Gate Driver IC Market - Industry Structure Evaluation, Demand Drivers Analysis, Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2032

Overview

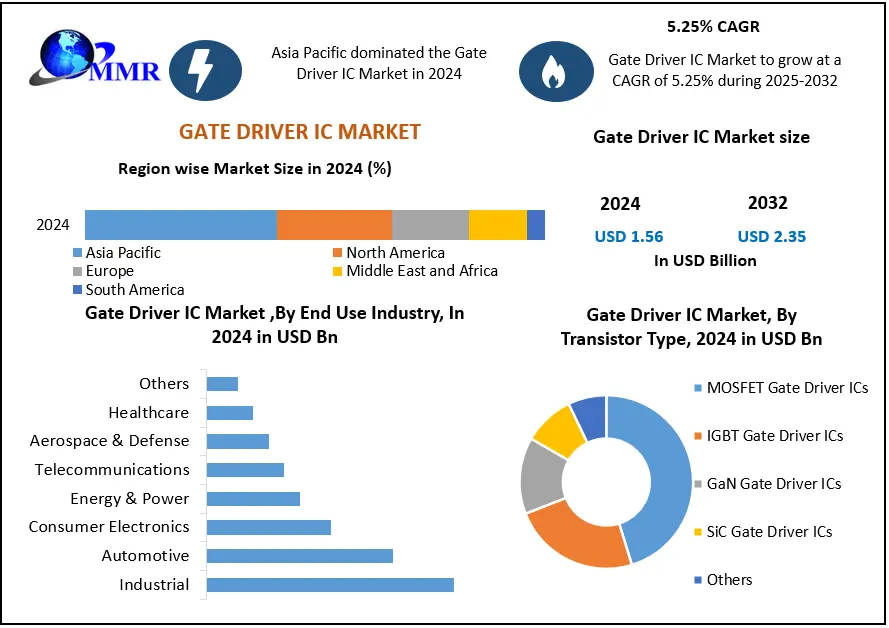

The Gate Driver IC Market size was valued at USD 1.56 Billion in 2024, and the total revenue is expected to grow at CAGR of 5.25 % from 2025 to 2032, reaching nearly USD 2.35 Billion.

The Gate Driver IC Market Report by MMR provides an in-depth analysis encompassing all key dimensions of the industry. It covers the impact of Artificial Intelligence on design, manufacturing, and market dynamics; detailed pricing and cost structure analysis; and a comprehensive technology and innovation landscape highlighting advancements in SiC and GaN drivers. The report further includes application and adoption metrics across major sectors, import-export dynamics, and an extensive review of the supply chain and manufacturing ecosystem. it offers a forward-looking investment and strategic outlook, along with dedicated sections on ESG integration and global regulatory frameworks, ensuring a holistic understanding of market trends, opportunities, and competitive positioning.

Gate Driver IC Market Overview:

Gate Driver IC is an integrated circuit chip that controls power dissipation, current flow, and heat flow in high-power transistor gates, such as MOSFET gate driver IC and IGBT gate driver IC and starts smooth switching operations in high-power transistor gates. Gatekeeper MOSFETs are commonly used in switching applications. The isolated gate-electrode of a MOSFET/IGBT forms a capacitor (gate capacitor) that must be charged or discharged every time the transistor is turned on or off. Because each transistor requires a certain gate voltage to turn on, the gate capacitor must be charged to at least that voltage for the transistor to turn on. Its driver IC is in charge of controlling this voltage. The gate driver IC market is expected to register a CAGR of approximately 5% during the forecast period.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

In recent years, a substantially higher number of home appliances, electric vehicles, hybrid vehicles (including mild hybrids), and renewable energy goods include on-board dedicated power semiconductor devices. The majority of these applications use power MOSFETs and IGBTs as power switches, while gate drivers and IGBT and MOSFET applications have varied adoption rates. MOSFETs were coupled to more than 60% of gate drivers used in power applications in 2020. Despite this, the revenue disparity between MOSFET and IGBT gate drivers is rapidly closing.

