General Aviation Engines Market: by Engine Type, by Platform, by Technology, by Components - Forecast to 2032

Overview

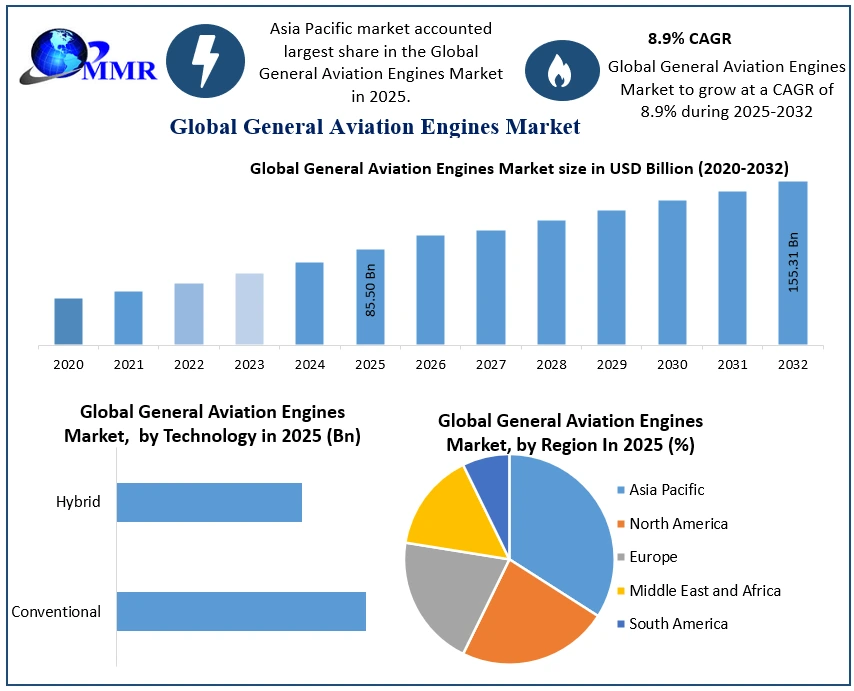

The General Aviation Engines Market size was valued at USD 85.50 Billion in 2025 and the total General Aviation Engines revenue is expected to grow at a CAGR of 8.9% from 2025 to 2032, reaching nearly USD 155.31 Billion by 2032.

During the forecast period, the general aviation engines market is expected to grow due to planned fleet modernization and expansion plans by airlines, aircraft operators, and charter operators. Demand for next generation engines with low emissions and reduced weight, which will boost aeroplane fuel economy, is driving market expansion. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Due to this trend, companies are investing in research and development of new engine models using the latest technologies, like additive manufacturing and composite technologies. However, growing concerns about aircraft engine failure during operation, and delays in delivery, are stifling the market's expansion.

Based on the engine type, the market is segmented into turbofan, turboprop, turboshaft, and piston. Based on platform, the market is segmented into Fixed wing, Rotary wing, UAV (Unmanned Ariel Vehicles). Based on components, the market is segmented into Compressor, Turbine, Gear Box, Exhaust Nozzle and Fuel System. The general aviation engines market is segmented based on technology into Conventional and Hybrid. The report also includes market sizes and forecasts for general aviation engines in major countries around the world. The market size and forecasts are provided in dollars (USD billion). The research excludes aftermarket sales of engines and parts, along with sales of auxiliary power units (APUs).

COVID-19 Impact on General Aviation Engine Market

Failure to maintain aircrafts was one of the primary issues encountered by the aviation industry, which resulted in operational stress. As a result of the sporadic breakdowns and restrictions, the aviation sector experienced delays and hindrances. Around the world, aircraft, engines, and component plants came to a standstill. Engineers' ability to undertake routine maintenance was also hampered by travel restrictions. Individual sites at companies including Safran, Collins Aerospace, and General Electric were affected as a result of the same, resulting in partial shutdowns for the safety of their employees.

The pandemic caused a drop in passenger traffic in 2021, however domestic passenger traffic in China, India, South Korea, and Australia began to recover in the second part of the year. Low-cost airlines in the region are strengthening their aircraft fleet with next generation aircraft to support their route development goals as domestic passenger traffic increases at a rapid pace. Robust aircraft orders as part of regional carriers' fleet modernization plans are expected to drive up demand for aircraft engines in the coming years.

