Polycarbonate Resins Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

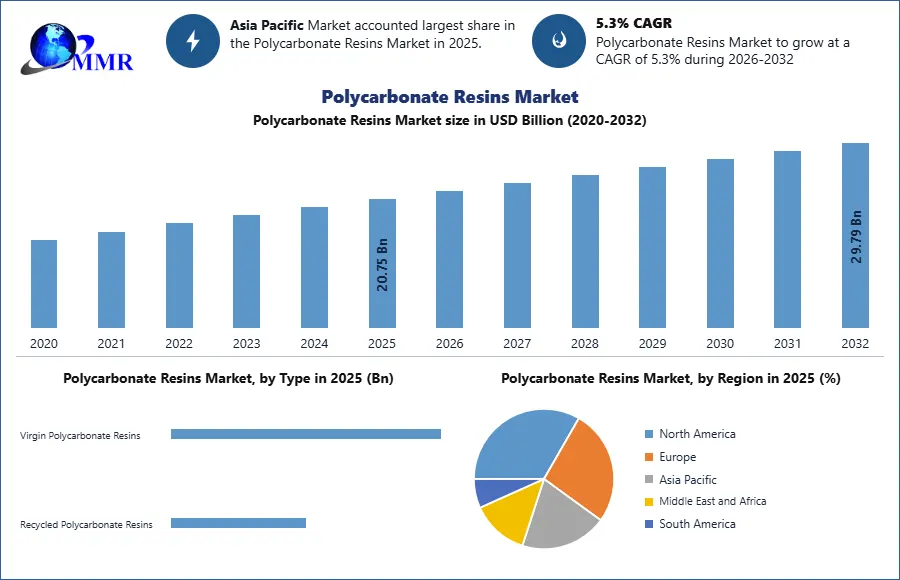

Polycarbonate Resins Market size is expected to reach nearly USD 20.75 Bn. by 2032 with the CAGR of 5.3% during the forecast period.

To Know About The Research Methodology :- Request Free Sample Report

The Polycarbonate Resins Market represents a dynamic sector in the global materials industry, focusing on the development and application of polycarbonate resins that offer superior durability, impact resistance, and optical clarity. Polycarbonate resins are widely used in applications across automotive, electrical & electronics, construction, medical devices, packaging, and optical products. The key growth factors driving the market include advancements in material technologies that offer enhanced properties, such as UV resistance, high-temperature stability, and flame retardancy. With the growing demand for lightweight and energy-efficient materials in industries like automotive and electronics, polycarbonate resins are increasingly being used to replace traditional materials like glass and metals.

Technological developments in the form of recycling technologies and bio-based polycarbonates are also contributing to market growth, as sustainability becomes a key consideration for manufacturers and consumers. The demand outlook remains strong, with the continuous expansion of industries like automotive, particularly electric vehicles (EVs), and electronics. The regulatory environment surrounding emissions, energy efficiency, and sustainability also plays a crucial role in fostering the adoption of polycarbonate resins, which are essential for producing high-performance, lightweight components.

The outlook for the Polycarbonate Resins Market is positive, with ongoing innovation and rising demand across key end-use industries expected to sustain growth through 2032. As market players continue to invest in innovation, efficiency, and sustainability, the market is poised for continued expansion globally.

Polycarbonate Resins Market Dynamics:

Polycarbonate Resins Market Drivers

Technological Advancements in Polycarbonate Resins Production

The market for polycarbonate resins is significantly driven by technological advancements in resin production. With innovations that enhance the chemical properties of polycarbonate resins, manufacturers are now able to meet the growing demand for high-performance applications in automotive, medical, and electronics sectors. For example, the development of flame-retardant polycarbonate resins has enhanced the safety features of automotive parts and electrical equipment. Furthermore, innovations like the introduction of bio-based polycarbonate resins contribute to the environmental appeal of these materials, making them more sustainable. These advancements not only improve performance but also reduce the environmental footprint of manufacturing processes, thereby encouraging industry adoption.

Growth in Automotive and Electronics Industries

The increasing demand for lightweight, durable, and energy-efficient materials in automotive and electronics is one of the primary drivers of the polycarbonate resins market. In the automotive sector, polycarbonate resins are extensively used in producing components such as headlamps, windows, and dashboards, thanks to their high impact resistance and ability to withstand extreme temperatures. The rise of electric vehicles (EVs) further accelerates the demand for polycarbonate resins, as manufacturers strive to reduce the weight of vehicles for improved fuel efficiency. In electronics, polycarbonate resins are used for housings, connectors, and displays, where high optical clarity and electrical insulating properties are crucial.