Gate Driver IC Market Research Methodology

The research report relies heavily on both primary and secondary data sources. The research process entails the investigation of various factors affecting the industry, such as government policy, market environment, competitive landscape, historical data, current market trends, technological innovation, upcoming technologies, and technical progress in related industries, as well as market risks, opportunities, market barriers, and challenges. All conceivable elements influencing the markets included in this research study have been considered, examined in depth, validated through primary research, and evaluated to provide the final quantitative and qualitative data. The market size for top-level markets and sub-segments is normalized, and the impact of inflation, economic downturns, regulatory & policy changes, and other variables is factored into the market forecast. This data is combined and added with detailed inputs and analysis, and presented in the report.

Gate Driver IC Market Dynamics:

New Technical Requirements in Power Transistors Demanding More Development in Driver ICs: Owing to the need for isolation integration, single-channel and half-bridge gate driver ICs will become more popular in the next few years. In 2020, half of bridge gate driver ICs are thought to have accounted for more than 40% of gate driver revenues. With roughly 30% of sales, single-side gate driver ICs were the second most prevalent architecture. For low-mid power, full bridge and three-phase gate drivers are commonly used in motor control and inverter applications. In recent years, all major players have begun to provide isolation-integrated devices, the most common of which is the coreless transformer. Many system manufacturers prefer to have isolation in the same package as the driver IC since it allows for further integration.

Aside from isolation methods, gate drivers can benefit from specialty applications such as high-temperature (HT) operation and other hard environment needs. Because of the material's high Tj and Te performance qualities, SiC-based power switches can withstand high temperatures. Cissoid and X-Rel Semiconductor, for example, are attempting to capitalize on SiC's potential in these niche applications.

GATE Driver Supply Chain is Integrating along with Rising Semiconductor Demand: Other actors in the supply chain have developed to offer alternate solutions for varied power management demands, in addition to gate driver IC manufacturers. Intelligent Power Modules (IPMs) and Plug-and-Play (PnP) gate driver boards are two of the most notable alternatives. To satisfy the demand for small, efficient, and application-specific power management, an IPM combines control, protection, gate driver, and power switching devices in a single package. White goods and motor control account for more than 70% of all IPMs. Moreover, the top five gate driver IC suppliers, including NXP, Infineon, and STMicroelectronics, control more than half of the market, with most of them also competing in the power semiconductor area. The power semiconductor industry is less consolidated than other semiconductor categories like as memory, CPU, and sensors, but it can still present an opportunity for enterprises to expand with the correct business model and strategy.

Adoption of Smart Home and Smart Grid Technologies: Urbanization, climate change, and population shift have compelled cities to improve their infrastructure in order to ensure seamless integration of renewable energies and reliable grids, and so preserve a good quality of life for city dwellers. Furthermore, as technology improves, electronic systems are becoming more compatible with technological changes. Home appliances and other electronic devices, notably in-home security infrastructure such as automatic door locks, smart plugs, and lights, are meant to communicate with customers over the internet. As a result, the introduction of smart home and smart grid technologies has the potential to increase gate driver IC sales. Electronic devices used in smart grids and smart homes to assure power utilization need the use of gate driver ICs to conserve energy consumption, which has a favorable influence on the gate driver IC and its demand, driving the gate driver IC market growth.

Increasing Use of New Materials to Integrate the Drives: The level of integration will be raised thanks to new materials like SiC and GaN. Both SiC and GaN devices have been in the works for a long time. Companies are shifting their focus away from components and toward system-level solutions to recuperate costs and maximize profits. Other companies that have traditionally avoided investing in these two materials can benefit from obtaining product portfolios and expertise from other companies.

Design Complexities of Gate Driver ICs: Design complexity is one of the primary issues impeding the growth of the gate driver IC industry. Microprocessors often have a large number of transistors and long copper connections. Furthermore, transistors should be extremely dependable. The gate driver IC design chain is far more sophisticated than those of other processors. Various complexities, such as thinner IC versions, the use of metallic casings, and others, reduce gate driver efficiency. The development of a good gate driver necessitates careful attention, accuracy, and a qualified team, which severely limits the growth of the gate driver IC market. The high cost of installation in automobiles is projected to impede worldwide market growth since this aspect contributes to higher car prices. Thus; the aforementioned factors are expected to have a significant impact on the growth of the gate driver IC industry.

