Building Insulation Materials Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

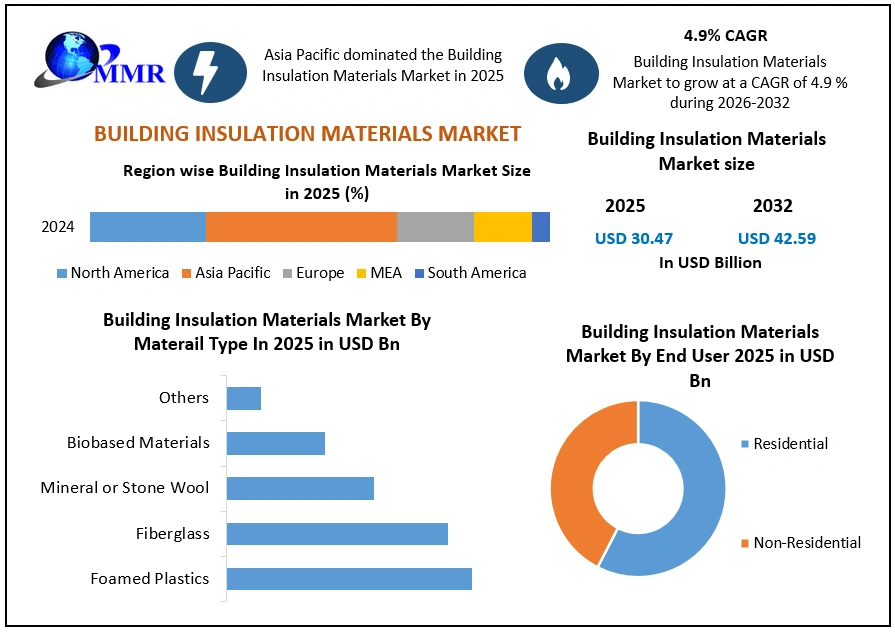

Building Insulation Materials Market size was valued at USD 30.47 Billion in 2025 and the total revenue is expected to grow at CAGR 4.9 % through 2026 to 2032, reaching nearly USD 42.59 Billion.

The MMR Building Insulation Materials Market report provides detailed analysis covering all critical aspects of the industry. The report examines insulation materials in comparison with alternative energy efficiency solutions, including HVAC upgrades, reflective coatings, and glazing systems, with detailed cost-effectiveness and payback assessments across new construction and renovation projects. It delivers in-depth regional pricing and cost benchmarking, evaluating historical trends, raw material and labor cost impacts, channel-wise price variations, and demand sensitivity. The report further analyzes global and regional demand–supply dynamics, manufacturing capacity utilization, and supply bottlenecks. It assesses installation practices, skill availability, and quality assurance implications on performance outcomes. the report covers investment attractiveness, ROI benchmarks, M&A activity, technology and innovation trends, go-to-market effectiveness, trade flows, supply chain resilience, sustainability and ESG impacts, and region-specific regulatory frameworks, offering a holistic, decision-ready market outlook.

Building Insulation Materials Market Overview:

Building insulation materials play a crucial role in constructing buildings by either forming the thermal envelope or reducing heat transfer. These materials have multiple functions, including thermal insulation, acoustic insulation, fire protection, and impact insulation, and their selection depends on their ability to perform these functions simultaneously.

The building insulation materials market has witnessed substantial growth recently due to its integral role in improving energy efficiency and reducing greenhouse gas emissions. Factors such as stringent energy efficiency regulations increased environmental sustainability awareness, and the need to minimize heating and cooling expenses boost market growth. Building Insulation Materials include fibreglass, mineral wool, cellulose, and foam, while innovative options like aerogel and reflective insulation are gaining popularity.

Building insulation materials industry players like Owens Corning, Saint-Gobain, and Rockwool International actively contribute to the advancement of building insulation materials through research and development efforts. The market is expected to continue expanding due to growing construction activities, particularly in emerging economies, and the escalating focus on energy-efficient buildings. The ongoing commitment to developing advanced insulation materials aims to enhance thermal performance and sustainability within the industry.

