Bio-Based Naphtha Market Size by Feedstock Type, Production Process, Application and End User

Overview

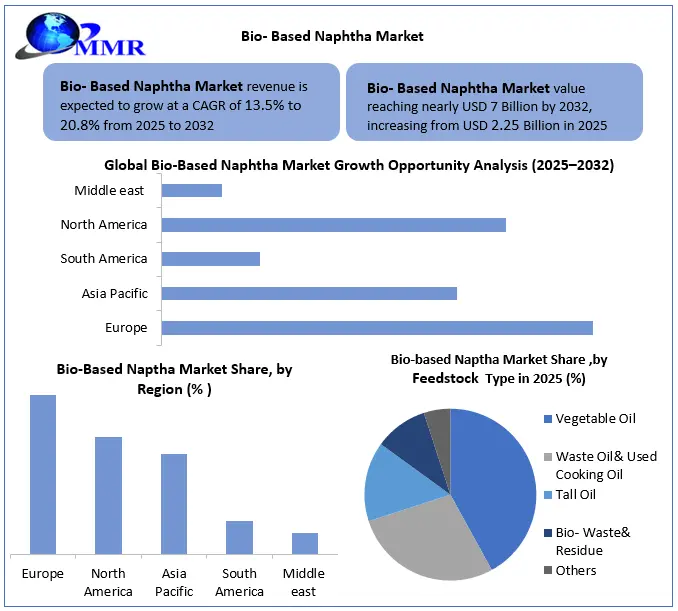

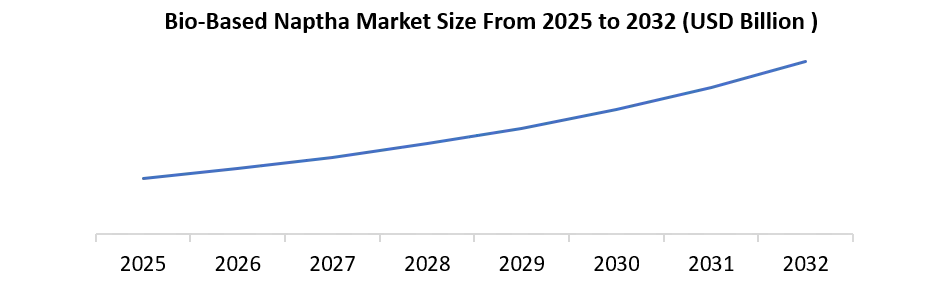

The Global Bio-Based Naphtha Market size was valued at USD 2.25 billion in 2025, and the total Bio-Based Naphtha Market revenue is expected to grow at a CAGR of 13.5% to 20.8% from 2025 to 2032, reaching nearly USD 7 billion by 2032.

The Bio-Based Naphtha Market is gaining strong global attention as industries accelerate their shift from fossil-based feedstocks toward renewable hydrocarbon solutions. Bio-based naphtha is increasingly positioned as a strategic drop-in replacement for conventional naphtha, particularly in petrochemical applications for producing ethylene, propylene, aromatics, and polymers, while supporting corporate net-zero and decarbonization commitments. Its compatibility with existing refinery and steam cracker infrastructure makes it a highly scalable pathway for reducing carbon intensity without major capital upgrades.

In 2025, demand is primarily driven by the growing requirement for sustainable plastics, renewable chemical intermediates, and regulatory mandates encouraging low-carbon production. Bio-based naphtha is also becoming a key enabler of circular economy strategies, especially where manufacturers combine bio-based feedstocks with recycled plastics to strengthen sustainability compliance and brand differentiation. Increasing long-term offtake agreements between biorefineries, chemical producers, and downstream polymer manufacturers are further supporting market expansion.

To know about the Research Methodology :- Request Free Sample Report

Bio-Based Naptha Market Dynamics:

Market Driver: Rising Regulatory Support and Corporate Sustainability Commitments

The Global Bio-Based Naphtha Market is being driven by increasing corporate net-zero commitments and supportive government policies promoting renewable feedstocks. Major chemical and plastics manufacturers are accelerating the adoption of bio-based naphtha to reduce carbon emissions and meet ESG goals. Regulatory initiatives such as the EU Renewable Energy Directive (RED III) and Sustainable Aviation Fuel (SAF) mandates are creating sustained demand for renewable feedstocks, while incentives under the U.S. Inflation Reduction Act (IRA) help offset production costs and encourage investments in biorefineries.

