Distribution Panel Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

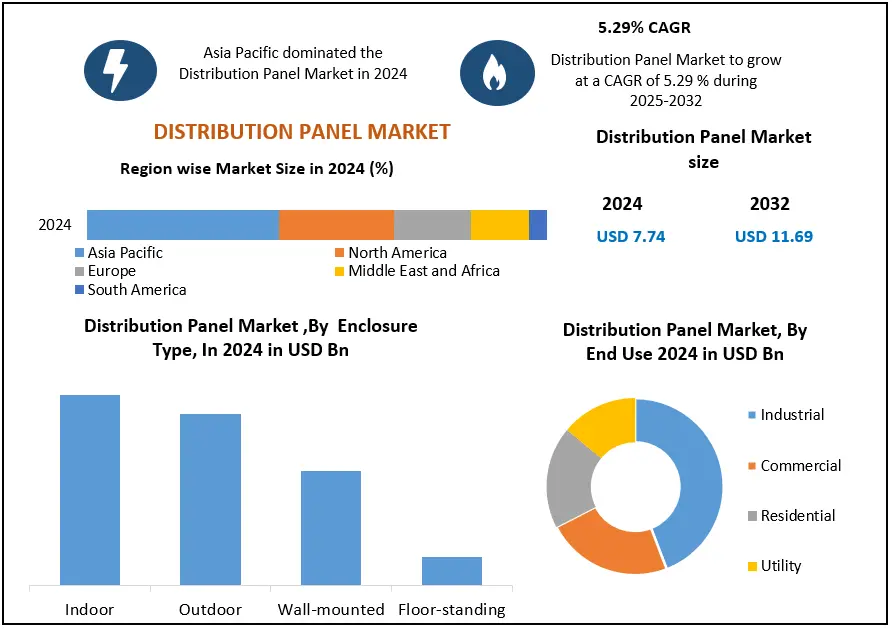

The Distribution Panel Market size was valued at USD 7.74 Billion in 2024, and the total revenue is expected to grow at CAGR of 5.29 % from 2025 to 2032, reaching nearly USD 11.69 Billion.

The MMR report covers the Distribution Panel Market through detailed analysis across key strategic and operational dimensions. It includes insights into energy sector integration, pricing and cost structures, demand and supply chain dynamics, technological innovations, trade activities, and lifecycle performance. The report also highlights sustainability initiatives, investment trends, and the evolving regulatory landscape across major regions. Each section provides an in-depth evaluation ranging from renewable energy integration and smart utility expansion to manufacturing capacity, product advancements, and global trade flow mapping. the report examines financial and strategic developments such as green financing, mergers, and alliances, enabling stakeholders to assess market opportunities, operational challenges, and growth prospects with a clear regional and industry-specific outlook.

Global Distribution Panel Market Overview

Distribution panels, also known as switchboards or panel boards, are essential for distributing electrical power to multiple circuits in industrial, commercial, and residential settings. They play a critical role in protecting electrical networks by housing circuit breakers, fuses, and associated switches. Ongoing urbanization, industrialization, and the need for consistent, centralized electrical distribution systems are driving steady growth and evolution in the Distribution Panel Market. The rising demand for smart buildings, advanced infrastructure, and renewable energy projects is further increasing the need for innovative, customizable, and energy-efficient distribution panel systems.

The new technologies and strategic advances with major Distribution panel market players. The Asia-Pacific market held the highest growth, with infrastructure improvements, grid modernization, and the rapidly industrializing economies of China, India, and Southeast Asia. Europe maintains a strong position due to strict energy regulations and the need for retrofitting older systems. Leading players such as Schneider Electric (France), Eaton (USA), ABB (Switzerland), and Larsen & Toubro (India) employ automation, digital integration, and modular systems as key strategies for the Distribution Panel market growth.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Global Distribution Panel Market Dynamics

Smart Infrastructure and Energy Optimization to Drive the Distribution Panel Market

Governments and utilities are increasingly adopting intelligent power distribution systems to enhance energy management and ensure reliable operation. These systems enable real-time monitoring for faults, optimise load sharing, and improve energy efficiency. By leveraging advanced technologies, they help reduce operational costs but also support the transition towards more sustainable energy infrastructure. At the commercial and industrial levels, advanced distribution panels are reshaping the way facilities approach safety, automation, and efficiency. Equipped with integrated IoT capabilities, sensors, and digital monitoring tools, these panels offer real-time diagnostics and control, enabling faster fault detection and proactive maintenance. This results in reduced downtime, improved operational reliability, and enhanced safety standards.

The growing emphasis on modular, space-saving, and energy-efficient distribution solutions is driving demand for these advanced panels. Their reduced footprint makes them ideal for modern infrastructure projects, while modularity allows for easier scalability and adaptability to changing power requirements. As utilities and industries work towards building resilient and future-ready power networks, smart distribution panels are emerging as a crucial component, offering both immediate operational benefits and long-term sustainability advantages. This trend is expected to increase the adoption of the advanced distribution panel market.

