Thin Film Photovoltaics Market by End-User, Technology, Application, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

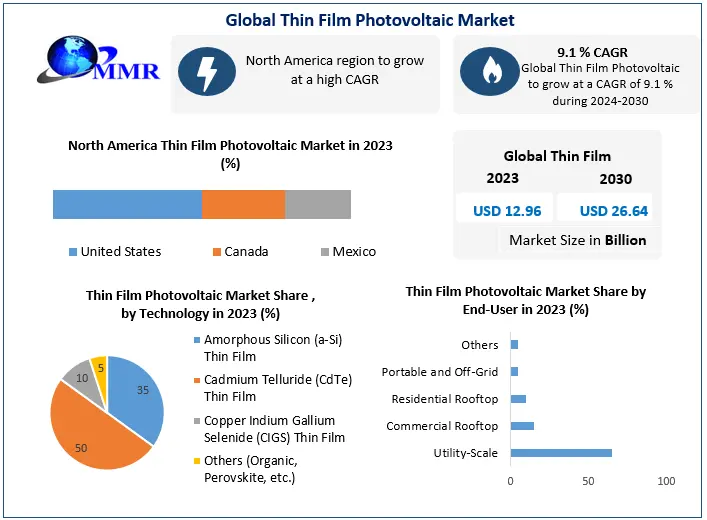

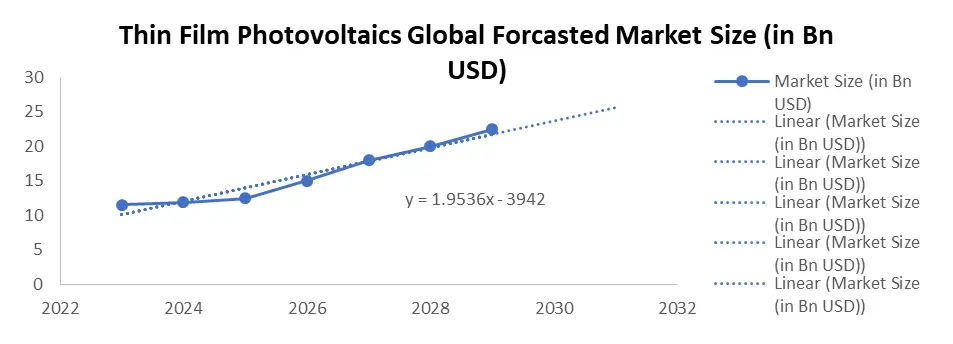

The Global Thin Film Photovoltaic Market size was valued at USD 12.96 Bn in 2023 and is expected to reach USD 26.64 Bn by 2030, at a CAGR of 9.1%.

Thin Film Photovoltaics Market Overview

Thin Film Photovoltaics is a type of solar cell technology that utilizes thin layers of semiconductors, typically a few micrometers thick, to convert sunlight into electricity. Unlike traditional crystalline silicon solar cells, Thin Film Photovoltaics can be fabricated on a variety of low-cost substrates such as glass, plastic or metal foils, making it a cost-effective option for large-scale solar power generation.

The global thin film photovoltaics market has witnessed significant growth in recent years, owing to increasing demand for clean and renewable energy sources, as well as the rising need for sustainable energy solutions across various industries. According to the report, the global Thin Film Photovoltaics market is expected to grow at a CAGR of 9.1% during the forecast period of 2024-2030, reaching a market size of USD 26.64 billion by 2030.

The major drivers for the growth of the Thin Film Photovoltaics market include the decreasing costs of solar PV systems, government initiatives and subsidies to promote renewable energy adoption, and increasing investments in research and development of thin film photovoltaic. Additionally, the increasing demand for off-grid electricity and portable solar devices such as mobile chargers, wearable devices, and remote sensors is expected to drive the growth of the Thin Film Photovoltaics market in the coming years.

The market growth is hampered by factors such as the high initial capital investment required for Thin Film Photovoltaics systems, low conversion efficiency compared to traditional crystalline silicon solar cells, and the lack of standardized testing methods and certification procedures.

