Global Cardiac Rhythm Management Devices Market Size, Share & Forecast (2026–2032)

Overview

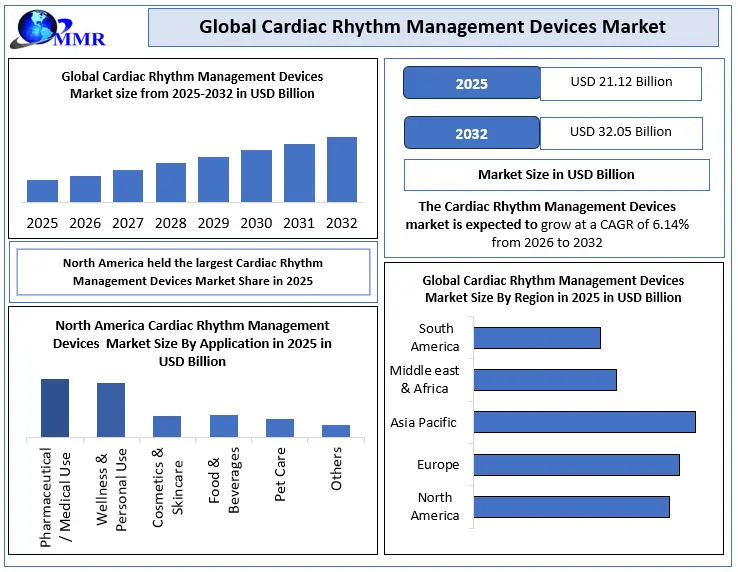

Global Cardiac Rhythm Management Devices Market was Valued at USD 21.12 Billion in 2025, Projected to Reach USD 32.05 Billion by 2032 at a CAGR of 6.14%

Every 40 seconds, someone in the United States suffers a cardiac arrest. Globally, 38 million people live with atrial fibrillation — a condition that silently multiplies stroke risk and can be managed, but not cured, without the right device at the right moment. The global cardiac rhythm management (CRM) devices market is built on this clinical reality. Valued at USD 21.12 billion in 2025 and projected to reach USD 32.05 billion by 2032 at a CAGR of 6.14%, this market is being reshaped by a generation of leadless pacemakers, AI-enabled remote monitoring platforms, and miniaturised implantable defibrillators that are redefining what it means to manage a failing heart — from the inside out. A pacemaker the size of a large vitamin capsule, implanted without surgery through a catheter, pacing a human heart for 15+ years without a single lead wire. That is not science fiction — that is Medtronic's Micra, implanted in over 300,000 patients globally. The CRM market is not just growing. It is being fundamentally reinvented.

Cardiac Rhythm Management Devices Market Overview

Key Highlights

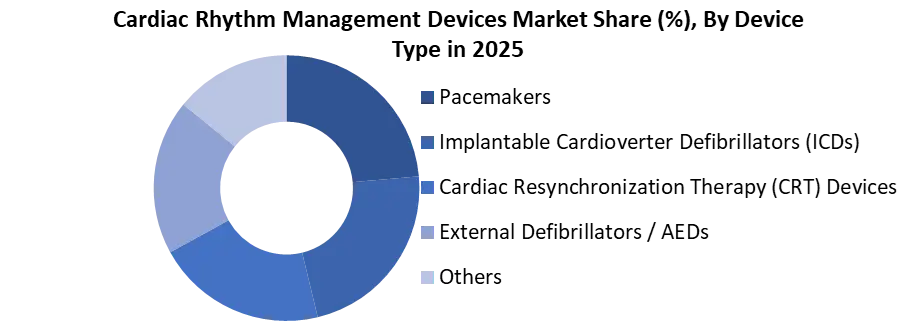

• The global CRM devices market was valued at USD 21.12 billion in 2025; pacemakers held the largest device-type share, with approximately 1.25 million implants performed annually worldwide.

• Leadless pacemaker adoption is accelerating — dual-chamber systems including Micra AV2 and AVEIR DR are achieving successful implantation rates of nearly 98%, with North America accounting for ~50% of global leadless pacemaker volume in 2025.

