Cattle Feed Market Size by Product Type, Animal Type, Form, Ingredients, Distribution Channel, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

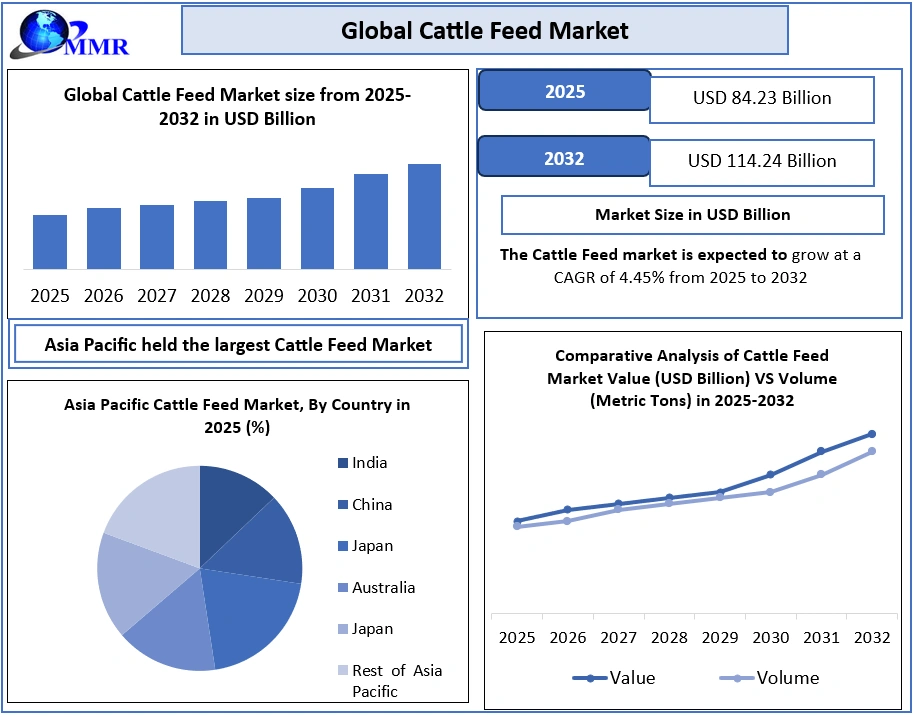

Global Cattle Feed Market 2026–2032:

The global Cattle Feed Market was valued at USD 84.23 billion in 2025 and is projected to reach USD 114.24 billion by 2032, growing at a CAGR of 4.45% during the forecast period 2026 to 2032.

Cattle Feed Market Overview

The global cattle feed market is driven by rising demand for high-quality livestock nutrition, improving feed efficiency, and the expansion of commercial dairy and beef farming. Increasing awareness among farmers regarding balanced nutrition, combined with technological advancements in feed formulation and processing, is supporting steady market growth.

To know about the Research Methodology :- Request Free Sample Report

The industry is witnessing a gradual shift toward fortified, protein-rich, and customized feed solutions aimed at improving milk yield, weight gain, and overall herd health. Additionally, growing emphasis on sustainable livestock farming practices and feed efficiency optimization is influencing feed ingredient selection and formulation strategies across regions.

Key Insights

• Protein-Rich Feed Demand: High-protein feeds such as soybean meal and fish meal play a critical role in improving cattle growth and milk yield. In 2025, over 60% of commercial dairy farms globally adopted protein-rich feed formulations.

• Sustainability Trends: Rising consumer and regulatory focus on sustainable livestock practices is driving interest in alternative feed ingredients. Insect-based protein solutions demonstrate significantly lower greenhouse gas emissions compared to conventional protein sources.

• Regional Growth: Asia-Pacific accounted for more than 50% of global cattle feed demand in 2025, supported by large livestock populations and increasing adoption of modern dairy farming practices in China and India.

• Raw Material Price Volatility: Fluctuating prices of key feed ingredients such as corn and soybean meal contributed to an estimated 8–10% increase in feed production costs, impacting profitability for small and medium-scale producers.

• Technological Innovation: Advancements in feed formulation, alternative protein development, and processing technologies are improving feed efficiency and supporting sustainability objectives.

Market Dynamics

Increasing Demand for High-Quality Protein in Livestock Feed

Rising global demand for milk and beef, driven by population growth and dietary shifts, is increasing the need for protein-rich cattle feed. In 2025, more than 60% of commercial dairy farms used formulated protein concentrates to improve productivity. High-protein feed formulations can enhance milk yield by 8–12% compared to lower-protein diets, supporting their widespread adoption across commercial operations.