Thin Film Photovoltaics Research Methodology

The research conducted utilized both primary and secondary data sources to ensure that all possible factors affecting the market were thoroughly examined and validated. The Thin Film Photovoltaics Market size for top-level markets and sub-segments is normalized and the impact of inflation, economic downturns, regulatory & policy changes, and other variables is factored into the market forecast.

The bottom-up approach and multiple data triangulation methodologies are used to estimate the market size and forecasts. The percentage splits, market shares, and breakdowns of the segments are derived based on weights assigned to each of the segments on their utilization rate and average sale price. The country-wise analysis of the overall market and its sub-segments are based on the percentage adoption or utilization of the given market Size in the respective region or country. Major players in the market are identified through secondary research based on indicators that include market revenue, price, services offered, advancements, mergers and acquisitions, and joint. Extensive primary research was conducted to acquire information and verify and confirm the crucial numbers arrived at after comprehensive market engineering and calculations for market statistics, market size estimations, market forecasts, Thin Film Photovoltaics Market breakdown, and data triangulation. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Thin Film Photovoltaics Market Dynamics

The Thin Film Photovoltaics market is forecasted to witness market growth significantly in the forecasted years, driven by increasing demand for clean energy solutions and the decreasing costs of solar PV systems. There is a great potential for the Thin Film Photovoltaics Industry thanks to the industry drivers. Such market drivers are been analysed in the report the overview of which is been discussed below.

Thin Film Photovoltaics Market Drivers:

The Thin Film Photovoltaics Market is poised for significant growth in the coming years, driven by various factors. The increasing need for sustainable energy solutions across industries is one of the major drivers, as companies seek to reduce their carbon footprint and meet their sustainability goals. Governments worldwide are also providing incentives and subsidies to promote renewable energy adoption, which is expected to fuel market growth and unlock the industry's growth potential.

The Thin Film Photovoltaics Market industry is also benefiting from investments in research and development of new materials and fabrication techniques. Technological advancements are leading to higher conversion efficiencies, which are making thin film photovoltaics more competitive with traditional crystalline silicon solar cells. This is creating opportunities for companies operating in the industry to innovate and develop next-generation materials and fabrication techniques, which can help them gain a competitive edge in the market. The growing demand for off-grid electricity and portable solar devices such as mobile chargers, wearable devices, and remote sensors is another key driver of market growth. Companies that can provide innovative solutions to meet this demand are expected to experience significant growth potential in the forecasted period.

While there are restraints to market growth, such as the high initial capital investment required and lower conversion efficiency compared to traditional solar cells, the drivers outlined above suggest that the Thin Film Photovoltaics Market has significant market potential. Companies that can invest in technology and innovation and capitalize on these opportunities are well-positioned to unlock the industry's growth potential and gain a competitive advantage in the market.

Thin Film Photovoltaics Market Restraints

Thin Film Photovoltaics systems require a high initial investment, which can be a significant barrier for some potential customers, especially in developing countries. This may limit the adoption of Thin Film Photovoltaics technology, particularly in areas with limited financial resources. The conversion efficiency of Thin Film Photovoltaics systems is generally lower compared to traditional crystalline silicon solar cells. This means that Thin Film Photovoltaics systems may require a larger surface area to produce the same amount of electricity as crystalline silicon solar cells, which could be a limiting factor in certain applications.

The lack of standardized testing methods and certification procedures for Thin Film Photovoltaics systems can create uncertainty and confusion for potential customers, which may limit their adoption of the technology.

The Thin Film Photovoltaics market faces competition from other renewable energy sources such as wind, hydro, and geothermal energy. This competition may limit the market growth of Thin Film Photovoltaics systems, especially in regions where these other sources of renewable energy are more prevalent. Thin Film Photovoltaics systems require rare earth elements and other materials that can have negative environmental impacts if not managed properly. This may limit the adoption of Thin Film Photovoltaics technology in regions with strict environmental regulations.

Thin Film Photovoltaics Market Trend

The Thin Film Photovoltaics (Thin Film Photovoltaics) market has been witnessing significant growth in recent years and is been forecasted for a great market potential thanks to the drivers which assists in the increasing demand for clean and sustainable energy sources.