• Globally, 38 million people live with atrial fibrillation; ventricular arrhythmias account for 75–80% of sudden cardiac death cases — the primary clinical demand engine for ICDs and CRT devices.

• Remote monitoring integration is reshaping payer economics — continuous cardiac monitoring platforms are demonstrating measurable reductions in hospitalisation rates and are increasingly covered under major reimbursement frameworks.

• North America dominated the CRM market in 2025 with the largest regional share, supported by over 356,000 annual out-of-hospital cardiac arrests in the U.S. alone and high clinical adoption of advanced implant technologies.

• AI integration into CRM platforms — enabling predictive arrhythmia detection, automated alert generation, and personalised therapy pathways — is emerging as the next primary differentiator among leading device manufacturers.

Why 2025–2032 Is the Defining Era for Cardiac Rhythm Management

For five decades, Cardiac Rhythm Management (CRM) meant one thing: a pacemaker with leads, a generator in the chest wall, and a patient living with the permanent awareness of a device inside them. That paradigm is being dismantled — simultaneously from multiple directions.

Leadless systems have eliminated the lead. Subcutaneous ICDs have moved the electrode outside the heart entirely. AI platforms now detect arrhythmia patterns weeks before a clinical event. Remote monitoring has shifted cardiac follow-up from the clinic to the cloud. And miniaturisation has made devices smaller, longer-lasting, and less invasive than any previous generation.

The USD 21.12 billion market of 2025 is not the same market as 2020. And the USD 32.05 billion market of 2032 will not be recognisable by 2020 standards. For manufacturers, distributors, clinicians, and investors, the strategic imperative is to understand not just where this market is going — but why the pace of change is accelerating faster than the headline CAGR suggests.

Key Market Drivers

Adoption of Leadless Pacemakers: Leadless pacemakers are gaining widespread acceptance due to their improved procedural success and adoption by electrophysiologists. LCPs, eliminate the need for leads and can be implanted directly into the heart via minimally invasive techniques. Dual-chamber leadless technologies, which achieve 97% atrial-ventricular synchrony, are leading the charge in this category, providing significant benefits in terms of patient comfort and reduced complications.

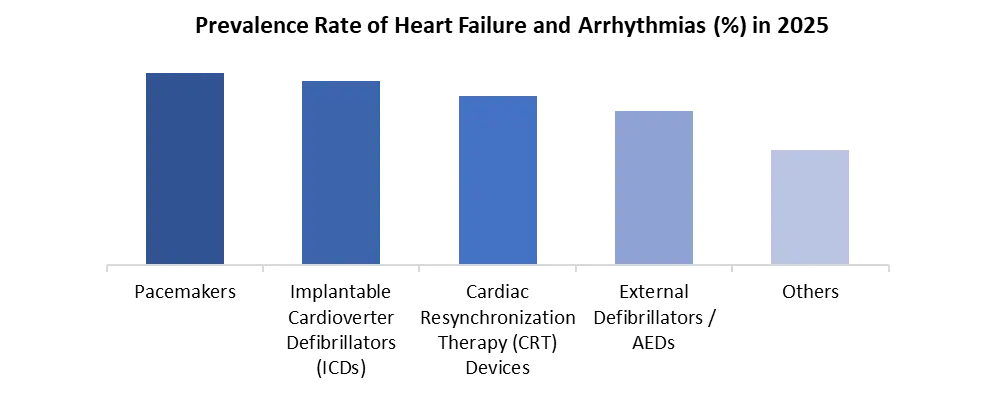

Prevalence of Heart Failure and Arrhythmias: In 2025, 7.4 million adults were living with heart failure, while globally, 38 million people suffer from atrial fibrillation. Arrythmias are a leading cause of stroke and increase the risk of a cardiac event. In 2025, Arrhythmias affect 2% of the US population, and ventricular arrhythmias cause 75%-80% of cases of sudden cardiac death. These rising figures are driving demand for pacemakers, implantable cardioverter-defibrillators (ICDs), and cardiac resynchronisation therapy (CRT) devices.

