for food crops because of population increase primarily drives the agricultural robots market growth. There has been growing automation of farm operations to increase food production and improve crop quality. Mounting adoption of advanced technologies to maximize crop production boosts the adoption of agricultural robotics. Rising labor costs, coupled with a shortage of labor on farms, have increased the demand for agricultural robots. Other factors driving the agricultural robots market growth include growth in the worldwide agricultural industry, growing environmental concerns, shifting focus towards organic food, and concerns regarding the scarcity of natural resources.

Integration of IoT, AI-ML, and 5G Technologies to Create Opportunities for Enhanced Efficiency and Sustainable Growth in the Agricultural Robots Market

Agricultural robotics startup Meropy, based in France, has created a robotic solution that independently examines crops from both aerial and sub-surface perspectives, providing a time and cost-saving alternative for farmers. In the development of future agricultural robots, architects and designers are increasingly embracing emerging technologies, including:

1. Internet of Things (IoT): In technologically advanced farms with a multitude of connected devices, the IoT ecosystem becomes crucial for seamlessly integrating robots into the system. This involves utilizing various connectors, actuators, and sensors to establish connectivity.

2. Cloud Computing & 5G: The vast amount of data generated by IoT devices on large farms requires rapid processing and transfer for effective cognitive decision-making by robots. Leveraging cloud computing and 5G technology is essential to handle the petabytes of data efficiently.

3. Artificial Intelligence-Machine Learning (AI-ML): Given that AI-ML is already a fundamental component of robotics, it should be employed as a guiding principle for the development of agricultural robots, enhancing their capabilities and functionality.

Limited Rural Connectivity and Cybersecurity Risks Pose Challenges to Widespread Adoption and Independent Use of Agricultural Robots

As society becomes increasingly digitized, the agricultural industry is also evolving in this direction. While this digital transformation presents opportunities to enhance efficiency and production rates in agriculture, it concurrently raises concerns about cybersecurity threats. Farmers are exposed to risks such as phishing, data hacking, and, notably, the necessity to resort to hacking their smart farm equipment when dealerships withhold software licenses required for repairs. The "right to repair" debate extends beyond agriculture but holds particular significance for farmers who often prefer to independently service their equipment without relying on third parties.

Another factor challenging the growth of the agricultural robots market is the availability of rural broadband, as not all farmers have access to a reliable internet connection on their operations. Despite the potential for increased efficiency, the adoption of farm robotics also introduces concerns about encouraging farm consolidation, unless there is a prioritized development of cyber infrastructure.

Global Agricultural Robots Market Segment Analysis

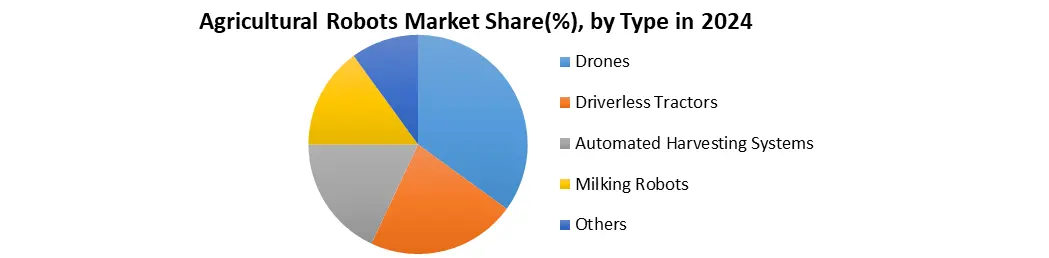

By Type, the market is segmented into driverless tractors, automated harvesting systems, drones, milking robots, and others. The drones segment dominated the agricultural robots market in 2024, and it's expected to hold the largest market share over the forecast period. Drones are used for aerial imaging, crop health monitoring, precision spraying, and other applications, and they give farmers high-resolution multispectral images and real-time data about crop condition, pests, irrigation management, and soil variability. The need for drones is most severe in broad-acre or large-scale commercial agriculture, being that manual monitoring is inefficient and cumbersome. Modern agricultural drones, now powered with AI and computer vision, can assess plant health, crop counts, benchmark field maps, and variable-rate spraying without needing input from a human operator. Because of cost-effectiveness and ease of deployment, and adaptability, drones fit very well in precision agriculture, especially when drone data is deployed to complement the farms' IoT platform. In the U.S., China, Japan, and India, among other countries, government action and grants for smart farming have provided positive support for drone manure.