Regulatory Compliance and Custom Engineering to Challenge the Distribution Panel Market

In this increasingly dynamic market, companies face challenges due to regulatory compliance standards based on electrical standards of particular countries, particularly in emerging regions with wide variances in regulations. Distribution panels require a certain degree of custom-engineered designs, allowing manufacturers to satisfy a growing number of load requirements in electrical applications, but this impacts manufacturing cost and manufacturing time. The growth of the distribution panels supply chain disruptions, fluctuations in raw material prices, especially steel and copper, limited accessibility to skilled labor to manage enhanced distribution panel systems, and the management of rising system costs, with global conditions affecting the economy and business. The global economy requires companies to manage engineering flexibility, maintain compliance, and cost-effective manufacturing in the Distribution Panel Market.

Surge in Renewable Energy Integration and Data Center Expansions to Create Opportunities in the Distribution Panel Market

The accelerating global shift towards clean energy is opening significant growth avenues for the distribution panel market. Governments are investing heavily in solar, wind, and electric vehicle (EV) charging infrastructure, driving the need for panels engineered to handle advanced functionalities such as bidirectional power flow, real-time metering, and seamless microgrid integration. These capabilities are essential for efficiently managing variable renewable energy inputs while ensuring grid stability and energy reliability.

The rapid expansion of data centers is fueling demand for intelligent power distribution systems capable of managing higher capacities and ensuring uninterrupted operations. As data centers become increasingly critical for cloud computing, AI workloads, and digital services, the emphasis on uptime, energy density, and operational resilience continues to grow Distribution Panel Market.

The evolving requirements, major industry players are forming strategic partnerships with technology providers to develop next-generation switchboards equipped with artificial intelligence (AI) and machine learning (ML) capabilities. These smart systems enable predictive maintenance, dynamic load balancing, and real-time monitoring, positioning them as vital components in renewable energy infrastructure and data center ecosystems. This demand is set to accelerate the Distribution Panel Market growth in the coming years.

Global Distribution Panel Market Segment Analysis

Based on End Use, the Distribution Panel market, it is divided into Residential, Commercial, Industrial, and Utility segments. In 2024, the Industrial segment held the largest market share and is expected to maintain its dominance throughout the forecast period. This is attributed to the extensive use of distribution panels across factories, manufacturing facilities, oil & gas sites, mining operations, and large-scale infrastructure projects. Industries continue to embrace automation and adopt energy-efficient electrical systems, the demand for high-capacity and intelligent distribution panels is expected to rise significantly. Growing investments in industrial automation, electrification of manufacturing processes, and the expansion of energy-intensive facilities such as data centers, EV battery plants, and semiconductor fabs are key factors fueling this segment’s growth. Industrial end-users also demand customized solutions featuring real-time monitoring, advanced fault detection, and operational redundancy, encouraging continuous innovation among manufacturers. the commercial segment is witnessing steady growth driven by expanding installations across office complexes, healthcare facilities, and retail developments. The residential segment benefits from ongoing urbanization, electrification, and smart home system integration. The utility segment continues to grow due to grid modernization, renewable energy integration, and transmission & distribution expansion programs, particularly in developing regions focusing on power reliability and network optimization.

Global Distribution Panel Market Regional Insights

The Asia-Pacific region is expected to lead the global distribution panel industry with the continued advancement of industrialization, smart city programs, and major investments in renewable energy, as well as electric vehicle infrastructure. China, India, Japan, and South Korea are all modernizing their power grids and promoting energy-efficient building development. With government programs such as the Indian RDSS, China’s push for green energy, and initiatives promoting localized electrical manufacturing, India is likely to bolster its electrical equipment manufacturing capabilities and set the stage for it to emerge as a manufacturing hub for electrical equipment in APAC. The attraction of being a cost-effective manufacturing destination, combined with the presence of OEMs, alongside increasing levels of Foreign Direct Investment, is bolstering the APAC region's standing in the residential, industrial, and smart electrification segments, positioning the region distribution panel market.

Table: Government Funding in Distribution Panel

| Country | Program/Policy | Funding | Focus Area |

| India | Revamped Distribution Sector Scheme (RDSS) | USD 40 billion | Smart metering, power infrastructure upgrades |

| China | Dual Carbon Goals + State Grid Investment | USD 65 billion | Smart grid, renewables, power distribution |

| Japan | Green Transformation (GX) Plan | USD 20 billion | Energy-efficient buildings and grid systems |

| South Korea | Smart Energy Infrastructure Plan | USD 15 billion | Industrial electrification and automation |

Global Distribution Panel Market Competitive Landscape

Major participants in the distribution panels market on expanding their smart panel portfolio, improving energy efficiency, and integrating digital technologies. Competition in the distribution panels is dependent on digitally connected power distribution with the Internet of Things (IoT), the ability to comply with regulations, and a company's ability to provide customized solutions in the industrial, commercial, and residential markets. Companies are increasingly developing manufacturing hubs in the Asia-Pacific and the Middle East to manage lead time and local demand. Schneider Electric (France) is the major player with its EcoStruxure concept, designed for LV and MV smart panels with digital monitoring and energy management, primarily for the data center, utility, and commercial building market segments. Eaton Corporation (USA) is focusing on modular and connected panels for the modernization of the grid and renewable energy capabilities in North America, Europe, and Asia. Siemens AG (Germany), Hager Group (Germany), Alfanar (Saudi Arabia), and NHP Electrical Engineering (Australia) are building market share through cooperation with strategic partners, expanding capacity, and focusing on innovative localized solutions for sustainable smart distribution systems.