Thin Film Photovoltaics market is the increasing adoption of renewable energy sources, especially solar energy, in residential, commercial, and industrial sectors. Thin Film Photovoltaics technology offers several advantages over traditional silicon-based photovoltaics, such as lower cost, higher efficiency, and flexibility in design and application.

The market is also being driven by government initiatives and policies aimed at promoting renewable energy sources and reducing carbon emissions. Several countries have set ambitious renewable energy targets and are providing subsidies and incentives to encourage the adoption of solar energy, which is expected to fuel the growth of the Thin Film Photovoltaics market.

Asia Pacific is currently the largest markets for Thin Film Photovoltaics, with the Asia Pacific region expected to witness the highest growth rate during the forecast period. This growth can be attributed to the increasing demand for solar energy in emerging economies such as China and India, along with the rising investments in renewable energy infrastructure in the region. However, the market also faces challenges such as high initial costs and the availability of alternative solar technologies. Nevertheless, the increasing focus on sustainable energy and the growing demand for solar power are expected to drive the growth of the Thin Film Photovoltaics market in the coming years.

Thin Film Photovoltaics Market Segment Analysis:

Thin Film Photovoltaics Market Segment Analysis:

By Technology,

The copper gallium Selenide (CIGS) Thin Film segment is emerging as the most dominating in the Thin Film Photovoltaics Market. CIGS thin film technology has gained prominence due to its high efficiency, flexibility, and potential for cost reduction in solar module production. Recent developments in the Thin Film Photovoltaics Market within the CIGS segment include advancements in manufacturing processes, innovations in materials, and increased research efforts aimed at improving conversion efficiency and scalability. These developments position CIGS as a leading contender in the thin-film solar technology landscape, contributing to the market's evolution and its role in meeting the growing demand for sustainable and efficient solar energy solutions.

The Thin Film Photovoltaics Market is experiencing continuous advancements across various technologies, including Amorphous Silicon (a-Si) Thin Film, Cadmium Telluride (CdTe) Thin Film, and other emerging technologies like Organic and Perovskite thin films. Ongoing research focuses on enhancing the performance, durability, and cost-effectiveness of thin-film photovoltaic technologies. As the market evolves, the integration of diverse thin-film technologies underscores its pivotal role in shaping the future of solar energy. The collective progress across these segments contributes to the overall growth and innovation within the Thin Film Photovoltaics Market.

Based on Application

The solar Farms segment stands out as the most dominating in the Thin Film Photovoltaics Market. The increasing demand for large-scale solar power generation and the growing trend toward renewable energy sources have propelled the dominance of thin-film photovoltaics especially in solar farm applications. Recent developments in the Thin Film Photovoltaics Market within the Solar Farms segment include advancements in thin-film module efficiency, durability, and manufacturing processes. Innovations in flexible and lightweight thin-film modules have contributed to their widespread adoption in solar farm installations, offering cost-effective solutions and efficient energy conversion. The market's focus on optimizing thin-film technology for large-scale solar projects underscores its pivotal role in driving the transition to sustainable and clean energy sources.

The Thin Film Photovoltaics Market is witnessing continuous progress across diverse applications, including Off-Grid Power Generation, Building-Integrated Photovoltaics (BIPV), Portable Electronics, and other emerging areas. Ongoing research and development initiatives are aimed at expanding the versatility and adaptability of thin-film technology to cater to various energy needs. As the market evolves, the Solar Farms segment, along with advancements in other application areas, collectively contributes to the dynamic growth and innovation within the Thin Film Photovoltaics Market, positioning it as a key player in the global solar energy landscape.

Geography/Region

The Thin Film Photovoltaics market is also segmented based on geography, including North America, Europe, Asia Pacific, Southern America, Middle East and Africa and the Rest of the World. North America and Europe are currently the largest markets for Thin Film Photovoltaics due to the favorable government policies, incentives, and increasing demand for renewable energy. Asia Pacific is expected to witness the highest growth rate during the forecast period due to the increasing population, economic growth, and demand for clean energy.

This includes segmentation based on the power output of the solar panels, which ranges from less than 50 Watts to more than 300 Watts. The power output of the Thin Film Photovoltaics panels depends on various factors such as the size, technology, and efficiency of the solar cells. The power output of Thin Film Photovoltaics panels is generally lower compared to conventional crystalline silicon (c-Si) solar panels.