Top 10 Protein Ingredients for Cattle Feed: Nutritional Benefits and Common Uses

| Sr. No. | Protein Ingredient | Protein Content | Benefits of Cattle Feed | Common Uses for Cattle Feed |

| 1. | Soybean Meal | 44–48% | Excellent amino acid profile, high digestibility, promotes muscle growth and milk yield. | Dairy cattle, beef cattle feed |

| 2. | DDGS (Distillers Dried Grains with Solubles) | 26–32% | Enhances gut health, improves feed conversion, and reduces feed cost. | Cattle feed |

| 3. | Groundnut Cake | 40–45% | Boosts weight gain, supports lean muscle growth. | Dairy cattle, goats, cattle feed |

| 4. | Rapeseed Meal (Mustard Cake) | 34–38% | Rich in methionine and cysteine; supports growth and development. | Cattle feed |

| 5. | Sunflower Meal | 28–35% | Contains methionine and healthy fats; supports immunity. | Dairy cattle, ruminant feed |

| 6. | Fish Meal | 55–65% | High in omega-3 fatty acids, calcium, and phosphorus; supports growth and feed palatability. | Cattle feed |

| 7. | Meat and Bone Meal (MBM) | 45–55% | Excellent source of protein, calcium, and phosphorus; strengthens bones and muscles. | Cattle feed |

| 8. | Cottonseed Meal | 35–40% | Improves milk production and body condition. | Cattle and sheep feed |

| 9. | Sesame Meal | 40–45% | Rich in methionine and calcium; improves growth and feed utilization. | Dairy cattle feed |

| 10. | Corn Gluten Meal | 55–60% | Enhances pigmentation, supports muscle growth, and improves productivity. | Cattle feed |

Volatility in Raw Material Prices to Restrain Cattle Feed Market Growth

Price volatility of core feed ingredients such as cereals and oilseed meals remains a key restraint for the cattle feed market. Fluctuating agricultural commodity prices and supply chain disruptions have increased feed production costs, placing pressure on profit margins, particularly for small and unorganized feed manufacturers.

• Fluctuations in Commodity Prices: The prices of key raw materials for cattle feed, such as corn and soybean meal, have experienced significant volatility. In 2025, the price of corn rose to USD 8.4 per bushel, a 56% increase from the previous year. The soybean meal prices surged by 62%, affecting production costs.

• Impact on Production Costs: The rising cost of raw materials has led to higher production costs, which could result in price increases for cattle feed products. The average cost of producing cattle feed has risen by 8-10% in the past 3 years, from 2025, due to these raw material price fluctuations.

• Profit Margin Pressure: Cattle feed manufacturers, especially in the unorganized sector, struggle to manage these costs, which can squeeze profit margins, especially for small-scale producers.

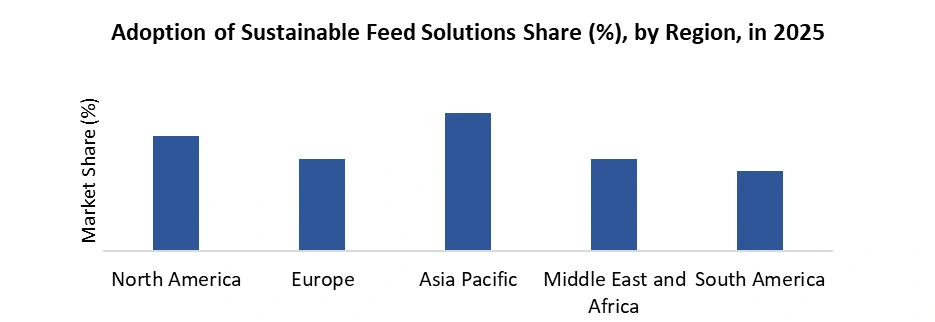

Opportunity: Adoption of Sustainable Feed Solutions

Sustainable Feed Ingredient Market: Innovations in feed ingredients, such as algae-based feed and insect protein, are gaining traction due to their lower environmental impact.

Environmental Impact Reduction: Sustainable feed solutions help reduce the carbon footprint of cattle farming. For example, insect protein production generates 50% less greenhouse gas emissions compared to traditional protein sources such as soy.

Consumer Demand for Eco-friendly Products: As consumer preferences shift towards more sustainable agricultural practices, there is an opportunity for cattle feed manufacturers to develop products that meet these environmental standards and cater to growing demand for eco-friendly livestock products.