Cardiac Rhythm Management Devices Market: Rising Burden of Cardiac Arrests and Arrhythmias: In the United States alone, over 356,000 out-of-hospital cardiac arrests occur annually, with ventricular arrhythmias responsible for 75–80% of sudden cardiac death cases. Globally, out-of-hospital cardiac arrests reached approximately 385,000 in 2024, rising to an estimated 393,000 in 2025 — figures that directly underpin demand for ICDs, pacemakers, and CRT devices across both established and emerging healthcare markets.

Integration of Wearable Technology and Remote Monitoring: Advanced remote monitoring & wearable platforms are increasingly integrated into cardiac care, enabling continuous data capture that supports predictive analytics and early intervention – factors associated with reductions in hospitalization and better patient outcomes.

Continuous remote monitoring has been shown to improve patient the detection of impending clinical deterioration and aids personalized treatment strategies, which strengthens payer support for remote platforms and help create predictable recurring revenue streams.

To know about the Research Methodology :- Request Free Sample Report

Cardiac Rhythm Management Devices Market Trend: The Rise of Leadless and Miniaturized Pacemakers

In 2025, clinical registries indicate that leadless pacing systems account for a growing percentage of pacemaker implants. Dual-chamber leadless pacemakers, such as the Micra AV2 and AVEIR DR, are achieving successful implantation rates of nearly 98%. These devices are reshaping clinical practices, improving patient comfort, and reducing complications typically associated with traditional leaded pacemakers. This migration from transvenous systems to intracardiac, leadless devices is supported by expanding training programs for electrophysiologists and wider insurance coverage for advanced implant techniques.

Increasing Prevalence of Heart Failure and Arrhythmias to Drive Cardiac Rhythm Management Devices Market

The rising prevalence of heart failure and arrhythmias, particularly in aging populations, is a key factor driving the Cardiac Rhythm Management Devices Market growth. By 2024, over 385,000 out-of-hospital cardiac arrests were occur globally to 393,000 in 2025. These figures highlight the urgent need for life-saving interventions, such as ICDs and pacemakers, to address these rising health challenges. The global burden of atrial fibrillation, affecting 38 million people, fuels the demand for advanced cardiac devices.

Clinical and Procedural Challenges

The advancements in CRM technologies offer significant benefits, but their clinical and procedural complexity pose challenges for the Cardiac Rhythm Management Devices Market. Devices such as MRI-compatible systems and leadless dual-chamber implants require specialised training for optimal utilisation. Hospitals are reporting longer procedure times and higher resource consumption compared to simpler single-chamber implants. Additionally, older populations with comorbidities or vascular access limitations may face restrictions in using newer CRM technologies.

Cardiac Rhythm Management Devices Market Segment Analysis

By Device Type, The Cardiac Rhythm Management Devices Market is segmented into pacemakers, implantable cardioverter defibrillators (ICDs), cardiac resynchronization therapy (CRT) devices, external defibrillators, and other devices. Pacemakers held the largest market share in 2025, due to their high procedural volumes and widespread clinical adoption. Approximately 1.25 million pacemaker implants are performed each year globally, with around 200,000 of these procedures occurring in the United States alone. As of 2025, approximately 3 million Americans are living with pacemakers, the majority of whom are aged 65 or older.

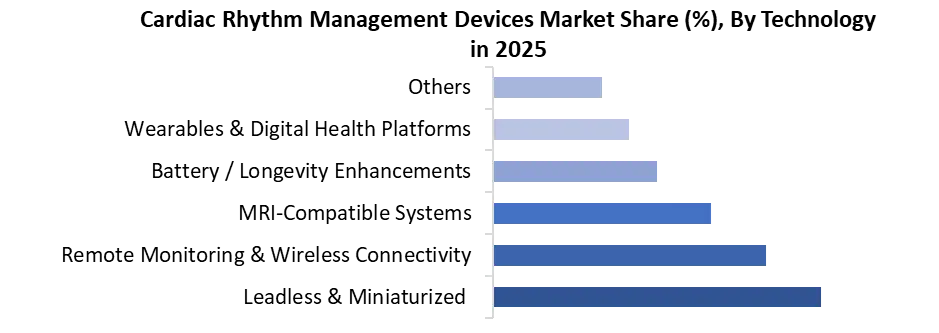

By Technology, The Cardiac Rhythm Management Devices Market is categorised by technology into leadless & miniaturized systems, remote monitoring & wireless connectivity, MRI-compatible systems, and wearables & digital health platforms. Leadless and miniaturised systems held the largest share in 2025, driven by advances in procedural adoption and technological evolution. These devices, such as the Micra AV2 and AVEIR DR, are completely intracardiac and reduce complications associated with traditional lead-based pacemakers, such as infection and lead dislodgement.