Gate Driver IC Market Segment Analysis:

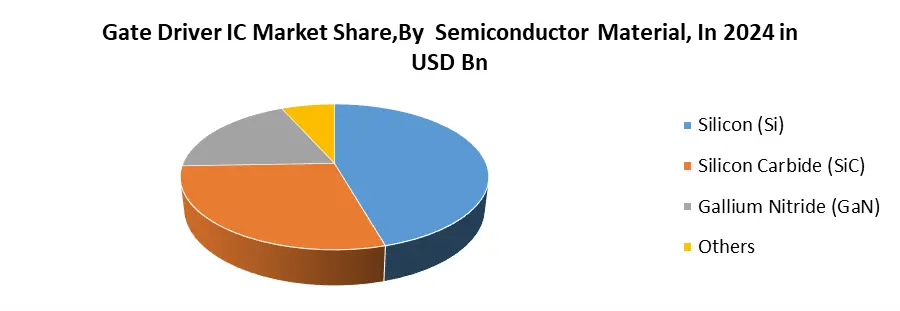

Based on the Semiconductor Material, In 2024, Silicon (Si) is expected to dominate the global Gate Driver IC Market, owing to its widespread adoption, proven reliability, and cost-effectiveness in conventional power management and industrial applications. However, Silicon Carbide (SiC) is rapidly gaining traction due to its superior efficiency, higher thermal conductivity, and suitability for high-voltage, high-temperature environments especially in EVs, renewable energy, and industrial drives. Gallium Nitride (GaN) follows, driven by growing use in fast-charging, data centers, and telecom power systems, where high switching frequency and compact form factors are critical. Other materials, including hybrid or emerging compound semiconductors, hold a niche share but are expected to expand gradually with ongoing R&D and performance optimization efforts.

Based on Isolation Type, In 2024, Isolated Gate Driver ICs are expected to dominate the global Gate Driver IC Market, driven by their superior safety, noise immunity, and suitability for high-voltage applications such as electric vehicles, industrial automation, and renewable energy systems. Their ability to provide galvanic isolation between control and power circuits enhances system reliability and protects against electrical faults. Non-Isolated Gate Driver ICs continue to hold significance in low- and mid-voltage applications like consumer electronics and small motor drives, where cost efficiency and compact design are prioritized. Although isolated types lead in terms of value and adoption across critical power systems, non-isolated variants are projected to witness steady growth in volume due to their widespread use in cost-sensitive and space-constrained applications.

Gate Driver IC Market Regional Analysis:

Asia Pacific is dominating the market with a share of 38%. Factors attributing to the growth of the region are increasing penetration of semiconductors in consumer electronics and automotive sectors. Moreover, semiconductor manufacturing trends have shifted towards IOT and 5G telecommunication services as players are diversifying their portfolios to increase their presence on regional grounds. China is the hottest market with a 56% market share owing to increasing cases and configurations for a wide range of products in the region.

During the forecast period, North America is expected to have a considerable share of the gate driver IC market. This is due to the presence of key competitors in the region as well as the rising demand for electric and hybrid vehicles. During the forecast period, South America is expected to have a substantial growth rate in the gate driver IC industry. The rising adoption of electric and hybrid vehicles is boosting market demand for consumer electronics devices with high-end data transmission capabilities, increasing the demand for gate driver ICs in South America. During the forecast period, Europe is expected to grow at the fastest CAGR. This region's success may be ascribed to increased R&D spending by major companies, which has resulted in the creation of novel products that meet a variety of application needs.

Gate Driver IC Market Report Scope:

The Gate Driver IC Market research report covers product classification, product application, development trend, product technology, competitive landscape, industrial chain structure, industry overview, national policy and planning analysis of the industry, and the most recent dynamic analysis, among other things. The report discusses the global market's drivers, opportunities, and limitations. It discusses the influence of various drivers, trends, and restraints on market demand during the forecast period.