Regulatory Support and Standards

Government regulations aimed at reducing emissions and improving fuel efficiency have accelerated the use of polycarbonate resins in various industries. Regulatory frameworks, such as the European Union's REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) regulation, ensure that manufacturers meet stringent environmental and safety standards, further driving the demand for polycarbonate resins in automotive, construction, and packaging sectors. Furthermore, the increasing focus on sustainability and the promotion of recycled and bio-based polycarbonate resins are gaining traction due to policy support in Europe, North America, and Asia.

Polycarbonate Resins Market Restraints

High Production Costs

Polycarbonate resins are relatively expensive to produce, primarily due to the costs associated with the raw materials and energy-intensive manufacturing processes. This high cost of production limits the widespread adoption of polycarbonate resins in cost-sensitive industries. Moreover, the need for specialized machinery and skilled labor to produce high-quality polycarbonate resins further adds to the overall production cost, limiting their application in industries with tight cost margins, such as the mass-market consumer goods sector.

Regulatory Challenges

The stringent regulatory requirements for polycarbonate resins, especially in terms of sustainability and environmental impact, create challenges for manufacturers. Polycarbonate resins must comply with various regional regulations concerning emissions, recycling, and waste management. For example, compliance with the European Union's REACH regulation necessitates significant investment in research and development to ensure that resins meet the required safety standards. These regulatory challenges not only increase production costs but also restrict the adoption of polycarbonate resins in some regions.

Supply Chain Disruptions

Polycarbonate resin production relies on a complex global supply chain, including the procurement of raw materials such as bisphenol-A (BPA) and phosgene. Disruptions in the supply chain, caused by factors such as geopolitical tensions, raw material shortages, or global pandemics, can lead to price fluctuations and production delays. Such disruptions pose a risk to the stability of polycarbonate resin supply and can negatively impact manufacturers' ability to meet demand, especially in fast-growing sectors like automotive and electronics.

Polycarbonate Resins Market Opportunities

Emerging Markets

As economies in Asia-Pacific, Latin America, and the Middle East continue to grow, new market opportunities are arising for polycarbonate resins. Developing countries in these regions are experiencing rapid urbanization and industrialization, creating significant demand for durable and high-performance materials in construction, automotive, and consumer electronics. These emerging markets offer lucrative growth prospects for polycarbonate resin manufacturers, particularly those offering sustainable and cost-effective solutions tailored to the specific needs of these regions.

Innovation in Resin Formulations

There is an increasing opportunity for polycarbonate resin manufacturers to innovate by developing new resin formulations to meet the evolving demands of industries such as automotive, medical devices, and electronics. For example, the development of polycarbonate resins with enhanced UV resistance, optical clarity, and flame retardancy could unlock new applications in high-performance sectors. Additionally, the continued evolution of biopolycarbonate resins presents an opportunity for manufacturers to cater to the growing consumer preference for sustainable, eco-friendly materials.

Strategic Investments in Sustainability

Polycarbonate resin manufacturers have an opportunity to capitalize on the growing demand for sustainable materials by investing in the development of recycled and bio-based polycarbonates. This trend aligns with the increasing consumer and regulatory demand for greener alternatives. Manufacturers that invest in sustainable production technologies and commit to the use of recycled or bio-based raw materials are likely to benefit from a competitive advantage, particularly as sustainability becomes a key factor in purchasing decisions across multiple industries.

Polycarbonate Resins Market Segment Analysis:

Polycarbonate Resins Market Segmentation, by Type

The Virgin Polycarbonate Resins segment dominated the Polycarbonate Resins Market in 2025, primarily due to the high demand for premium-quality, high-performance resins in industries such as automotive, medical, and electronics. Virgin polycarbonate resins are preferred for applications that require the highest level of durability, optical clarity, and impact resistance. These resins are especially valued in the automotive sector for parts such as headlamps, windshields, and interior panels, as they offer superior strength and resilience. The demand for virgin polycarbonate resins has been bolstered by the automotive industry's shift towards lightweight materials for improving fuel efficiency.

The Recycled Polycarbonate Resins segment is also experiencing significant growth, driven by the increasing focus on sustainability and the adoption of circular economy principles. Recycled polycarbonate resins are used in a variety of applications, including packaging, construction, and consumer goods. The demand for recycled resins is expected to grow as both manufacturers and consumers prioritize sustainability. Recycling technologies have advanced, making it possible to produce high-quality polycarbonate resins from post-consumer waste, which is helping to drive this segment’s growth.

Polycarbonate Resins Market Segmentation, by Grade

The High-Flow Polycarbonate Resins segment was the largest in 2025, driven by the increasing adoption of polycarbonate resins in industries requiring fast injection molding and high productivity. High-flow resins are particularly valuable in the manufacturing of automotive parts, electrical devices, and consumer goods, where speed and efficiency are crucial in production processes. The ability of high-flow resins to quickly fill molds and produce complex shapes makes them ideal for use in injection molding applications, which is a significant growth driver.

