Drone Software Market Size by Solution, Architecture, Deployment, Deployment Mode, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

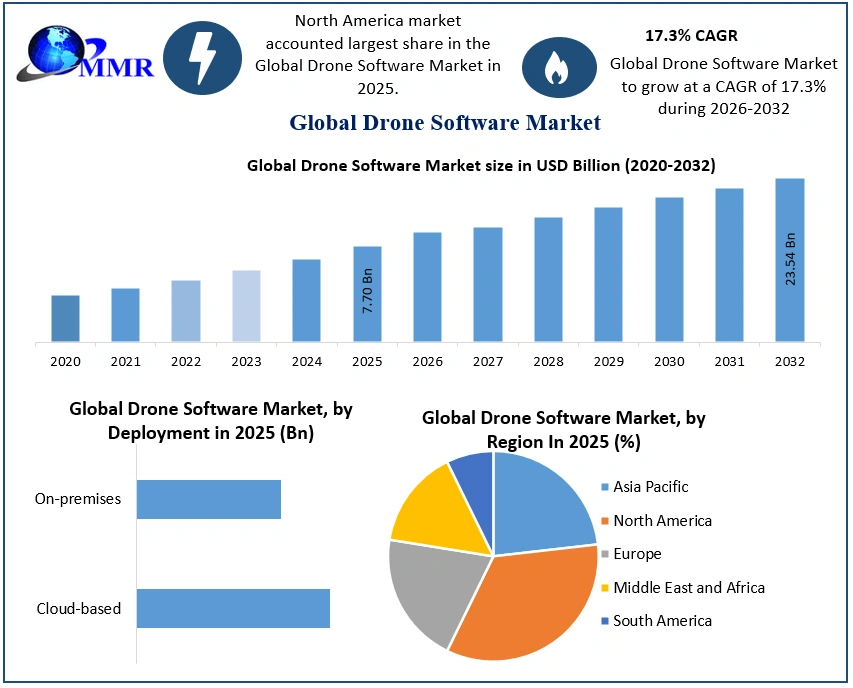

The Drone Software Market size was valued at USD 7.70 Billion in 2025 and the total Drone Software revenue is expected to grow at a CAGR of 17.3% from 2026 to 2032, reaching nearly USD 23.54 Billion by 2032.

Drone Software Market Overview

Drone software is the type of software that controls, processes and analyses data captured by drones. It has been used for a variety of resolutions such as mapping and surveying, videography photogrammetry and data analysis. The software is accountable for controlling the flight of the drone. It involves features including flight planning, real-time telemetry, waypoint navigation and autopilot functions. Drone data capture software permits operators to gather data from several sensors and cameras on the drone. Analysis software processes and interprets this data, offering valuable insights for various applications, such as agriculture, environmental monitoring and infrastructure inspection. Technological advancements, urban planning and smart cities and emergency response and disaster management are the driving factors for the Drone Software Market. The market report focuses on the drivers, challenges and major restraints of the Drone Software industry. The report contains a comprehensive analysis of the global Drone Software market's trends, forecasts, and monetary values. The qualitative and quantitative methods are included in the report for the analysis of the data of the market.

To know about the Research Methodology :- Request Free Sample Report

Drone Software Market Dynamics

Growing adoption of Drones to fuel the Drone Software Market growth

Drones are adopted across a broad range of industries such as agriculture, construction, energy, transportation and public safety. These industries need specialized software to maximize the capabilities of drones for their specific requirements. Drones have been performing tasks more efficiently and at a lower cost compared to traditional methods. For instance, in agriculture, drones have been quickly surveying large fields and providing insights on crop health, resulting in targeted interventions and minimizing resource wastage. Drone software enhances these efficiency gains. Drones are equipped with several sensors that have been collecting vast amounts of data including images, videos and environmental measurements. Drone software enables the analysis, processing and visualization of this data, offering valuable insights for decision-making, which drive the Drone Software Market growth. Drones have been utilized for hazardous tasks including inspecting tall structures, monitoring hazardous environments and conducting search and rescue operations. By using drones and their associated software, human exposure to risks has been reduced. In industries such as agriculture and mining, precision is essential. Drone software have been assist in specific navigation, data collection and analysis, leading to precise results and improved outcomes. As drone regulations become more stringent and defined, businesses are encouraged to use reliable drone software to ensure compliance with flight regulations, airspace restrictions, and data privacy laws. Several industries and applications need tailored solutions. Drone software has been customized and integrated with existing systems, enabling the seamless integration of drones into existing workflows.