Despite the decline in commercial aviation engine deliveries in 2021 and 2021, the remaining performance obligations (RPO) of aircraft engine manufacturers are growing due to the increasing aircraft backlog of aircraft OEMs. Moreover, engine manufacturers are collaborating with aircraft manufacturers to produce eco-friendly aircraft engine systems with low weight and emissions. Furthermore, regional players are collaborating with foreign players in response to rising demand for local manufacturing.

General Aviation Engines Market Dynamics

The general aviation engine market is expected to grow through the forecast period as air passenger traffic increases. Total air passenger traffic climbed by 21 percent in 2021, with carriers flying more than 80 lakh passengers during the period following a two-month hiatus beginning, after the gradual reopening of domestic airline facilities. In order to meet the growing demand for air travel, several airlines are updating their fleets by acquiring new planes, which increases the need for new engines. According to the International Air Transport Association (IATA), the number of passengers might quadruple to 8.2 billion by 2037. Therefore, the growing air passenger traffic drives the growth of the aircraft engine market.

Qatar Airways ordered GE9X engines in January 2022 as part of a global launch deal for up to 50 Boeing 777-8 Freighters. The airline has committed to 30 GE9X engines and four GE90-115B engines for Boeing 777-8 aircraft, according to GE Aviation (34 aircraft firm order with an additional 16 purchase right options).

The high maintenance costs of aviation engines are expected to restrict market growth during the forecast period. Washing and drying jet engine components, quality inspections of the interiors and exteriors, dismantling the engine, repair and replacement of any parts, and finally reassembly and testing of the engine are all steps in the maintenance of aviation engines. The CT7-2E1 turboshaft engine's Version 6.0 Software upgrade was published in June 2021, bringing a variety of enhancements to civil and military engine operators. The software upgrade adds three major features that provide operators more freedom.

Air travel is on the rise as the population's disposable income rises, making flying a more accessible choice. This issue is pressuring airlines to expand their fleets. As airline carriers purchase aircraft in large numbers, this is one of the primary reasons driving the growth of general aviation engines market. Safran Helicopter Engines and ST Engineering signed a Memorandum of Understanding (MoU) in February 2025 to conduct research on the use of Sustainable Aviation Fuel (SAF) in helicopter engines. The goal of the project is to help helicopter operators transition from traditional fossil fuels to SAF.

Environmental pollution caused by the emission and expulsion of gases produced by the burning of fuel in aircraft engines is expected to slow market growth. Aircraft engines are expensive products, which are expected to hinder the general aviation engines market and manufacturers' expansion. The number of orders placed by airlines determines the size of the aviation engine market. Huge orders are expected to put a burden on aircraft engine makers' productivity, which will slow the market's development over the forecast period.

Maintenance and manufacturing of aviation engines require highly skilled professionals, which raises the cost of investment, which is one of the significant reasons slowing market growth. During the forecast period, increased demand for lightweight aircraft engines and an increase in aircraft manufacturers are expected to create various possibilities in the market. Embraer, Widere, and Rolls-Royce signed a 12-month research cooperation agreement in February 2025 to undertake a study and investigate breakthrough sustainable technologies for regional planes, with an emphasis on building a hypothetical zero-emissions aircraft.

General Aviation Engines Market Segment Analysis

Turbofan Aircraft Engine Type is Expected to Witness a Higher CAGR During the Forecast Period

Based on engine type, the market is segmented into Turboprop, Turbofan, Turboshaft and piston engine. A turbofan engine, also known as a fanjet or bypass engine, is a kind of jet engine that generates thrust by combining jet core efflux with bypass air that has been accelerated by a ducted fan powered by the jet core. The bypass ratio is the ratio of the mass of air bypassing the engine core to the amount of air travelling through the core. A turbofan engine that gets most of its thrust from its fan is called a low bypass engine, whereas one that gets most of its push from the jet engine core is called a high bypass engine. During the forecast period, turbofan aircraft engines are expected to grow at the fastest CAGR in the general aviation engine market. Turbofan engines are far more capable of flying at a greater altitude than other engines, and they also produce less noise than other engines. Because of their smaller weight, they are the best engine for long-range flights.

The Turbine is Expected to Witness the Highest CAGR During the Forecast Period

Based on the component, the market is segmented into Compressor, Turbine, Gearbox, Exhaust System, Fuel System and others. During the forecast period, the turbine is expected to grow at the fastest CAGR in the general aviation engines market. A turbine is a rotating engine that extracts energy from a flowing stream of combustion gases. As a result, a turbine converts the kinetic energy of these gases into rotational motion. A turbine in an aviation engine is made up of a series of blades that enable gases to flow into the turbine and drive the blade forward. This causes a circular motion, following which the less energetic gases are evacuated.