The rapid expansion of the bioplastics industry, particularly for Bio-PE and Bio-PP, is further boosting demand for renewable naphtha as a sustainable raw material. Additionally, bio-based naphtha's drop-in compatibility with existing petrochemical infrastructure minimizes capital investment requirements, facilitating faster adoption. The growing implementation of carbon pricing mechanisms and the Carbon Border Adjustment Mechanism (CBAM) is also improving the cost competitiveness of bio-based naphtha compared to conventional fossil-based alternatives, supporting long-term market growth.

Market Restraint: High Production Costs and Feedstock Supply Constraints

The Global Bio-Based Naphtha Market is restrained by higher production costs, which remain 20–40% above conventional fossil-based naphtha in the absence of government subsidies or policy incentives. Additionally, increasing competition for renewable feedstocks from the food, animal feed, and biofuel industries is tightening raw material availability and placing upward pressure on prices. Fluctuating feedstock costs create margin volatility for producers, making long-term pricing and investment decisions more challenging. The limited availability of ISCC- and RSB-certified sustainable feedstocks further restricts the production of certified bio-based naphtha required by global chemical manufacturers. Moreover, the cost of converting and upgrading existing refining infrastructure for bio-based feedstock processing remains more than 20% higher than conventional petrochemical refining, slowing large-scale commercial adoption.

Market Opportunity: Emerging Feedstocks and Expanding Bioeconomy Initiatives

The Global Bio-Based Naphtha Market presents significant growth opportunities through the adoption of non-food feedstocks such as algae and municipal solid waste (MSW), which can provide sustainable and scalable raw material supplies without competing with food production. The integration of advanced biorefineries capable of producing multiple renewable products—including sustainable aviation fuel (SAF), bio-based naphtha, and biodiesel—is improving production efficiency and overall project economics. Furthermore, the growing supply gap in the Asia-Pacific region offers substantial opportunities for new market entrants to establish local production capacity.

Government-backed bioeconomy initiatives in Brazil, India, and ASEAN countries are also encouraging investments in renewable chemicals and fuels, creating new regional production hubs. In addition, the availability of tall oil and forestry by-products in Nordic Europe provides a reliable source of low-ILUC certified feedstocks, while long-term offtake agreements with packaging, automotive, and consumer goods companies are reducing investment risks and supporting capacity expansion across the bio-based naphtha value chain.

Market Challenge: Feedstock Volatility and Regulatory Uncertainty

The Global Bio-Based Naphtha Market faces several challenges, including geopolitical disruptions affecting the supply of key feedstocks such as palm oil and soybean oil, leading to significant price volatility and supply chain uncertainties. Concerns surrounding Indirect Land Use Change (ILUC) continue to threaten the certification status of several bio-based feedstocks, creating compliance risks for producers. Additionally, fragmented regulatory frameworks across regions increase certification and compliance complexity for global manufacturers operating in multiple markets.

Growing consumer and policymaker concerns regarding the use of food-based feedstocks may also negatively impact market perception and accelerate the shift toward non-food alternatives. Furthermore, periods of low fossil naphtha prices reduce the cost competitiveness of bio-based naphtha, making widespread adoption more challenging without supportive government incentives or carbon pricing mechanisms.

Bio-Based Naptha Market Regional Insight:

