Global Database Automation Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

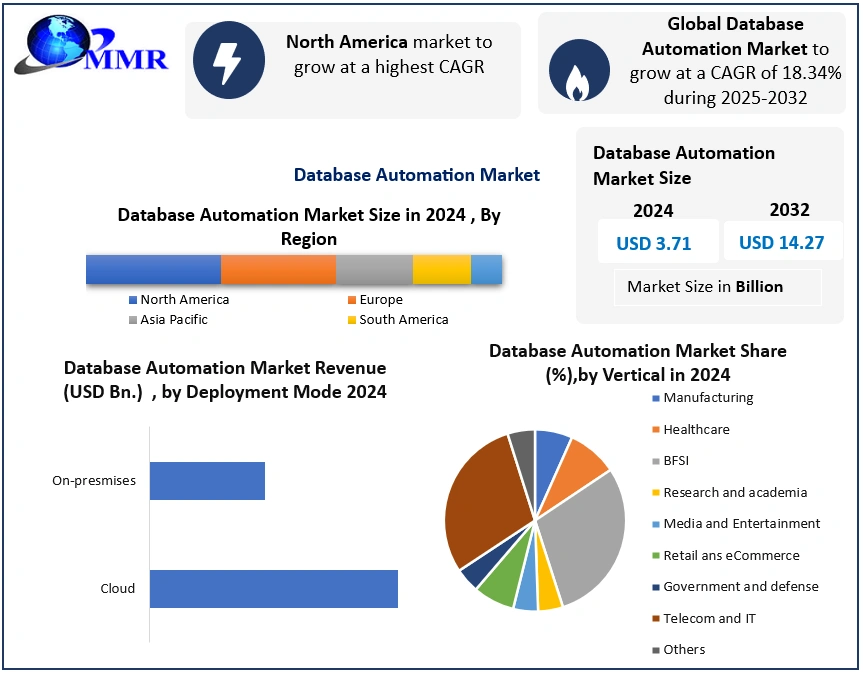

Global Database Automation Market size was valued at USD 3.71 Billion in 2024, and the total Database Automation Market revenue is expected to grow by 18.34% from 2025 to 2032, reaching nearly USD 14.27 Billion.

Database Automation Market Overview

Database automation automatically refers to the use of software tools and technologies, automatically involving the management of database, such as provisioning, configuration, patching, backup, monitoring and performing tuning performance. It plays an important role in industries including IT services, finance, healthcare, telecommunications and e-commerce, where data requires credibility and operational efficiency. The database automation market has been experiencing a rapid growth, which is inspired by increasing database data, demand and continuous deployment, and to reduce manual intervention in database administration. For example, automated database equipment is now an integral organ for modern cloud-based infrastructure, which allows for the spontaneous scaling and better uptime-mating needs for those businesses that prefer to change.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Database automation tools are engineered to be platform-oriented and often include characteristics such as policy-based management, A-estimated adaptation, real-time analysis, and integration with CI/CD pipelines. These devices improve stability, reduce human error, and free up efficient DBAs to focus on high-value strategic functions. With the rise of hybrid and multi-cloud environments, sellers are integrated into the dynamic charge, intelligent performance tuning, and support for the self-healing database system. Development is extended beyond regulatory compliance requirements, focusing on data security, and rapid data processing is sought. North America led the Database Automation Market in 2024, especially in adopting its advanced cloud infrastructure and automation, while Europe follows strong enterprise digitization trends and data security laws closely. Since the Asia-Pacific region is emerging rapidly due to cloud investment and the digital economy initiative.

Database Automation Market Dynamics

Increasing Demand for Data Efficiency and Scalability to Drive the Database Automation Tools Market

The database automation tools are experiencing strong growth due to the growing requirement for market-efficient, scalable, and safe data infrastructure. Rapidly in areas with digital changes, organizations are handling a rapidly complex and high-volume data environment. This has made database automation a requirement for continuous integration, DevOps, and enterprises pursuing agile application delivery. Automation tools reduce manual errors, lower operating costs, and improve response time - making them attractive to businesses trying to achieve high availability and data reliability. Cloud adoptions, especially hybrids and multi-cloud models, are also demanding devices that can dynamically provide a database provision, monitor and tune. In areas such as banking, healthcare, retail, and telecom, real-time data access, compliance reporting, and data stability in distributed systems further enhance the market for advanced automation capabilities. Integration of AI and machine learning in database management platforms is also re-shaping the expectations for self-healing and auto-scaling database environments.

