Blood Collection Device Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2029

Overview

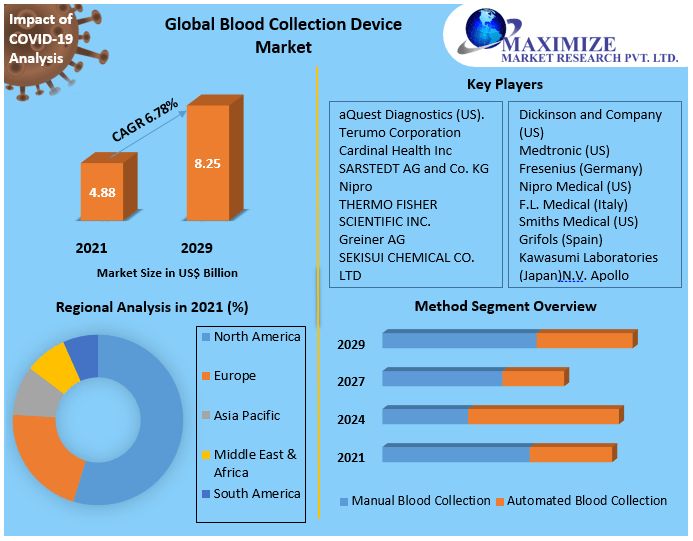

Blood Collection Device Market is expected to reach US$ 8.25 Bn. at a CAGR of 6.78% during the forecast period 2029.

To know about the Research Methodology :- Request Free Sample Report

The Blood Collection Device Market is being anticipated to take advantage of the growing awareness about blood donation through various government initiatives. This could eventually increase the demand for blood products and thus produce quality business opportunities in the Blood Collection Device Market. In addition to manual blood collection, other methods such as automatic blood collection should be widely available worldwide. Players seeking to enter the market could benefit from these advances in the industry.The report study has analyzed revenue impact of COVID -19 pandemic on the sales revenue of market leaders, market followers and market disrupters in the report and same is reflected in our analysis.

The growth in the blood collection device segment is due to the increasing prevalence of blood disorders, the increasing demand for biopharmaceutical plasma for plasma fractionation, for apheresis devices, whole blood sampling in emerging economies. Blood collection involves taking blood samples from the donor to perform diagnostic tests in the laboratory and treat patients.

The Blood Collection Device Market is segmented by product, method, end user, and region. The blood collection tubes are segmented by tube type as plasma separation tube, heparin tubes, serum separator tubes, EDTA tubes, rapid serum tubes, and others. Serum separation tubes have the largest market share followed by EDTA tubes. This is due to the factors such as collection of more serum samples and used for various diagnostic applications.

Geographically, North America has been the largest market for blood collection, due to heightened awareness, the established health care industry and the growing prevalence of infectious and non-infectious diseases in the region. The United States contributed the most to the revenue from the Blood Collection Device Market in North America and globally. The presence of a large number of diagnostic laboratories and hospitals and the increasing prevalence of people with blood disorders are the main growth factors for the US Blood Collection Device Market.

The key players in the Blood Collection Device Market include Becton, Dickinson and Company (US), Medtronic (US), Fresenius (Germany), Nipro Medical (US), F.L. Medical (Italy), Smiths Medical (US), Grifols (Spain), Kawasumi Laboratories (Japan), and Quest Diagnostics (US).

The objective of the report is to present comprehensive Global Blood Collection Device Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with analysis of complicated data in simple language. The report covers all the aspects of industry with dedicated study of key players that includes market leaders, followers and new entrants by region.

PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors by region on the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give clear futuristic view of the industry to the decision makers.

The report also helps in understanding Global Blood Collection Device Market North America for Asia Pacific dynamics, structure by analyzing the market segments, and project the Global Blood Collection Device Market North America for Asia Pacific size. Clear representation of competitive analysis of key players by type, price, financial position, product portfolio, growth strategies, and regional presence in the Global Blood Collection Device Market North America for Asia Pacific make the report investor’s guide.

The years that have been considered for the study are:

• Base year – 2021

• Estimated year – 2022

• Forecast period – 2021 to 2029

Target Audience:

• Healthcare service providers (hospitals and pathology laboratories)

• Blood collection product manufacturers

• Blood banks

• NGOs and government organizations associated with blood collection

• Market research and consulting firms

Blood Collection Device Market Scope: Inquire before buying

Blood Collection Device Market - Key Segments:

Blood Collection Device Market, By Product:

• Blood Collection Tubes:

o Serum Collection Tubes

o Plasma or Whole Blood Collection tubes

EDTA Tubes

Heparin Tubes

Coagulation Tubes

Glucose Tubes

ESR Tubes

• Needles and Syringes

• Blood Bags

• Blood Collection Devices

• Lancets

Blood Collection Device Market, By Method:

• Manual Blood Collection

• Automated Blood Collection

Blood Collection Device Market, By End User:

• Hospitals

• Clinical Laboratories

• Pharmaceutical and Biotechnology Companies & Contract Research Organizations (CROs)

• Blood Banks

• Research & Academic Laboratories

• Others

Blood Collection Device Market, by Region:

North America:

• U.S

• Canada

Europe:

• Germany

• France

• UK

• Italy

• Spain

• Russia

• Rest of Europe

Asia Pacific:

• Japan

• China

• India

• South Korea

• Australia

• Rest of Asia Pacific

Rest of the World (ROW):

• Middle-East

• Africa

• Latin America

Blood Collection Device Market Key layers:

• Becton,

• Dickinson and Company (US)

• Medtronic (US)

• Fresenius (Germany)

• Nipro Medical (US)

• F.L. Medical (Italy)

• Smiths Medical (US)

• Grifols (Spain)

• Kawasumi Laboratories (Japan)

• aQuest Diagnostics (US).

• Terumo Corporation

• Cardinal Health Inc

• SARSTEDT AG and Co. KG

• Nipro

• THERMO FISHER SCIENTIFIC INC.

• Greiner AG

• SEKISUI CHEMICAL CO. LTD

• Narang Medical Limited.

Frequently Asked Questions:

1. Which region has the largest share in Global Blood Collection Device Market?

Ans: North America region holds the highest share in 2021.

2. What is the growth rate of Global Blood Collection Device Market?

Ans: The Global Blood Collection Device Market is growing at a CAGR of 6.78% during forecasting period 2022-2029.

3. What is scope of the Global Blood Collection Device market report?

Ans: Global Blood Collection Device Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Blood Collection Device market?

Ans: The important key players in the Global Blood Collection Device Market are – Becton,, Dickinson and Company (US), Medtronic (US), Fresenius (Germany), Nipro Medical (US), F.L. Medical (Italy), Smiths Medical (US), Grifols (Spain), Kawasumi Laboratories (Japan), aQuest Diagnostics (US)., Terumo Corporation, Cardinal Health Inc, SARSTEDT AG and Co. KG, Nipro, THERMO FISHER SCIENTIFIC INC., Greiner AG, SEKISUI CHEMICAL CO. LTD, and Narang Medical Limited.

5. What is the study period of this market?

Ans: The Global Blood Collection Device Market is studied from 2021 to 2029.