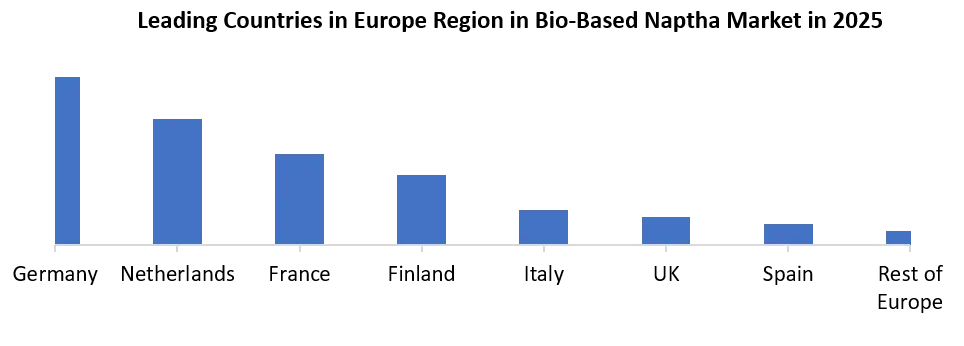

Europe dominates the Global Bio-Based Naphtha Market, supported by stringent renewable energy regulations, ambitious carbon reduction targets, and a well-established bioeconomy. The region benefits from advanced biorefining infrastructure and strong demand from the chemicals, plastics, and sustainable aviation fuel (SAF) sectors. Germany, the Netherlands, France, and Finland are the leading contributors, driven by investments in renewable feedstocks and circular economy initiatives.

North America holds a significant market share due to increasing investments in renewable fuels, favorable government incentives, and expanding bio-based chemical production. The region is witnessing growing adoption of bio-based naphtha across packaging, automotive, and consumer goods industries. The United States leads the regional market, followed by Canada and Mexico.

Asia-Pacific is expected to register the fastest growth during the forecast period, fueled by rapid industrialization, expanding petrochemical production, and increasing government support for sustainable manufacturing. Rising demand for renewable plastics and chemicals is further accelerating market growth. China, Japan, India, and South Korea are the key countries driving regional expansion.

South America is emerging as a promising market owing to abundant biomass resources and a strong biofuel industry. The region is benefiting from increasing investments in renewable feedstocks and biorefinery projects, particularly in Brazil, while Argentina and Chile are also contributing to market development.

The Middle East & Africa market is witnessing gradual growth, supported by diversification strategies in the petrochemical sector and increasing investments in renewable energy projects. Governments are promoting sustainable industrial development to reduce dependence on fossil fuels. Saudi Arabia, the United Arab Emirates (UAE), and South Africa are the leading markets in the region.

Bio-Based Naptha Market Competitive Landscape:

The Global Bio-Based Naphtha Market is moderately consolidated, with competition driven by integrated energy companies, renewable fuel producers, and advanced biorefinery operators. Leading market participants are focusing on expanding renewable refining capacity, securing sustainable feedstock supplies, and developing advanced conversion technologies to strengthen their competitive position. Strategic initiatives such as capacity expansions, long-term feedstock agreements, mergers and acquisitions, and collaborations with chemical and polymer manufacturers are enabling companies to meet the growing demand for low-carbon feedstocks used in biofuels, bioplastics, and renewable chemicals.

Competition is further intensifying as companies invest in next-generation feedstocks such as waste oils, municipal solid waste (MSW), algae, and forestry residues to reduce dependence on food-based raw materials and comply with sustainability standards. Market leaders are also pursuing certifications such as ISCC and RSB to enhance product credibility and meet regulatory requirements across Europe and North America. Additionally, increasing investments in integrated biorefineries capable of producing bio-based naphtha, sustainable aviation fuel (SAF), renewable diesel, and bio-based chemicals are improving operational efficiency and strengthening the long-term competitiveness of key players in the global market.

Bio-Based Naptha Market Scope: Inquire before buying

| Bio-Based Naptha Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 2.25 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 13.5% | Market Size in 2032: | USD 7 Bn. |

| Segments Covered: | by Feedstock Type | Vegetable Oil-Based Naphtha Waste Oil & Used Cooking Oil (UCO)-Based Naphtha Tall Oil-Based Naphtha Bio-Waste & Residue-Based Naphtha Others |

|

| by Production Process | Hydrotreated Vegetable Oil (HVO) Fischer-Tropsch Synthesis Pyrolysis Gasification Others |

||

| by Application | Petrochemicals Biofuels Bioplastics Sustainable Aviation Fuel (SAF) Chemicals & Polymers Others |

||

| by End-User | Chemical Manufacturers Petrochemical Companies Biofuel Producers Plastic & Packaging Manufacturers Aviation Fuel Producers |

||

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

The Global Bio-Based Naphtha Market Key Players:

| Company | Headquarters | Core Competencies |

| Neste Oyj | Finland | Renewable diesel, sustainable aviation fuel (SAF), bio-based naphtha, waste & residue feedstocks |

| UPM Biochemicals | Germany | Wood-based biofuels, bio-based chemicals, renewable naphtha from forestry residues |