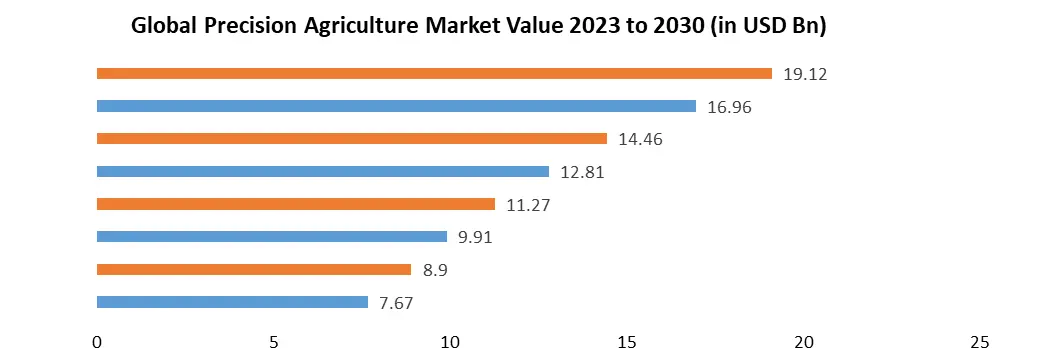

Precision Agriculture to fuel Drone Software Market growth

Precision agriculture's goals are to optimize the use of resources including water, fertilizers and pesticides. Drones equipped with specialized sensors and cameras have been capturing high-resolution imagery of fields, allowing farmers to identify areas with varying crop health and apply resources only where required. Drone software assists in processing this data and generating actionable insights for targeted interventions. Drone-collected data, when processed by advanced software, offers valuable insights into crop health, growth patterns, and stress factors. Farmers have been making informed decisions based on real-time and historical data, resulting in improved yields and minimized input costs which fuel the Drone Software Market growth. Drone software has been helping monitor crop growth and predict yield potential by analyzing data over time. This information aids farmers in adjusting their strategies and making timely decisions to maximize crop production. Drones equipped with multispectral and thermal sensors have been identify signs of pest infestations and disease outbreaks early, allowing farmers to take quick actions to moderate damage and reduce losses. For Instance, In India, drones have been enhancing overall performance and promoted farmers to solve other assorted barriers and receive plenty of advantages through precision agriculture. With the market for agricultural drones reaching an enormous USD 1.3 billion, UAVs (unmanned aerial vehicles) fill the gap between human error and the inadequacy of traditional farming methods. The resolution of adopting drone technology is to eliminate any ambiguity and instead emphasize precise and reliable information.

Drone Software Market Trend

Environmental Monitoring and Sustainability

Drones equipped with sensors and cameras have been gathering data from several environmental sources such as forests, oceans and remote areas. This data have been supporting researchers and organizations to monitor changes in ecosystems, track biodiversity and assess the impact of climate change more systematically. Drone software have been enable real-time data collection and analysis, offering instant insights into environmental conditions. This capability is precarious for responding promptly to environmental disasters such as wildfires, or natural disasters, leading to fuel the Drone Software Market growth. Drones have access to isolated and hard-to-reach locations, making them valued tools for monitoring areas that are demanding to access safely for humans. This is particularly useful for monitoring fragile ecosystems, studying wildlife and tracking changes in areas affected by pollution. Drones have a smaller carbon footprint compared to traditional data collection methods including manned aircraft or ground-based surveys. Using drones for environmental monitoring have been help minimize the overall environmental impact of data collection efforts. Drone software has been helping conservation efforts by providing accurate data on species distribution, habitat health and changes in biodiversity. This information benefits in making informed decisions to protect as well as restore ecosystems. Drones have been assisting in precision agriculture and forestry by assessing soil conditions, plant health and resource utilization. This precision results in more sustainable land management practices and optimized resource allocation which drive the Drone Software Market growth.

Drone Software Market Restraint

High Initial costs to hamper Drone Software Market growth

The substantial upfront investment needed to purchase drone hardware, software licenses and related equipment have been create a barrier to entry, especially for small businesses or start-ups with inadequate financial resources. This have been limit the ability of new players to enter the market, thereby potentially slowing overall market growth and innovation. Many businesses, especially in sectors that are exploring drone adoption, have limited budgets allocated for technology and innovation. The high cost of drone software have been make it stimulating for these businesses to justify the investment, even if the long-term advantages are significant. While drone software has various benefits including improved efficiency, data insights and cost savings, the return on investment (ROI) has not been immediately evident to potential buyers. This uncertainty regarding the potential ROI have been make decision-makers tentative to commit to the initial costs. As a result, the High Initial costs hamper the

Drone Software Market growth.