By Application, the market is segmented into field farming, harvest management, dairy farm management, soil and irrigation management, and inventory monitoring and crop monitoring. And field farming segment has dominated the Agricultural Robots Market in 2024, and it's expected to hold the largest market share over the forecast period. Growth in this segment is driven by the quest for efficiency, sustainability, and precision in the large-scale growing of crops. Field farming robots are widely used for sowing, spraying, fertilizing, weeding, and monitoring the crops. These robots provide a mechanism to automate labor-intensive movements that were previously done by hand. This reduces labor dependency while providing productivity gains. Field farming robots are highly adopted in the U.S.A., Canada, Germany, Australia, Brazil, and are continuously growing where large farms and a dwindling rural workforce are being realized. With transformations in AI, computer vision, and GPS-guided systems, a field robot can now assess and accurately determine plant stress, nutrient deficiencies, and pest infestations. Autonomous sprayers or precision seeders, for example, apply correct inputs (seeds, water, fertilizers) with high accuracy as to how much or where to apply, reduce overall use of inputs while maximizing yield.

Agricultural Robots Market Regional Insights:

The North American Agricultural Robots Market is expected to grow at a high rate during the forecast period. The potential of farming robotics technology to contribute to a sustainable future for U.S. agriculture is significant. The agricultural sector is witnessing a substantial demand for autonomy in the region. However, the current solutions often tap into only minimal potential. Numerous agricultural robot companies are currently focused on creating autonomous tractors and niche robotics solutions for agriculture. In December 2023, Solinftec, a renowned global leader in artificial intelligence solutions and sustainable agricultural practices, intensified its collaboration with WHIN and increased its manufacturing capabilities in the United States through a strategic partnership with Still Waters Manufacturing. The commencement of Solix robot production in the WHIN region of Indiana signifies a significant enhancement of Solinftec's footprint in the United States during the last quarter.

The Asia Pacific Agricultural Robots Market is expected to grow rapidly during the forecast period. Despite originating from a region not traditionally associated with extensive agricultural activity, Singaporean agriculture developer Singrow has placed a strong emphasis on leveraging robotics and related technologies to tackle challenges such as food security and promote agricultural sustainability. Much like private enterprises such as Singrow, governments are actively incorporating robotics into the agricultural sector, as illustrated by the Singaporean government's initiative known as the Agri-Food Cluster Transformation Fund (ACT). This program explicitly commits to investing USD 45.08 million to explore avenues for enhancing overall productivity in the domestic agri-food sector, with a particular emphasis on the relevance of robotics in achieving this goal. The Chinese Academy of Agricultural Sciences (CAAS) has declared its dedication to investigating the implementation of technological solutions in China's agricultural sector. In addition to its goal of enhancing seed varieties, increasing grain yield, and improving overall agricultural sustainability, CAAS is expected to focus on automating processes using robotics. Through this initiative, the government-affiliated organization aspires to modernize conventional farming practices, aiming to lower costs and enhance supply chain efficiency.

Agricultural Robots Market Competitive Landscape

The Agricultural Robots Market is very competitive as it is bolstered by innovations in precision farming, automation, and the use of artificial intelligence-backed solutions. Major players internationally are John Deere (USA) and DJI Technology Co., Ltd. (China), who dominate ground machinery and aerial drone segments, respectively. According to reports, John Deere has revenue of USD 61.25 billion out of the Production & Precision Agriculture segment was (43.7%) and attributed to the need for autonomous tractors and AI-enabled sprayers after John Deere realized successful acquisitions for companies like Bear Flag Robotics and Blue River Technology. Both companies remain committed to integrating cloud technology, computer vision, and solutions focused on sustainability, reducing the reliance on human labor, and the impact on the environment, highlighting the rising importance of robotics in global agricultural practices. DJI Technology Co. Ltd. reportedly has 70–80% of the global market share of agricultural drones that has revenue of USD 805 million in 2024, using its Agras drone, which has features that also provide precision spraying and monitoring of crops. Where both companies continue to expand their cloud-enabled products that utilize AI and computer vision more rapidly, labor remains a part of the agricultural industry, less undesirable for progressive and informed advances.

Agricultural Robots Market Recent Development

• In January 2025 at CES Las Vegas, John Deere (USA) announced a second-generation autonomous kit that is being applied to a suite of fully autonomous vehicles, including a large-size 9RX tractor with 16 cameras and NVIDIA-powered edge AI, a diesel orchard tractor with LiDAR for dense-canopy spraying, a battery electric commercial lawn mower, and a driverless articulated dump truck, called "Dusty," for heavy duty hauling. They also announced retrofit kits for existing equipment to help farmers and contractors reduce labor shortages.

• In February 2025, DJI announced a 50-fold increase in sales in Thailand since 2019 and partnered with Siam Kubota for an Ag Drone competition, showing a 20–30% reduction in chemical use in durian orchards and increased crop value.

• Lely Holding S.A.R.L. (Netherlands) introduced the Vector MFR Next, a next-generation robotic mixer feeder with an 800 kg capacity, 35% greater than its predecessors, with improved safety visibility from both front and rear lights for automated feed management on March 1, 2025. Before that, the North American “Vector Tour” in May 2025 reported that farms using the Lely Vector system realized 98.4% feeding accuracy and 30% freed up farmer workforce time.