By Application: Bradycardia management held the largest application share in the CRM devices market in 2025, driven by the high global prevalence of slow or irregular heartbeats requiring pacemaker intervention. Approximately 3 million Americans live with implanted pacemakers — the majority aged 65 or older — reflecting the aging population's disproportionate burden of bradyarrhythmias. Tachycardia management, addressed primarily through ICDs and anti-tachycardia pacing, represented the second-largest application segment, underpinned by the 75–80% share of ventricular arrhythmias in sudden cardiac death cases. Heart failure, addressed through CRT-P and CRT-D devices, is the fastest-growing application, supported by the 7.4 million U.S. adults living with heart failure in 2025 and expanding clinical evidence for CRT-driven reverse remodelling in eligible patient populations.

By End User: Hospitals and cardiac surgical units dominated the CRM devices end-user segment in 2025, accounting for the largest share of device implantations due to their infrastructure for electrophysiology labs, cardiac catheterisation facilities, and post-implant monitoring programs. Cardiac care and electrophysiology labs represented a high-growth sub-segment, driven by increasing procedural specialisation and the migration of complex leadless and subcutaneous ICD implants to dedicated EP centres. Ambulatory Surgical Centers (ASCs) are the fastest-growing end-user category, supported by the shift toward outpatient cardiac procedures, cost containment pressures from payers, and regulatory approvals enabling select CRM implant procedures outside inpatient settings — a trend expected to accelerate through the 2026–2032 forecast period.

Cardiac Rhythm Management Devices Market Regional Analysis

Cardiac Rhythm Management Devices Market - North America

NA dominated the Cardiac Rhythm Management Devices Market in 2025 with the largest Market share. The prevalence of heart failure, arrhythmias, and out-of-hospital cardiac arrests is driving the demand for ICDs and pacemakers. The rapid adoption of leadless pacemakers in the region is expected to boost market growth. As of 2025, North America represented approximately 50% of the global leadless pacemaker market, reflecting high clinical uptake and adoption.

Cardiac Rhythm Management Devices Market - Europe:

Europe represented the second-largest CRM devices market in 2025, with Germany, France, the UK, and Italy accounting for the majority of regional revenue. Strong public healthcare reimbursement frameworks, aging demographics, and early adoption of MRI-compatible and remote monitoring-enabled CRM systems support sustained regional demand. The EU MDR (Medical Device Regulation) continues to reshape the competitive landscape, extending device approval timelines and raising post-market surveillance requirements — consolidating market share toward established players with the regulatory infrastructure to comply.

Cardiac Rhythm Management Devices Market - Asia Pacific:

Asia Pacific is the fastest-growing regional market for CRM devices, driven by rising cardiovascular disease burden across China, India, Japan, and South Korea — combined with expanding healthcare infrastructure, increasing device reimbursement coverage, and growing electrophysiology procedural volumes. China represents the largest APAC opportunity, supported by domestic manufacturers including MicroPort and Lepu Medical gaining share alongside global incumbents. Japan and South Korea lead in technology adoption, while India and Southeast Asia represent high-growth frontier markets with significant under-penetration in ICD and CRT device categories.

Cardiac Rhythm Management Devices Market - Middle East & Africa:

The MEA CRM devices market remains at an early adoption stage but is growing steadily, supported by GCC nations' healthcare modernisation investment, expanding cardiac care infrastructure in Saudi Arabia and UAE, and growing awareness of arrhythmia management. Access limitations, reimbursement gaps, and the concentration of advanced cardiac care in urban centres constrain broader penetration across the African continent, representing a long-term opportunity as healthcare infrastructure develops.

Cardiac Rhythm Management Devices Market - South America:

Brazil dominates the South American CRM devices market, supported by its large patient population, expanding SUS (unified health system) coverage for cardiac devices, and a growing private healthcare sector. Argentina and Colombia represent secondary growth markets. Price sensitivity, reimbursement variability, and regulatory timelines for device approval remain the primary constraints on market penetration across the region.