| Preem AB | Sweden | Renewable fuels, co-processing of bio-feedstocks, sustainable refinery operations |

| TotalEnergies SE | France | Renewable fuels, bio-refining, sustainable feedstocks, circular chemicals |

| Shell plc | United Kingdom | Bio-refining, renewable feedstocks, integrated petrochemical operations |

| BP plc | United Kingdom | Bioenergy, renewable fuels, sustainable feedstock integration |

| Repsol S.A. | Spain | Renewable fuels, circular economy, advanced bio-refineries |

| Eni S.p.A. | Italy | HVO technology, bio-refining, waste-based renewable feedstocks |

| OMV AG | Austria | Sustainable refining, renewable fuels, chemical feedstocks |

| Chevron Renewable Energy Group | United States | Renewable diesel, bio-based feedstocks, advanced biofuel technologies |

| Marathon Petroleum Corporation | United States | Renewable fuels, refinery integration, sustainable feedstock processing |

| Phillips 66 | United States | Renewable fuel production, bio-feedstock co-processing |

| HF Sinclair Corporation | United States | Renewable diesel, bio-based refinery conversion technologies |

| Valero Energy Corporation (Diamond Green Diesel) | United States | Renewable diesel, waste oils, renewable feedstock integration |

| World Energy LLC | United States | Sustainable aviation fuel, renewable hydrocarbons, bio-based feedstocks |

| LanzaJet Inc. | United States | Alcohol-to-Jet (ATJ) technology, sustainable fuel production |

| SkyNRG B.V. | Netherlands | Sustainable aviation fuel, renewable feedstock supply chain |

| Borealis AG | Austria | Circular polymers, renewable feedstocks, sustainable petrochemicals |

| Braskem S.A. | Brazil | Bio-based polymers, renewable naphtha applications, green polyethylene |

| SABIC | Saudi Arabia | Certified renewable polymers, circular chemicals, bio-feedstock integration |

| BASF SE | Germany | Bio-based chemicals, sustainable feedstocks, mass balance approach |

| LyondellBasell Industries | Netherlands | Renewable polymers, circular feedstocks, petrochemical integration |

| Dow Inc. | United States | Bio-based plastics, renewable chemicals, sustainable packaging solutions |

| INEOS Group | United Kingdom | Petrochemicals, renewable feedstocks, circular economy solutions |

| Mitsubishi Chemical Group | Japan | Bio-based chemicals, sustainable polymers, renewable materials |

| Mitsui Chemicals, Inc. | Japan | Renewable chemicals, sustainable feedstock technologies |

| LG Chem Ltd. | South Korea | Bio-based plastics, renewable chemicals, sustainable material innovation |

| Indian Oil Corporation Ltd. (IOCL) | India | Bio-refining, renewable fuels, integrated energy solutions |

| Petrobras | Brazil | Biofuel integration, renewable refinery projects, sustainable hydrocarbons |

| Clariant AG | Switzerland | Biomass conversion technologies, advanced catalysts, sustainable chemical solutions |

Frequently Asked Questions:

1. What is the projected market size of the Global Bio-Based Naphtha Market by 2032?

The Global Bio-Based Naphtha Market is projected to grow from USD 2.25 billion in 2025 to approximately USD 6.95 billion by 2032.

2. What is the expected CAGR of the Global Bio-Based Naphtha Market during 2025–2032?

The market is expected to expand at a CAGR of 17.5% during the forecast period, driven by increasing demand for renewable feedstocks and sustainable chemicals.

3. Which region dominates the Global Bio-Based Naphtha Market?

Europe dominates the market due to stringent renewable energy regulations, advanced biorefining infrastructure, and growing adoption of bio-based feedstocks in the chemical and plastics industries.

4. What are the key factors driving the growth of the Global Bio-Based Naphtha Market?

The market is driven by rising corporate net-zero commitments, supportive government policies, increasing demand for bio-based plastics and sustainable aviation fuel (SAF), and growing investments in renewable feedstock technologies.

5. Who are the leading companies operating in the Global Bio-Based Naphtha Market?

Major players include Neste Oyj, TotalEnergies SE, Shell plc, BP plc, Repsol S.A., Eni S.p.A., UPM Biochemicals, Braskem S.A., BASF SE, and SABIC.