However, Thin Film Photovoltaics panels have several advantages such as flexibility, lightweight, and low-cost production. Thin Film Photovoltaics panels with lower power output are typically used for small-scale applications such as portable devices and off-grid power systems, while higher power output Thin Film Photovoltaics panels are used for utility-scale applications and grid-connected systems. Thin Film Photovoltaics market segmentation based on the distribution channels is applicable for the sales and marketing of Thin Film Photovoltaics panels. The distribution channels include direct sales, distributors, and e-commerce platforms.

Thin Film Photovoltaics Market Competitive Landscape:

The report identifies some of the key companies in the Thin Film Photovoltaics market, including First Solar, Solar Frontier, Hanergy, MiaSolé, and Sharp Solar. These companies have a significant presence in the Thin Film Photovoltaics market, with a range of products and services aimed at different segments of the market. The report includes the complete internal and external analysis of all such competitors along with the strategies they have recently implemented. Overview of some of the competitors is been mentioned in the following paragraph

First Solar is one of the leading players in the Thin Film Photovoltaics market, with a focus on utility-scale solar projects. The company has a vertically integrated business model, which allows it to control the entire value chain from manufacturing to project development. First Solar's cadmium telluride (CdTe) technology is known for its high efficiency and low cost, making it a popular choice for large-scale solar projects.

Solar Frontier is another major player in the Thin Film Photovoltaics market, with a focus on the residential and commercial rooftop market. The company's copper indium selenium (CIS) technology is known for its high efficiency and ability to perform well under low light conditions. Solar Frontier has a strong presence in the Japanese market and has expanded its operations to Europe, the Middle East, and Africa.

Hanergy is a Chinese company that has made significant investments in Thin Film Photovoltaics technology and has a range of products aimed at different segments of the market. The company's thin-film gallium arsenide (GaAs) technology is known for its high efficiency, but its products are generally higher priced compared to other Thin Film Photovoltaics products. Hanergy has also invested in the development of flexible Thin Film Photovoltaics products, which can be integrated into a range of applications.

MiaSolé is a US-based company that specializes in flexible CIGS (copper indium gallium selenide) Thin Film Photovoltaics products. The company has a range of products aimed at different applications, including building-integrated photovoltaics (BIPV) and portable solar devices. MiaSolé's products are known for their high efficiency and flexibility, making them suitable for a range of applications.

Sharp Solar is a Japanese company that has a range of Thin Film Photovoltaics products aimed at different segments of the market, including utility-scale and residential markets. The company's thin-film amorphous silicon (a-Si) technology is known for its low cost and suitability for large-scale solar projects. Sharp Solar has also invested in the development of BIPV products, which can be integrated into building facades and roofs.

Thin Film Photovoltaics Market Regional Insights:

The Thin Film Photovoltaics market is witnessing significant growth globally, with increasing demand for renewable energy sources and the need to reduce carbon emissions. The report provides a detailed analysis of the Thin Film Photovoltaics market in various regions, including North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa.

The Asia-Pacific region, including China and India, has been the largest market for Thin Film Photovoltaics due to several factors, including favourable government policies and incentives, increasing demand for renewable energy sources, and growing awareness of the benefits of Thin Film Photovoltaics products. China, for example, has set ambitious targets to achieve carbon neutrality by 2060, which is expected to drive the demand for Thin Film Photovoltaics products in the country.

Europe is forecasted to lead the market due to its ambitious renewable energy targets and favourable government policies promoting the adoption of Thin Film Photovoltaics products. The European Union has set a target to achieve a 55% reduction in greenhouse gas emissions by 2030 and become carbon-neutral by 2050. In addition, the EU has launched several initiatives and funding programs to support the adoption of renewable energy sources, including Thin Film Photovoltaics.

European countries have already made significant progress in the adoption of renewable energy sources, with several countries such as Germany, Spain, and Italy leading the way. The favourable regulatory environment, technological advancements, and growing awareness of the benefits of Thin Film Photovoltaics products are expected to further boost the demand for Thin Film Photovoltaics products in the region.