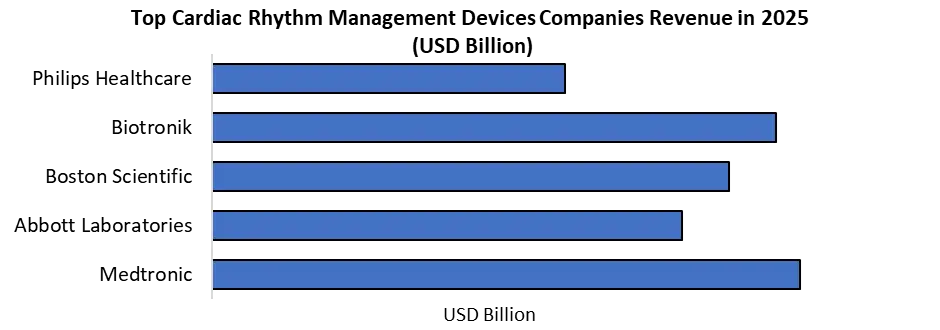

Cardiac Rhythm Management Devices Market Competitive Landscape

The Global CRM devices market is moderately consolidated, with Medtronic, Abbott Laboratories, and Boston Scientific collectively holding the majority of global revenue share across pacemakers, ICDs, and CRT devices. Medtronic maintains category leadership through its Micra leadless pacemaker franchise and Cobalt/Crome ICD platform, while Abbott has rapidly gained share through the AVEIR leadless pacemaker system — recording 10% CRM sales growth in Q2 2025 — and its comprehensive remote monitoring ecosystem. Boston Scientific competes aggressively in the ICD and CRT segment, with recent CE mark expansion for its INGEVITY pacing leads supporting conduction system pacing applications.

Biotronik and Philips maintain meaningful positions in select regional markets, particularly in Europe, while MicroPort and Lepu Medical are increasingly competitive in Asia Pacific, leveraging cost advantages and expanding domestic regulatory approvals. Competitive differentiation is shifting from device reliability — now largely commoditised among Tier 1 players — toward AI-powered remote monitoring platforms, procedural ease for electrophysiologists, battery longevity, and the breadth of reimbursement coverage for next-generation leadless and subcutaneous ICD systems.

The Cardiac Rhythm Management Devices Market Will Not Reward All Players Equally

Winners — Platform Ecosystem Builders: Medtronic, Abbott, and Boston Scientific are not competing on devices alone — they are competing on ecosystems. Remote monitoring platforms, AI-driven alert systems, physician workflow tools, and reimbursement navigation support are increasingly the decision factors in hospital procurement. The manufacturer whose remote monitoring platform is already embedded in an EP lab's workflow has a switching-cost advantage that no incremental product improvement from a competitor can easily overcome.

Challengers — Asian Manufacturers Scaling Rapidly: MicroPort and Lepu Medical are no longer fringe players in their home markets. With CE marks, NMPA approvals, and expanding clinical evidence bases, they are moving into European and Southeast Asian markets with cost structures that Medtronic and Abbott cannot match at the mid-tier. The question is not whether they will take share — it is how fast, and in which segments first.

At Risk — Single-Product Specialists Without Platform Strategy: Smaller CRM device manufacturers competing on a single device category without remote monitoring integration, AI analytics, or a reimbursement support infrastructure face an increasingly hostile competitive environment. Hospitals are consolidating device vendor relationships — and the vendor without an ecosystem play risks being rationalised out of procurement conversations regardless of device quality.

Recent Developments in Cardiac Rhythm Management Devices Market

• In October 2025, Abbott's CRM business reported a 10% sales growth in Q2, driven by the adoption of its AVEIR leadless pacemaker systems. Abbott’s AVEIR DR LP, FDA-approved in 2023, eliminates cardiac leads and offers synchronised pacing.