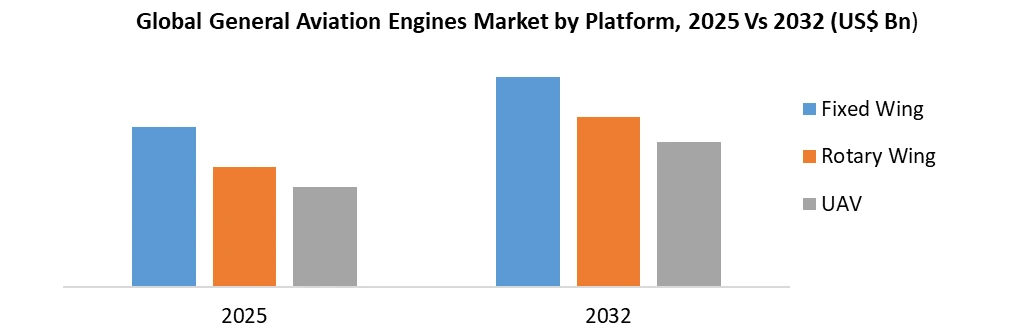

Fixed-wing Aircraft Engines to Exhibit the Highest Growth Rate During the Forecast Period

Based on platform, the market is segmented into Fixed Wing Aircraft, Rotary Wing Aircraft and Unmanned Ariel Vehicles. The global market for general aviation aircraft and engines is growing due to a rise in leisure and business air travel, rising disposable income, and the development of aviation infrastructure to accept and manage more general aviation aircraft. Turbofan engines power the majority of general aviation aircraft. Due to global expenditures made to expand the size of the existing general aviation fleet of fast, powerful, and fuel-efficient aircraft, turbofans are expected to grow at the fastest rate among aircraft engines.

The global shipping of piston-engine aircraft increased by 15.9% in 2021, to 1509 units, up from 1302 units in 2021. In 2025, sales of some of the most popular general aviation aircraft types increased, including the Cirrus Aircraft SR 22T, Cirrus SF 50, Diamond Aircraft DA 40, Bombardier business jets, Daher Kodiak 100, and others. Improvements in design and technology, such as the refinement of high by pass turbofan design, are making fixed-wing aircraft engines more fuel-efficient and powerful, boosting market growth.

Conventional Aircraft Engine Estimated to Witness the Highest CAGR During the Forecast Period

Based on technology, the market is segmented into Conventional and Hybrid. During the forecast period, the conventional aircraft engine category is expected to grow at the fastest CAGR in the general aircraft engine market. Aero engine is another term for a normal aeroplane and it is the most powerful component of the aircraft's propulsion system. The vast majority of aircraft engines are either piston or gas turbine aircraft engines. Turboprop aircraft engines, turbofan aircraft engines, turboshaft aircraft engines, and piston aircraft engines are some of the most common types of aircraft engines.

General Aviation Engines Market Regional Insights

North America held the largest regional share of the general aviation engine market. Because of the rapid expansion of technologically advanced aircraft engines in the area, North America is now dominating the aircarft engine industry. The growing aerospace and defence aviation business in North America is driving aircraft engine manufacturers to provide technologically innovative and efficient solutions across a variety of aircraft types.

The general aviation engine market in North America is driven by rising demand for aircraft engines and the presence of some of the market's key companies, including General Electric Company, Honeywell International Inc., Collins Aerospace, and Textron Inc. These companies are working on R&D to expand their product lines and are creating aircraft engines with technologically improved systems, subsystems, and other components.

Asia-Pacific region is expected to witness the highest growth during the forecast period thanks to the strong demand for domestic air travel in developing economies. Due to geopolitical concerns in the area, governments are increasing their investments in advanced aircraft acquisitions and replacement to strengthen their aerial capabilities. As part of its strategy to bridge the gap between the present number of squadrons and the desired number of squadrons, the Indian Air Force plans to buy 450 fighter aircraft for deployment on the country's northern and western borders by 2035. In the next years, such fleet modernization initiatives are estimated to drive demand for improved lightweight and fuel-efficient engines.