The Medium-Flow Polycarbonate Resins segment holds a significant share of the market due to its balanced properties of ease of processing and strength. These resins are commonly used in automotive interior applications, optical products, and medical devices, where both mechanical strength and processing ease are required. Medium-flow resins provide good clarity and can be molded into parts with high dimensional accuracy, making them essential for industries that require precision.

The Low-Flow Polycarbonate Resins segment is comparatively smaller but still plays a vital role in the production of high-strength components that need to withstand demanding conditions. These resins are particularly used in industries such as construction, where strength and durability are prioritized over processing speed. Although the demand for low-flow resins is lower than that for high-flow resins, they remain essential in specific heavy-duty applications.

Polycarbonate Resins Market Segmentation, by Product Type

The Sheets segment was the largest in 2025, driven by the widespread use of polycarbonate sheets in construction, automotive, and electronics industries. Polycarbonate sheets are known for their high impact resistance, optical clarity, and ability to withstand high temperatures, making them ideal for use in building and construction applications such as skylights, roofing, and protective glazing. The versatility of polycarbonate sheets is a major factor behind their dominance in the market, as they can be fabricated into different sizes and thicknesses to meet specific requirements.

The Films segment is experiencing growing demand, particularly in the electronics industry, where polycarbonate films are used in displays, touch panels, and protective films for screens. Polycarbonate films offer excellent clarity and resistance to scratching and UV degradation, making them ideal for high-quality electronic applications. The increasing use of polycarbonate films in the packaging industry, especially for durable and transparent packaging, is also contributing to the growth of this segment.

The Granules segment is important for manufacturers who produce polycarbonate resins in bulk and then mold or extrude them into the desired shapes and sizes. Polycarbonate granules are primarily used in injection molding applications and are essential in the production of automotive components, electrical parts, and consumer goods. This segment's demand is largely driven by the high volume of production required for industries such as automotive, consumer electronics, and medical devices.

The Blends segment is a niche yet growing area in the Polycarbonate Resins Market, with increasing adoption in industries such as automotive and construction. Polycarbonate blends are created by combining polycarbonate with other resins to enhance specific properties, such as impact resistance, flame retardancy, and UV stability. These blends are ideal for applications that require improved material performance under harsh environmental conditions.

Polycarbonate Resins Market Regional Insights:

Polycarbonate Resins Market Regional Analysis

North America was the leading region in 2025, driven by significant industrial growth, policy support, and technology leadership. The United States, in particular, exhibited dominance in the Polycarbonate Resins Market, bolstered by a strong automotive industry, a growing demand for lightweight materials, and regulatory support for sustainability. The U.S. market was further supported by infrastructure investments in electric vehicles and the increasing adoption of polycarbonate resins in automotive, medical, and electronics applications. North America's strong focus on innovation, coupled with government policies encouraging the use of sustainable materials, made it the dominant region in 2025.

Recent Development

January 2025: SABIC launched a new line of sustainable polycarbonate resins designed to meet the growing demand for eco-friendly materials in automotive and electronics.

March 2025: Covestro AG announced a partnership with a major automotive manufacturer to supply polycarbonate resins for lightweight vehicle components, focusing on electric vehicle applications.

June 2025: LG Chem expanded its polycarbonate resin production capacity in North America to meet the growing demand for materials in the automotive and electronics industries.

Polycarbonate Resins Market Scope: Inquire before buying

| Polycarbonate Resins Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 20.75 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.3% | Market Size in 2032: | 29.79 USD Billion |

| Segments Covered: | by Type | Virgin Polycarbonate Resins Recycled Polycarbonate Resins |

|

| by Grade | Low-Flow Medium-Flow High-Flow |

||

| by Product Type | Sheets Films Granules Blends |

||

| by Process | Injection Molding Extrusion Blow Molding |

||

| by End-Use Industry | Automotive & Transportation Electronics & Electrical Construction & Building Consumer Goods Others |

||

Polycarbonate Resins Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players/Competitors Profiles Covered in the Polycarbonate Resins Market Report in Strategic Perspective

- SABIC

- Covestro AG

- LG Chem

- Mitsubishi Engineering-Plastics Corporation

- Trinseo S.A.

- Chi Mei Corporation

- Teijin Limited

- Sumitomo Chemical Company

- DIC Corporation

- Polymaker

- Lanxess AG

- BASF SE

- Eastman Chemical Company

- SABIC Innovative Plastics

- Toray Industries

- Asahi Kasei Corporation

- Royal DSM N.V.

- Borealis AG

- Solvay Group

- Evonik Industries

- Repsol

- Indorama Ventures

- DSM Engineering Materials

- Saudi Basic Industries Corporation

- Celanese Corporation