• September 2025: Boston Scientific Corporation obtained CE mark approval to broaden the indication for its current-generation INGEVITY Pacing Leads—thin wires implanted in the heart and connected to a pacemaker. The updated indication supports conduction system pacing (CSP) and sensing in the left bundle branch area (LBBA) of the heart when connected to a single- or dual-chamber pacemaker.

Cardiac Rhythm Management Devices Market Scope: Inquire before buying

| Cardiac Rhythm Management Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 21.12 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.14% | Market Size in 2032: | USD 6.14 Bn. |

| Segments Covered: | by Device Type | Pacemakers Single-chamber pacemakers Dual chamber pacemakers Leadless pacemakers Others Implantable Cardioverter Defibrillators (ICDs) Transvenous ICDs Subcutaneous ICDs (S ICDs) Others Cardiac Resynchronization Therapy (CRT) Devices CRT Pacemakers (CRT P) CRT Defibrillators (CRT D) External Defibrillators / AEDs Automated External Defibrillators Patient worn external defibrillators Others |

|

| by Technology | Leadless & Miniaturized Remote Monitoring & Wireless Connectivity MRI-Compatible Systems Battery / Longevity Enhancements Wearables & Digital Health Platforms Others |

||

| by Application | Bradycardia management Tachycardia Heart Failure Others |

||

| by End User | Hospitals & Cardiac Surgical Units Cardiac Care / Electrophysiology Labs Ambulatory Surgical Centers (ASCs) Others |

||

Cardiac Rhythm Management Devices Market Key Players

1. Medtronic

2. Abbott Laboratories

3. Boston Scientific

4. Biotronik

5. Koninklijke Philips N.V

6. MicroPort Scientific Corporation

7. Medico

8. Zoll Medical Corporation

9. EBR Systems, Inc.

10. Osypka AG

11. Stryker Corporation (Physio-Control)

12. Nihon Kohden Corporation

13. Schiller AG

14. Lepu Medical Technology (Beijing) Co., Ltd.

MMR Research Manager - Rucha Deshpande’s View on Cardiac Rhythm Management Devices Market — What Every Cardiac Device Executive Must Understand

The cardiac rhythm management market's 6.14% CAGR is deceptively modest for a market undergoing structural transformation. The aggregate number reflects the maturity of the pacemaker base segment — but within it, leadless systems, subcutaneous ICDs, and AI-integrated CRT platforms are growing at rates two to three times the market average.

The manufacturers who shift revenue mix toward these high-growth sub-segments while maintaining their pacemaker installed base are compounding structural advantage. The risk in this market is not demand — cardiovascular disease burden is only increasing with global aging — it is clinical adoption pace, reimbursement policy evolution, and the ability to scale EP training fast enough to meet implant demand. For investors, the most defensible long-term positions are in companies with integrated device-plus-platform business models and established reimbursement relationships with major payers. The device alone, in 2025, is no longer sufficient. The ecosystem around it is where the value lives.

Frequently Asked Questions

1. What are the growth drivers for the Cardiac Rhythm Management Devices Market?

Answer: The market is driven by the rising prevalence of heart failure and arrhythmias, increasing adoption of leadless pacemakers, advancements in remote monitoring technologies, and demand for minimally invasive devices.

2. What are the major restraints for the growth of the Cardiac Rhythm Management Devices Market?

Answer: Key restraints include high device costs, clinical complexity requiring specialized training, limited adoption in smaller healthcare practices, and challenges in patient eligibility due to vascular access and comorbidities.

3. Which region is expected to lead the global Cardiac Rhythm Management Devices Market during the forecast period?

Answer: North America is expected to lead due to high adoption of advanced CRM technologies, strong healthcare infrastructure, and the significant prevalence of heart failure and arrhythmias in the region.

4. What is the projected market size and growth rate of the Cardiac Rhythm Management Devices Market?

Answer: The CRM market, valued at USD 21.12 billion in 2025, is projected to grow at a CAGR of 6.14%, reaching USD 32.05 billion by 2032 due to rising demand for pacemakers and ICDs.

5. What segments are covered in the Cardiac Rhythm Management Devices Market report?

Answer: The market report covers segmentation by device type (pacemakers, ICDs), technology (leadless pacemakers, remote monitoring), application (arrhythmia management, heart failure), end users (hospitals, cardiac centers), and regions.