Europe Fiber Reinforced Plastic Recycling Market Size by Material Type, Recycling Technology, End Use, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

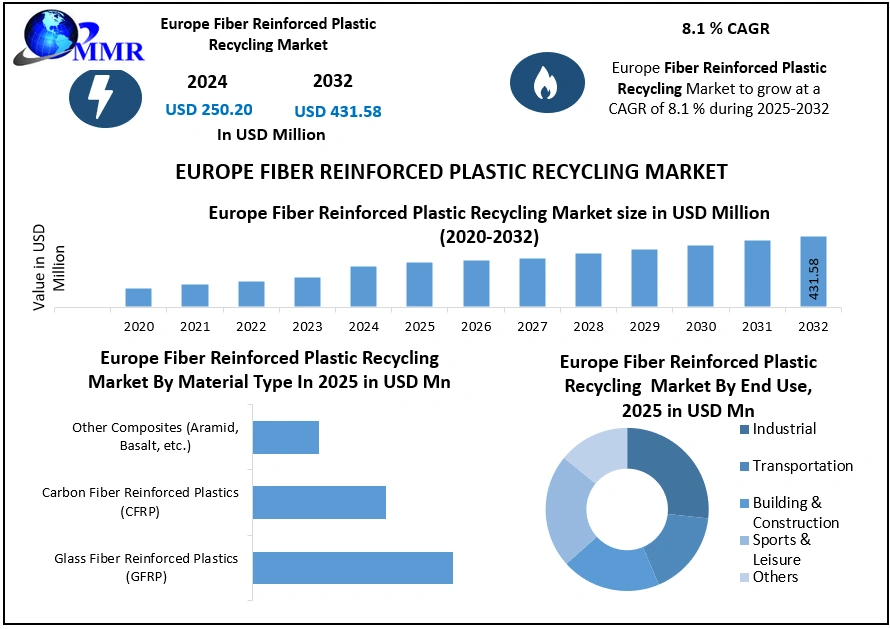

The Europe Fiber Reinforced Plastic Recycling market size was valued at USD 250.20 Million in 2025, and the total Europe Fiber Reinforced Plastic Recycling revenue is expected to grow at a CAGR of 8.1% from 2025 to 2032, reaching nearly USD 431.58 Mn.

Europe Fiber Reinforced Plastic Recycling Market Overview

Fiber Reinforced plastic recycling involves reprocessing composite waste (carbon or glass fiber embedded in plastic) into reusable materials through mechanical, thermal, or chemical methods. It supports circular economy goals by transforming end-of-life aerospace, automotive, and wind turbine components into high-value raw materials, reducing landfill waste and costs.

Europe Fiber Reinforced Plastic recycling market is driven by stringent EU regulations, automotive/wind energy sector demand, and advanced recycling technologies such as pyrolysis, although high cost and infrastructure gaps increase. Glass-Fiber Reinforced plastic (GFRP) dominates material types due to cost-effective recycling, while mechanical recycling leads in technology. Automotive waste is the largest source, which benefits from the established collection network, and the construction filler is the top end-use. Europe has a 55% global market, led by Germany and France, with prominent players such as ELG Carbon

Europe Fiber Reinforced Plastic Recycling Market Update (2024)

The European Fiber Reinforced Plastic Recycling Industry is experiencing accelerated growth driven by stringent EU landfill bans (effective 2025) and €380M in Horizon Europe funding for advanced recycling infrastructure.

Europe Fiber Reinforced Plastic Recycling Market Recent Development

| Year | Company | Recent Development |

| March-12-2024 | ELG Carbon Fibre (UK) | Europe Fiber Reinforced Plastic Recycling manufacturer opened a new pyrolysis plant in the UK with a €20M investment to recycle 2,000 tons per year of aerospace CFRP waste. |

| June-5-2024 | SIGRA (Germany) | A leading Europe Fiber Reinforced Plastic Recycling supplier launched Europe’s largest GFRP recycling facility, with a capacity of 50,000 tons per year, targeting automotive and construction waste in the Europe Fiber Reinforced Plastic Recycling industry. |

Europe Fiber Reinforced Plastic Recycling Market Recent News

May 2024: France bans landfilling of composite waste, pushing €200M into pyrolysis plants. Vestas partners with chemical giants to scale up solvent-based blade recycling by 2025.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Europe Fiber Reinforced Plastic Recycling Market Dynamics

Growing Demand from the Automotive & Wind Energy Sectors to Boost the Europe Fiber Reinforced Plastic Recycling Market Growth

Europe Fiber Reinforced Plastic recycling market is experiencing robust growth, driven by stringent environmental regulations like the EU Landfill Directive banning untreated FRP waste by 2025, alongside rising demand from the automotive and wind energy sectors. Advancements in recycling technologies, such as pyrolysis and solvolysis, along with industry-government collaborations promoting circular economy practices, are accelerating the Europe Fiber Reinforced Plastic recycling market.