• Nexus Robotics Inc. (Canada) announced La Chèvre, its next generation autonomous weeding robot with real-time computer vision, AI driven algorithms, articulated robotic arms, RTK GPS navigation, and LiDAR, in early 2024 and soon moved towards commercial operation which removes over 95% of weeds without herbicides—operating 24/7, up to 50% reduction in herbicide/fungicide applications, and four workers saving in labor equivalent per unit.

• In 2025, Naïo Technologies (France) highlighted upgrades to the Oz robot and introduced a vineyard implement for the straddler Ted such as a Naotec vine shoot remover and centimeter level GPS, and an upgraded motor that is not only stronger and more powerful, but also 50% more energy efficient which further improved simultaneous multi-tasking operation after pruning and mechanical weeding.

Agricultural Robots Market Recent Trends

1. Integration of AI and Computer Vision in Precision Farming

Innovative AI and machine learning models are being embedded into robotics for real-time decision making, plant recognition, and disease detection.

John Deere’s See & Spray™ Ultimate system uses AI and computer vision to distinguish between crops and weeds, enabling targeted herbicide application. This reduces chemical usage by over 77% compared to traditional blanket spraying.

2. Rise of Autonomous Drones and Aerial Robots

Drones are being adopted at a rapid rate for precision spraying, crop mapping, and crop health monitoring in large, irregular shapes and uneven topography.

DJI's Agras T50 and T100 drones, which will come to market in 2024, provide autonomous route planning, terrain radar, and real-time variable spraying features, which are very advantageous for row crops and orchards.

3. Autonomous Field Robots for Seeding, Weeding & Harvesting

Robots are automating labor-intensive activities like weeding, seeding, and harvesting for specialty crops.

Naïo Technologies' Oz and Dino both autonomously perform weeding tasks in vegetable fields (saving labor costs and allowing organic farming).

Agricultural Robots Market Scope: Inquire before buying

| Agricultural Robots Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 15.67 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 24.1% | Market Size in 2032: | USD 88.15 Bn. |

| Segments Covered: | by Type | Driverless tractors Automated harvesting systems Drones Milking robots Others |

|

| by Application | Field farming Harvest management Dairy farm management Soil and irrigation management Inventory and crop monitoring |

||

| by Farm Produce | Fruits and Vegetables Field Crops Dairy and Livestock Others |

||

Agricultural Robots Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, and the Rest of APAC)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

North America Agricultural Robots Market Key Players

1. Deere & Company (John Deere) [Moline, Illinois, USA]

2. AGCO Corporation [Duluth, Georgia, USA]

3. Trimble Inc. [Sunnyvale, California, USA]

4. AG Leader Technology [Ames, Iowa, USA]

5. Topcon Positioning Systems [Livermore, California, USA]

6. Autonomous Tractor Corporation (ATC) [Minneapolis, Minnesota, USA]

7. Harvest CROO Robotics [Plant City, Florida, USA]

8. Autocopter Corp. [Indianapolis, Indiana, USA]

9. Harvest Automation [Bedford, Massachusetts, USA]

10. FarmWise [San Francisco, California, USA]

11. Nexus Robotics Inc. [Brossard, Quebec, Canada]

Europe Agricultural Robots Market Key Players

1. CNH Industrial [London, United Kingdom]

2. Naio Technologies [Toulouse, France]

3. Lely Group [Maassluis, Netherlands]

4. Bosch Deepfield Robotics [Stuttgart, Germany]

Asia Pacific Agricultural Robots Market Key Players

1. SoftBank Robotics [Tokyo, Japan]

2. DJI (Dà-Jiāng Innovations) [Shenzhen, China]

3. Yanmar Co., Ltd. [Osaka, Japan]

Frequently Asked Questions:

1. Which region has the largest share in the Global Agricultural Robots Market?

Ans: North America held the highest share in 2024.

2. What is the growth rate of the Global Agricultural Robots Market?

Ans: The Global Market is expected to grow at a CAGR of 24.1% during the forecast period 2025-2032.

3. What is the scope of the Global Agricultural Robots Market report?

Ans: The Global Agricultural Robots Market report helps with the PESTEL, Porter's, Recommendations for Investors and leaders, and market estimation for the forecast period.

4. Who are the key players in the Global Agricultural Robots Market?

Ans: The important key players in the Global Agricultural Robots Market are – SoftBank Robotics [Tokyo, Japan], DJI (Dà-Jiāng Innovations) [Shenzhen, China], Yanmar Co., Ltd. [Osaka, Japan], Deere & Company (John Deere): [Moline, Illinois, USA], AGCO Corporation [Duluth, Georgia, USA], Trimble Inc. [Sunnyvale, California, USA], AG Leader Technology [Ames, Iowa, USA]

5. What is the study period of this market?

Ans: The Global Agricultural Robots Market is studied from 2024 to 2032.