Cattle Feed Market Segmentation Analysis:

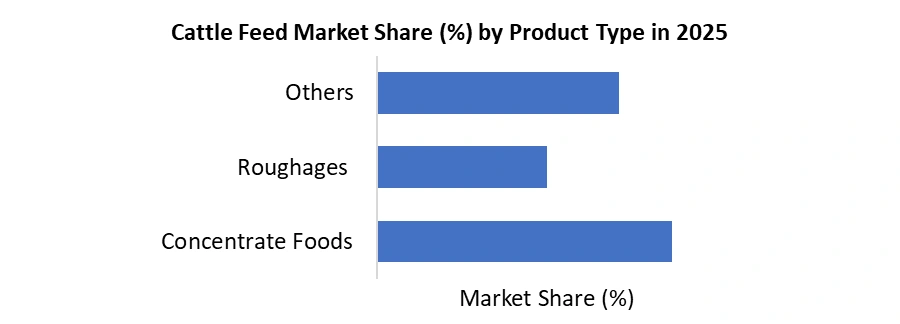

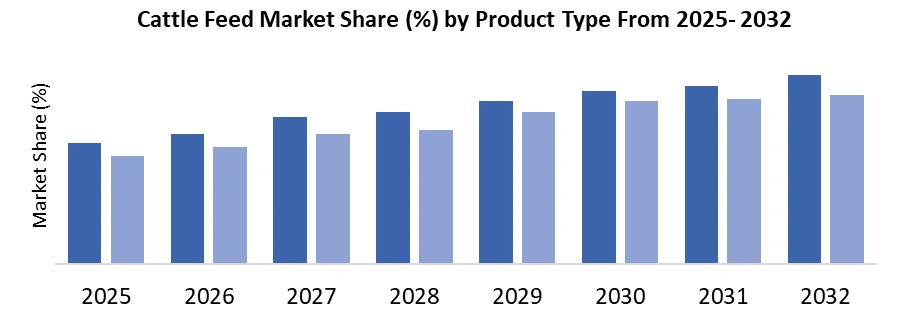

By Product Type, concentrate feeds dominated the cattle feed market in 2025. Approximately 80% of commercial cattle farms globally rely on concentrate feeds as a primary nutritional source, supplying over half of daily protein and energy requirements. High adoption is driven by improved feed conversion efficiency, faster weight gain, and higher milk yields compared to roughage-based diets

About 8 out of every 10 commercial cattle farms use concentrate feeds as the primary nutritional source. Concentrates supply over 50% of the daily protein and energy requirements for cattle compared to roughages. In major producing regions such as North America and the Asia Pacific, concentrate usage exceeds 75% of all formulated feeds. This preference is driven by the need for balanced nutrition, rapid growth, enhanced milk yields, and improved feed conversion efficiency in dairy and beef cattle.

Based on Animal Type, the market is segmented into the Dairy Cattle and Beef Cattle. Dairy cattle dominated the animal type in the cattle feed market in 2025. In leading regions such as the Asia Pacific, dairy cattle make up 60–70% of all cattle herds receiving formulated feed. On many commercial dairy farms, 8–9 out of 10 cattle are fed specialized dairy rations to support lactation, resulting in dairy feed volumes that exceed beef feed by about 15–20 percentage points. The prioritization of nutrition for milk production, milk quality, and herd health, with dairy cattle consuming the majority of nutrient-dense feed types.

Cattle Feed Market Regional Insights

Asia Pacific dominated the Cattle Feed Market in 2025 and is expected to continue its dominance over the forecast period.

Key Growth Drivers:

• Increasing meat and dairy consumption due to rising population and urbanization, particularly in countries such as China and India.

• India and China alone contribute over 60% of the Asia Pacific's cattle feed demand in 2025.

Rising Livestock Production:

• Asia Pacific is home to more than 50% of the world’s cattle population.

• Major growth in dairy and beef cattle farming, leading to higher demand for high-quality feed.

Technological Adoption: Advanced feed technologies and sustainable practices, such as insect-based feed and plant-based protein adoption, are gaining momentum in countries such as Japan and Australia.

Cattle Feed Market Competitive Landscape

The Cattle Feed Market is highly competitive, with key players such as Cargill, Inc., Archer Daniels Midland Company (ADM), Land O’Lakes, Inc., Nutreco, De Heus, and ForFarmers dominating the landscape. These companies leverage extensive distribution networks, advanced feed technologies, and sustainability initiatives to strengthen their market positions.

Recent Developments

• September 5, 2024 – Cargill has acquired two U.S. feed mills from Compana Pet Brands, located in Denver, Colo., and Kansas City, Kan., enhancing its production and distribution capabilities for the Animal Nutrition and Health business. The acquisition, finalized on September 3, 2024, allows Cargill to better serve large farming/ranching segments and local retailers.