Scope and Research Methodology

The Building Insulation Materials Market report represents innovation, policy support, increased competition, and environmental concerns by global and local players holding the Building Insulation Materials Market in different countries. The report covered Market structure by comparative analysis of key players, and market followers, which makes this report insightful to the Building Insulation Materials Outlook.

The Building Insulation Materials Market report aims to outlook the market size based on segments, regional distribution and industry competition. The bottom-up approach has been used to estimate and forecast market size and market growth. The report provides a detailed examination of the key players in the Building Insulation Materials industry, including revenue. The report covers the global, regional and local level analysis of the Building Insulation Materials Market with the factors restraining, driving and challenging the market growth during the forecast period.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Building Insulation Materials Market Dynamics:

Building Insulation Materials Market Drivers

Growing Construction Industry fueling the demand for building insulation materials

The expansion of settlements, from small villages to towns and cities, including mega-cities with populations exceeding ten million, is by natural population growth and rural-to-urban migration. This urbanization process necessitates sufficient housing to accommodate the increasing urban population. Consequently, government initiatives such as the Indian government's 'Housing for All by 2022' mission play a significant role in driving the building insulation materials market. These initiatives aim to provide affordable housing and enforce mandatory reforms to facilitate the availability of urban land for housing purposes. Central assistance, provided for affordable housing through programs like the Affordable Housing in Partnership and Beneficiary-led individual house construction or enhancement, contributes to the demand for insulation materials.

The development of green buildings is another market driver. Green buildings focus on using environmentally friendly and resource-efficient practices throughout the building's lifecycle, from design and construction to operation and deconstruction. The emphasis on environmental sustainability and the reduction of carbon emissions drives the adoption of energy-efficient materials like building insulation. The robust growth of the construction industry, particularly in emerging economies, also fuels the demand for building insulation materials. The increasing awareness of the importance of energy efficiency and the environmental impact of buildings further supports the market growth in this sector.

Building Insulation Materials Market Restraint

High Initial Costs Hindering Adoption Building Insulation Materials

The high initial investment required for installing building insulation materials poses a significant barrier to adoption, particularly in price-sensitive markets, deterring budget-conscious consumers and construction companies from investing in insulation solutions. Additionally, limited awareness among end-users, especially in developing regions, about the benefits and types of building insulation materials further hampers market expansion. Lack of knowledge results in potential customers not understanding the value proposition of insulation solutions, such as energy savings. For instance, in rural areas of certain countries, residents may not be aware of the energy-saving benefits or the various types of insulation available, leading to low demand in those regions.

The unstable prices of raw materials used in insulation manufacturing, such as petroleum-based products and fibreglass, can impact the profitability of market players. Despite efforts by governments to mitigate these barriers through measures like energy efficiency standards and financial incentives, the high initial costs associated with building insulation materials remain a significant restraint. Retrofitting existing buildings with insulation materials also presents challenges due to logistical complexities and high costs, limiting their widespread adoption and impeding the overall growth of the industry.

Building Insulation Materials market opportunities:

Government Initiatives and Incentives offers growth opportunity to the market

Governments worldwide are implementing energy efficiency programs and providing financial incentives to drive the adoption of building insulation materials, creating opportunities for market growth by reducing barriers and increasing demand. For example, governments may offer tax credits or subsidies to homeowners undertaking insulation upgrades, making such projects financially attractive and leading to a surge in market demand for insulation materials. These initiatives, recognized by governments globally, emphasize the importance of energy efficiency and sustainable construction practices, resulting in the implementation of various measures to promote the adoption of building insulation materials.