Thanks to the significant growth showcased by China, India, and Japan in terms of new aircraft orders and deliveries in the past five years, Asia Pacific region is expected to witness a significant growth. China currently has approximately 2,600 general aviation aircraft, with demand from the short-haul transportation, tourism, forestry, and emergency medical treatment sectors expected to expand in the future years. Around 60% of the operational fleet is fixed-wing aircraft, with the remainder being rotorcraft. The Gulfstream G450, G550, Dassault Falcon 7X, and Bombardier Challenger 850 are the top four business jet models in China.

The Cessna Citation XLS+ is powered by a PW545C turbofan engine from Pratt & Whitney Canada. Similarly, Japan's overall fleet grew significantly in 2021 compared to 2021. The expansion of turboprop and piston engine aircraft in the region has been fueled by the development of airports in distant locations and smaller cities. Club One Air is India's largest business jet charter company, with eight of its ten planes dedicated completely to charter flights. Within the next two years, the firm wants to increase its fleet size. Such advances in general aviation in the Asia-Pacific region are expected to generate considerable demand for aircraft engines in the near future, driving market growth.

Europe region is expected to witness a significant growth through the forecast period. The generator and related power electronics were delivered to the newly rebuilt Testbed 108 in Bristol, UK, in July 2021, after completing an intensive development test programme at the Rolls-Royce plant in Trondheim, Norway. It will be part of the Power Generation System 1 (PGS1) demonstration programme for future regional aircraft, with a capacity of 2.5 megawatts (MW). In April 2021, Europe next generation fighter within the FCAS program takes a decisive step forward as Safran Aircraft Engines and MTU Aero Engines finalized their collaboration agreement by creating a 50/50 joint company. The new entity is called EUMET GmbH (derived from European Military Engine Team).

For example, India's Defence Research and Development Organisation (DRDO) was in negotiations with Safran in March 2022 about developing a 125KN engine for the indigenous fifth-generation Advanced Medium Combat Aircraft (AMCA) (currently under development with the first flight planned for 2024). Such advancements are expected to aid firms in expanding their global reach in the future years.

The objective of the report is to present a comprehensive analysis of the global General Aviation Engines Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the General Aviation Engines Market dynamic, structure by analyzing the market segments and projecting the General Aviation Engines Market size. Clear representation of competitive analysis of key players by Vehicle type, price, financial position, product portfolio, growth strategies, and regional presence in the General Aviation Engines Market make the report investor’s guide.

General Aviation Engines Market Scope: Inquiry Before Buying

| General Aviation Engines Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 85.50 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 8.9% | Market Size in 2032: | USD 155.31 Bn. |

| Segments Covered: | by Engine Type | Turbofan Turboprop Turboshaft Piston |

|

| by Platform | Fixed Wing Rotary Wing UAV |

||

| by Technology | Conventional Hybrid |

||

| by Components | Compressor Turbine Gear Box Exhaust Nozzle Fuel System |

||

General Aviation Engines Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

General Aviation Engines Market, Key Players are:

1. Safran SA

2. General Electric Company (through GE Aviation)

3. Rolls-Royce Holding PLC

4. MTU Aero Engines AG

5. Engine Alliance (General Electric and Pratt & Whitney)

6. Raytheon Technologies Corporation (through Pratt & Whitney)

7. CFM International (GE Aviation and Safran)

8. International Aero Engines (Pratt & Whitney, Japanese Aero Engine Corporation, and MTU Aero Engines)

9. Pratt & Whitney

10. Japanese Aero Engine Corporation

Frequently Asked Questions:

1. Which region has the largest share in Global General Aviation Engines Market?

Ans: Asia Pacific region held the highest share in 2025.

2. What is the growth rate of Global General Aviation Engines Market?

Ans: The Global General Aviation Engines Market is growing at a CAGR of 8.9% during forecasting period 2026-2032.

3. What is scope of the Global General Aviation Engines Market report?

Ans: Global General Aviation Engines Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global General Aviation Engines Market?

Ans: The important key players in the Global General Aviation Engines Market are – Safran SA, General Electric Company (through GE Aviation), Rolls-Royce Holding PLC, MTU Aero Engines AG, Engine Alliance (General Electric and Pratt & Whitney), Raytheon Technologies Corporation (through Pratt & Whitney), CFM International (GE Aviation and Safran), International Aero Engines (Pratt & Whitney, Japanese Aero Engine Corporation, and MTU Aero Engines), Pratt & Whitney, Japanese Aero Engine Corporation.

5. What is the study period of this Market?

Ans: The Global General Aviation Engines Market is studied from 2025 to 2032.