Thin Film Photovoltaics Market Scope: Inquire before buying

Thin Film Photovoltaics Market Scope: Inquire before buying

| Global Thin Film Photovoltaics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 12.96 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 9.1% | Market Size in 2030: | US $ 26.64 Bn. |

| Segments Covered: | By Technology | Amorphous Silicon (a-Si) Thin Film Cadmium Telluride (CdTe) Thin Film Copper Indium Gallium Selenide (CIGS) Thin Film Others (Organic, Perovskite, etc.) |

|

| By Application | Solar Farms Off-Grid Power Generation Building-Integrated Photovoltaics (BIPV) Portable Electronics Others |

||

| By End-User | Residential Commercial Industrial Others |

||

Thin Film Photovoltaic Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

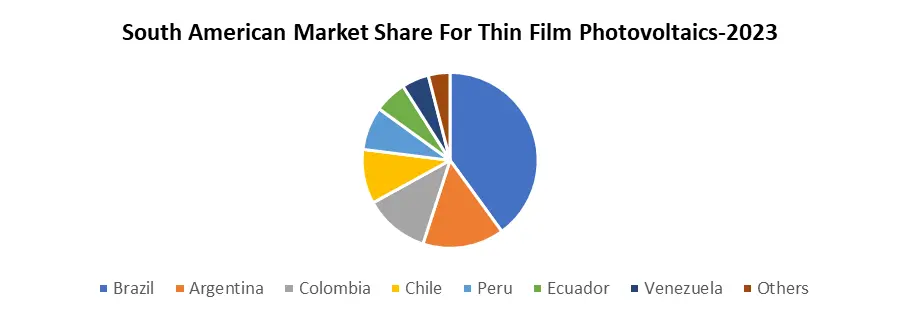

South America (Brazil, Argentina Rest of South America)

Thin Film Photovoltaic Market Key Players are:

1. First Solar, Inc.(USA)

2. Hanergy Thin Film Power Group Ltd. (China)

3. Solar Frontier K.K. (Japan)

4. Kaneka Corporation (Japan)

5. MiaSolé Hi-Tech Corp. (USA)

6. Sharp Corporation (Japan)

7. Trony Solar Holdings Co. Ltd. (China)

8. Ascent Solar Technologies, Inc. (USA)

9. Stion Corporation (USA)

10. AVANCIS GmbH & Co. KG (Germany)

11. NexPower Technology Corp. (Taiwan)

12. Xunlight Kunshan Co., Ltd. (China)

13. United Solar Ovonic LLC (USA)

14. Solarion AG (Germany)

15. Flisom AG (Switzerland)

16. Heliatek GmbH (Germany)

17. Nanosolar Inc. (USA)

18. Moser Baer Solar Limited (India)

19. T-Solar Global S.A. (Spain)

20. Global Solar Energy Inc. (USA)

21. Hyundai Heavy Industries Green Energy Co., Ltd. (South Korea)

22. Sunflare (USA)

23. SoloPower Systems, Inc. (USA)

24. Bosch Solar CISTech GmbH (Germany)

25. DUNMORE Corporation (USA)

26. ISET (South Korea)

27. Siva Power (USA)

FAQs

1] What is the growth rate of the Thin Film Photovoltaic Market?

Ans. The Global Thin Film Photovoltaic Market is growing at a significant rate of 9.1 % over the forecast period.

2] Which region is expected to dominate the Thin Film Photovoltaic Market?

Ans. North America region is expected to dominate the Thin Film Photovoltaic Market over the forecast period.

3] What is the expected Global Thin Film Photovoltaic Market size by 2030?

Ans. The market size of the Thin Film Photovoltaic Market is expected to reach USD 26.64 Billion by 2030.

4] Who are the top players in the Thin Film Photovoltaic Market?

Ans. The major key players in the Global Thin Film Photovoltaic Market are Archer Daniels Midland Company, Arla Foods Amba, Kerry Group PLC, Saputo, Inc., Fonterra Co-operative Group Limited, and Royal Frieslandcampina N.V., Schreiber Foods, Inc.

5] Which factors are expected to drive the Thin Film Photovoltaic Market growth by 2029?

Ans. A major driver for the global Thin Film Photovoltaic market is the need for infant formula for newborns and babies who are in the pre or early weaning age.