Cost, Quality, and Infrastructure to Create Europe Fiber Reinforced Plastic Recycling Market Challenge

The growth of Europe's Fiber Reinforced Plastic recycling market faces significant hurdles, including high processing costs of USD 1,500–USD2,500/tonne for pyrolysis compared to just USD 1,000/tonne for landfilling (CE Delft, 2023), with only 30% of FRP waste currently recycled due to infrastructure gaps (European Composites Industry Association, 2024). The economic viability remains challenged as virgin carbon fiber (USD 20–USD 30/kg) competes closely with recycled (USD 15–USD25/kg), while limited infrastructure - with just 5 dedicated EU recycling plants (Smithers, 2025) - and regulatory inconsistencies (40% of EU nations lack FRP recycling mandates further constrain market expansion despite rising sustainability demands.

Environmental Regulations and Corporate Sustainability to Create Europe Fiber Reinforced Plastic Recycling Market Opportunity

Stringent environmental regulations and growing corporate sustainability commitments are driving significant opportunities in Europe's Fiber Reinforced Plastic recycling market, with the EU's Circular Economy Action Plan and End-of-Life Vehicle Directive (requiring 95% material recovery by 2032) creating a robust regulatory framework that already covers over 60% of fiber reinforced plastic recycling waste streams.

Emerging Opportunities in the FRP Recycling Reinforced Plastic Recycling Market Driven by Regulations, Sustainability, and Wind Energy Waste

| Factor | Key Statistic | Impact on FRP Recycling Market |

| Environmental Regulations | EU landfill bans on untreated FRP waste by 2025 | Forces Fiber Reinforced Plastic recycling industries to adopt recycling, boosting demand |

| Corporate Sustainability | 90% fiber recovery via pyrolysis/solvolysis | Enables high-value material reuse, attracting investors |

| Wind Energy Sector Demand | 50,000 tonnes/year of wind blade waste by 2030 | Creates urgent need for large-scale GFRP recycling solutions |

Europe Fiber Reinforced Plastic Recycling Market Segment

Based on Material Type, the Europe Fiber Reinforced Plastic recycling market is segmented into Glass-Fiber Reinforced Plastic, Carbon-Fiber Reinforced Plastic, and Other Composites (Aramid, Basalt, etc.). Glass Fiber Reinforced Plastic Segment has dominated the Europe Fiber Reinforced Plastic recycling market in 2025 and is expected to hold the largest market share over the forecast period. Due to its extensive use in the automotive and construction sectors, it generates the highest waste volumes. Its cost-effective mechanical recycling process (3-5x cheaper than carbon fiber methods) and alignment with EU circular economy policies favoring easily recyclable materials solidify its leading position, despite growing interest in carbon fiber recycling for high-value applications.

Based on Recycling Technology, the Europe Fiber Reinforced Plastic recycling market is segmented into Mechanical Recycling, Thermal Recycling, and Chemical Recycling. Mechanical Recycling Segment has dominated the Europe Fiber Reinforced Plastic recycling market in 2025 and is expected to hold the largest market share over the forecast period, due to its cost-effectiveness and compatibility with widely used glass fiber composites (GFRP). The process, involving shredding and grinding waste into reusable fillers, requires lower capital investment (USD 0.5M– USD 1M per plant, making it ideal for construction and automotive applications. While pyrolysis and solvolysis grow for carbon fiber recovery, their higher costs (USD 2– USD 4/kg) and complex infrastructure limit adoption, cementing mechanical recycling as the preferred solution for high-volume GFRP waste streams under EU circular economy mandates.

Based on Source of Waste, the market is segmented into Automotive, Transportation, Aerospace & Defense, Wind Energy (Turbine Blades), Construction & Infrastructure, Marine & Sports Equipment, and Other. The Automotive Sector Segment has dominated the market in 2024 and is expected to hold the largest market share over the forecast period. The automotive sector dominates Europe's FRP waste stream, producing over 40% of total recycled volume. This leadership stems from stringent EU End-of-Life Vehicle (ELV) regulations mandating 95% material recovery, coupled with high glass fiber usage in vehicle components. The sector benefits from established collection networks and cost-effective mechanical recycling methods for GFRP.

Based on End-Use Application, the market is segmented into Fillers & Additives (Construction materials), Recycled Fiber Reuse (Non-structural parts), and Energy Recovery (Waste-to-energy). Fillers & Additives (Construction materials) Segment has dominated the market in 2024 and is expected to hold the largest market share over the forecast period. Due to €1.2 billion in EU circular construction funding. Automotive reuse follows at 30%, projected to supply 25% of non-structural car parts by 2025, while energy recovery remains limited to 5% under EU sustainability policies. Germany and Poland lead adoption, currently processing 60% of construction-grade GFRP waste, driven by cost-effective material solutions and strong regulatory support for circular economy practices in building materials.