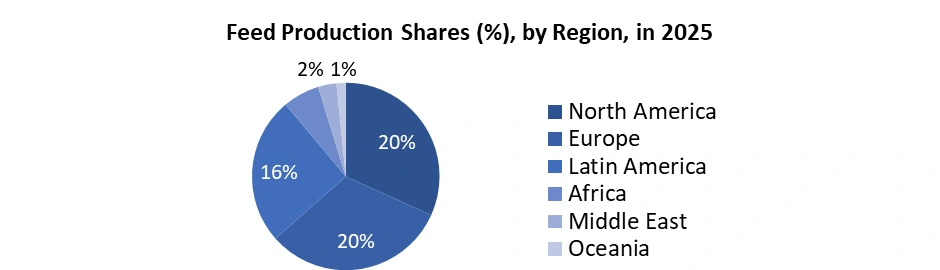

• April 29, 2025 – Alltech's 2025 Agri-Food Outlook reveals that global feed production rebounded in 2025, rising by 1.2% to 1.396 billion metric tons. North America and Latin America experienced modest growth, driven by increased beef, poultry, and pork feed production. Europe's feed production rose by 2.7%, while Africa and the Middle East posted the highest percentage growth at 5.4%, reflecting expanding commercial feeds in poultry and ruminants.

Cattle Feed Market Scope: Inquire Before Buying

| Global Cattle Feed Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 84.23 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.45% | Market Size in 2032: | USD 114.23 Bn. |

| Segments Covered: | by Product Type | Concentrate Foods Roughages Others |

|

| by Animal Type | Dairy Cattle Beef Cattle |

||

| by Form | Pellets Mash Crumble Liquid Others |

||

| by Ingredients | Cereals Cakes and Mixes Food Wastages Feed Additives Others |

||

| by Distribution Channel | Offline Online |

||

Cattle Feed Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

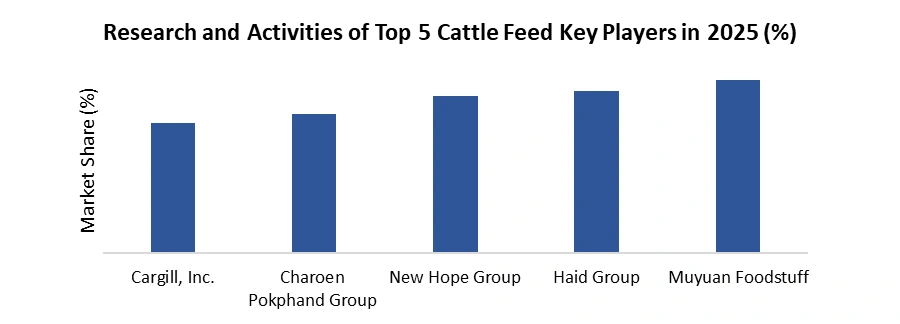

Cattle Feed Key Players

1. Cargill, Inc.

2. Charoen Pokphand Group

3. New Hope Group

4. Haid Group

5. Muyuan Foodstuff

6. Wen’s Food Group

7. Shuangbaotai

8. De Heus

9. Archer Daniels Midland Company (ADM)

10. Nutreco (Trouw Nutrition)

11. Alltech

12. ForFarmers

13. Godrej Agrovet

14. Purina Animal Nutrition

15. Biomin

16. DBN Group

17. Harbro Ltd

18. Zambeef Products

19. Ceylon Grain Elevators PLC

20. Wayne Sanderson Farms

21. Smithfield Foods

22. Koch Foods Inc.

23. Mountaire Farms

24. Tyson Foods

25. CP Foods (Charoen Pokphand Foods)

26. Nutriad

27. Trouw Nutrition

28. Elanco

29. Phibro Animal Health

30. Others

FAQ:

1. What are the growth drivers for the Cattle Feed Market?

Ans. Key growth drivers include rising demand for milk and meat products, growth in commercial dairy and beef farming, increasing awareness of animal nutrition, and higher adoption of formulated and fortified feeds.

2. What are the major restraints for the Cattle Feed Market growth?

Ans. Volatility in raw material prices (cereals, oilseed cakes), dependence on climatic conditions, supply chain disruptions, and high feed costs for small and marginal farmers are major restraints limiting market growth.

3. Which region is expected to lead the global Cattle Feed Market during the forecast period?

Ans. Asia Pacific is the leading region, driven by a large cattle population, rising dairy consumption, expanding livestock farming, and strong demand from countries such as China and India.

4. What is the expected market size and growth rate of the Cattle Feed Market?

Ans. The global Cattle Feed Market was valued at around USD 84.23 billion in 2025 and is expected to grow at a 4.45% CAGR, reaching USD 114.24 billion by 2032.

5. What segments are covered in the Cattle Feed Market report?

Ans. The report covers segmentation by Product Type, Animal Type, Form, Ingredient, Distribution Channel, and Region.