High Complexity and Legacy Integration to Restrain the Database Automation Tools Market

Despite the strong demand, the database automation tools market faces challenges that may obstruct adoption. Integrating automation solutions with heritage database systems can be highly complex, especially in older infrastructure or silent operations. Many enterprises are cautious due to alleged risks of automation failures or unexpected changes in important data systems. Additionally, the lack of trained skilled personnel in advanced automation equipment can slow down implementation, especially in mid-shaped and public sector organizations. Licensing costs and prolonged onboarding time can further increase market growth in small businesses or developing areas. Regulatory barriers around data security, storage locations and compliance audit may also hesitate to fully automate certain database functions.

AI-Driven Tools and Cloud-Native Architectures to Open Opportunities in the Database Automation Tools Market

The future of database automation tools is connected close to the development of AI-operated analytics, cloud-country platforms and digital-first enterprise strategies. As the cloud adoption deepens, especially in the Asia-Pacific and Latin America, the demand for scalable and safe database automation will increase in the lead. Emerging technologies such as autonomous databases, low-code/no-code growth environments, and data fabric architecture provide new areas for innovation. In addition, the observation, monitoring of real -time and pushing for future performing performance management is making place for more intelligent automation tools. Mother-in-law-based models and managed services are also reducing cost barriers and making automation accessible to small firms and startups. Since stability becomes a commercial goal, energy-skilled data centers and automation systems are likely to obtain traction, opening the niche market for green IT initiatives. These trends suggest that a database automation tool developed to handle global data will be important for digital flexibility and commercial continuity in the economy.

Database Automation Market Segment Analysis

The global Database Automation Market is segmented into Components, Deployment Modes, Verticals, and Applications.

Based on Vertical, in 2024, the Telecom and IT segment accounted for a dominant share of over 34.10%. Telecom is one of the industries that generates the most data, and companies are developing cloud services primarily geared towards large-scale data integration. As the need for cloud services grows among telecom customers, collaboration between database automation and telecom companies is becoming more widespread. For example, in addition to Sielte S.P.A., Telefónica Tech has adopted Percona Kubernetes Operator to streamline database deployment and scalability across its hybrid cloud infrastructure.

The growing use of public and private clouds to manage massive amounts of data has resulted in a greater demand for better and more cost-effective database automation solutions. Oracle Autonomous Database, for example, combines the cloud's flexibility with the capability of machine learning. The solution, according to the business, may reduce administrative expenses by up to 85% with full automation of operations and tuning, as well as runtime costs by up to 92% by charging only for resources used at any given moment.

Database Automation Market Regional Analysis

In 2024, North America was responsible for the largest 38.5% market share for the growing demand for automation in the region. The US is expected to demonstrate rapid growth during 2025-2032 due to adopting advanced technologies in industries. Industries such as retail, BFSI, manufacturing and healthcare are making significant contribution to data generation using advanced technologies such as AI, IOT, smart devices, automation and more.

However, Europe is expected to account for the largest share, followed by North America, by 2032. The presence of leading industries like manufacturing, automotive, and healthcare drives the demand for database automation. The rising demand for digital technologies in economies such as the UK, France, Germany, Spain, and others drives the EU Database Automation Market growth.

Database Automation Market Competitive Landscape:

The database automation tools market includes a mixture of global technology leaders and specialized software vendors, each of which includes its unique status, innovation, and market strategies. Among the top players are Oracle Corporation (North America) and Redgate Software (Europe), which both represent different approaches for database automation through large-scale venture integration, and the other through developer-centered, flexible solutions.

Oracle Corporation, located in the United States, is a major force in the enterprise-grade database system, and its Oracle Autonomous database is a major example of full-stack automation. Oracle provides an integrated platform where machine learning algorithms handle regular functions such as sequencing, patching, tuning, and backup - reducing human error and improving safety. The company's strength lies in its deep product ecosystem, its long presence in the enterprise IT, and the capacity for scale in multi-scale, multi-cloud, and hybrid environments. Oracle's market appeal is the strongest among large organizations in finance, government, healthcare, and global commerce that demand high availability, regulatory compliance, and underlying security. Its end-to-end automation with AI-based performance tuning has made it an important player in how global enterprises manage their data infrastructure.