The research also outlines market potential on a global scale. The research includes the production time, base distribution, technical characteristics, research and development trends, technology sources, and raw material sources of main Gate Driver IC Market firms in terms of production bases and technologies. The more precise study also contains the primary market and consumer application sectors, significant regions and consumption, major producers, distributors, raw material suppliers, equipment providers, and their contact information, as well as an industry chain relationship analysis. This report's study also contains product specifications, manufacturing processes, cost structure, and data information organized by area, technology, and application.

Gate Driver IC Market Scope: Inquire before buying

| Global Gate Driver IC Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 1.56 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.25% | Market Size in 2032: | USD 2.35 Bn. |

| Segments Covered: | by Transistor Type | MOSFET Gate Driver ICs IGBT Gate Driver ICs GaN Gate Driver ICs SiC Gate Driver ICs Others |

|

| by Gate Driver Type | Half-Bridge Gate Drivers Full-Bridge Gate Drivers High-Side Gate Drivers Low-Side Gate Drivers Three-Phase Gate Drivers Others |

||

| by Isolation Type | Isolated Gate Driver ICs Non-Isolated Gate Driver ICs |

||

| by Semiconductor Material | Silicon (Si) Silicon Carbide (SiC) Gallium Nitride (GaN) Others |

||

| by Application | Power Supplies (AC-DC, DC-DC Converters) Motor Drivers Class D Audio Amplifiers Industrial Automation Consumer Electronics (TVs, Laptops, etc.) Renewable Energy Systems (Solar, Wind) Electric Vehicles & Charging Infrastructure Data Centers and Servers Others |

||

| by End Use Industry | Automotive Industrial Consumer Electronics Telecommunications Aerospace & Defense Energy & Power Healthcare Others |

||

| by Channel Type | Single Channel Dual Channel Multi-Channel |

||

Gate Driver IC Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Gate Driver IC Market Key Players

1. Infineon Technologies AG

2. STMicroelectronics

3. Texas Instruments Incorporated

4. Toshiba Electronic Devices & Storage Corporation

5. Renesas Electronics Corporation

6. Semiconductor Components Industries, LLC

7. Analog Devices

8. Microchip Technology Inc.

9. NXP Semiconductors

10. Mitsubishi Electric Corporation

11. Fuji Electric

12. Rohm Semiconductor

13. Vishay Intertechnology

14. Diodes Incorporated

15. uPI Semi Corp

16. Sanken Electric

17. Semikron Danfoss

18. Delta Electronics

19. Hitachi Power Semiconductor Device Ltd.

20. Broadcom Inc.

21. Monolithic Power Systems, Inc.

22. Power Integrations (US)

23. Semtech Corporation (US)

24. IXYS Corporation (US)

25. Everlight Europe GmbH

26. Skyworks Solutions, Inc.

27. NOVOSENSE Microelectronics Co., Ltd

28. Wolfspeed, Inc.

29. Allegro MicroSystems

30. Efficient Power Conversion Corporation, Inc.

31. Others

Frequently Asked Questions:

1] What segments are covered in the Gate Driver IC Market report?

Ans. The segments covered in the Gate Driver IC Market report are based on Transistor Type, Gate Driver Type, Isolation Type, Semiconductor Material, Application, End Use Industry, Channel Type and region

2] Which region is expected to hold the highest share of the Gate Driver IC Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Gate Driver IC Market.

3] What is the market size of the Gate Driver IC Market by 2032?

Ans. The market size of the Gate Driver IC Market by 2032 is USD 2.35 Bn.

4] What is the growth rate of the Gate Driver IC Market?

Ans. The Global Gate Driver IC Market is growing at a CAGR of 5.25% during the forecasting period 2025-2032.

5] What was the market size of the Gate Driver IC Market in 2024?

Ans. The market size of the Gate Driver IC Market in 2024 was USD 1.56 Bn.