Drone Software Market Regional Insights

North America dominated the Drone Software Market in 2025 and is expected to continue its dominance over the forecast period. North America, especially the United States, is a core for technological innovation in the drone industry. The expansions in drone hardware and software capabilities such as machine learning, artificial intelligence and data analytics, are driving drone software market growth. The United States Federal Aviation Administration (FAA) has been actively working on integrating drones into national airspace. As regulations become more distinct and accommodative, industries are finding it easier to adopt drone technology and associated software for various applications. Diverse industries in the region such as agriculture, energy, construction, infrastructure inspection and public safety, are implementing drones and drone software to improve safety, efficiency, and data collection. The agriculture sector in North America has been growing adopting drones and drone software for precision agriculture. The capability to monitor crop health, optimize resource allocation, and enhance yield predictions is boosting the demand for drone software solutions which drives the Drone Software Market growth.

Drones equipped with specialized software are being used for search and rescue missions, disaster response and law enforcement operations. The effectiveness of drones in these settings is contributing to market growth. Infrastructure Inspection and Maintenance: Drone software enables efficient and cost-effective infrastructure inspection including bridges, pipelines and power lines. The requirement for regular maintenance and monitoring is fuelling the adoption of drone technology and software. North America has seen significant investment and funding in drone technology start-ups and research initiatives. This financial support is contributing to the development of advanced drone software solutions. Collaboration between research institutions, government agencies and private companies is raising innovation in the drone software market. Partnerships are boosting the development of specialized software for specific applications. Consumer, as well as commercial interest in drones, is contributing to the growth of the drone software market. Consumer drones, utilized for photography and recreation, are generating awareness and driving interest in more advanced drone software.

Drone Software Market Segment Analysis

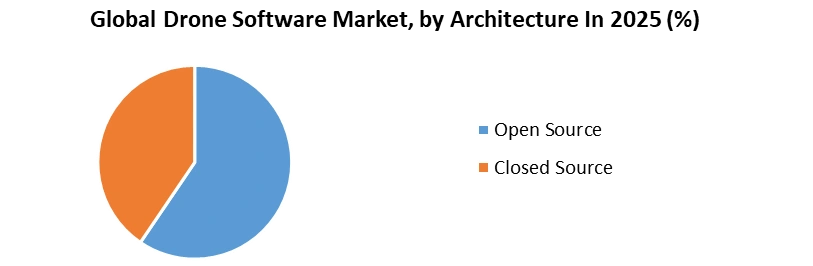

Based on Architecture, the market is segmented into Open Source and Closed Source. Open Source dominated the Drone Software Market in 2025 and is expected to have the highest CAGR over the forecast period. Open-source drone software promotes collaboration among developers, researchers and enthusiasts from around the world. This collaborative approach adopts rapid innovation, continuous improvement and the development of features compelled by real-world use cases. Open source software allows users to customize and tailor the software to their specific requirements and needs. This is especially significant in the drone industry, where several applications demand specialized functionalities. The open source development model enables rapid development cycles. Developers have been contributing code, testing new features, and offering feedback, resulting in quicker updates and releases. Open source software frequently excludes licensing fees, making it an attractive option for organizations and individuals with budget constraints. This accessibility encourages wider adoption, particularly in industries where cost considerations are significant. The open source model boosts the formation of active and engaged user communities. Users have been seeking help, sharing knowledge, and collaborating on problem-solving, leading to faster issue resolution and continuous learning. Open source software has been more easily incorporated with other tools and systems due to its open nature. This is important in the drone industry, where seamless integration with existing technologies is critical. The transparency of open source software allows users to review the source code for security vulnerabilities, improving trust and enabling swift identification and resolution of potential risks. Organizations using open source software have superior control over their technology stack. They have been adapting and modifying the software as needed, minimizing reliance on external vendors and fuelling the Drone Software Market growth.