Measures such as the Energy Performance of Buildings Directive (EPBD) in Europe, which sets mandatory energy efficiency standards and offers financial incentives like grants and subsidies, encourage building owners to improve insulation and overall energy performance. These examples demonstrate how government initiatives and incentives reduce financial barriers, boost consumer demand, and promote sustainable construction practices, thereby presenting significant opportunities for the building insulation materials market. By leveraging these initiatives, market players can capitalize on the growing focus on energy efficiency, contributing to a greener and more sustainable built environment.

Building Insulation Materials Market Segment Analysis:

Based on Material Type, in 2025, foamed plastics dominated the Building Insulation Materials Market by material type, driven by superior thermal performance, lightweight properties, and widespread use in residential and commercial buildings. Fiberglass follows, supported by cost-effectiveness, ease of installation, and strong penetration in retrofit applications. Mineral or stone wool maintains steady demand due to fire resistance, acoustic insulation, and sustainability credentials, particularly in Europe. Bio-based materials witness faster growth from green building adoption and low-carbon construction trends, though from a smaller base. Others, including aerogels and reflective insulation, account for niche applications requiring high-performance or space-efficient solutions.

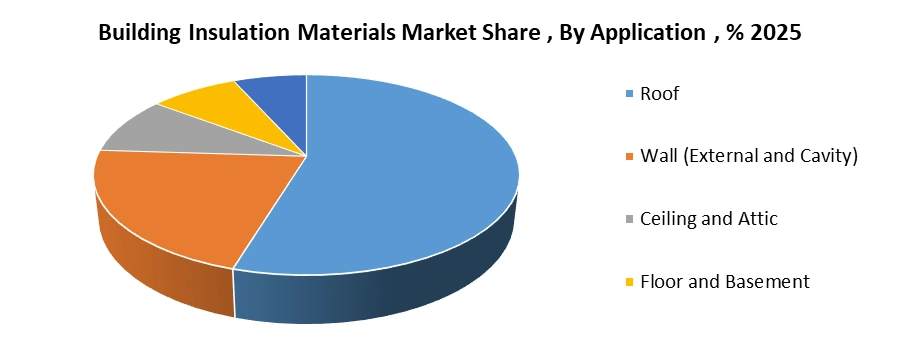

Based on Application, in 2025, roof insulation dominates the building insulation materials market, driven by high heat-loss prevention needs and energy-efficiency regulations in residential and commercial buildings. Wall insulation, including external and cavity applications, follows due to its critical role in thermal performance of building envelopes. Ceiling and attic insulation shows steady demand for retrofitting and energy upgrades. Floor and basement insulation adoption is moderate, mainly in cold climates and high-performance buildings. Acoustic partitions and HVAC duct insulation represent a smaller but growing segment, supported by rising focus on indoor comfort, noise control, and energy-efficient HVAC systems.

Regional Insights:

North America is a significant market for building insulation materials due to strict energy efficiency regulations, increasing awareness of sustainable construction practices, and a focus on carbon emissions reduction. Initiatives like ENERGY STAR and tax incentives in the United States incentivize the adoption of insulation materials, while the region's robust construction activity in the residential and commercial sectors further drives market demand. Europe, being a mature market, places a strong emphasis on energy efficiency and sustainability.

The Energy Performance of Buildings Directive (EPBD) implemented by the European Union sets energy performance standards, and countries like Germany, France, and Nordic nations have stringent building codes that promote insulation materials. Market growth is also supported by incentives such as grants and subsidies. Germany, with the largest construction industry in Europe, experiences expansion in residential and commercial sectors, while the United Kingdom witnesses growth in construction output and receives significant investments in infrastructure projects from the European Fund for Sustainable Development.

The Asia Pacific region demonstrates rapid growth in the building insulation materials market, fueled by urbanization, industrialization, and increasing construction activities. China, India, and Japan are key contributors to market demand as they prioritize energy efficiency and greenhouse gas emissions reduction. Factors like rising disposable incomes, a growing middle-class population, and heightened awareness of energy-efficient buildings drive market expansion. Policies such as India's Smart City project and Housing for All by 2024 further bolster the demand for insulation materials. Overall, the building insulation materials market exhibits promising growth globally, supported by regulatory measures, construction activities, and initiatives promoting energy efficiency and sustainability.