Database Automation Market Key Developments:

June 2025-IBM (Whatsanx/Netza) -AI-AI-Access Netza Database Assistant

IBM launched the AI-Powered Netezza database Assistant, an AI-operated chatbot operated by IBMWATSONX, which is now usually available June 24, 2025. It enables DBAS to manage Netezaza through natural language for monitoring, troubleshooting, performance insight, and new members for a user.

August 2025 -Autonomous Database on dedicated Exadata infrastructure) -Feature: Oracle Key Vault (OKV) & Point Group Association with Autonomous Contact Database (ACD)

Now you can add a new or existing autonomous container database (ACD) to the autonomous database commitment on the Exadata infrastructure dedicated to the Custom Oracle's Walt (OKV) and point Group, which can compete through the metamization of OKV concluding points for increased safety and operational flexibility.

July 2025- Oracle (Oracle database@AWS Autonomous Database on Exadata infrastructure)

Using the autonomous database on the EXADATA infrastructure dedicated to Oracle database@AWS, you can run OCI-Managed Exadata Infrastructure within AWS public sectors and availability areas, Oracle database workloads on the infrastructure, AWS S3, CloudWatch, EVIDWATCH, and AWS with the original integration for zeroetl.

Database Automation Market Key Trends:

• Global expansion of cloud data services

MongoDB Atlas, spread over the Google Cloud regions in Mexico and South Africa, reflects the increasing trend of regional cloud expansion. This enables businesses to meet the needs of local data residences, compliance, and delay when scaling globally - an important step takes into the demand for geographically distributed applications.

• Strategic cloud partnership

MongoDB earned a 2025 Google Cloud Partner of the Year (Data and Analytics - Marketplace) for the sixth year in a row, indicating a comprehensive tendency to deepen the ecosystem cooperation. Enterprises rely on rapid entrepreneurship and rush into tight integration between cloud platforms and data solutions to run customer-focused services.

Database Automation Market Scope: Inquire before buying

| Global Database Automation Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 3.71 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 18.34% | Market Size in 2032: | USD 14.27 Bn. |

| Segments Covered: | by Component | Solutions Database design and configuration automation Database patch and release automation Application release automation Database test automation Services Professional services Managed services |

|

| by Deployment Mode | Cloud On-premises |

||

| by Power Source | Hydraulic-Powered Electric-Powered Hybrid Models |

||

| by Enterprise Size | Provisioning Backup Security and compliance |

||

| by Vertical | Manufacturing Healthcare BFSI Research and academia Media and entertainment Retail and eCommerce Government and defence Telecom and IT Others (transportation, oil and gas) |

||

Database Automation Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Database Automation Market, Key Players

North America

1. Oracle Corporation (USA)

2. Amazon Web Services (AWS) (USA)

3. Microsoft Corporation (USA)

4. IBM Corporation (USA)

5. MongoDB, Inc. (USA)

6. SAP SE (USA)

7. ServiceNow, Inc. (USA)

8. UiPath Inc. (USA)

9. Quest Software Inc. (USA)

10. BMC Software, Inc. (USA)

11. Datavail (USA)

12. IDERA, Inc. (USA)

13. Pegasystems Inc. (USA)

14. Elastic N.V. (USA)

15. SnapLogic (USA)

16. Tungsten Automation (USA)

17. Redgate Software (UK)

18. Micro Focus (UK)

19. Severalnines (Sweden)

20. EnterpriseDB (EDB) (USA/India)

21. Hortonworks (now part of Cloudera) (USA/China)

22. MapR Technologies (now part of HPE) (USA)

Europe

1. Software AG (Germany)

2. Akeneo (France)

Asia-Pacific

1. HashMicro (Singapore)

2. Yonyou (China)

3. Yokogawa Electric (Japan)

Frequently Asked Questions

1] What segments are covered in the Database Automation Market report?

Ans. The segments covered in the Database Automation Market report are based on Component, Deployment Mode, Vertical, and Application.

2] Which region is expected to hold the highest share in the Database Automation Market?

Ans. North America region is expected to hold the highest share in the Database Automation Market.

3] What is the market size of the Database Automation Market by 2032?

Ans. The market size of the Database Automation Market by 2032 is US$14.27 Bn.

4] What is the forecast period for the Database Automation Market?

Ans. The forecast period for the Database Automation Market is 2025-2032.

5] What was the market size of the Database Automation Market in 2024?

Ans. The market size of the Database Automation Market in 2024 was US$3.71 Bn.