Based on Platform, the market is categorized into Desktop Based Software and Application Based Software. Desktop Based Software held the largest Drone Software Market share in 2025 and is expected to grow at a significant CAGR during the forecast period. Desktop-based software typically provides more computational power and resources compared to mobile or web applications. This makes it appropriate for processing large volumes of data, leading complex analyses and generating detailed maps or 3D models. Industries including agriculture, land surveying and environmental monitoring have relied on detailed data analysis, boosting the preference for desktop-based solutions. Some industries need highly customized solutions to incorporate drone data with existing workflows, databases and software systems. Desktop-based software permits more flexibility in customization and integration compared to mobile apps, making it a preferred choice for industries with specialized requirements. Geographic Information Systems (GIS) and mapping applications frequently demand extensive data processing, geospatial analysis, and the creation of detailed maps. Desktop-based software offers the tools and resources required for these applications. In professional and enterprise settings, where precision and accuracy are paramount, desktop-based software has been providing more comprehensive tools for planning, executing and analyzing drone missions. Industries such as construction, infrastructure inspection, and urban planning need advanced desktop software capabilities. Desktop-based software has been operating without a continuous internet connection, which has been crucial in remote or offline environments where drones are utilized. Field operators rely on desktop software for mission planning and data analysis without requiring an internet connection which drives the Drone Software Market growth.

Drone Software Market Competitive Landscape

The Competitive Landscape of the Drone Software industry covers the number of key companies, company size, their strengths, weaknesses, barriers, and threats. It also focuses on potential, new market entrants, customers, suppliers, and substitute services that boost the profitability of Drone Software companies. The global Drone Software markets include several market players at the country, regional, and global levels. Some of the key players are Airware, Inc. (US), 3D Robotics (US), Dreamhammer Inc. (US), Drone Volt (France), Drone Deploy Inc. (US), ESRI (U.S.), Pix4D (Switzerland), Presisionhawk Inc. (US), Sensefly Ltd. (Switzerland), DJI (China), Altitude Angel (UK), Propeller Aerobatics Pty Ltd (Australia), Aloft Technologies, Inc. (US), Cyberhawk (UK), MEASURE(US) and others. Many key players conducted mergers and acquisitions to expand their solutions portfolio. For instance, in 2025 Drone Volt acquired Lorenz Technology ApS Denmark to expand its drone-based solutions portfolio. This acquisition has enabled Drone Volt to expand its portfolio of drone-based solutions and enhance its position in the global market. This acquisition has allowed DRONE VOLT to provide end-to-end drone solutions that combine hardware and software, making it a one-stop-shop for clients' requirements. It also provides DRONE VOLT with a stronger foothold in the European Drone Software Market.

Drone Software Market Scope: Inquire Before Buying

| Global Drone Software Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 7.70 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 17.3% | Market Size in 2032: | USD 23.54 Bn. |

| Segments Covered: | by Solution | System Software Application Software Flight Planning, Fleet Operation & Management Data Capture (Mapping Software) Software Development Kit (SDK) Data Processing & Analytics |

|

| by Architecture | Open Source Closed Source |

||

| by Deployment | Cloud-based On-premises |

||

| by Deployment Mode | Defense & Government Commercial Consumer |

||

Drone Software Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Drone Software Key Player

1. DJI

2. Environmental Systems Research Institute, Inc.

3. Pix4D SA

4. DroneDeploy Inc.

5. Skydio, Inc.

6. Yuneec, Inc.

7. Kespry

8. Skycatch, Inc.

9. Sharper Shape

10. AgEagle Aerial Systems Inc.

11. Emesent

12. Altitude Angel

13. DreamHammer

14. Unifly

15. Propeller Aerobotics Pty Ltd

16. ALOFT Technologies, Inc.

17. Cyberhawk

18. Other Key Players

Frequently Asked Questions:

1] What is the growth rate of the Global Drone Software Market?

Ans. The Global Drone Software Market is growing at a significant rate of 17.3 % during the forecast period.

2] Which region is expected to dominate the Global Drone Software Market?

Ans. North America is expected to dominate the Drone Software Market during the forecast period.

3] What is the expected Global Drone Software Market size by 2032?

Ans. The Drone Software Market size is expected to reach USD 23.54 Bn by 2032.

4] Which are the top players in the Global Drone Software Market?

Ans. The major top players in the Global Drone Software Market are Airware, Inc. (US), 3D Robotics (US), Dreamhammer Inc. (US), Drone Volt (France), Drone Deploy Inc. (US), ESRI (U.S.), Pix4D (Switzerland), Presisionhawk Inc. (US), Sensefly Ltd. (Switzerland), DJI (China), Altitude Angel (UK), Propeller Aerobatics Pty Ltd (Australia), Aloft Technologies, Inc. (US), Cyberhawk (UK), MEASURE(US) and others.

5] What are the factors driving the Global Drone Software Market growth?

Ans. The growing adoption of drains and precision agriculture are expected to drive market growth during the forecast period.