Competitive Landscape:

The global Building Insulation Materials Market is characterized by intense competition among renowned global brands, regional players, and emerging contenders, all striving to secure their market share. Leading companies such as Owens Corning, Knauf Insulation, and Rockwool International leverage their strong brand reputation, extensive product portfolios, and global distribution networks to maintain a competitive edge.

These industry giants prioritize research and development to continuously innovate their product offerings and meet evolving consumer demands, ensuring they stay at the forefront of the competition. Additionally, certain regional markets witness the dominance of local players, who have an in-depth understanding of the specific market dynamics and preferences. These key players collectively shape the landscape of the Building Insulation Materials Market, catering to the increasing need for energy-efficient and sustainable solutions in the construction industry. Each company brings its unique strengths and strategies into play, be it through groundbreaking product advancements, sustainability initiatives, or strategic market expansions. By focusing on these aspects, they uphold their competitive positions and capture market opportunities, solidifying their leading positions in the industry.

Building Insulation Materials Market Scope: Inquire before buying

| Building Insulation Materials Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 30.47 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.9 % | Market Size in 2032: | USD 42.59 Bn. |

| Segments Covered: | by Material Type | Foamed Plastics Expanded Polystyrene (EPS) Polyurethane and Polyisocyanurate Extruded Polystyrene (XPS) Others Fiberglass Batts and Blankets Loose Fill Roof Deck Board Pipe and Duct Wrap Others Mineral or Stone Wool Batts and Blankets Board loose Fill Others Biobased Materials Wood Denim Sheep Wool Hemp Straw Others Others |

|

| by Installation | New Construction Renovation |

||

| by Application | Roof Wall (External and Cavity) Floor and Basement Ceiling and Attic Acoustic Partition and HVAC Duct |

||

| by End-User | Residential Non-Residential Commercial Infrastructure Others |

||

Building Insulation Materials Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players

1.Saint-Gobain S.A.

2. ROCKWOOL International A/S

3. Kingspan Group plc

4. Owens Corning

5. Knauf Insulation

6. Johns Manville

7. BASF SE

8. Dow Inc.

9. Huntsman Corporation

10. GAF Materials Corporation

11. Covestro AG

12. Recticel Group

13. Armacell International S.A.

14. Aspen Aerogels Inc.

15. Synthos S.A.

16. Lloyd Insulations India Limited

17. Atlas Roofing Corporation

18. Holcim Group

19. Cabot Corporation

20. URSA Insulation

21. Paroc Group Oy

22. KCC Corporation

23. Kaneka Corporation

24. Evonik Industries AG

25. Fletcher Building Limited

26. L’Isolante K-Flex

27. Cellofoam North America Inc.

28. Xtratherm Limited

29. Superglass Holdings PLC

30. NICHIAS Corporation

31. Others

Frequently Asked Questions:

1] What segments are covered in the Building Insulation Materials Market report?

Ans. The segments covered in the Building Insulation Materials Market report are based on Material Type, Installation, Application, end-user, and region

2] Which region is expected to hold the highest share of the Building Insulation Materials Market?

Ans. Asia Pacific region is expected to hold the highest share of the Building Insulation Materials Market.

3] What is the market size of Building Insulation Materials Market by 2032?

Ans. The market size of Building Insulation Materials Market by 2032 is USD 42.59 Bn.

4] What is the growth rate of Building Insulation Materials Market?

Ans. The Global Building Insulation Materials Market is growing at a CAGR of 4.9% during forecasting period 2025-2032.

5] What was the market size of Building Insulation Materials Market in 2025?

Ans. The market size of Building Insulation Materials Market in 2025 was USD 30.47 Bn.