Europe Fiber Reinforced Plastic Recycling Market Country Analysis

Holding over 55% global share in 2025, driven by stringent EU regulations like landfill bans and Circular Economy Action Plan targets mandating 70% composite recycling rates. The region processes 60% of the world's wind turbine blade waste, with industry leaders like Siemens Gamesa and Vestas pioneering scalable solutions. Heavy R&D investments (e.g., Horizon Europe's Fiber Use project) and mature recycling infrastructure further solidify its lead.

Europe Fiber Reinforced Plastic Recycling Market Competitive Landscape

The competitive environment for the Europe Fiber Reinforced Plastics (FRP) recycling sector includes the presence of a mixture of specialized recyclers; technology-focused businesses; and companies that have been defined as regionally focused composite recovery organizations. For example, SIGRA Composite and ELG Carbon Fibre Ltd. have emerged as the leaders in the development and commercialization of industrial-scale carbon fibre recycling and continue to provide recyclers with recycled carbon fibres for automotive, aerospace, and industrial applications. Carbon Fibre Recycling and CFK Valley Stade Recycling, together, have established themselves as leaders in process innovation and closed-loop recycling and are helping manufacturers meet their sustainability initiatives across the continent of Europe. Conversely, Shocker Composites and MCR Recycling have placed emphasis on developing mechanical and hybrid solutions for recycling glass and carbon fibre composites and serve the construction and wind energy sectors by addressing the waste streams of these industries. A new wave of players, such as Carbon Cleanup, are becoming increasingly competitive by leveraging cost-effective recovery technologies as well as establishing localized collection networks resulting in greater levels of technological adoption and friendly competition within the European FRP recycling marketplace.

Europe Fiber Reinforced Plastic Recycling Leaders – Technological and Operational Profiles

| Attribute | ELG Carbon Fibre Ltd. (UK) | SIGRA Composite (Germany) |

| Core Focus | Carbon fiber recycling (CFRP) | Glass fiber recycling (GFRP) |

| Recycling Method | Pyrolysis-based recovery | Mechanical processing (shredding, milling) |

| Key Sectors Served | Aerospace, automotive, and high-performance industries | Construction, automotive, industrial fillers |

| Fiber Purity | 90 %+ purity (near-virgin quality) | Lower purity (optimized for bulk applications) |

| Revenue (2023) | Not publicly disclosed (dominant in CFRP recycling) | £2,761.2 million |

| Scale | Large-scale CFRP recovery (global supply chain) | High-volume GFRP recycling (regional EU focus) |

| Regulatory Driver | EU circular economy policies (high-value materials) | Germany’s strict recycling laws (e.g., Kreislaufwirtschaft) |

| Key Advantage | Patented pyrolysis tech; aerospace-grade output | Cost-effective filler production for construction |

| EU Project Role | Likely participant in FiberEUse (CFRP focus) | Active in FiberEUse (GFRP integration) |

| Sustainability Claim | Reduces carbon footprint by 90% vs. virgin CF | Diverts glass waste from landfills (circular loops) |

Europe Fiber Reinforced Plastic Recycling Market Scope: Inquire before buying

| Europe Fiber Reinforced Plastic Recycling Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2024: | USD 250.20 Mn |

| Forecast Period 2026 to 2032 CAGR: | 8.1% | Market Size in 2032: | USD 431.58 Mn |

| Segments Covered: | by Material Type | Glass Fiber Reinforced Plastics (GFRP) Carbon Fiber Reinforced Plastics (CFRP) Other Composites (Aramid, Basalt, etc.) |

|

| by Recycling Technology | Incineration & Co-Incineration Thermal/Chemical Recycling Mechanical Recycling |

||

| by End Use | Industrial Transportation Building & Construction Sports & Leisure Others |

||

Europe Fiber Reinforced Plastic Recycling by Regions

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Europe Fiber Reinforced Plastic Recycling Key Players are:

1. SIGRA Composite

2. ELG Carbon Fibre Ltd.

3. Carbon Fiber Recycling

4. CFK Valley Stade Recycling

5. Shocker Composites

6. MCR Recycling

7. Carbon Cleanup

8. Others

Frequently Asked Questions

1] What segments are covered in the Europe Fiber Reinforced Plastic Recycling Market report?

Ans. The segments covered in the Market report are based on Material Type, Recycling Technology, End-Use, and Country.

2] What is the market size of the Market by 2032?

Ans. The market size of the Market by 2032 is USD 431.58 Mn.

3] What is the growth rate of the Market?

Ans. The Market is growing at a CAGR of 8.1 % during the forecasting period 2026-2032.

4] What was the market size of the Market in 2024?

Ans. The market size of the Market in 2025 was USD 250.20 Million.