Global Distribution Panel Market Trends

| Category | Trend | Key Example | Market Impact |

| Smart Technologies Integration | Rising adoption of IoT-enabled and AI-integrated smart distribution panels | Schneider Electric’s EcoStruxure with real-time diagnostics and remote monitoring | Improves energy management, predictive maintenance, and system optimization |

| Sustainability & Energy Efficiency | Growing demand for energy-efficient and eco-friendly panel designs | ABB’s Emax 2 smart breaker and Eaton’s Green Motion panels supporting renewable integration | Supports green building codes, lowers carbon footprint, and appeals to ESG goals |

| Modular & Customizable Solutions | Shift toward pre-engineered, modular, and application-specific panels | Legrand’s user-friendly modular panels for residential and SME applications | Enhances design flexibility, shortens installation time, and reduces inventory cost |

Global Distribution Panel Market Recent Development

• Eaton (USA)

In October 2024, it expanded its manufacturing footprint in Puducherry, India by adding a 120,000 sq ft facility and doubling its capacity for developing and producing LV/MV distribution components with advanced Industry 4.0 capabilities. The expansion supports local demand from data centre and industrial customers.

• Schneider Electric (France)

In March 2025, it partnered with South Bihar Power Distribution Company as part of a project to use EcoStruxure projects to upgrade the regional grids and adapt panel upgrades to enhance reliability by 90% and minimize engineering time by 70%.

• ABB (Switzerland)

A new series of IoT-enabled distribution panels was launched in 2024 with new and enhanced fault detection, based on the ability to manage loads and utilities which will lower failure rates around 18%.

• Siemens (Germany)

In 2025, it introduced a high-efficiency, industrial grade distribution panel for heavy-manufacturing. With similar design it achieve energy loss reductions of ~15% due to improvements in reliability in power distribution.

Scope of the Global Distribution Panel Market: Inquire before buying

| Distribution Panel Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 7.74 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.29% | Market Size in 2032: | USD 11.69 Bn. |

| Segments Covered: | by Panel Configuration | Single-phase Three-phase Main Distribution Board (MDB) Sub-Distribution Board (SDB) |

|

| by Voltage | Low-Voltage (LV) Medium Voltage (MV) High Voltage (HV) |

||

| by Enclosure Type | Indoor Outdoor Wall-mounted Floor-standing |

||

| by Mounting Type | Surface-Mounted Panels Flush-Mounted Panels Floor-Mounted Panels |

||

| by End-Use | Residential Commercial College/university Office Government military Others Industrial Power generation Chemical Refinery Cement Others Utility |

||

| by Distribution Channel | Direct Sales Distributors Online Sales |

||

Global Distribution Panel Market, by Region

North America (United States, Canada, Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Philippines, Thailand, Vietnam, Rest of Asia Pacific)

Middle East and Africa (MEA) (South Africa, GCC, Nigeria, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Rest of South America)

Global Distribution Panel Market, Key Players

1. ABB

2. Schneider Electric SE

3. Siemens AG

4. Eaton Corporation plc

5. Legrand SA

6. General Electric (GE)

7. Larsen & Toubro (L&T)

8. Hager Group

9. Mitsubishi Electric Corporation

10. NHP Electrical Engineering Products

11. Lucy Electric

12. Rockwell Automation, Inc.

13. Crompton Greaves Consumer Electricals Ltd.

14. Fuji Electric Co., Ltd.

15. CHINT Group

16. E+I Engineering

17. Rittal GmbH & Co. KG

18. Hensel Electric India Pvt. Ltd.

19. Socomec Group

20. BCH Electric Limited

21. Siemens Energy

22. NHP Electrical Engineering Products

23. CHINT Group

24. Rexel Group

25. Phoenix Contact GmbH & Co. KG

26. WEG Industries

27. LS Electric Co., Ltd.

28. Others

Frequently Asked Questions

1] What segments are covered in the Distribution Panel Market report?

Ans. The segments covered in the Distribution Panel Market report are based on Panel Configuration, Voltage, Enclosure Type, Mounting Type, End-Use, Distribution Channel, and region

2] Which region is expected to hold the highest share of the Distribution Panel Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Distribution Panel Market.

3] What is the market size of the Distribution Panel Market by 2032?

Ans. The market size of the Distribution Panel Market by 2032 is USD 11.69 Bn.

4] What is the growth rate of the Distribution Panel Market?

Ans. The Global Distribution Panel Market is growing at a CAGR of 5.29 % during the forecasting period 2025-2032.

5] What was the market size of the Distribution Panel Market in 2024?

Ans. The market size of the Distribution Panel Market in 2024 was USD 7.74 Bn.